Global Space Exploration Market Outlook to 2030

Region:Global

Author(s):Naman Rohilla

Product Code:KROD11271

Region:Global

Author(s):Naman Rohilla

Product Code:KROD11271

December 2024

94

The Global Space Exploration Market is highly competitive, with influence exerted by leading space agencies and private companies. This consolidation underscores the pivotal role these entities play in pioneering space technologies and advancing space exploration capabilities.

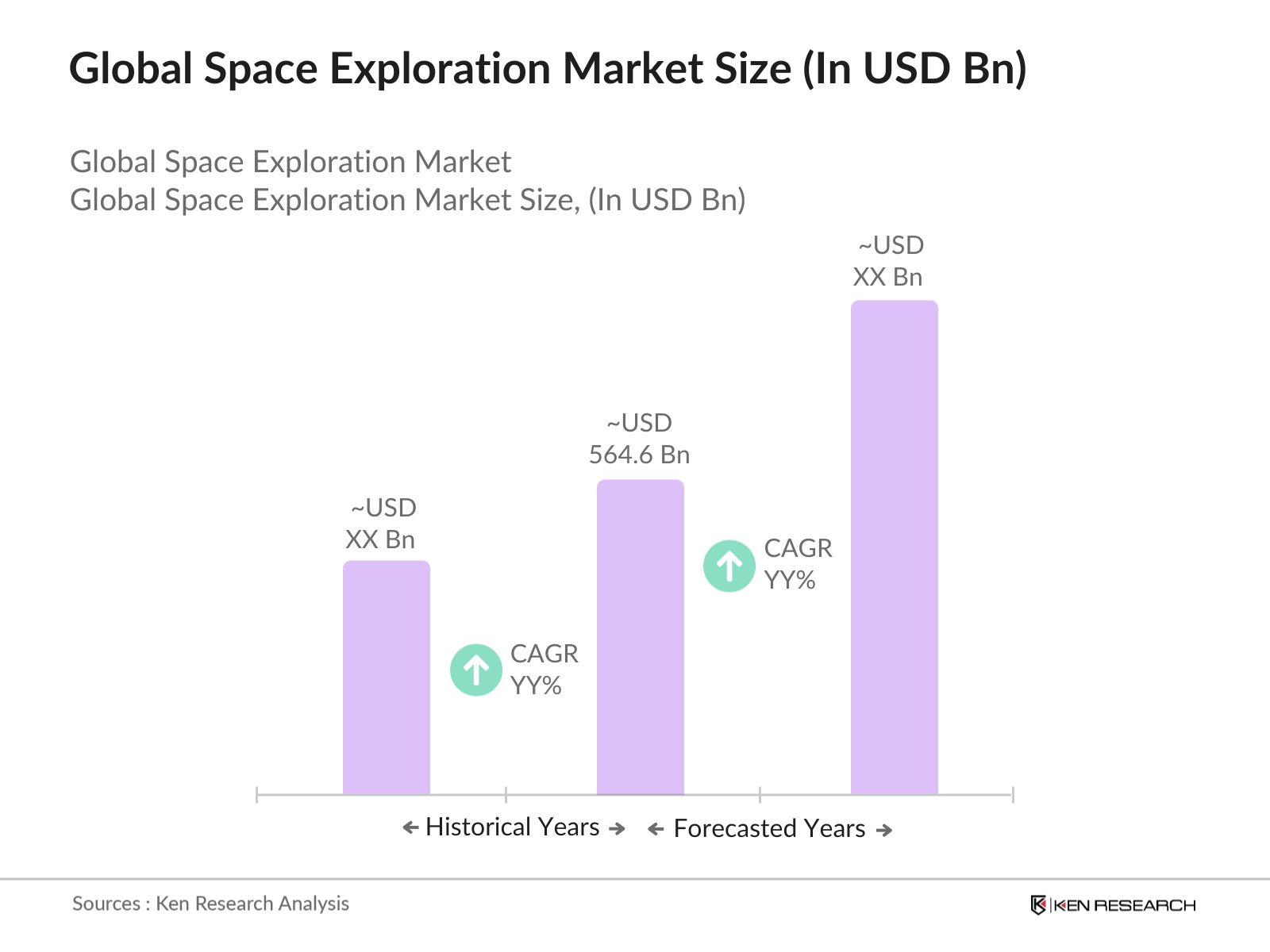

Over the next five years, the Global Space Exploration Market is expected to experience robust growth, driven by advancements in reusable rocket technology, deep-space propulsion systems, and international collaborations. The increasing involvement of private sector players in space tourism, satellite communications, and resource extraction will further enhance market expansion. Furthermore, emerging economies are also beginning to invest in space exploration, suggesting an accelerated global shift towards establishing a more inclusive space economy.

|

By Mission Type |

Lunar Exploration |

|

By End User |

Government & Space Agencies |

|

By Technology |

Propulsion Systems |

|

By Application |

Earth Observation |

|

By Region |

North America |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers (Funding from Government & Private Sectors, Technological Advancements, Growing Interest in Commercial Space Ventures)

3.1.1 Increased Funding for Lunar Missions

3.1.2 Rise in Deep Space Exploration Programs

3.1.3 Growth in Satellite Constellations for Communication

3.1.4 Expanding Commercial Sector

3.2 Market Challenges (High Costs, Regulatory Hurdles, Limited Launch Capabilities)

3.2.1 Technical Complexities in Deep Space Missions

3.2.2 Financial Constraints for Smaller Enterprises

3.2.3 International Space Regulations

3.2.4 Resource Scarcity and Management

3.3 Opportunities (International Partnerships, New Horizons in Space Tourism, Mining in Space)

3.3.1 Emerging Market in Space Tourism

3.3.2 Advancements in Space Mining for Resources

3.3.3 Collaborations for Manned Space Missions

3.4 Trends (Reusable Rockets, Miniaturization in Satellites, AI and Robotics in Space Missions)

3.4.1 Rising Demand for Reusable Launch Vehicles

3.4.2 Increased Use of CubeSats

3.4.3 AI in Spacecraft and Rovers

3.5 Government Regulations (Space Debris Management, Mission Licensing, National & International Policies)

3.5.1 National Space Policies

3.5.2 Licensing and Mission Control Requirements

3.5.3 International Treaties on Space Activities

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem (Space Agencies, Private Companies, Investors)

3.8 Porters Five Forces Analysis

3.9 Competitive Ecosystem

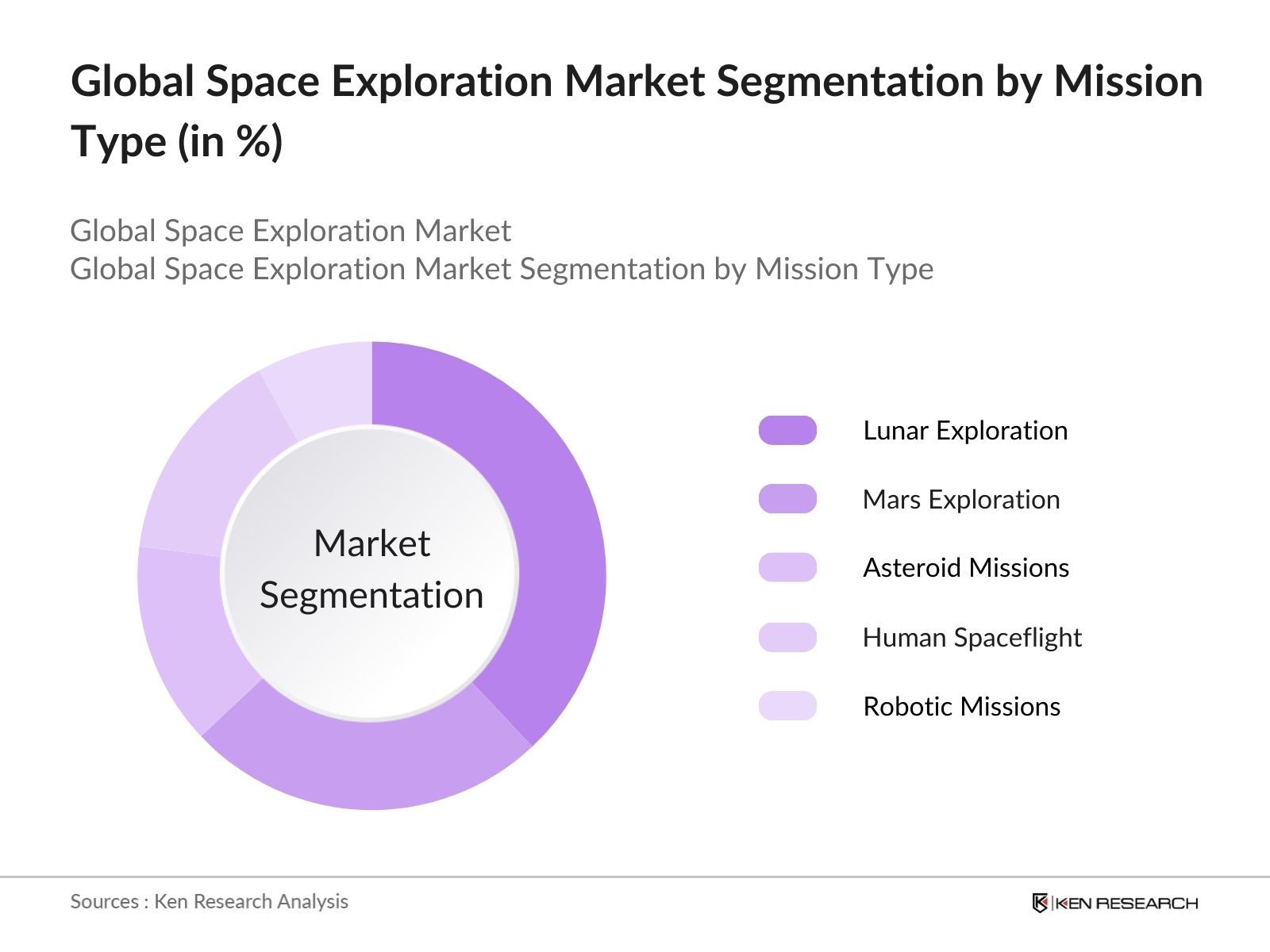

4.1 By Mission Type (In Value %)

4.1.1 Lunar Exploration

4.1.2 Mars Exploration

4.1.3 Asteroid Missions

4.1.4 Human Spaceflight

4.1.5 Robotic Missions

4.2 By End User (In Value %)

4.2.1 Government & Space Agencies

4.2.2 Private Sector Companies

4.2.3 Research Institutes

4.2.4 Commercial Enterprises

4.3 By Technology (In Value %)

4.3.1 Propulsion Systems

4.3.2 Spacecraft and Satellite Manufacturing

4.3.3 Ground Operations and Launch Facilities

4.3.4 Communication Systems

4.4 By Application (In Value %)

4.4.1 Earth Observation

4.4.2 Communication and Navigation

4.4.3 National Defense

4.4.4 Scientific Research

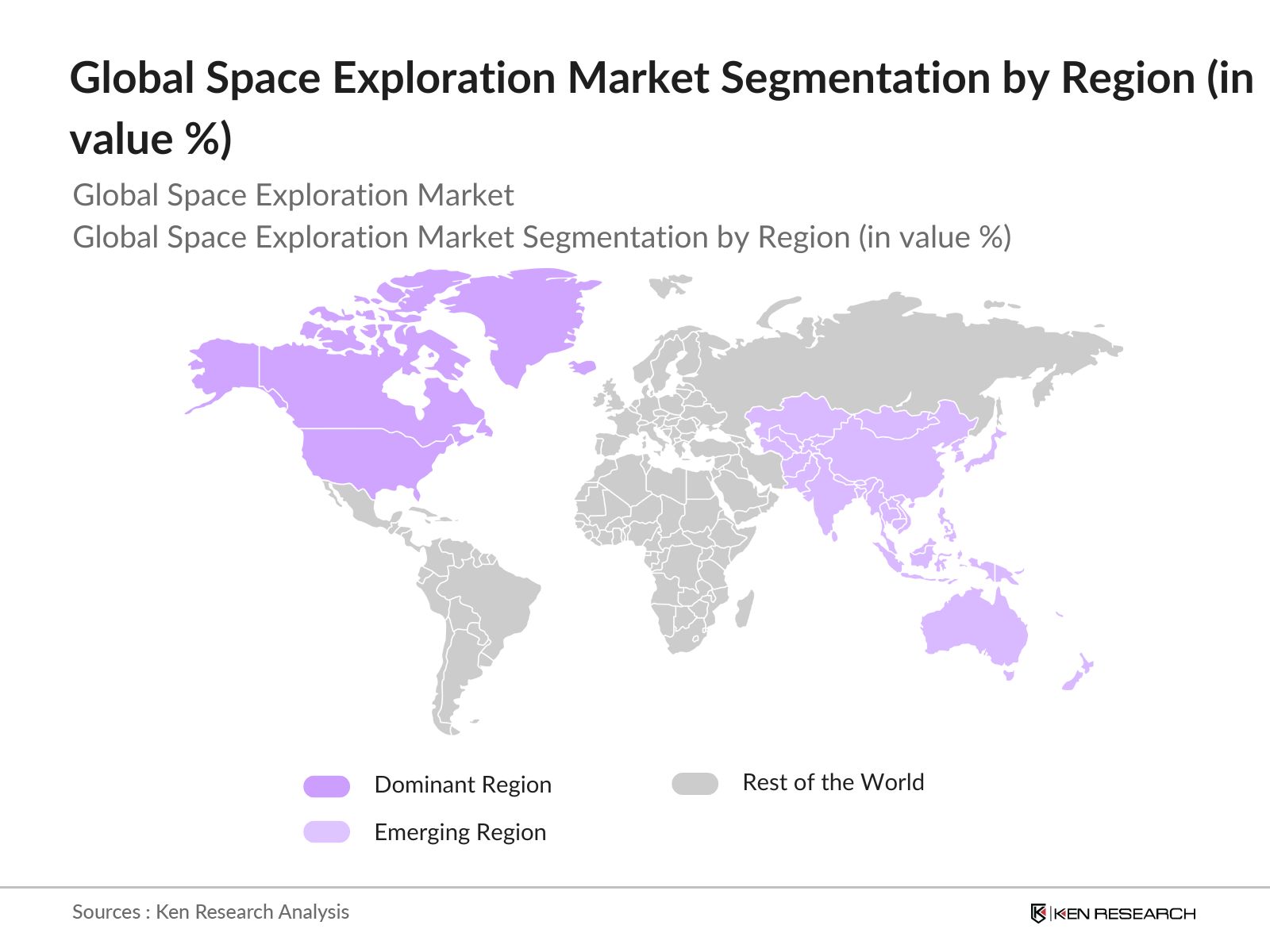

4.5 By Region (In Value %)

4.5.1 North America

4.5.2 Europe

4.5.3 Asia-Pacific

4.5.4 Latin America

4.5.5 Middle East & Africa

5.1 Detailed Profiles of Major Companies

5.1.1 SpaceX

5.1.2 NASA

5.1.3 Roscosmos

5.1.4 European Space Agency (ESA)

5.1.5 China National Space Administration (CNSA)

5.1.6 Blue Origin

5.1.7 Lockheed Martin

5.1.8 Boeing

5.1.9 Northrop Grumman

5.1.10 Rocket Lab

5.1.11 Virgin Galactic

5.1.12 Planet Labs

5.1.13 Sierra Nevada Corporation

5.1.14 Arianespace

5.1.15 ISRO (Indian Space Research Organisation)

5.2 Cross Comparison Parameters (Launch Capabilities, Partnerships, Mission Success Rate, R&D Investment, Revenue, Technological Expertise, Workforce, Market Reach)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Government Funding

5.8 Private Equity and Venture Capital Funding

6.1 International Space Laws

6.2 Space Traffic Management

6.3 Compliance and Licensing

6.4 Debris Mitigation Requirements

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Mission Type (In Value %)

8.2 By End User (In Value %)

8.3 By Technology (In Value %)

8.4 By Application (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Opportunity Analysis

9.3 Strategic Partnership Recommendations

9.4 Market Expansion Strategy

Disclaimer Contact UsThis initial phase involves a comprehensive mapping of key stakeholders within the Global Space Exploration Market. Utilizing extensive secondary and proprietary data sources, we identify critical market influencers such as private companies, governmental agencies, and new entrants into space technology.

In this step, historical data for market dynamics, mission expenditures, and technological advancements are compiled and analyzed. This includes assessing the penetration rates of governmental vs. private sector projects and the annual revenue generation from each segment.

Market assumptions are validated through direct consultation with industry experts, including space agency officials and leading private-sector executives, to gain operational and strategic insights into market trends and growth factors.

The concluding phase synthesizes findings from primary and secondary research, culminating in a comprehensive and validated report. This process involves cross-referencing data with industry standards, ensuring that final outputs provide actionable insights for stakeholders.

The Global Space Exploration Market is valued at USD 564.6 billion, largely fueled by governmental investments and the expansion of private sector missions into space.

Challenges include high mission costs, complex regulatory requirements, and limited launch capabilities. Additionally, there are technological constraints that limit certain deep-space explorations.

Key players include NASA, SpaceX, Roscosmos, ESA, and CNSA. These entities lead due to their extensive funding, advanced R&D capabilities, and successful track records in space missions.

Growth is driven by substantial government funding, technological advancements, and private sector expansion into areas like space tourism and satellite communications.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.