Global Semiconductors Market Outlook to 2030

Region:Global

Author(s):Shivani

Product Code:KROD7734

Region:Global

Author(s):Shivani

Product Code:KROD7734

October 2024

86

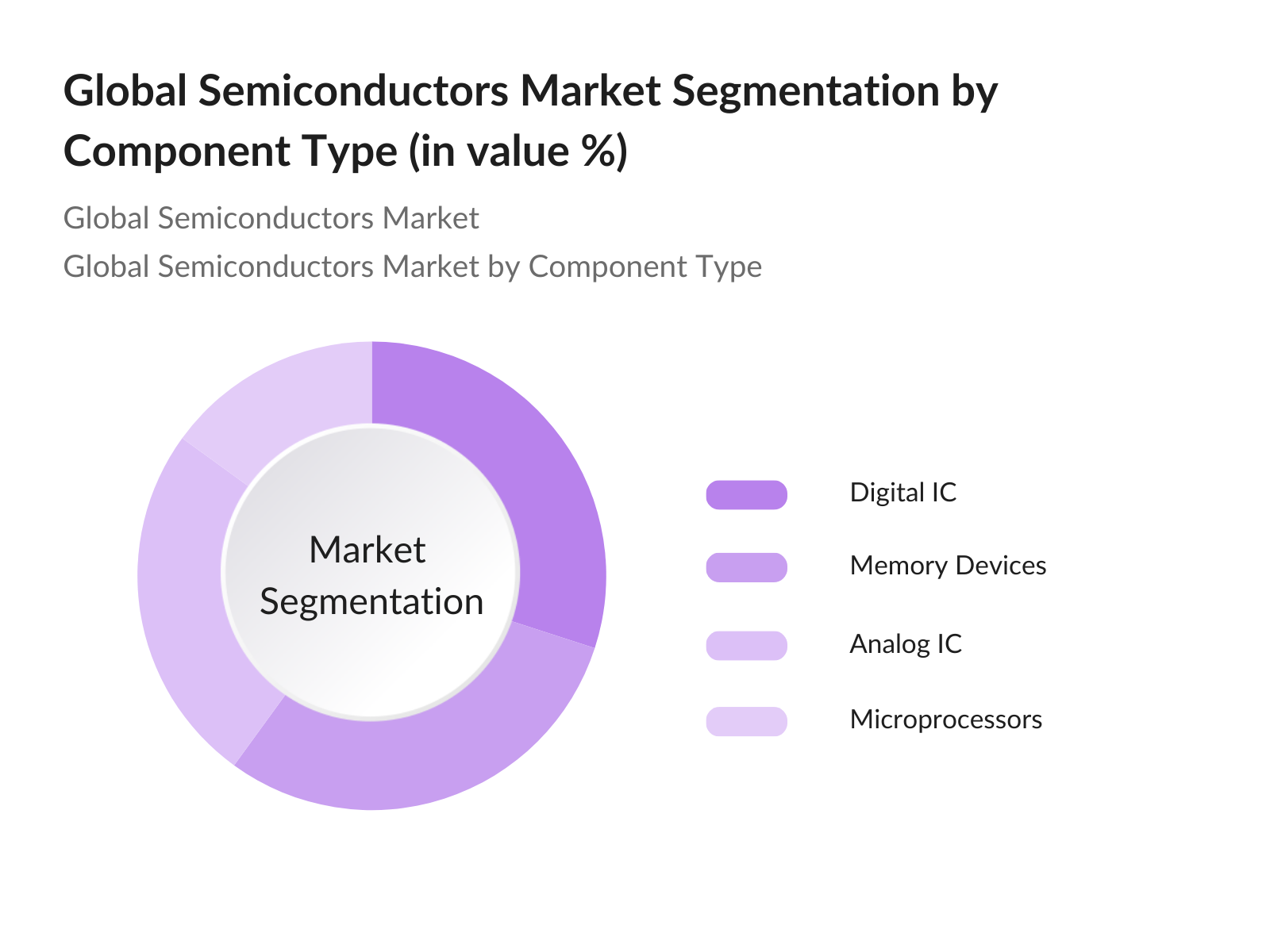

By Component Type: The semiconductor market is segmented by component type into Analog IC, Digital IC, Microprocessors, and Memory Devices. Memory devices, particularly DRAM and NAND flash, dominate the market due to their widespread use in data centers and smartphones. The demand for cloud computing and data storage solutions has significantly increased the market share of memory devices, making them a leading segment within the industry.

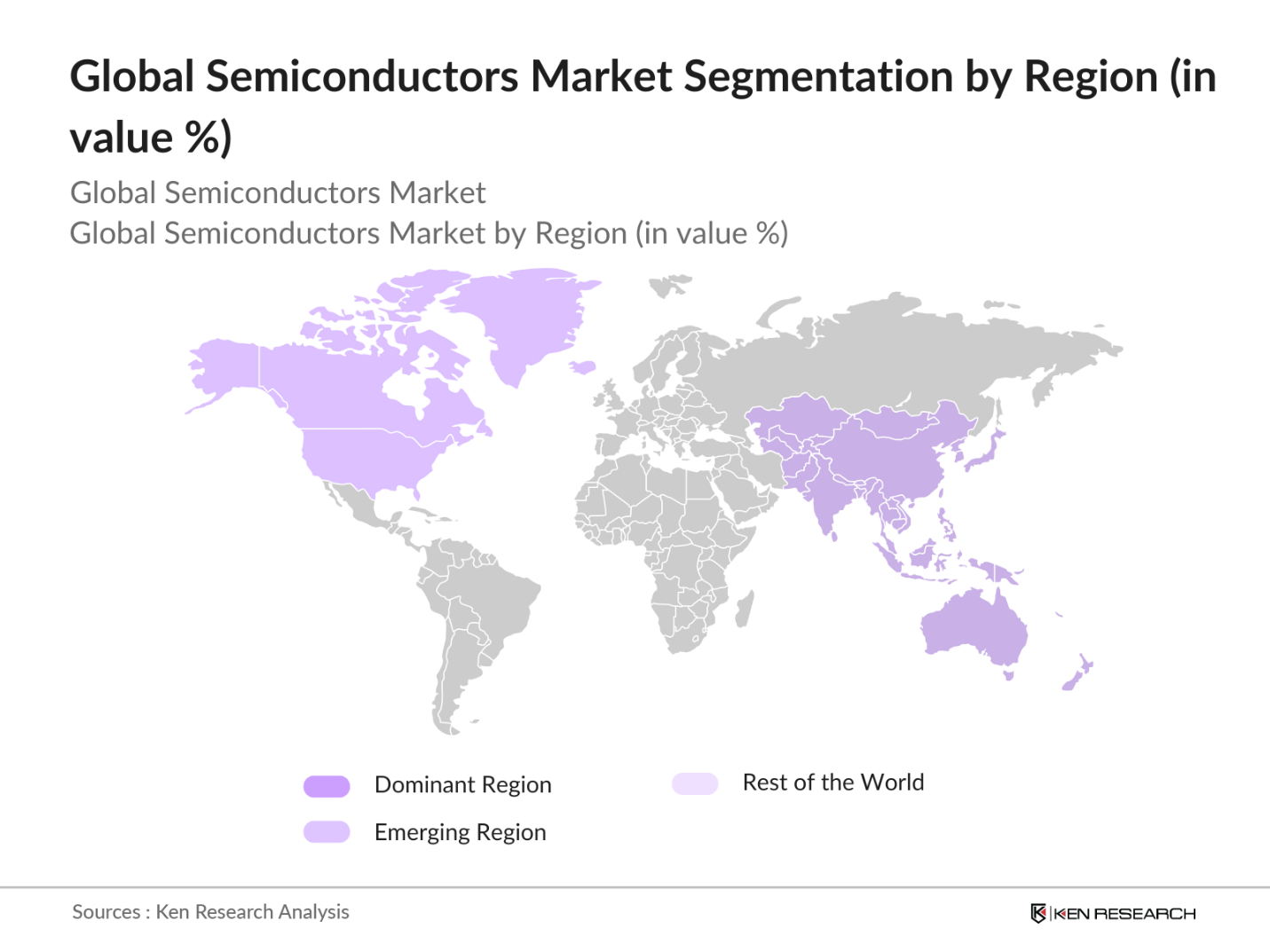

By Region: The semiconductor market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific is the dominant region, thanks to its strong manufacturing base and the presence of key industry players. Taiwan and South Korea, home to TSMC and Samsung, are at the forefront of global semiconductor production, contributing significantly to the market's expansion.

The global semiconductor market is dominated by several major players with strong market positions due to their technological advancements, R&D investments, and extensive manufacturing capabilities. The market is highly consolidated, with companies like Intel and TSMC playing pivotal roles. These firms lead in innovation and production capacity, contributing to their market dominance.

|

Company |

Establishment Year |

Headquarters |

R&D Expenditure |

Patent Portfolio |

Revenue |

Production Capacity |

Regional Presence |

Market Share |

|

Intel Corporation |

1968 |

Santa Clara, USA |

High |

|||||

|

Taiwan Semiconductor (TSMC) |

1987 |

Hsinchu, Taiwan |

Very High |

|||||

|

Samsung Electronics |

1969 |

Suwon, South Korea |

High |

|||||

|

Qualcomm Inc. |

1985 |

San Diego, USA |

Moderate |

|||||

|

Nvidia Corporation |

1993 |

Santa Clara, USA |

High |

Over the next few years, the global semiconductors market is expected to witness significant growth. This surge will be driven by technological advancements, including the expansion of 5G networks, AI integration, and the proliferation of electric and autonomous vehicles. Increasing demand for semiconductors in the automotive and industrial sectors, coupled with the growing need for high-performance computing chips, will further propel market growth.

|

By Component Type |

Analog IC Digital IC Microprocessors Memory Devices |

|

By Application |

Consumer Electronics |

|

By Technology Node |

<10nm |

|

By Material Type |

Silicon |

|

By Region |

North America |

Intel Corporation

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Dynamics

1.4 Value Chain Analysis

2.1 Historical Market Size

2.2 Growth Rate Analysis (CAGR)

2.3 Major Market Milestones and Developments

2.4 Impact of Technological Advancements

3.1 Key Growth Drivers (Supply Chain Efficiency, Chip Design, AI Integration, etc.)

3.2 Market Challenges (Supply Chain Disruptions, Geopolitical Risks, etc.)

3.3 Opportunities (5G Rollout, IoT Proliferation, Automotive Semiconductors)

3.4 Key Trends (Miniaturization, Moores Law Adaptation, Chip Customization)

3.5 Regulatory Influence (US-China Trade Tensions, Environmental Standards)

3.6 Porters Five Forces Analysis

3.7 SWOT Analysis

3.8 Stakeholder Ecosystem

4.1 By Component Type (In Value %)

4.1.1 Analog IC

4.1.2 Digital IC

4.1.3 Microprocessors

4.1.4 Memory Devices

4.2 By Application (In Value %)

4.2.1 Consumer Electronics

4.2.2 Automotive

4.2.3 Industrial

4.2.4 Communications

4.2.5 Data Centers

4.3 By Technology Node (In Value %)

4.3.1 <10nm

4.3.2 10-20nm

4.3.3 >20nm

4.4 By Material Type (In Value %)

4.4.1 Silicon

4.4.2 Gallium Nitride

4.4.3 Silicon Carbide

4.5 By Region (In Value %)

4.5.1 North America

4.5.2 Europe

4.5.3 Asia-Pacific

4.5.4 Latin America

4.5.5 Middle East & Africa

5.1 Detailed Profiles of Major Companies

5.1.1 Intel Corporation

5.1.2 Taiwan Semiconductor Manufacturing Co. (TSMC)

5.1.3 Samsung Electronics

5.1.4 Qualcomm Inc.

5.1.5 Nvidia Corporation

5.1.6 Broadcom Inc.

5.1.7 Advanced Micro Devices (AMD)

5.1.8 Texas Instruments

5.1.9 Infineon Technologies

5.1.10 STMicroelectronics

5.1.11 Micron Technology

5.1.12 NXP Semiconductors

5.1.13 Renesas Electronics

5.1.14 GlobalFoundries

5.1.15 ON Semiconductor

5.2 Cross Comparison Parameters (R&D Expenditure, Market Cap, Patent Portfolio, Revenue Mix, Production Capacity, Supply Chain, Market Share, Regional Presence)

5.3 Strategic Initiatives

5.4 Mergers and Acquisitions

5.5 Investment and Funding Analysis

5.6 Joint Ventures and Collaborations

6.1 Export Control Laws

6.2 Environmental Regulations

6.3 Intellectual Property Rights

6.4 Industry Standards (JEDEC, ISO, etc.)

7.1 Projections for Market Growth

7.2 Key Drivers for Future Market Growth

8.1 By Component Type

8.2 By Application

8.3 By Technology Node

8.4 By Material Type

8.5 By Region

9.1 TAM/SAM/SOM Analysis

9.2 Market Entry Strategies

9.3 White Space Opportunity Analysis

9.4 Competitive Positioning

The initial stage focuses on identifying the major stakeholders within the global semiconductors market. Comprehensive desk research, including the use of proprietary and secondary databases, helps map the ecosystem and identify the key variables driving market growth.

In this step, historical data related to the semiconductor market is compiled and analyzed. This includes assessing production capacities, sales figures, and overall market penetration. The primary aim is to build a detailed picture of the market's performance.

Hypotheses regarding market trends and growth projections are formulated and validated through expert consultations. Interviews with industry experts provide insights into operational efficiencies, market dynamics, and future trends, enhancing the accuracy of the report.

The final phase integrates data collected from manufacturers and other industry stakeholders to validate the findings. The bottom-up approach ensures a comprehensive and accurate representation of the market.

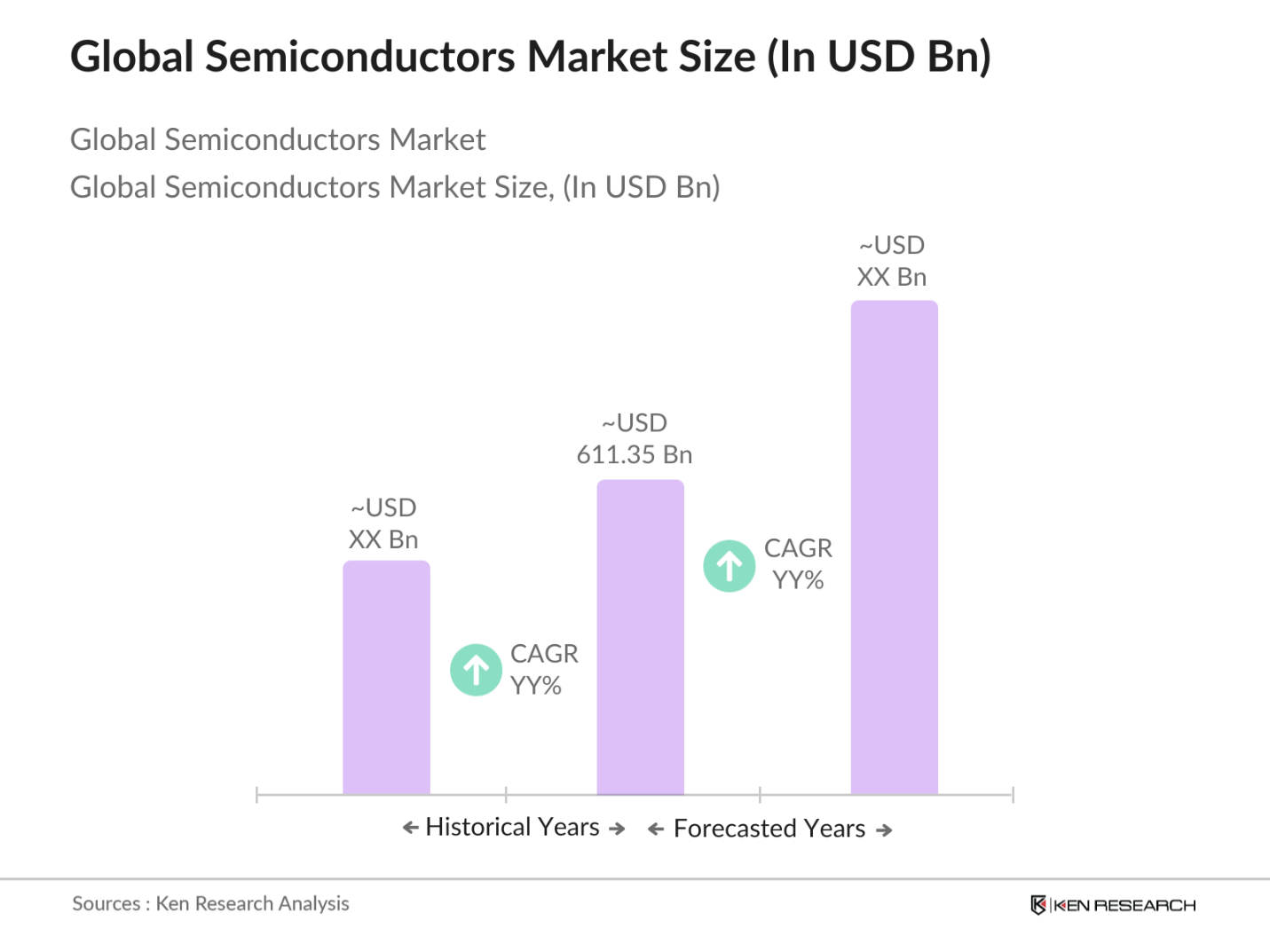

The global semiconductors market is valued at USD 611.35 billion, driven by strong demand from sectors such as consumer electronics, automotive, and telecommunications.

Challenges include supply chain disruptions, geopolitical tensions, and the high cost of research and development. Additionally, the global chip shortage has posed a significant challenge for manufacturers.

Key players include Intel Corporation, Taiwan Semiconductor Manufacturing Co. (TSMC), Samsung Electronics, Qualcomm Inc., and Nvidia Corporation, dominating due to their extensive R&D capabilities and production capacities.

The market is propelled by the expansion of 5G, AI, electric vehicles, and the increased demand for data centers. Advancements in semiconductor technologies and rising demand for high-performance computing also contribute to growth.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.