Global Tractor Implements Market Outlook to 2030

Region:Global

Author(s):Naman Rohilla

Product Code:KROD9344

December 2024

86

About the Report

Global Tractor Implements Market Overview

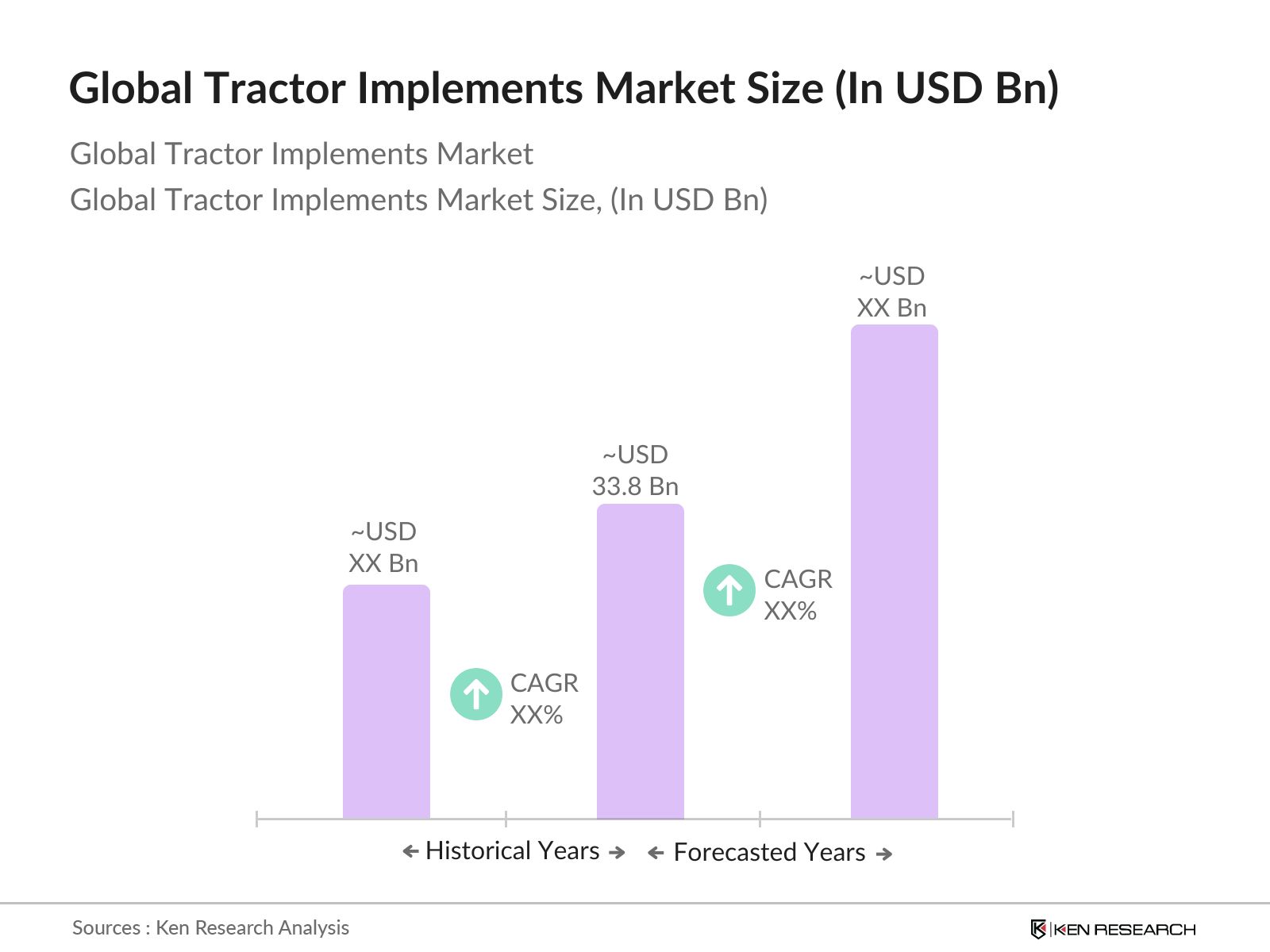

- The global tractor implements market is valued at USD 33.8 billion, based on an extensive five-year historical analysis. Its growth is driven primarily by increasing agricultural mechanization, government subsidies on agricultural equipment, and a surge in demand for high-efficiency farming practices. The market is witnessing robust investments in advanced technology and precision farming tools, enhancing productivity and reducing labor dependence.

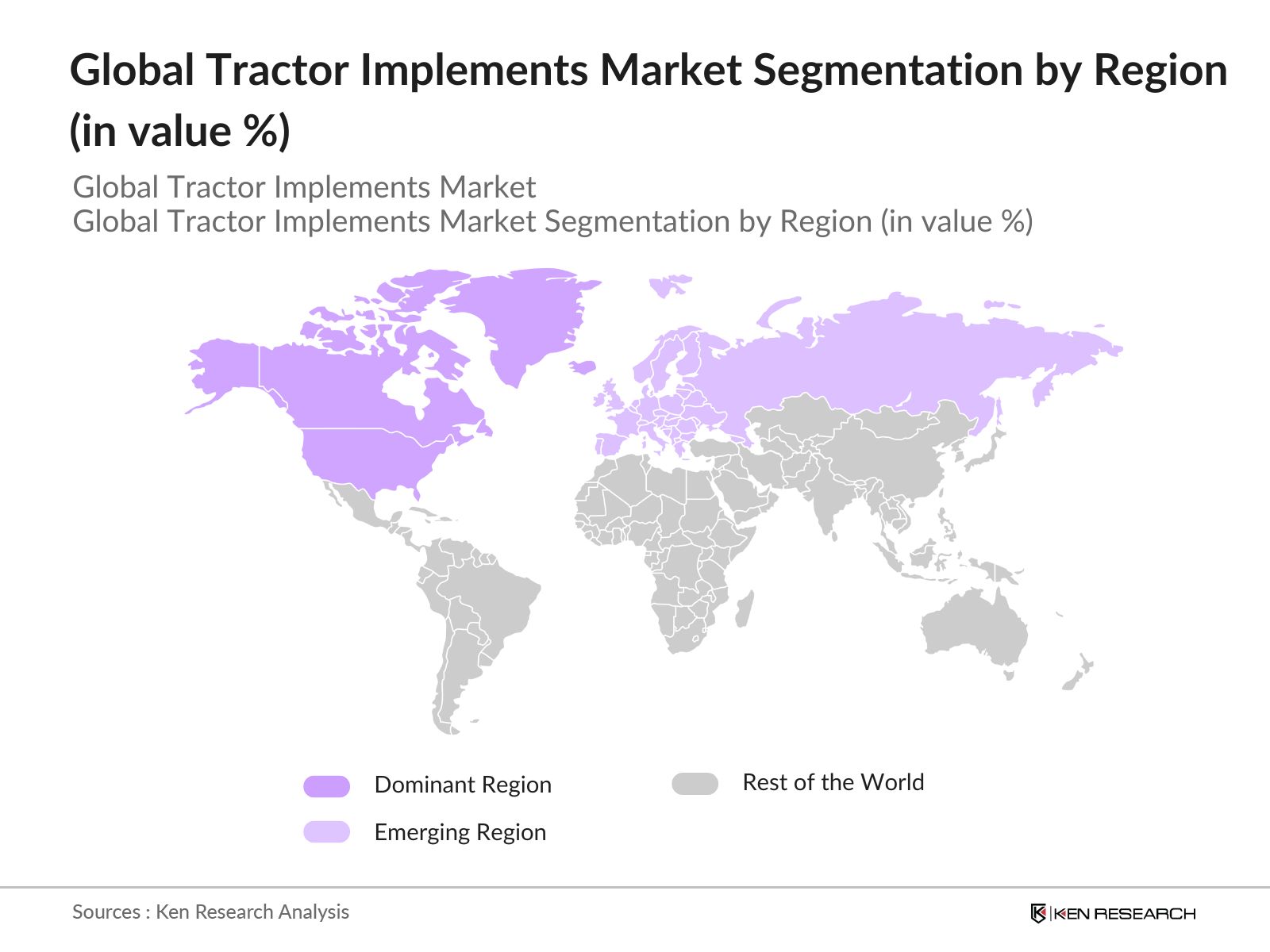

- Regions such as North America and Europe dominate the global tractor implements market, with extensive adoption of mechanized farming and high demand for advanced machinery. North Americas dominance is largely due to its well-established agricultural infrastructure and substantial support from government programs. Europe follows with similar trends, bolstered by government initiatives promoting sustainable agriculture and reducing environmental impact.

- Stringent emission standards are being implemented to reduce the environmental impact of agricultural machinery. In 2024, the EPA introduced new regulations reducing allowable emissions by 20% for all new agricultural equipment, influencing the development and adoption of cleaner tractor implements.

Global Tractor Implements Market Segmentation

By Implement Type: The tractor implements market is segmented by implement type into Plows, Harrows, Seeders and Planters, Sprayers, and Balers. Recently, Plows hold a dominant market share due to their essential role in land preparation. They remain critical in enhancing soil aeration and preparing the land for optimal seed placement. The demand for plows is bolstered by their compatibility with precision agriculture practices, allowing farmers to achieve high crop yield and efficient water use.

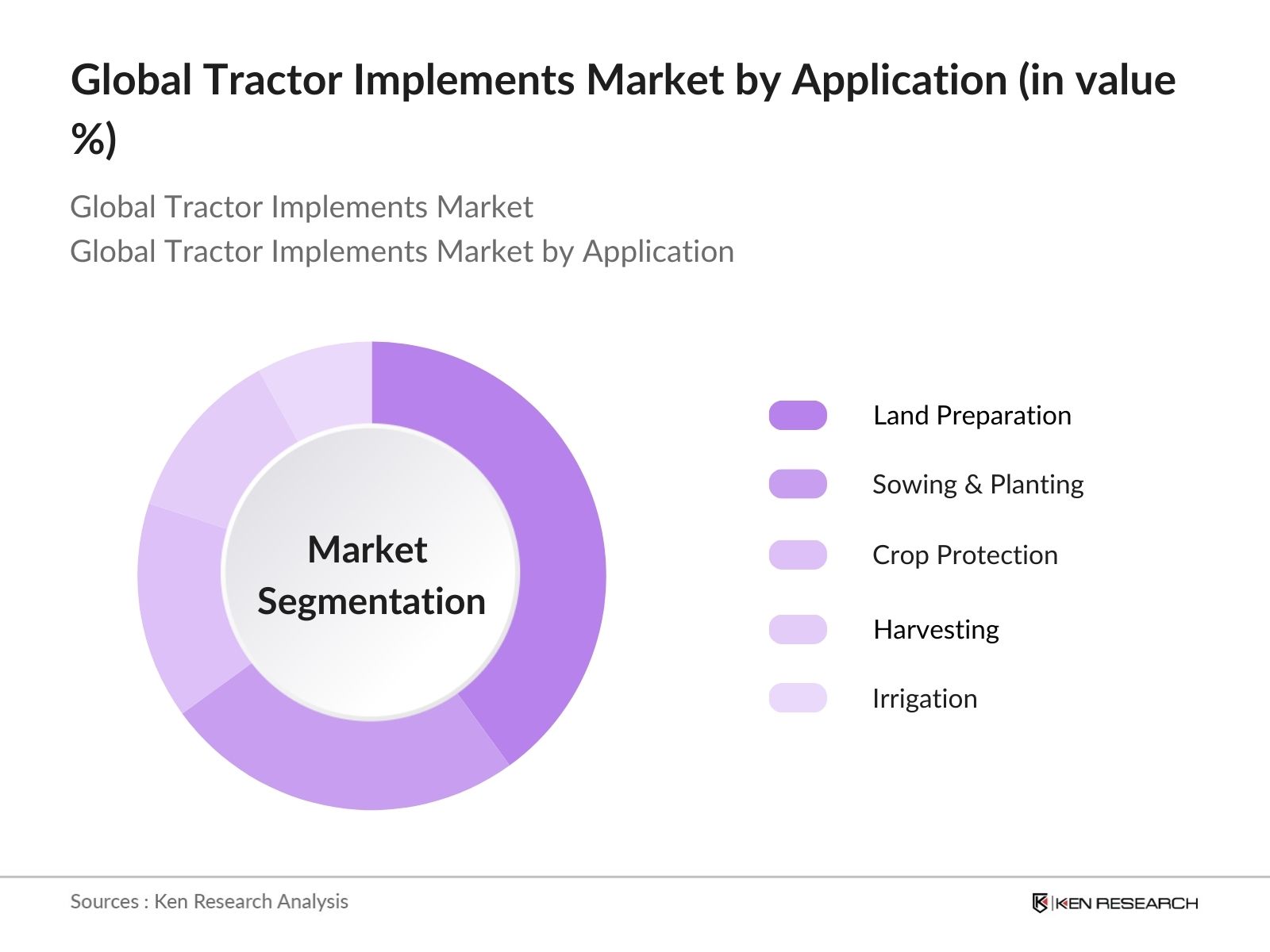

By Application: The market is segmented by application into Land Preparation, Sowing and Planting, Crop Protection, Harvesting, and Irrigation. Land Preparation has emerged as a dominant application segment. This dominance is attributed to the critical role of soil preparation in ensuring higher crop yields, especially as precision agriculture techniques gain traction. Moreover, government subsidies and agricultural grants support farmers in purchasing advanced equipment for this essential step.

By Region: The market is segmented by region into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America is the leading region, driven by extensive mechanization of farms and favorable government policies supporting modern farming equipment. High investment in technology, particularly in the U.S., supports the demand for advanced implements, enabling farmers to increase productivity and reduce dependency on manual labor.

Global Tractor Implements Market Competitive Landscape

The global tractor implements market is dominated by a few major players, including industry giants such as John Deere, CNH Industrial, and Kubota Corporation, alongside emerging regional players in Asia and Europe. This competitive landscape indicates a consolidation of market power among key players who are advancing with product innovations, strategic partnerships, and regional expansions.

Global Tractor Implements Market Analysis

Market Growth Drivers

- Mechanization in Agriculture: The mechanization of agriculture is a significant driver in the tractor implements market. In 2023, the World Bank reported that countries like India allocated USD 6.7 billion to agricultural mechanization, aiming to enhance farming efficiency. Similarly, the United States Department of Agriculture (USDA) invested USD 500 million in 2024 to support farm machinery upgrades, reflecting a strategic move to boost productivity and reduce labor dependency. These investments are crucial in driving the adoption of advanced tractor implements.

- Increase in Crop Production Demand: Increasing global demand for food drives the need for efficient agricultural practices. According to the Food and Agriculture Organization (FAO), global crop production needs to rise by 70% by 2050 to meet the population growth. Investments in tractor implements are crucial for achieving this, as evidenced by a 60% increase in the adoption of mechanized sowing and harvesting tools in Southeast Asia as of 2024.

- Technological Advancements in Implements: Technological advancements significantly influence the tractor implements market. Innovations such as GPS tracking and AI-based monitoring systems have been integrated into implements, improving precision and efficiency. In 2023, the International Finance Corporation (IFC) reported that the adoption of such technologies in developing countries increased by 30%, indicating a trend toward smarter agriculture.

Market Challenges

- High Initial Investment Costs: The high cost of advanced agricultural equipment poses a significant challenge. According to the World Bank, the average initial investment for precision farming equipment, including tractor implements, exceeded USD 20,000 per unit in major agricultural nations like Brazil and China in 2023, which can be prohibitive for small to medium-sized farms.

- Shortage of Skilled Labor for Modern Equipment: The shift towards technologically advanced tractor implements requires skilled operators. In 2024, a USDA survey indicated a 25% shortage in qualified agricultural machinery operators in the United States. This shortage hinders the effective utilization of sophisticated farming equipment, impacting productivity.

Global Tractor Implements Market Future Outlook

Over the next few years, the global tractor implements market is expected to experience steady growth, fueled by the adoption of advanced agricultural technologies, increased government support for sustainable farming practices, and an upward trend in precision farming. Emerging economies, particularly in the Asia-Pacific region, are anticipated to contribute to this growth through substantial investments in farm mechanization and infrastructure development.

Market Opportunities

- Precision Agriculture Integration: Integration of precision agriculture technologies into tractor implements presents significant growth opportunities. For example, the deployment of GPS and sensor technology in implements has led to a 20% increase in crop yields in regions like the Midwest USA as of 2023, demonstrating the potential for market expansion through technological integration.

- Increased Farm Consolidation: Farm consolidation trends offer opportunities for the tractor implements market. As farms merge to form larger operational units, the demand for high-capacity agricultural machinery rises. In 2024, the USDA reported a 30% increase in the sales of large-scale farming implements due to farm consolidations in North America.

Scope of the Report

|

Implement Type |

Plows Harrows Seeders and Planters Sprayers Balers |

|

Application |

Land Preparation Sowing and Planting Crop Protection Harvesting Irrigation |

|

Mechanism Type |

Mechanical Implements Hydraulic Implements Pneumatic Implements |

|

Power Source |

Tractor-Powered Implements Self-Propelled Implements |

|

Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

Products

Key Target Audience

Farmers and Agricultural Cooperatives

Agricultural Machinery Distributors

Government and Regulatory Bodies (USDA, EU Agricultural Policy Office)

Precision Agriculture Solution Providers

Investor and Venture Capitalist Firms

Agricultural Research Institutions

Regional Farming Associations

Supply Chain Management Companies

Companies

Players Mentioned in the Report

John Deere

CNH Industrial

Kubota Corporation

AGCO Corporation

Mahindra & Mahindra

TAFE

Escorts Group

CLAAS

SDF Group

JCB

Table of Contents

1. Global Tractor Implements Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. Global Tractor Implements Market Size (In USD Billion)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Global Tractor Implements Market Analysis

3.1 Growth Drivers

3.1.1 Mechanization in Agriculture

3.1.2 Government Subsidies for Agricultural Equipment

3.1.3 Increase in Crop Production Demand

3.1.4 Technological Advancements in Implements

3.2 Market Challenges

3.2.1 High Initial Investment Costs

3.2.2 Shortage of Skilled Labor for Modern Equipment

3.2.3 Fluctuations in Raw Material Prices

3.3 Opportunities

3.3.1 Precision Agriculture Integration

3.3.2 Increased Farm Consolidation

3.3.3 Expansion into Emerging Economies

3.4 Trends

3.4.1 Adoption of Autonomous Implements

3.4.2 Sustainable and Eco-Friendly Implements

3.4.3 Increased Use of Smart and Connected Implements

3.5 Government Regulation

3.5.1 Emission Standards for Agricultural Equipment

3.5.2 Safety and Operational Standards

3.5.3 Agricultural Subsidy Programs

3.5.4 Import Tariffs and Export Policies

3.6 SWOT Analysis

3.7 Value Chain Analysis

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape and Ecosystem

4. Global Tractor Implements Market Segmentation

4.1 By Implement Type (In Value %)

4.1.1 Plows

4.1.2 Harrows

4.1.3 Seeders and Planters

4.1.4 Sprayers

4.1.5 Balers

4.2 By Application (In Value %)

4.2.1 Land Preparation

4.2.2 Sowing and Planting

4.2.3 Crop Protection

4.2.4 Harvesting

4.2.5 Irrigation

4.3 By Mechanism Type (In Value %)

4.3.1 Mechanical Implements

4.3.2 Hydraulic Implements

4.3.3 Pneumatic Implements

4.4 By Power Source (In Value %)

4.4.1 Tractor-Powered Implements

4.4.2 Self-Propelled Implements

4.5 By Region (In Value %)

4.5.1 North America

4.5.2 Europe

4.5.3 Asia-Pacific

4.5.4 Latin America

4.5.5 Middle East & Africa

5. Global Tractor Implements Market Competitive Analysis

5.1 Profiles of Major Companies

5.1.1 John Deere

5.1.2 CNH Industrial

5.1.3 Mahindra & Mahindra

5.1.4 Kubota Corporation

5.1.5 AGCO Corporation

5.1.6 TAFE

5.1.7 Escorts Group

5.1.8 CLAAS

5.1.9 SDF Group

5.1.10 JCB

5.1.11 Iseki & Co., Ltd.

5.1.12 Kuhn Group

5.1.13 Yanmar

5.1.14 Maschio Gaspardo

5.1.15 Lemken GmbH & Co. KG

5.2 Cross Comparison Parameters (R&D Expenditure, Manufacturing Facilities, Production Capacity, Geographic Presence, Product Line Diversification, Market Share, Innovation Rate, Pricing Strategy)

5.3 Market Share Analysis

5.4 Strategic Initiatives by Competitors

5.5 Mergers and Acquisitions

5.6 Investment and Funding Analysis

5.7 Venture Capital Influence

5.8 Government Subsidies and Grants

5.9 Private Equity Investments

6. Global Tractor Implements Market Regulatory Framework

6.1 Emission Regulations for Agricultural Machinery

6.2 Safety Standards and Certifications

6.3 Compliance Requirements for Import/Export

6.4 Agricultural Subsidies and Tax Benefits

7. Global Tractor Implements Market Future Market Size (In USD Billion)

7.1 Market Size Projections

7.2 Key Drivers for Future Growth

8. Global Tractor Implements Market Future Segmentation

8.1 By Implement Type (In Value %)

8.2 By Application (In Value %)

8.3 By Mechanism Type (In Value %)

8.4 By Power Source (In Value %)

8.5 By Region (In Value %)

9. Global Tractor Implements Market Analysts Recommendations

9.1 Total Addressable Market Analysis

9.2 Customer Demographics Analysis

9.3 Marketing and Distribution Strategies

9.4 Identification of Growth Opportunities

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial step involves mapping the key stakeholders within the global tractor implements market. This includes an extensive review of secondary data sources, encompassing industry reports and proprietary databases, to identify the primary drivers, challenges, and trends shaping the market.

Step 2: Market Analysis and Construction

Historical data from credible sources is analyzed to assess the market's size and growth trajectory. This step involves segment-level analysis to understand the adoption rates of various tractor implements across different applications and regions.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through interviews with industry experts and stakeholders, including manufacturers, distributors, and agricultural advisors. These consultations offer insights into operational dynamics and help corroborate secondary research findings.

Step 4: Research Synthesis and Final Output

The final step synthesizes primary and secondary research insights, ensuring accuracy and validity. The results are presented in a comprehensive report format, including market size, segmentation, competitive landscape, and actionable recommendations.

Frequently Asked Questions

01. How big is the Global Tractor Implements Market?

The global tractor implements market is valued at USD 33.8 billion, driven by technological advancements in agriculture and increased demand for high-efficiency farming equipment.

02. What are the challenges in the Global Tractor Implements Market?

Challenges in the market include high initial costs of advanced machinery, raw material price volatility, and a lack of skilled labor to operate high-tech equipment.

03. Who are the major players in the Global Tractor Implements Market?

Major players include John Deere, CNH Industrial, Kubota Corporation, AGCO Corporation, and Mahindra & Mahindra, each with a significant market presence and extensive product portfolio.

04. What are the growth drivers of the Global Tractor Implements Market?

The market growth is driven by factors such as government subsidies, increased mechanization, and advancements in precision agriculture, which enhance productivity and reduce labor costs.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.