Global Semiconductor Market Outlook to 2030

Region:Global

Author(s):Rohit and Shashank

Product Code:KENGR028

October 2024

92

About the Report

Global Semiconductor Market Overview

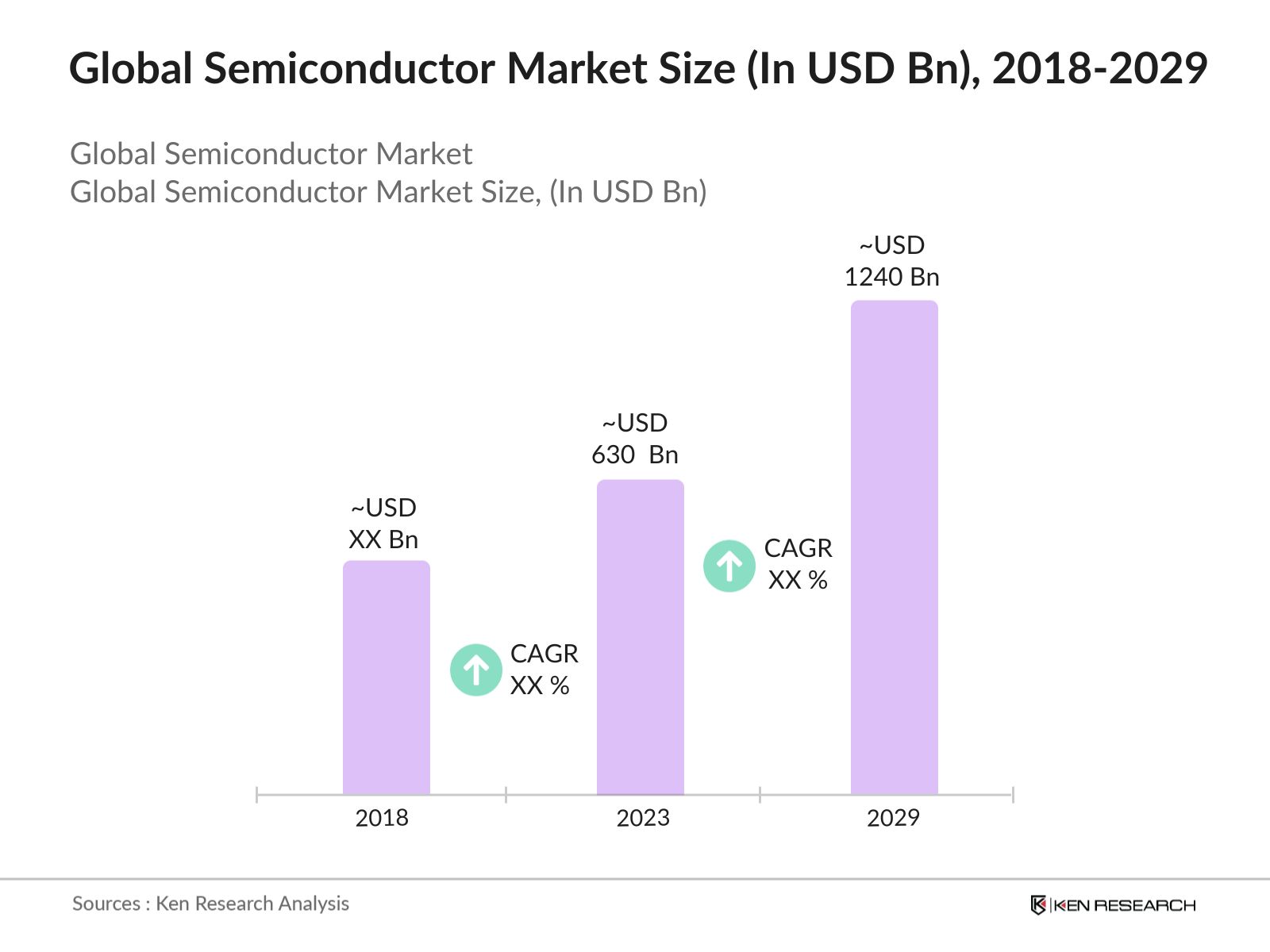

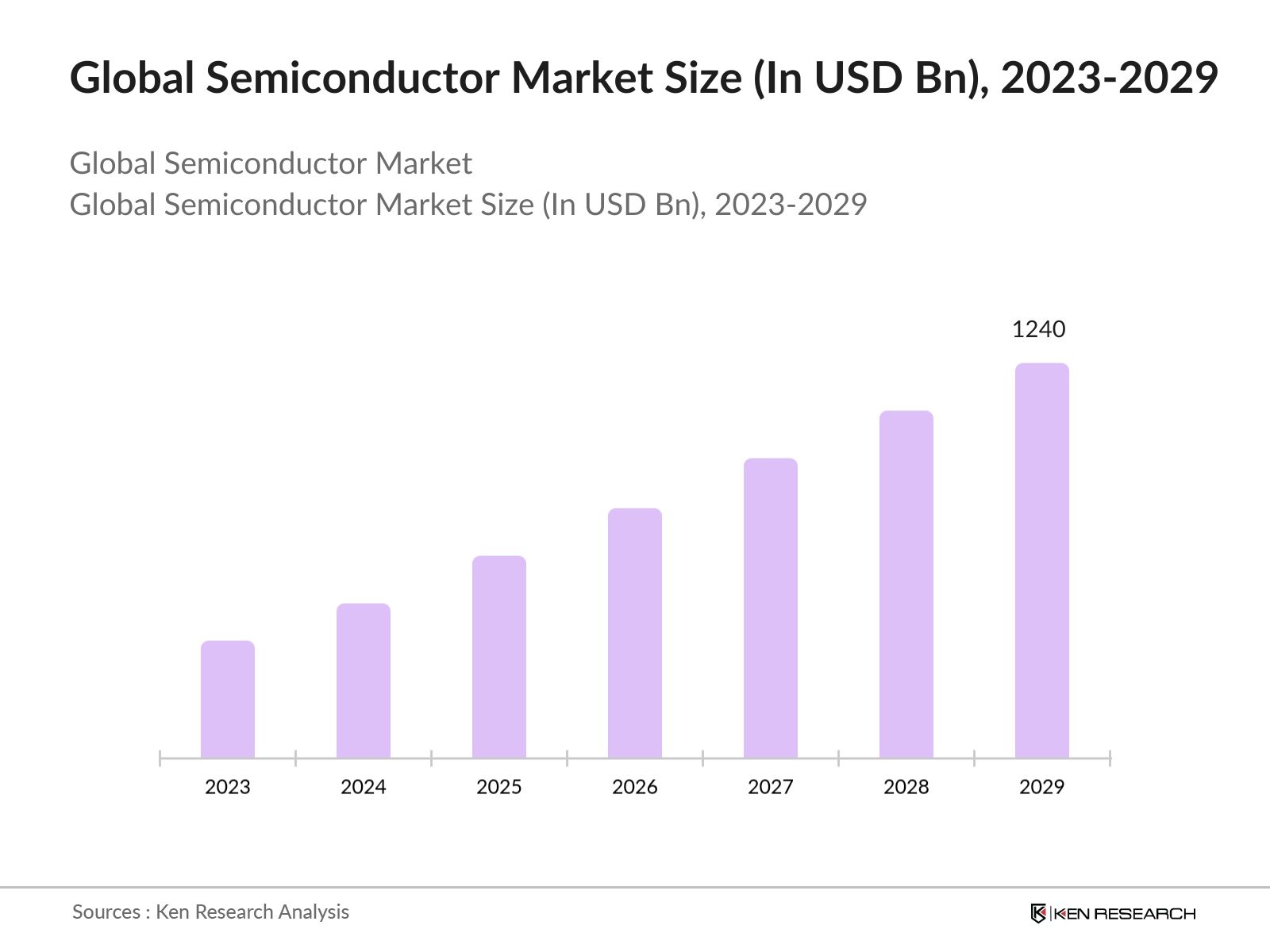

- In 2023, global semiconductor market was estimated at USD 630 Bn and is forecasted to reach a market size of USD 1240 Bn in 2029 driven by Electrification of transportation and the growth of the electric vehicle industry, increasing prevalence of wireless and portable electronics, and demand for specialized semiconductors in emerging technologies.

- The market is highly fragmented with prominent players in the market including Samsung Semiconductors, Taiwan Semiconductor Manufacturing Company Limited (TSMC), Intel Corporation, Qualcomm Incorporated, and SK Hynix Inc.

- In March 2022, Air Liquide S.A., a global leader in gases, technologies, and services for industry and health, announced a substantial investment of 318 million euros to establish four new production units in Japan. This strategic investment is aimed at strengthening Air Liquide's presence in the Japanese market and enhancing its production capabilities to meet the growing demand for industrial gases.

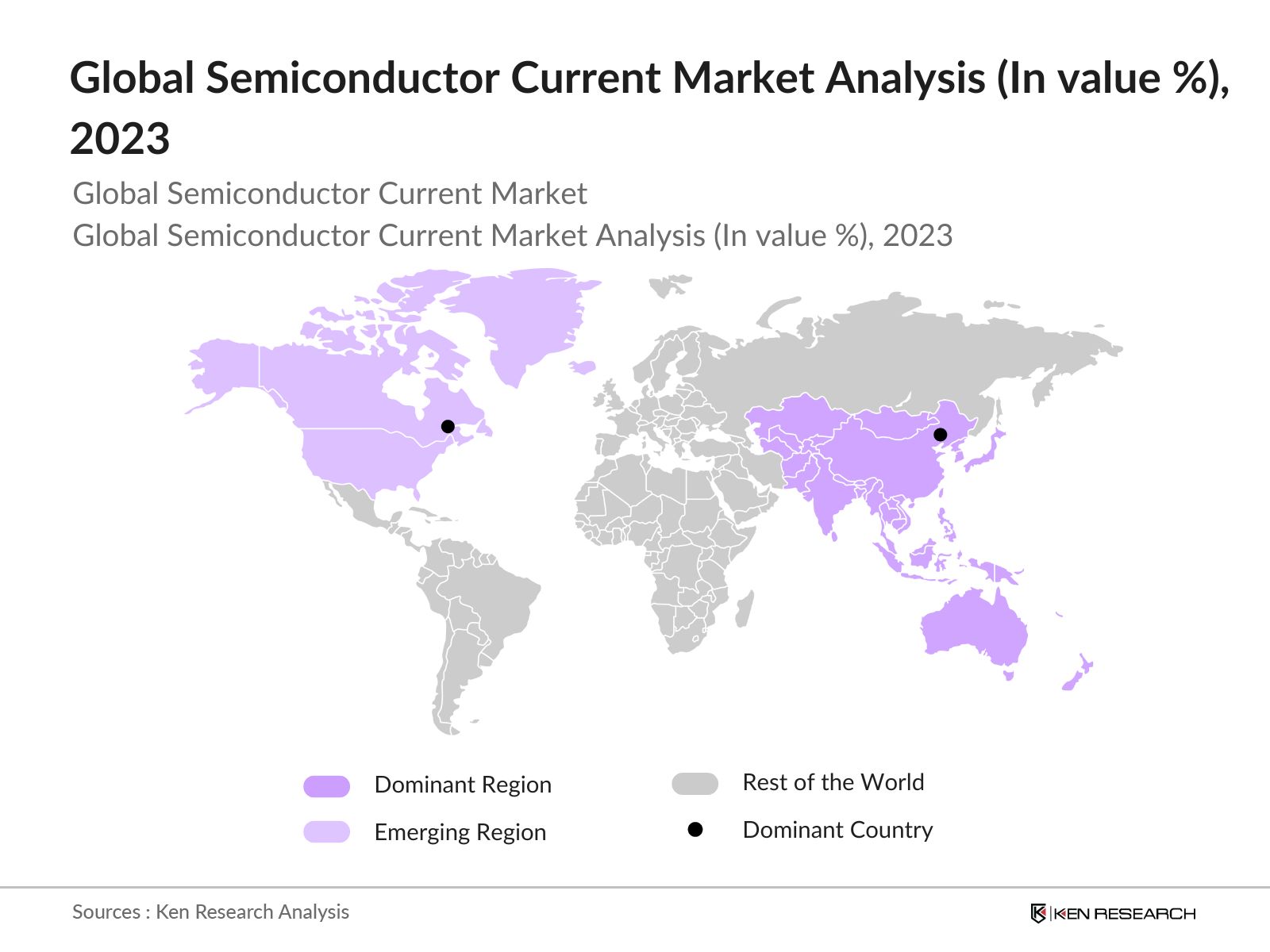

Global Semiconductor Current Market Analysis

- APAC as dominant region: The Asia-Pacific region consistently maintains its leading market share due to its manufacturing dominance, notably driven by China, Japan, South Korea and Taiwan as pivotal manufacturing hubs for semiconductor chips.The South Korean government plans to invest USD 450 billion over the next decade to establish a robust semiconductor supply chain, aiming to solidify its position as a global leader in the industry.Additionally, in 2023, China has launched its largest state-backed investment fund, amounting to USD 47.5 billion. This fund is part of a broader strategy to enhance domestic chip production amidst increasing US export restrictions.

- North America as emerging region: North America is poised to be the next emerging region in the market due to its advanced technological infrastructure, strong economic growth, and investment in research and development.Additionally, the economic stability and favorable business environments in the United States and Canada also encourage investment and market expansion. In 2023, the CHIPS and Science Act allocates a total of USD 52.7 billion to bolster semiconductor production in the U.S., with USD 11 billion specifically earmarked for R&D initiatives. This includes a USD 5 billion investment to establish the National Semiconductor Technology Center (NSTC).

- China as dominant country: China is the largest country in APAC region owing to its growing manufacturing industry, advanced technological innovations in areas such as telecommunications, artificial intelligence, and e-commerce, and infrastructure development.In 2022, about USD 49.7 billion of FDI (Foreign Direct Investment) was invested into the manufacturing sector in China. Additionally, in 2023, China's total output of integrated circuits (ICs) reached 351.4 billion units, marking a 6.9% increase from the previous year, when the output was 324.2 billion units.Further, China's extensive infrastructure development and strong trade and export capabilities, being the world's largest exporter, further solidify its dominant position in the APAC region.

Global Semiconductor Market Segmentation

The Global Semiconductor Market can be segmented based on several factors:

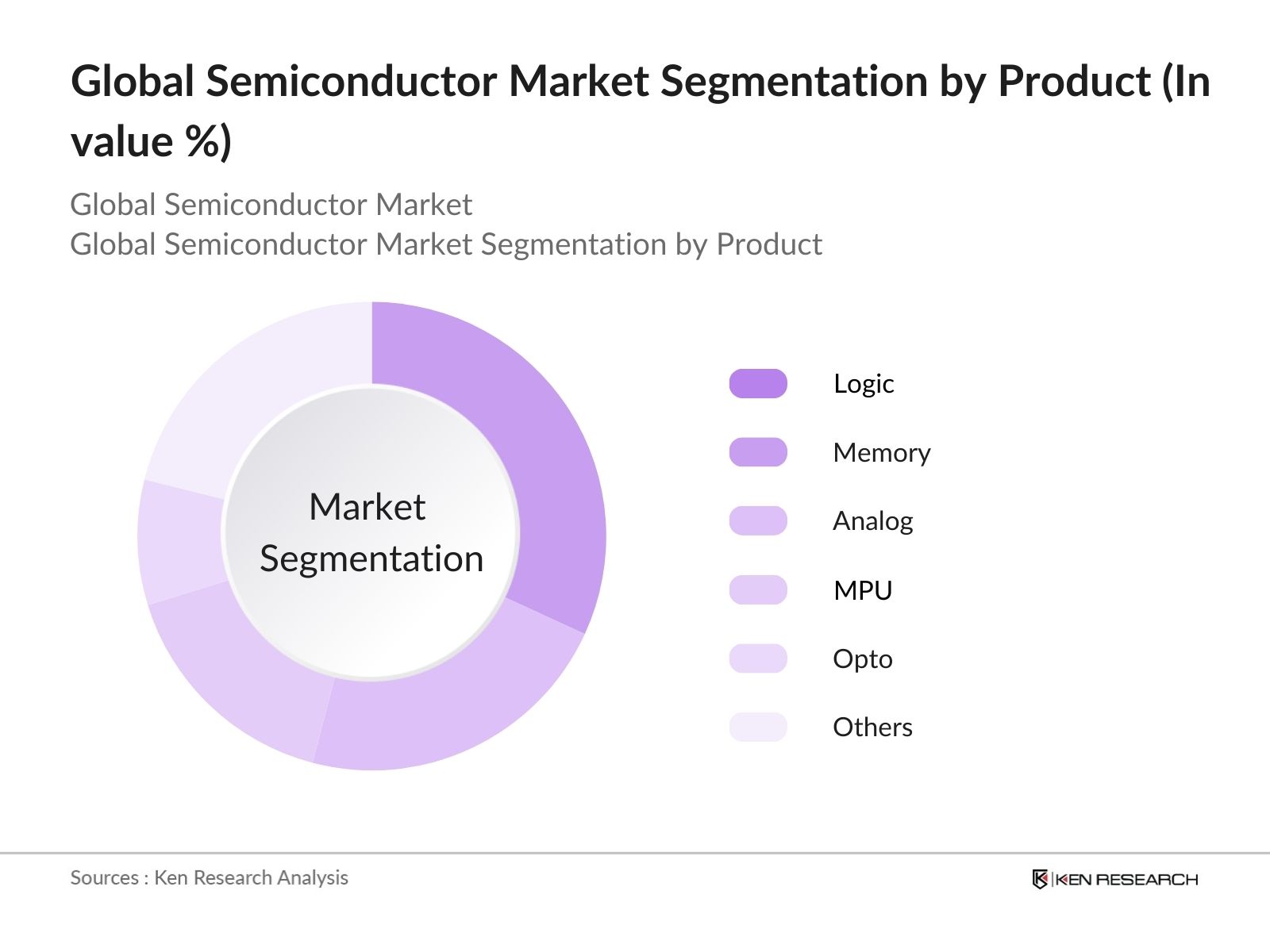

- By Product: The global semiconductor market's segmentation by product includes Logic, Memory, Analog, MPU, Opto, Discretes, MCU, Sensors, and DSP. In 2023, the Logic segment led the market due to its critical role in processing data and executing instructions across various devices. The increasing demand for high-performance computing in smartphones, personal computers, and data centers propelled Logic semiconductors to the forefront, making them the dominant segment in the global semiconductor market.

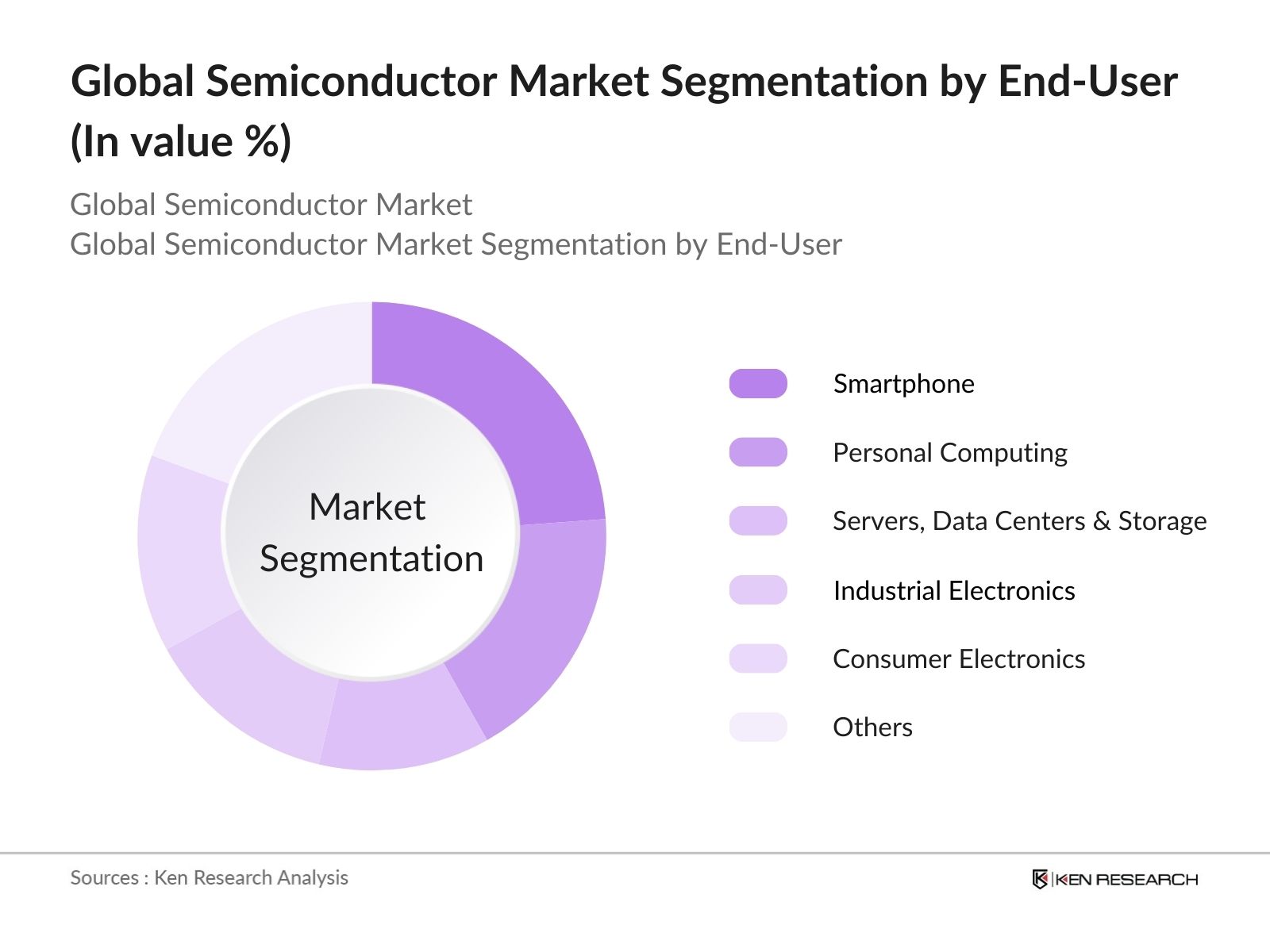

- By End-User: The global semiconductor market's segmentation by end-user includes smartphone, personal computing, servers, data centers & storage, industrial electronics, consumer electronics, automotive, wired/wireless infrastructure (networking), and others. In 2023, the Smartphone segment led the market owing to the rapid proliferation of smartphones and the continuous advancements in smartphone technology. The increasing adoption of 5G technology and the demand for high-performance, energy-efficient chips significantly boosted the semiconductor market in the smartphone segment.

- By Nodal Size: The global semiconductor market's segmentation by nodal size includes 5 nm, 7/5 nm, 10/7 nm, 16/14 nm, 22/20 nm, 32/28 nm, 45/40 nm, 65 nm, 90 nm, 130 nm, and 180 nm. In 2023, the 7/5 nm segment dominated the market due to its advanced technology, offering higher performance and energy efficiency. The adoption of 7/5 nm nodes in high-end applications such as advanced processors and AI accelerators drove the growth, making it the leading segment in terms of nodal size.

Global Semiconductor Market Competitive Landscape

|

Company |

Headquarter |

Establishment Year/Vintage |

CAPEX' 23 (USD Bn) |

|

BASF Electronic Chemicals |

Germany |

1865 |

5.52 |

|

Air Liquide S.A |

France |

1902 |

NA |

|

Air Products & Chemicals, Inc |

USA |

1940 |

4.65 |

|

DuPont |

USA |

1802 |

0.6 |

|

Linde PLC |

Ireland |

1879 |

NA |

Global Semiconductor Industry Analysis

Global Semiconductor Market Growth Drivers:

- Opportunities in the EV Industry for Semiconductor Manufacturers: The electrification of transportation and the rapid growth of the electric vehicle (EV) industry present significant opportunities for semiconductor manufacturers. As EVs become more prevalent, the demand for critical components such as power management systems, battery management systems, and advanced driver-assistance systems (ADAS) increases. In 2023, Battery electric vehicles (BEVs) accounted for 9.5 million out of the 13.6 million EVs sold globally in 2023, with PHEVs (plug-in hybrid electric vehicles) making up the remaining 4.1 million. Additionally, EV sales represented around 18% of total car sales worldwide in 2023, up from 14% in 2022.

- Growth in Semiconductor Demand from Wireless and Portable Electronics: The increasing prevalence of wireless and portable electronics is driving innovation and growth within the semiconductor industry. Consumers and businesses are demanding smaller, faster, and more power-efficient devices, leading semiconductor companies to develop advanced solutions to meet these evolving requirements. Mobile and consumer electronics account for 60% of global semiconductor demand, with mobile devices alone consuming about 55% of this segment. This includes the miniaturization of components, enhancement of processing power, and improvements in energy efficiency, all of which are essential for the next generation of smartphones, tablets, wearables, and other portable electronics.

- Demand for Specialized Semiconductors in Emerging Technologies: Emerging technologies such as artificial intelligence (AI), machine learning (ML), augmented reality (AR), virtual reality (VR), blockchain, and 5G telecommunications are driving substantial growth in the semiconductor industry. These technologies require specialized semiconductor components for processing, memory, connectivity, and sensor capabilities. By 2025, it is anticipated that 5% of customer interactions will be powered by AI further driving the market. Additionally, in 2021, venture capital investments in blockchain startups hit a record high of USD 5 billion.

Global Semiconductor Market Challenges:

- Concentration of Manufacturing: The global semiconductor industry faces a significant challenge due to the concentration of manufacturing in a few key regions, notably East Asia, including Taiwan, South Korea, and China. These regions are home to some of the world's largest semiconductor foundries, such as TSMC and Samsung. This geographic concentration makes the industry highly susceptible to disruptions caused by natural disasters, geopolitical tensions, and supply chain bottlenecks.

- Rapid Technological Advancements: As semiconductor manufacturing processes advance, they become increasingly complex, posing several challenges. Process miniaturization, which involves reducing the size of semiconductor devices to fit more transistors on a chip, is a significant challenge due to physical and technical limitations. Achieving higher yields, which means producing more functional chips from a single wafer, becomes more difficult as processes shrink. Additionally, reliability testing becomes more crucial and complex, ensuring that these tiny, densely packed devices perform consistently over time.

Global Semiconductor Market Future Outlook

The Global Semiconductor market is expected to reach a market size of USD 1240 Bn by 2029 showing substantial growth driven by Increasing Demand for AI and machine learning chips, rising investment in research and development, and changing geopolitical dynamics.

Future Market Trends

- Increasing Demand for AI and Machine Learning Chips: The adoption of artificial intelligence (AI) and machine learning (ML) technologies across industries is significantly driving demand for specialized semiconductor chips optimized for AI inference, training, and acceleration tasks. These chips, such as GPUs, TPUs, and custom AI accelerators, are designed to handle the intensive computational requirements of AI algorithms.

- Rising Investment in Research and Development: Companies in the semiconductor industry are investing heavily in research and development (R&D) to innovate and develop new technologies that meet the evolving needs of various applications. These investments are crucial for advancements in materials science, chip design, manufacturing processes, and packaging techniques.

Scope of the Report

|

By Region |

North America Europe APAC Latin America MEA |

|

By Product Type |

Logic Memory Analog MPU Opto Discretes MCU Sensors DSP |

|

By End-User Type |

Smartphone Personal Computing Servers, Data Centers & Storage Industrial Electronics Consumer Electronics Automotive Wired/ Wireless Infrastructure (Networking) Others |

|

By Nodal Size Type |

5 nm 7/5 nm 10/7 nm 16/14 nm 22/20 nm 32/28 nm 45/40 nm 65 nm 90 nm 130 nm 180 nm |

|

By Extrinsic & Intrinsic Type |

Extrinsic Intrinsic |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Banks and Financial Institutions

Government and Regulatory Bodies (FCC, NDRC, and METI)

Venture Capitalists

Semiconductor Manufacturers

Electronics and Consumer Goods Companies

Automotive Industry Players

Telecommunications and Networking Companies

Industrial Electronics Companies

Healthcare Technology Firms

Time Period Captured in the Report:

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2029

Companies

Players Mentioned in the Report:

BASF Electronic Chemicals

Air Liquide S.A

Air Products & Chemicals, Inc

DuPont

Linde PLC

Table of Contents

1. Executive Summary

1.1 Global Electronics Market

1.2 Global Semiconductor Market

2. Global Overview

2.1 Overview of Global Economics

2.2 Overview of Global Electronics Market

2.3 Global Electronics Revenue

2.4 Global Semiconductor Infrastructure

3. Global Semiconductor Market Overview

3.1 Ecosystem

3.2 Value Chain

3.3 Case Study

4. Global Semiconductor Market Size (in USD Bn), 2018-2023

5. Global Semiconductor Market Segmentation (in value %), 2018-2023

5.1 By Region (North America, Europe, APAC, Latin America and MEA) in value %, 2018-2023

5.2 By Product (Logic, Memory, Analog, MPU, Opto, Discretes, MCU, Sensors, and DSP) in value%, 2018-2023

5.3 By End-User (Smartphone, Personal Computing, Servers, Data Centers & Storage, Industrial Electronics, Consumer Electronics, Automotive, Wired/ Wireless Infrastructure (Networking), and Others) in value %, 2018-2023

5.4 By Nodal Size (5 nm, 7/5 nm, 10/7 nm, 16/14 nm, 22/20 nm, 32/28 nm, 45/40 nm, 65 nm, 90 nm, 130 nm, and 180 nm) in value %, 2018-2023

5.5 By Extrinsic & Intrinsic (Extrinsic and Intrinsic) in value %, 2018-2023

6. Global Semiconductor Market Competition Landscape

6.1 Market Share Analysis

6.2 Market Heat Map Analysis (By Technology)

6.3 Market Heat Map Analysis (By Offerings)

6.4 Market Cross Comparison

6.5 Comparison Matrix

6.6 Investment Landscape

7. Global Semiconductor Market Dynamics

7.1 Growth Drivers

7.2 Challenges

7.3 Trends

7.4 Case Studies

7.5 Strategic Initiatives

8. Global Semiconductor Future Market Size (in USD Bn), 2023-2029

9. Global Semiconductor Future Market Segmentation (in value %), 2023-2029

9.1 By Region (North America, Europe, APAC, Latin America and MEA) in value %, 2023-2029

9.2 By Product (Logic, Memory, Analog, MPU, Opto, Discretes, MCU, Sensors, and DSP) in value%, 2018-2023

9.3 By End-User (Smartphone, Personal Computing, Servers, Data Centers & Storage, Industrial Electronics, Consumer Electronics, Automotive, Wired/ Wireless Infrastructure (Networking), and Others) in value %, 2018-2023

9.4 By Nodal Size (5 nm, 7/5 nm, 10/7 nm, 16/14 nm, 22/20 nm, 32/28 nm, 45/40 nm, 65 nm, 90 nm, 130 nm, and 180 nm) in value %, 2018-2023

9.5 By Extrinsic & Intrinsic (Extrinsic and Intrinsic) in value %, 2018-2023

10. Analyst Recommendations

11. Research Methodology

11.1 Market Definitions and Assumptions

11.2 Abbreviations

11.3 Market Sizing Approach

11.4 Consolidated Research Approach

11.5 Understanding Market Potential Through In-Depth Industry Interviews

11.6 Primary Research Approach

11.7 Limitations and Future Conclusion

Disclaimer

Contact Us

Research Methodology

Step 01 Hypothesis Creation:

The research team has first framed a hypothesis about the market through analysis of existing industry factors obtained from press releases and industry reports from major financial & non-financial institutions, journals, and annual reports of major companies (Intel Corporation, Samsumg Electronics, TSMC,SK Hynix Inc).

Step 02 Data Collection from Public and Proprietary Databases:

The team has used both public and proprietary databases to define and collect each market data point such as the revenue, industry wise segmentation and several other factors.

Step 03 Primary Research and Expert Interviews:

CATIs with the management to understand their operating and financial indicators including business model, pricing models, market share, geographical presence, revenue, product offerings & latest news.

Step 04 Data Validation and Cross-Analysis:

General consensus on data collected from primary research and public and proprietary databases has been reached by conducting in-house decision tree analysis of the data points available and thereafter comparing it with changes in the macro-economic factors affecting the market.

Frequently Asked Questions

01 How big is the global semiconductor market?

In 2023, Global Semiconductor market was estimated at USD 630 Bn and is forecasted to reach a market size of USD 1240 Bn in 2029 driven by Electrification of transportation and the growth of the electric vehicle industry, increasing prevalence of wireless and portable electronics, and industry 4.0 and the role of semiconductors in smart manufacturing.

02 What are the challenges in the global semiconductor market?

Challenges in the global semiconductor market include supply chain disruptions, high manufacturing costs, and the need for continuous innovation. Additionally, geopolitical tensions and trade restrictions can impact the stability and growth of the market.

03 Who are the major players in the global semiconductor market?

Key players in the global semiconductor market include Samsung Semiconductors, Taiwan Semiconductor Manufacturing Company Limited (TSMC) , Intel Corporation, Qualcomm Incorporated, and SK Hynix Inc. These companies dominate due to their advanced manufacturing capabilities and extensive research and development efforts.

04 What are the growth drivers of the global semiconductor market?

The global semiconductor market is driven by Electrification of transportation and the growth of the electric vehicle industry, increasing prevalence of wireless and portable electronics, and industry 4.0 and the role of semiconductors in smart manufacturing. Additionally, advancements in automotive electronics and industrial automation are contributing to the market's growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.