Global Semiconductor Chips Market Outlook to 2030

Region:Global

Author(s):Shreya Garg

Product Code:KROD9174

Region:Global

Author(s):Shreya Garg

Product Code:KROD9174

December 2024

88

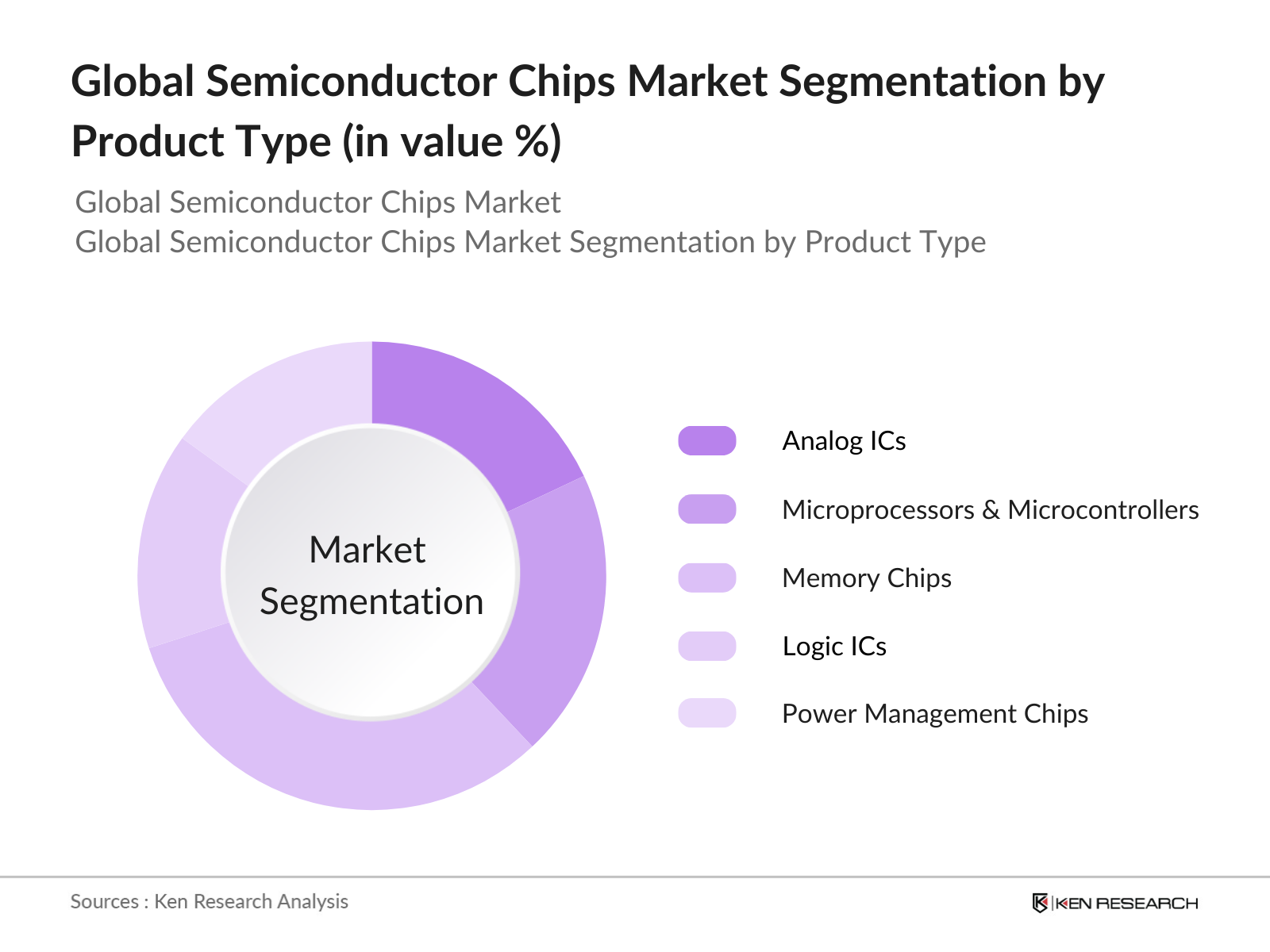

By Product Type: The market is segmented by product type into analog ICs, microprocessors and microcontrollers, memory chips, logic ICs, and power management chips. Memory Chips dominate the product type segment, particularly DRAM and flash memory, driven by growing demand from data centers, smartphones, and personal computing devices. As cloud computing and big data applications expand, the need for larger storage capacities has grown, which is fueling the market for memory chips.

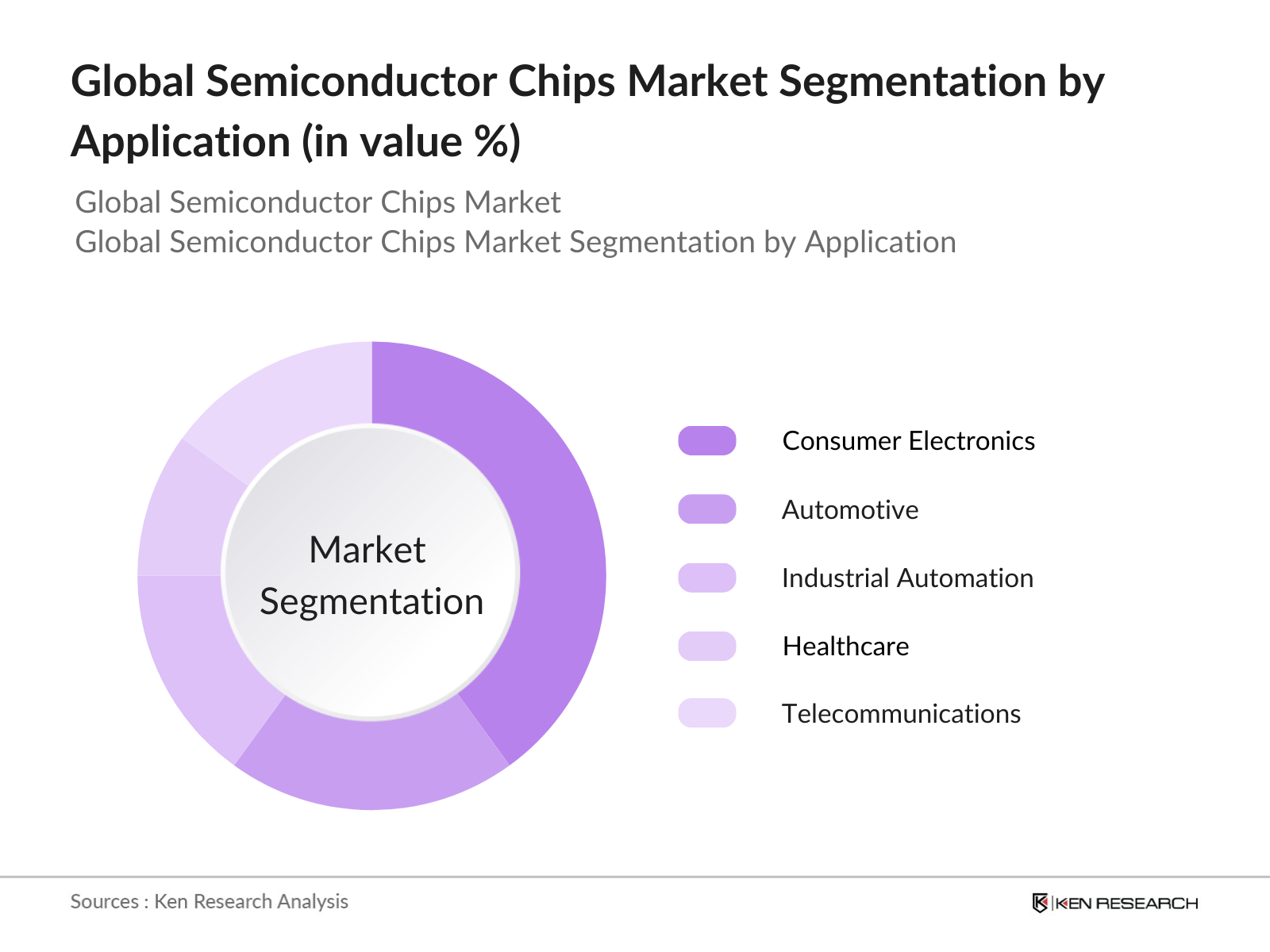

By Application: The market is segmented by application into consumer electronics, automotive, industrial automation, healthcare, and telecommunications. Consumer Electronics is the largest application segment, accounting for a significant share of the market. This dominance is due to the ubiquity of smartphones, laptops, and wearable devices, all of which require semiconductor chips to function. Additionally, the growing trend of smart homes and connected devices continues to fuel the demand for semiconductors in this segment.

The global semiconductor chips market is dominated by a few major players, including TSMC, Samsung, Intel, and other leading fabless firms. This consolidation highlights the significant influence of these key companies in driving innovation, setting industry standards, and meeting the ever-increasing demand for semiconductors in various applications such as consumer electronics, automotive, and telecommunications.

|

Company Name |

Year Established |

Headquarters |

R&D Investment |

Revenue (USD Bn) |

Number of Patents |

Fab Locations |

Strategic Initiatives |

Market Share |

|

Taiwan Semiconductor Manufacturing Company (TSMC) |

1987 |

Hsinchu, Taiwan |

||||||

|

Samsung Electronics |

1969 |

Suwon, South Korea |

||||||

|

Intel Corporation |

1968 |

Santa Clara, U.S. |

||||||

|

Qualcomm |

1985 |

San Diego, U.S. |

||||||

|

Broadcom Inc. |

1991 |

San Jose, U.S. |

The global semiconductor chips market is expected to show substantial growth over the next few years. Factors driving this growth include continuous advancements in semiconductor technology, increasing demand for AI and IoT applications, and the rollout of 5G infrastructure globally. Additionally, the automotive sector's transition toward electric and autonomous vehicles will further accelerate the demand for semiconductor chips, particularly in areas like power management and sensor technologies.

|

Product Type |

Analog ICs Microprocessors Memory Chips Logic ICs Power Management Chips |

|

Application |

Consumer Electronics Automotive Industrial Automation Healthcare, Telecommunications |

|

Technology |

CMOS Technology FinFET SOIEUV Lithography Quantum Dot Technology |

|

Material |

Silicon Gallium Nitride Silicon Carbide Germanium Sapphire |

|

Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size (Wafer Production, IC Design)

2.2 Year-On-Year Growth Analysis (Unit Shipments, Revenue Growth)

2.3 Key Market Developments and Milestones (Technological Advancements, Major Investments)

3.1 Growth Drivers

3.1.1 Increase in IoT Devices

3.1.2 Growth in AI and Machine Learning Adoption

3.1.3 Expanding 5G Infrastructure

3.1.4 Automotive Electrification

3.2 Market Challenges

3.2.1 Supply Chain Disruptions (Raw Materials Shortage)

3.2.2 High R&D Costs

3.2.3 Geopolitical Tensions Impacting Trade

3.2.4 Environmental Regulations (E-waste Management)

3.3 Opportunities

3.3.1 Advancements in Chip Miniaturization (3nm Technology)

3.3.2 Growth in Quantum Computing Applications

3.3.3 Increasing Demand for High-Performance Computing (HPC)

3.3.4 Expansion of Semiconductor Manufacturing in Emerging Markets

3.4 Trends

3.4.1 Rising Demand for Custom Chips (ASICs, SoCs)

3.4.2 Increased Usage of Advanced Packaging (Fan-out Wafer Level Packaging)

3.4.3 Growth in AI Chips and Neuromorphic Computing

3.4.4 Surge in Usage of Gallium Nitride (GaN) and Silicon Carbide (SiC) for Power Electronics

3.5 Government Regulation

3.5.1 Semiconductor Trade Policies (Tariffs, Export Controls)

3.5.2 Incentives for Local Semiconductor Manufacturing (CHIPS Act)

3.5.3 Environmental Standards for Chip Production

3.5.4 Public-Private Partnerships for Semiconductor Research

3.6 SWOT Analysis

3.7 Stake Ecosystem (Foundries, IDM, Fabless Firms)

3.8 Porters Five Forces (Supplier Power, Buyer Power, Competition Intensity)

3.9 Competition Ecosystem (Fabless vs Integrated Firms)

4.1 By Product Type (In Value %)

4.1.1 Analog ICs

4.1.2 Microprocessors and Microcontrollers

4.1.3 Memory Chips (DRAM, Flash)

4.1.4 Logic ICs (ASICs, FPGAs)

4.1.5 Power Management Chips

4.2 By Application (In Value %)

4.2.1 Consumer Electronics (Smartphones, PCs)

4.2.2 Automotive (ADAS, EVs)

4.2.3 Industrial Automation

4.2.4 Healthcare (Medical Devices, Wearables)

4.2.5 Telecommunications (5G Infrastructure, Data Centers)

4.3 By Technology (In Value %)

4.3.1 CMOS Technology

4.3.2 FinFET Technology

4.3.3 SOI Technology

4.3.4 EUV Lithography

4.3.5 Quantum Dot Technology

4.4 By Material (In Value %)

4.4.1 Silicon (Si)

4.4.2 Gallium Nitride (GaN)

4.4.3 Silicon Carbide (SiC)

4.4.4 Germanium

4.4.5 Sapphire

4.5 By Region (In Value %)

4.5.1 North America

4.5.2 Europe

4.5.3 Asia-Pacific

4.5.4 Latin America

4.5.5 Middle East & Africa

5.1 Detailed Profiles of Major Companies

5.1.1 Intel Corporation

5.1.2 Samsung Electronics

5.1.3 Taiwan Semiconductor Manufacturing Company (TSMC)

5.1.4 Broadcom Inc.

5.1.5 Qualcomm Technologies Inc.

5.1.6 NVIDIA Corporation

5.1.7 Advanced Micro Devices, Inc. (AMD)

5.1.8 Micron Technology, Inc.

5.1.9 Texas Instruments Incorporated

5.1.10 SK Hynix Inc.

5.1.11 STMicroelectronics N.V.

5.1.12 Infineon Technologies AG

5.1.13 MediaTek Inc.

5.1.14 ON Semiconductor

5.1.15 NXP Semiconductors N.V.

5.2 Cross Comparison Parameters (Number of Employees, Revenue, Headquarters, Market Share, Manufacturing Capabilities, R&D Spending, Fab Location, IP Portfolio)

5.3 Market Share Analysis (Top Players Market Share)

5.4 Strategic Initiatives (Collaborations, Product Launches, Market Expansions)

5.5 Mergers And Acquisitions

5.6 Investment Analysis (CapEx, FDI in Semiconductor Industry)

5.7 Venture Capital Funding in Semiconductor Startups

5.8 Government Grants and Subsidies for Semiconductor Manufacturing

5.9 Private Equity Investments in Chip Firms

6.1 Semiconductor Manufacturing Compliance (ISO Certifications, Environmental Regulations)

6.2 Export Control Policies (U.S. Export Administration Regulations)

6.3 Global Standards for Semiconductor Chips (JEDEC Standards)

6.4 Regional Policies (Europe's Chips Act, Chinas Five-Year Plan)

7.1 Future Market Size Projections (By Value and Volume)

7.2 Key Factors Driving Future Market Growth (Emerging Applications, New Chip Architectures)

8.1 By Product Type (In Value %)

8.2 By Application (In Value %)

8.3 By Technology (In Value %)

8.4 By Material (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis (Total Addressable Market, Serviceable Available Market)

9.2 Customer Cohort Analysis (Key End-User Segments)

9.3 Marketing Initiatives (Brand Positioning, Go-to-Market Strategies)

9.4 White Space Opportunity Analysis (Unexplored Applications, New Markets)

Disclaimer Contact UsIn the first stage, we identified critical variables influencing the global semiconductor chips market. This involved constructing an ecosystem map of major stakeholders, including manufacturers, raw material suppliers, and end-user industries. Extensive secondary research from proprietary databases and public sources was used to collect this information.

We compiled historical data on market penetration rates, production output, and revenue generation across different semiconductor product categories. This was followed by an analysis of the key demand drivers, such as growth in the IoT and automotive sectors.

Market hypotheses were validated through interviews with industry experts and key market players, providing real-world insights into product segments and financial trends. We conducted surveys and computer-assisted telephone interviews (CATIs) to gain operational insights directly from industry practitioners.

In the final step, we synthesized the data from multiple sources and consultations to verify the findings. This ensured that the market analysis was both comprehensive and validated by industry stakeholders, providing a highly reliable output for decision-makers.

The global semiconductor chips market is valued at USD 640 billion, driven by demand from consumer electronics, automotive applications, and industrial automation.

Challenges in the global semiconductor chips market include supply chain disruptions, high R&D costs, geopolitical tensions, and environmental regulations related to chip production.

Key players in the global semiconductor chips market include TSMC, Samsung, Intel, Qualcomm, and Broadcom, dominating due to advanced manufacturing technologies, extensive R&D investments, and strong partnerships.

The global semiconductor chips market is driven by the increasing adoption of AI, 5G, IoT devices, and the electrification of vehicles, which have significantly expanded the demand for semiconductor chips.

Future trends in the global semiconductor chips market include the development of advanced chip architectures such as 3nm technology, increased demand for AI and quantum computing chips, and the use of advanced packaging solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.