Global Soil Moisture Sensor Market Outlook to 2030

Region:Global

Author(s):Vijay Kumar

Product Code:KROD6481

Region:Global

Author(s):Vijay Kumar

Product Code:KROD6481

December 2024

93

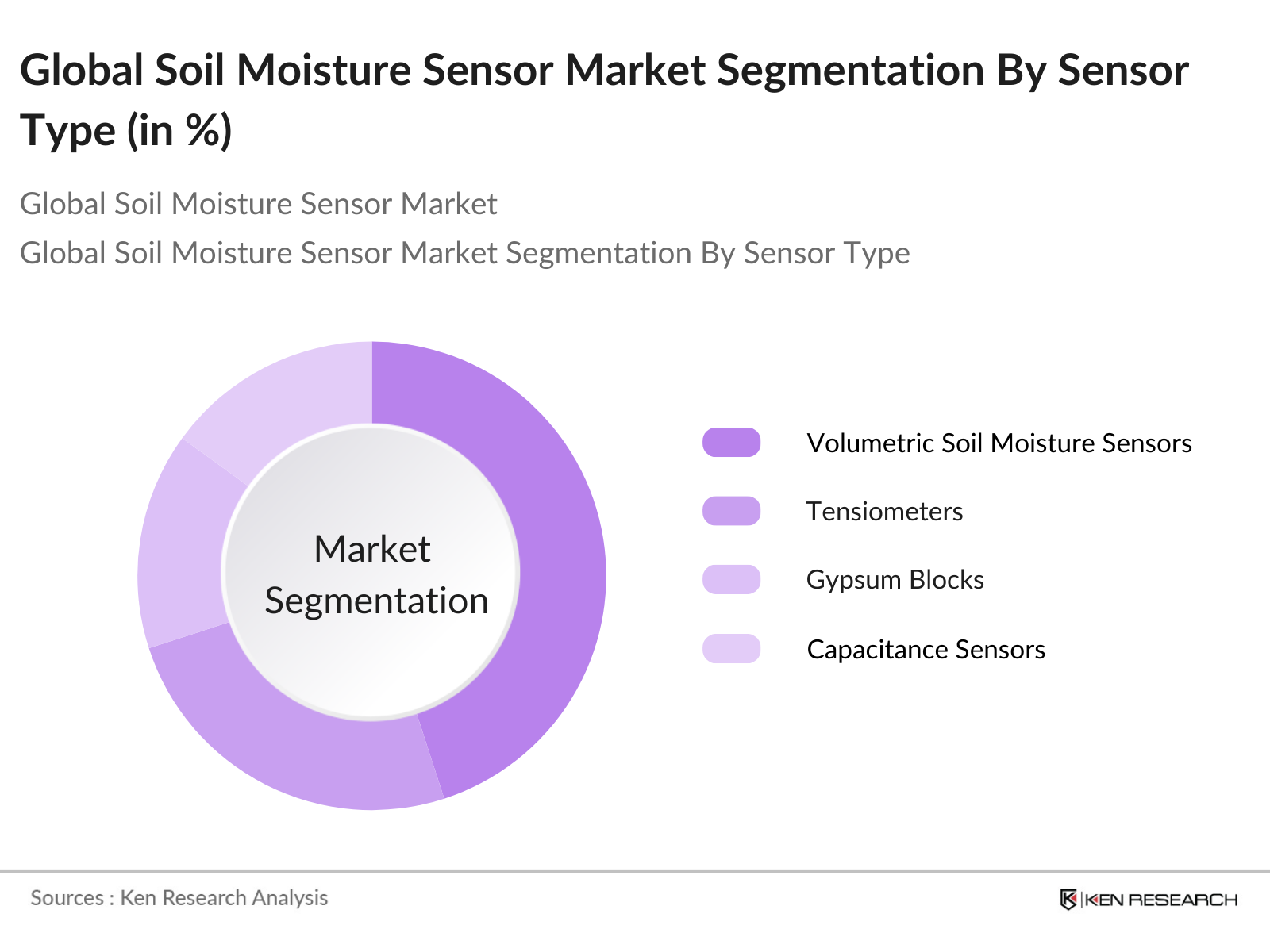

By Sensor Type: The soil moisture sensor market is segmented by sensor type into volumetric soil moisture sensors, tensiometers, gypsum blocks, and capacitance sensors. Recently, volumetric soil moisture sensors hold the dominant market share under this segmentation due to their higher accuracy and reliability in various agricultural applications. These sensors are preferred in precision agriculture due to their capability to provide real-time data on soil moisture content, leading to better water management and improved crop yields.

By Application: In terms of application, the market is segmented into agriculture, construction and landscaping, research and education, and environmental monitoring. Agriculture dominates the application segment due to the growing demand for precision farming technologies, especially in regions with water scarcity. Farmers are increasingly adopting soil moisture sensors to optimize irrigation, reduce water usage, and enhance crop yields, contributing to this segments growth.

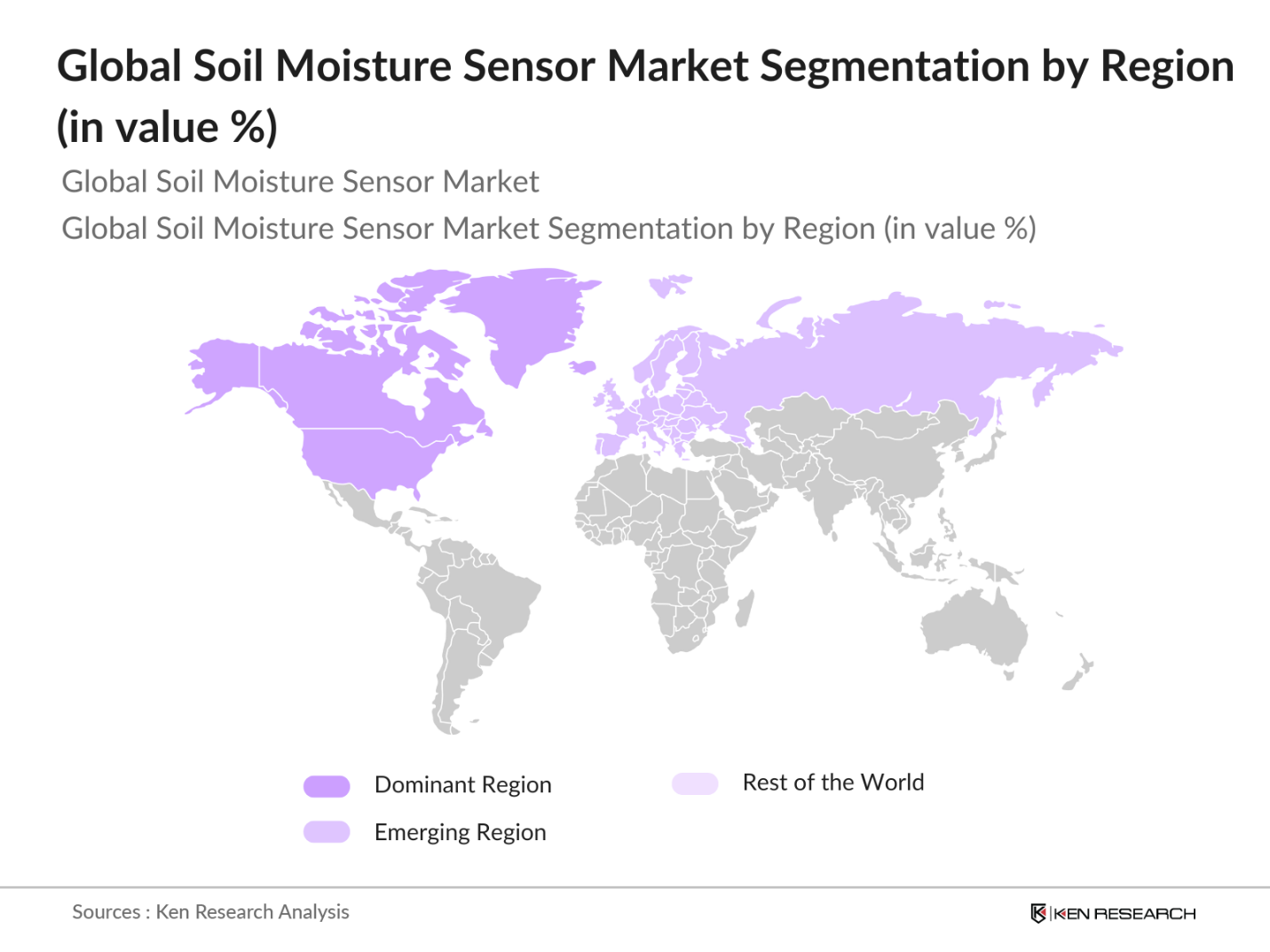

By Region: The soil moisture sensor market is segmented by region into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. North America holds the largest market share, primarily driven by the high adoption of precision agriculture and environmental monitoring initiatives in the United States and Canada. The presence of major market players in this region also plays a pivotal role in the market's dominance.

The global soil moisture sensor market is dominated by a few major players, with companies leveraging innovation, strategic partnerships, and geographical expansion to maintain their competitive edge. These firms continue to invest heavily in research and development to improve the efficiency and accuracy of soil moisture sensors. The competition is further intensified by the presence of startups focusing on disruptive sensor technologies. This consolidation emphasizes the significant influence of these key companies, making it a highly competitive market.

Over the next five years, the global soil moisture sensor market is expected to witness substantial growth driven by the increasing adoption of precision agriculture, the need for efficient water management, and advancements in IoT-enabled smart farming technologies. Rising awareness about sustainable farming practices and government support for water conservation initiatives are also expected to fuel the market's growth trajectory.

|

Sensor Type |

Volumetric Soil Moisture Sensors Tensiometers Gypsum Blocks Capacitance Sensors |

|

Application |

Agricultural Construction and Landscaping Research and Education Environmental Monitoring |

|

End-user |

Farmers Research Institutes Agronomists Government Bodies |

|

Technology |

Analog Soil Moisture Sensors Digital Soil Moisture Sensors |

|

Region |

North America Europe Asia Pacific Latin America Middle East & Africa |

1.1. Definition and Scope

1.2. Market Taxonomy (Sensor Type, Application, End-user, Geography)

1.3. Market Growth Rate

1.4. Market Segmentation Overview

1.5. Value Chain Analysis

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Technological Advancements, Major Investments)

3.1. Growth Drivers

3.1.1. Rising Need for Precision Agriculture

3.1.2. Growing Environmental Monitoring Initiatives

3.1.3. Government Support and Funding

3.1.4. Expansion of IoT in Agriculture

3.2. Market Challenges

3.2.1. High Initial Investment in Sensor Technology

3.2.2. Limited Adoption in Developing Regions

3.2.3. Data Accuracy and Calibration Issues

3.3. Opportunities

3.3.1. Integration with Smart Irrigation Systems

3.3.2. Growing Demand for Sustainable Agriculture

3.3.3. Research & Development in Advanced Sensing Technologies

3.4. Trends

3.4.1. Adoption of Wireless and Remote Monitoring Technologies

3.4.2. Use of Cloud-Based Data Analytics

3.4.3. Increased Penetration in Water Conservation Programs

3.5. Government Regulations

3.5.1. Environmental Compliance and Reporting Standards

3.5.2. Water Conservation Mandates

3.5.3. Agricultural Subsidies and Funding for Technological Integration

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Sensor Type (In Value %)

4.1.1. Volumetric Soil Moisture Sensors

4.1.2. Tensiometers

4.1.3. Gypsum Blocks

4.1.4. Capacitance Sensors

4.2. By Application (In Value %)

4.2.1. Agricultural

4.2.2. Construction and Landscaping

4.2.3. Research and Education

4.2.4. Environmental Monitoring

4.3. By End-user (In Value %)

4.3.1. Farmers

4.3.2. Research Institutes

4.3.3. Agronomists

4.3.4. Government Bodies

4.4. By Technology (In Value %)

4.4.1. Analog Soil Moisture Sensors

4.4.2. Digital Soil Moisture Sensors

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5.1. Detailed Profiles of Major Companies

5.1.1. The Toro Company

5.1.2. Campbell Scientific, Inc.

5.1.3. Decagon Devices, Inc.

5.1.4. Delta-T Devices Ltd

5.1.5. Sentek Technologies

5.1.6. Stevens Water Monitoring Systems, Inc.

5.1.7. Irrometer Company, Inc.

5.1.8. Acclima Inc.

5.1.9. AquaCheck Pvt. Ltd.

5.1.10. METER Group, Inc. USA

5.1.11. SDEC France

5.1.12. IMKO Micromodultechnik GmbH

5.1.13. Spectrum Technologies, Inc.

5.1.14. E.S.I. Environmental Sensors Inc.

5.1.15. Dynamax Inc.

5.2. Cross Comparison Parameters (Revenue, Geographic Presence, Sensor Technology, Application Focus, Innovation Index, R&D Expenditure, Number of Patents, Client Portfolio)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Environmental Standards

6.2. Agricultural Standards

6.3. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Sensor Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-user (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Market Penetration Strategy

9.4. Strategic Partnerships and Alliances

9.5. White Space Opportunity Analysis

In the first step, an ecosystem map of all major stakeholders within the global soil moisture sensor market was constructed. Extensive desk research and secondary data sources were used to identify and define critical market variables, such as sensor technology adoption and regional market trends.

In this phase, historical data on the soil moisture sensor market was compiled, including sensor penetration rates and the revenue generation from different market segments. These statistics were assessed to ensure reliability and comprehensiveness, providing a solid foundation for market sizing.

Key market hypotheses were validated through in-depth interviews with industry professionals using computer-assisted telephone interviews (CATI). Insights from these experts helped refine and corroborate the market analysis data.

In the final step, direct engagements with sensor manufacturers were carried out to acquire detailed insights into segment-specific sales and consumer preferences. The synthesized research outputs formed the basis of this comprehensive market report, ensuring accuracy and market relevance.

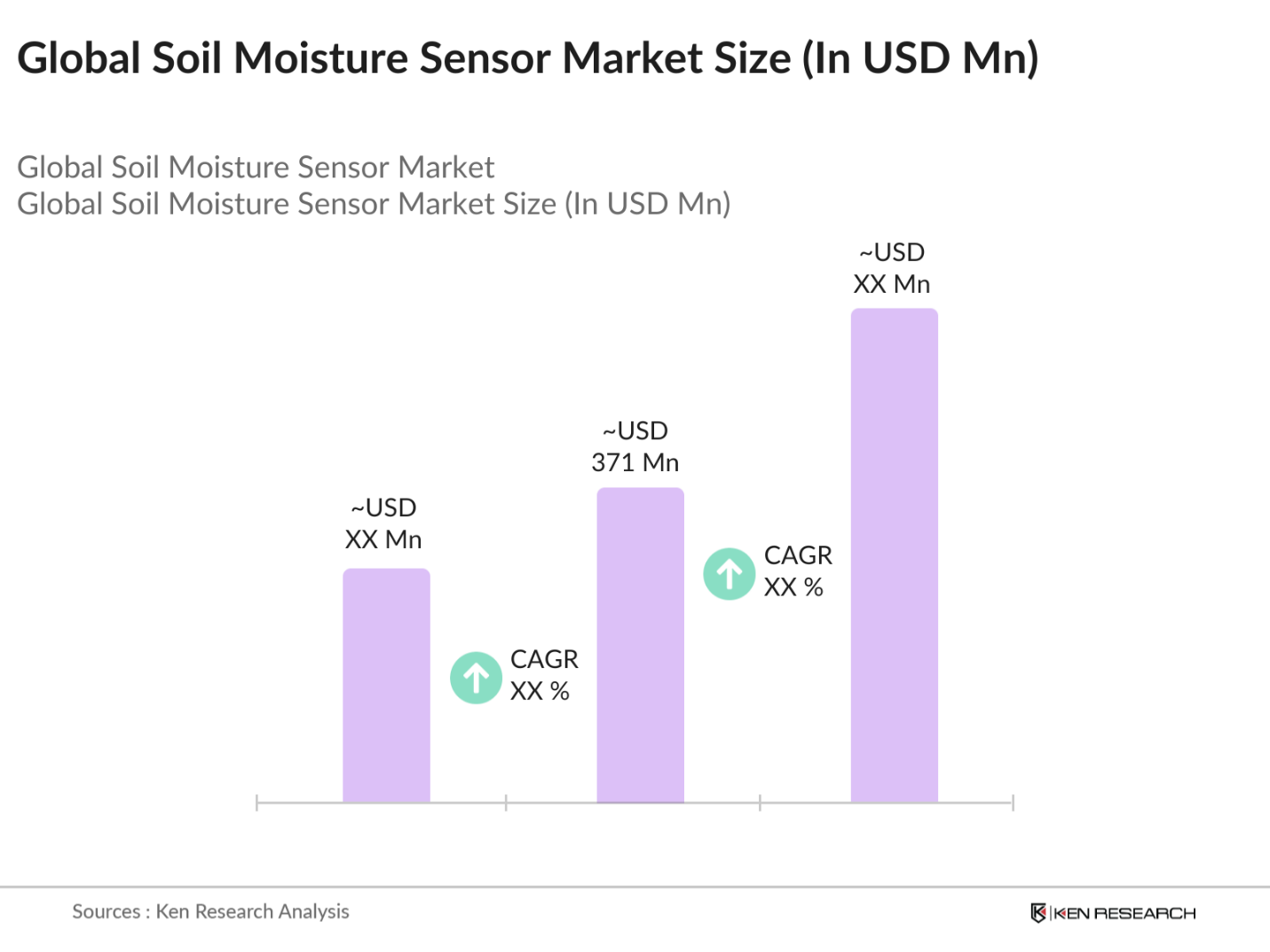

The global soil moisture sensor market is valued at USD 371 million, based on a five-year historical analysis. The growth of this market is primarily driven by the increasing need for precision agriculture and the rising awareness of water conservation techniques, especially in regions facing water scarcity.

Key challenges include high initial investment costs and limited adoption in developing regions, where farming practices may not yet support high-tech solutions like moisture sensors.

Major players include The Toro Company, Campbell Scientific, Inc., Decagon Devices, Inc., Delta-T Devices Ltd, and Sentek Technologies, each driving market innovation through advanced sensor technology.

Growth drivers include the rise of precision farming, government support for water conservation, and technological advancements such as IoT integration with soil moisture sensors.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.