Global Software Defined Perimeter Market Outlook to 2030

Region:Global

Author(s):Abhinav kumar

Product Code:KROD2251

December 2024

94

About the Report

Global Software Defined Perimeter Market Overview

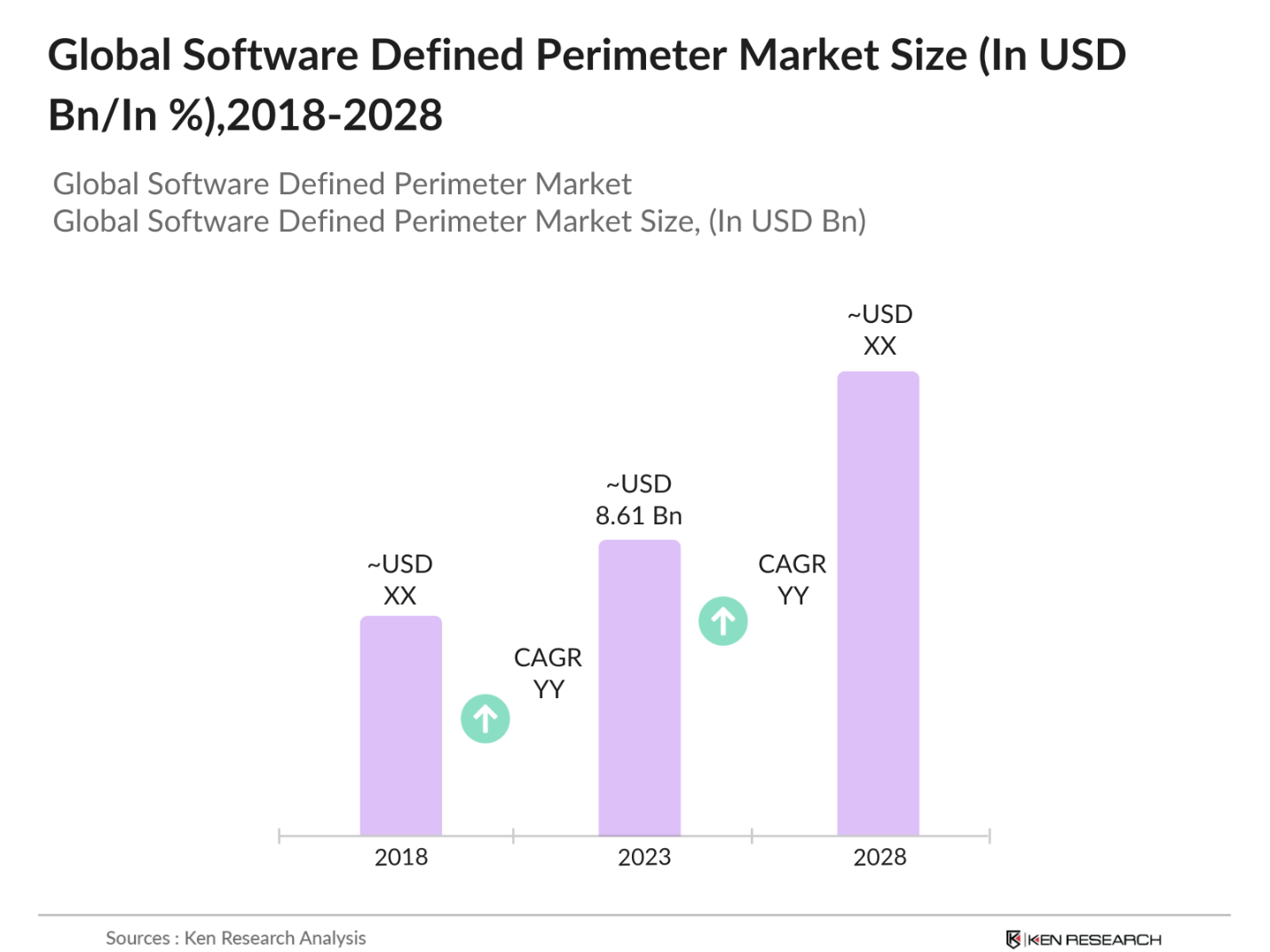

- The Global Software Defined Perimeter (SDP) Market was valued at USD 8.61 billion in 2023. The market is driven by the rising need for secure network access control, fueled by increasing cyber threats, the growing adoption of cloud-based infrastructure, and the global shift towards zero-trust security frameworks. Enterprises are adopting SDP solutions to mitigate security risks, ensuring that only authenticated users can access their networks.

- Key players in the global SDP market include Cisco Systems, Palo Alto Networks, Zscaler, Fortinet, and Broadcom Inc. (formerly Symantec). These companies are at the forefront of innovation, offering solutions that integrate with artificial intelligence (AI) and machine learning to enhance security, improve user experience, and reduce the risk of unauthorized access.

- In April 2023, Palo Alto Networks announced its acquisition of CloudGenix, a prominent provider of software-defined wide area network (SD-WAN) solutions. This acquisition is seen as a strategic move to integrate SD-WAN capabilities with their existing SDP solutions, enhancing secure network access for enterprises. This highlights a growing trend in combining SD-WAN and SDP technologies to secure corporate networks.

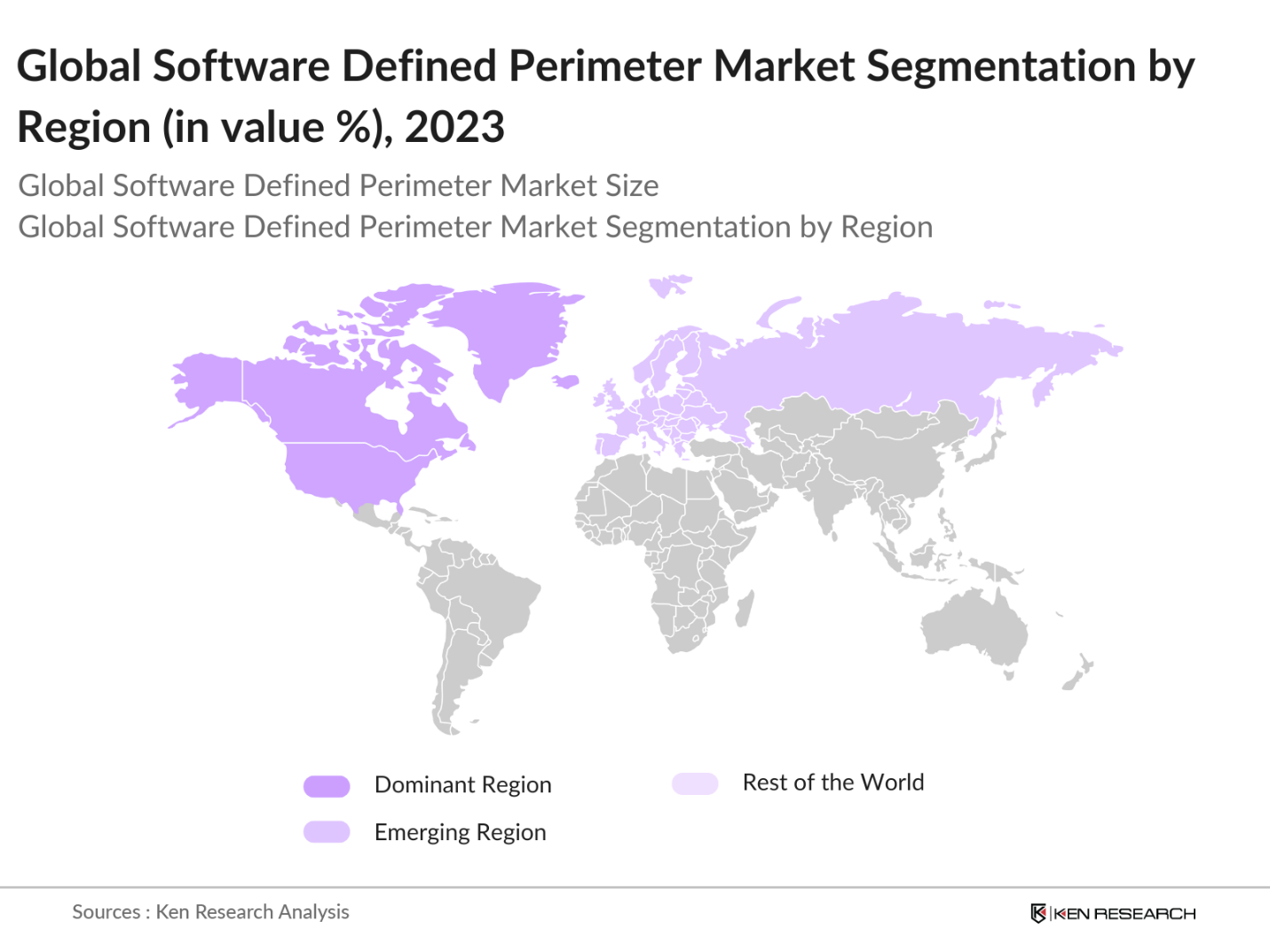

- In 2023, North America dominated the global SDP market due to early technology adoption, a robust cloud infrastructure, and a high number of cyberattacks. This region continues to lead in demand for advanced security solutions, especially as federal and corporate entities enhance their cybersecurity protocols.

Global Software Defined Perimeter Market Segmentation

The global SDP market is segmented by region, component, and deployment mode.

By Region: The global SDP market is segmented into North America, Europe, Asia-Pacific (APAC), Middle East & Africa (MEA), and Latin America. In 2023, North America led the market due to substantial investments in cybersecurity and a growing emphasis on cloud computing. Europe followed closely due to strict regulations like GDPR, pushing organizations to adopt advanced security measures.

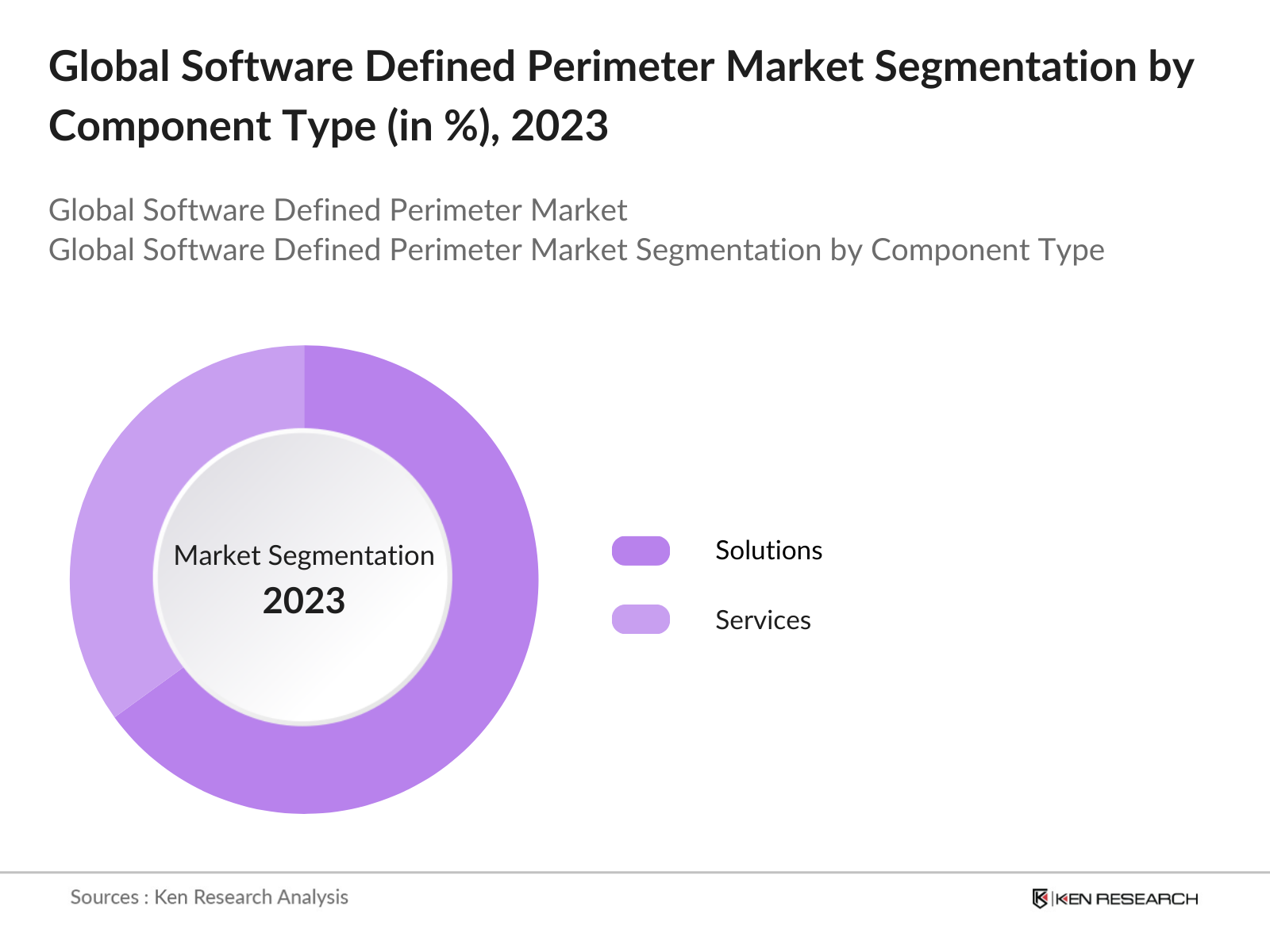

By Component: The market is segmented into software and services. In 2023, the software segment held the highest market share, driven by the growing need for scalable security solutions that ensure secure access across distributed networks.

By Deployment Mode: The market is segmented into cloud-based and on-premise solutions. In 2023, the cloud-based deployment segment held the largest market share, due to the growing reliance on cloud infrastructure for business operations and the flexibility these solutions offer for securing remote workforces.

Global Software Defined Perimeter Market Competitive Landscape

|

Company |

Establishment Year |

Headquarters |

|

Cisco Systems |

1984 |

San Jose, California, USA |

|

Palo Alto Networks |

2005 |

Santa Clara, California, USA |

|

Zscaler |

2008 |

San Jose, California, USA |

|

Fortinet |

2000 |

Sunnyvale, California, USA |

|

Broadcom Inc. (Symantec) |

1961 |

San Jose, California, USA |

- Cisco Systems: In 2024, Cisco introduced new SDP capabilities that integrate with their existing zero-trust offerings, ensuring enhanced protection for hybrid cloud environments. This development helps companies securely scale their operations across cloud and on-premise environments.

- Zscaler: In 2023, zscaler expanded its zero-trust platform , signing contracts with multiple Fortune 500 companies to secure remote access for over 100,000 users globally. The companys focus on cloud-native security solutions continues to strengthen its market position.

Global Software Defined Perimeter Market Analysis

Global Software Defined Perimeter Market Growth Drivers

- Increasing Cyber Threats: In 2023, businesses globally faced a sharp rise in sophisticated cyberattacks targeting critical infrastructure. The number of ransomware attacks on industries like healthcare, government, and finance reached an all-time high, necessitating investment in security technologies like SDP to mitigate these risks.

- Growing Cloud Adoption: In 2023, cloud infrastructure investments totaled USD 105 billion globally. As more businesses move their operations to the cloud, the need for secure access management becomes crucial, with SDP solutions offering a scalable and effective way to protect cloud environments.

- Shift Towards Zero-Trust Architectures: In 2023, zero-trust frameworks, which require strict identity verification for network access, are gaining popularity across industries. This shift is driven by increasing demands for improved security protocols, particularly in highly regulated sectors like BFSI and healthcare.

Global Software Defined Perimeter Market Challenges

- Complex Integration with Legacy Systems: Many companies, especially in sectors like manufacturing and utilities, face difficulties in integrating modern SDP solutions with their existing IT infrastructure. The cost and complexity of transitioning to new systems remain a significant hurdle for widespread adoption.

- Lack of Standardization: The absence of globally accepted protocols for SDP implementation across industries hampers seamless integration. Regions such as Latin America and parts of Africa lag in adoption due to inconsistent regulatory standards and slow digital infrastructure development.

Global Software Defined Perimeter Market Government Initiatives

- European Unions NIS2 Directive (2024) In 2024, the European Union's NIS2 Directive, set to come into force, aims to strengthen the cybersecurity posture of critical infrastructure organizations within the region. The directive mandates enhanced security measures, including the adoption of advanced cybersecurity frameworks like SDP. The directive has prompted companies to invest heavily in upgrading their security systems, with SDP technologies being a key component of compliance.

- Indias National Cybersecurity Strategy (2023) In 2023, India launched its National Cybersecurity Strategy, focusing on strengthening the countrys critical infrastructure and digital economy through the adoption of cutting-edge cybersecurity solutions like SDP. The government has allocated 700 crore (approximately USD 84 million) for implementing cybersecurity measures across various sectors. This initiative is expected to drive the adoption of SDP technologies among both public and private organizations.

Global Software Defined Perimeter Market Future Outlook

The Global Software Defined Perimeter Market is poised for substantial growth over the next five years, driven by the increasing demand for secure network access, advancements in zero-trust frameworks, and growing investments in cloud-based infrastructure.

Future Market Trends

- AI Integration in SDP Solutions: By 2028, SDP solutions are expected to incorporate AI and machine learning to enhance threat detection and response capabilities. AI-driven analytics will enable organizations to predict potential security risks, offering real-time protection against cyberattacks.

- Expansion of Zero-Trust Networks: By 2028, the adoption of zero-trust architectures will continue to grow, with 70% of global enterprises expected to have implemented these frameworks. SDP will play a crucial role in facilitating the secure deployment of these architectures, particularly in industries handling sensitive data.

Scope of the Report

|

By Component |

Software Services |

|

By Deployment Mode |

Cloud-Based On-Premise |

|

By Organization Size |

Large Enterprises Small and Medium Enterprises (SMEs) |

|

By End-Use Industry |

BFSI Healthcare IT & Telecom Government Retail |

|

By Region |

North America Europe Asia-Pacific (APAC) Middle East & Africa (MEA) Latin America |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

Cloud Service Companies

Network Security companies

Telecommunication Companies

Healthcare Industry

Government and Regulatory Bodies (ENISA, NIST)

Manufacturing Companies

E-commerce Companies

Investments and Venture Capitalist Firms

Time Period Captured in the Report

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

Cisco Systems

Palo Alto Networks

Zscaler

Broadcom Inc. (Symantec)

Fortinet

Okta

Akamai Technologies

Google Cloud

IBM Corporation

Check Point Software Technologies

Table of Contents

1. Global Software Defined Perimeter Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Global Software Defined Perimeter Market Size (in USD Bn), 2018-2023

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Global Software Defined Perimeter Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Cyber Threats

3.1.2. Growing Cloud Adoption

3.1.3. Shift Towards Zero-Trust Architectures

3.2. Restraints

3.2.1. Complex Integration with Legacy Systems

3.2.2. Lack of Standardization

3.3. Opportunities

3.3.1. Technological Advancements

3.3.2. Expansion into Emerging Markets

3.3.3. Increased Investment in AI

3.4. Trends

3.4.1. AI Integration in SDP Solutions

3.4.2. Expansion of Zero-Trust Networks

3.4.3. Growth in Cloud-Based Deployment

3.5. Government Initiatives

3.5.1. European Unions NIS2 Directive (2024)

3.5.2. Indias National Cybersecurity Strategy (2023)

3.5.3. US Cybersecurity Strategy Enhancements

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Competition Ecosystem

4. Global Software Defined Perimeter Market Segmentation, 2023

4.1. By Component (in Value %)

4.1.1. Software

4.1.2. Services

4.2. By Deployment Mode (in Value %)

4.2.1. Cloud-Based

4.2.2. On-Premise

4.3. By Organization Size (in Value %)

4.3.1. Large Enterprises

4.3.2. Small and Medium Enterprises (SMEs)

4.4. By End-Use Industry (in Value %)

4.4.1. BFSI

4.4.2. Healthcare

4.4.3. IT & Telecom

4.4.4. Government

4.4.5. Retail

4.5. By Region (in Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific (APAC)

4.5.4. Middle East & Africa (MEA)

4.5.5. Latin America

5. Global Software Defined Perimeter Market Cross Comparison

5.1. Detailed Profiles of Major Companies

5.1.1. Cisco Systems

5.1.2. Palo Alto Networks

5.1.3. Zscaler

5.1.4. Fortinet

5.1.5. Broadcom Inc. (Symantec)

5.1.6. Cloudflare

5.1.7. Akamai Technologies

5.1.8. IBM Security

5.1.9. Check Point Software

5.1.10. McAfee

5.1.11. Juniper Networks

5.1.12. Forcepoint

5.1.13. Barracuda Networks

5.1.14. Trend Micro

5.1.15. Tufin Software

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

6. Global Software Defined Perimeter Market Competitive Landscape

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

7. Global Software Defined Perimeter Market Regulatory Framework

7.1. Data Protection Standards

7.2. Compliance Requirements

7.3. Certification Processes

8. Global Software Defined Perimeter Market Future Market Size (in USD Bn), 2023-2028

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

9. Global Software Defined Perimeter Market Future Market Segmentation, 2028

9.1. By Component (in Value %)

9.2. By Deployment Mode (in Value %)

9.3. By Organization Size (in Value %)

9.4. By End-Use Industry (in Value %)

9.5. By Region (in Value %)

10. Global Software Defined Perimeter Market Analysts Recommendations

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step: 1 Identifying Key Variables

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around the Market to collate Market-level information.

Step: 2 Market Building

Collating statistics on the Global Software Defined Perimeter Market over the years, and analyzing the penetration of Marketplaces as well as the ratio of service providers to compute the revenue generated for the market. We will also review service quality statistics to understand the revenue generated which can ensure accuracy behind the data points shared.

Step: 3 Validating and Finalizing

Building Market hypotheses and conducting CATIs with Market experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Step: 4 Research Output

Our team will approach multiple Software Defined Perimeter companies to understand the nature of service segments, consumer preferences, and other parameters. This supports validating statistics derived through a bottom-to-top approach from these Software Defined Perimeter companies, ensuring accuracy and reliability in the report.

Frequently Asked Questions

01 How big is the Global Software Defined Perimeter (SDP) market?

The global Software Defined Perimeter market was valued at USD 8.61 billion in 2023, driven by rising concerns over network security, the growing adoption of cloud-based services, and the increasing frequency of cyberattacks targeting various sectors such as healthcare, finance, and retail.

02 What are the challenges in the Global Software Defined Perimeter market?

Challenges include the lack of standardized protocols across industries, the complexity of integrating SDP solutions with legacy systems, and limited awareness among small and medium-sized enterprises (SMEs), which are still heavily reliant on traditional security models like VPNs and firewalls.

03 Who are the major players in the Global Software Defined Perimeter market?

Key players in the market include Cisco Systems, Palo Alto Networks, Zscaler, Fortinet, and Broadcom Inc. (Symantec). These companies dominate due to their advanced SDP offerings, strong customer bases, and continuous innovations in zero-trust security solutions.

04 What are the growth drivers of the Global Software Defined Perimeter market?

The market is driven by the global adoption of zero-trust security frameworks, increasing incidents of cyberattacks, and growing investments in cloud infrastructure. These factors are pushing organizations across industries to adopt more robust security solutions like SDP.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.