Global Video Gaming Market Outlook to 2030

Region:Global

Author(s):Rishabh Verma

Product Code:KENGR012

Region:Global

Author(s):Rishabh Verma

Product Code:KENGR012

October 2024

96

The Global Video Gaming Market can be segmented based on several factors:

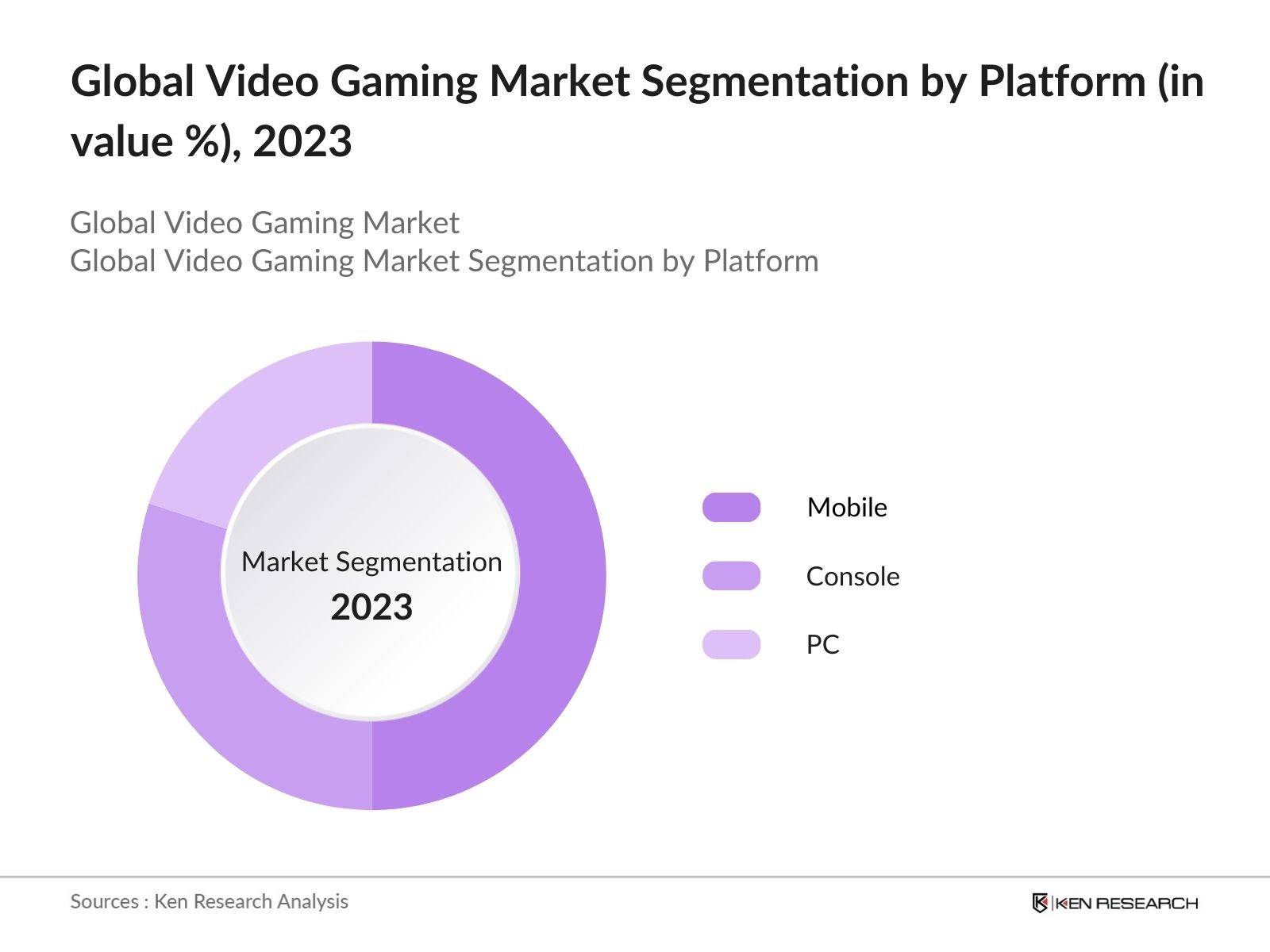

By Platform: Global video gaming market segmentation by platform is divided into mobile, PC and console. In 2023, mobile gaming emerged as the most dominant segment of the global video gaming market, driven by widespread smartphone adoption and the growth of high-speed internet. The convenience of mobile platforms, along with the popularity of casual gaming and in-app purchases, reinforces mobile gaming's leading position.

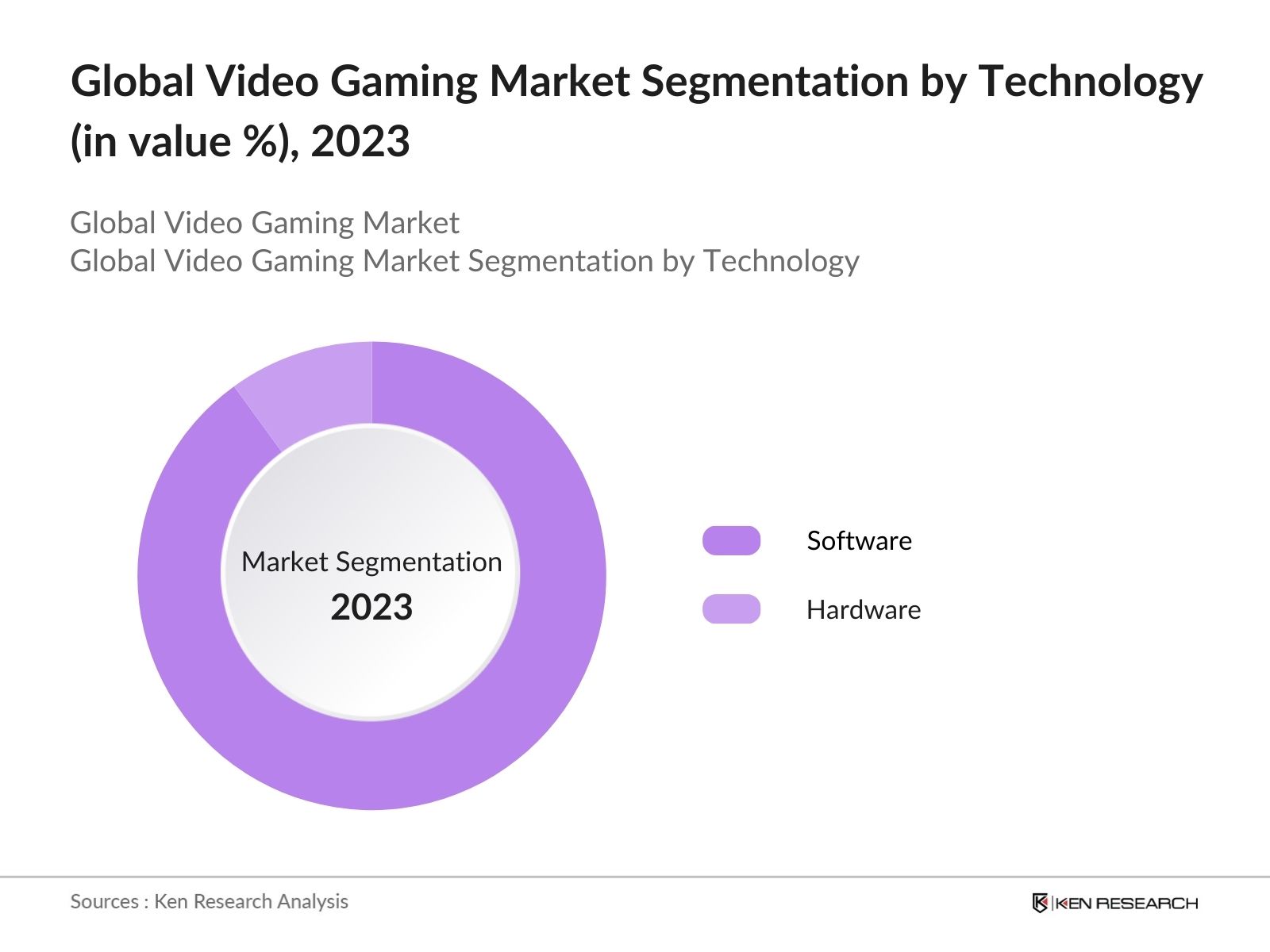

By Technology: In the Global video gaming market segmentation by technology is divided into hardware and software. In 2023, software was the leading segment in the global video gaming market, driven by advancements in game engines, high-quality graphics, and immersive gameplay. The demand for sophisticated development tools and continuous content updates further fueled the growth of the software segment.

| Company | Headquarters | Establishment Year |

|---|---|---|

| Tencent Holdings | Shenzhen, China | 1998 |

| Microsoft (Incl. Activision Blizzard) | California, United States | 2008 |

| Sony Interactive Entertainment | California, United States | 1994 |

| Nintendo | Kyoto, Japan | 1889 |

| NetEase, Inc. | Hangzhou, Zhejiang, China | 1997 |

| Electronic Arts | California, United States | 1982 |

| Take-Two Interactive | New York, United States | 1993 |

| Ubisoft | Paris, France | 1989 |

| Square Enix | Tokyo, Japan | 1975 |

| Roblox Corporation | California, United States | 2004 |

| Bandai Namco Entertainment | Tokyo, Japan | 2006 |

| Sega Corporation | Tokyo, Japan | 1960 |

Global Video Gaming Market Growth Drivers:

Global Video Gaming Market Challenges:

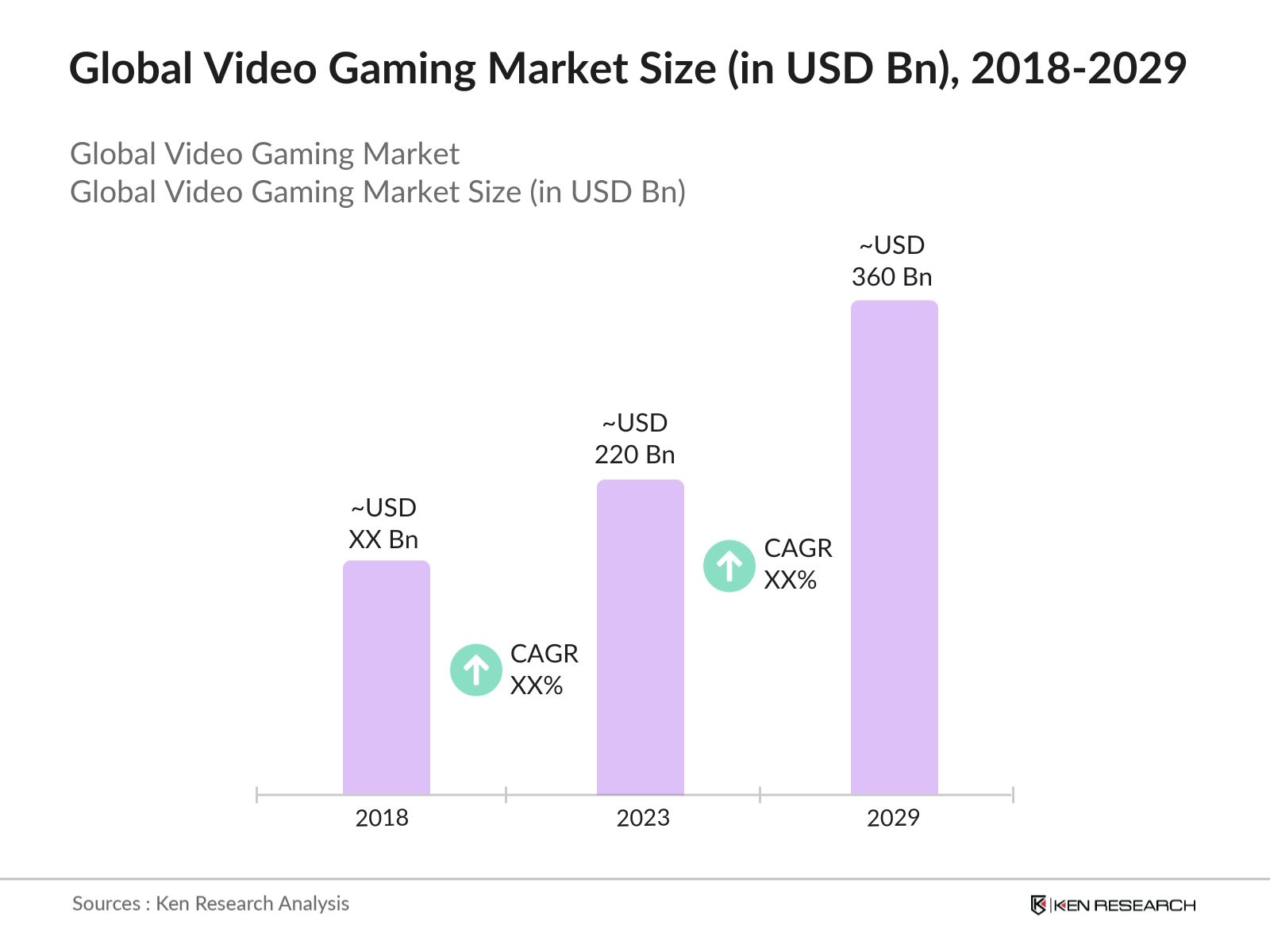

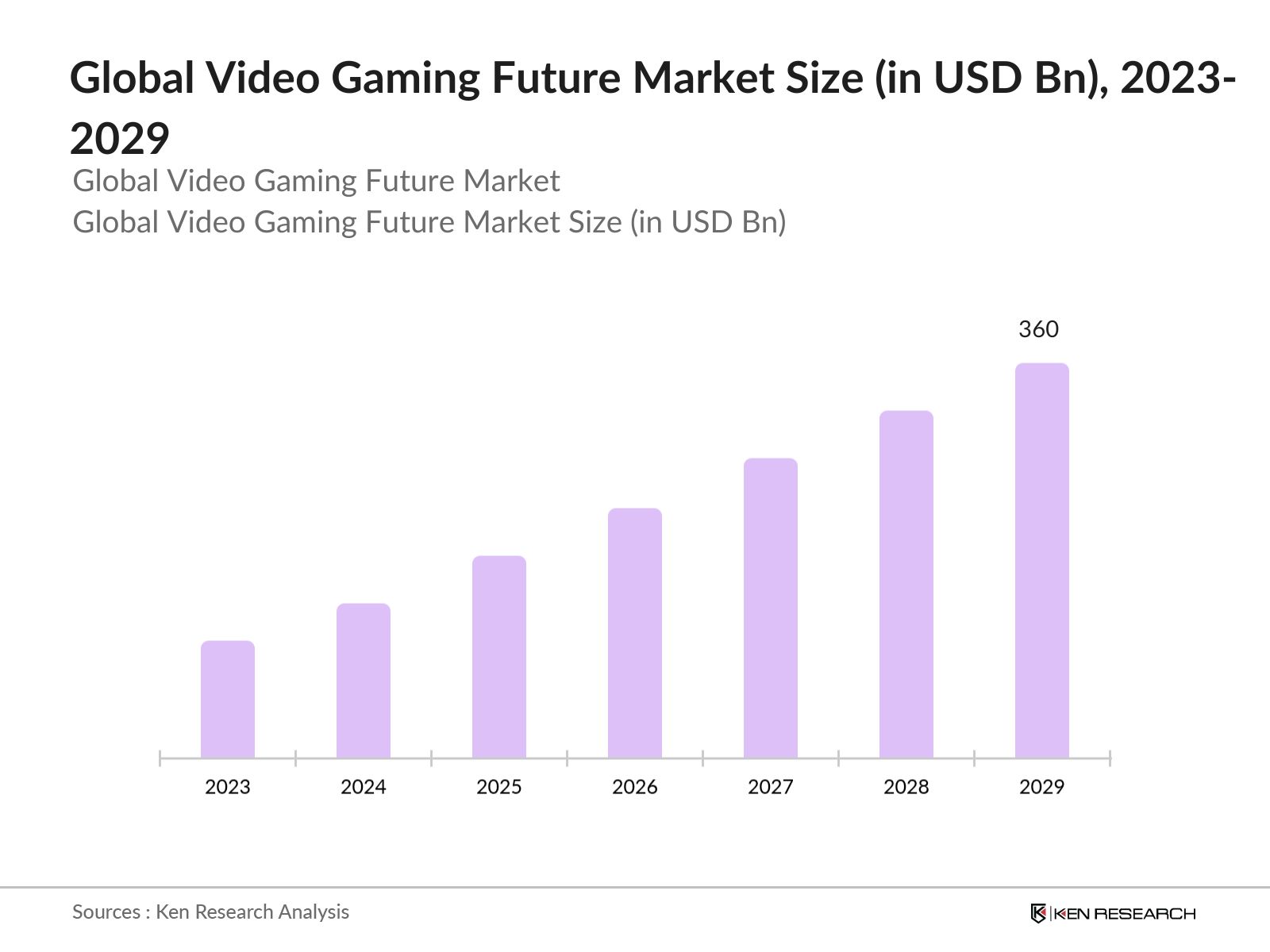

The Global Video Gaming market is expected to reach USD 360 Bn by 2029 driven by increasing penetration of 5G technology, the rise of cloud gaming services, and the expansion of the gaming audience across emerging markets. Additionally, innovations in virtual and augmented reality are expected to open new avenues for immersive gaming experiences.

Future Market Trends

|

By Region |

North America Europe APAC Latin America MEA |

|

By Platform |

Mobile Console PC |

|

By Technology |

Software Hardware |

1.1 Global Entertainment and Media Market

1.2 Global Video Gaming Market

2.1 Overview of Global Economics

2.2 Overview of Global Entertainment and Media Industry

2.3 Global Entertainment and Media (Console Games, PC Games, Mobile Games, And Online Gaming) Revenue

2.4 Global Video Gaming (Offline and Online)

3.1 Global Video Gaming Market Ecosystem: Game Developer/Publisher

3.2 Global Video Gaming Market Ecosystem: Game Distributor (Digital)

3.3 Global Video Gaming Market Ecosystem: Gaming Console Manufacturers

3.4 Global Video Gaming Market Value Chain

3.5 Global Video Gaming Market Opportunity

3.6 Global Video Gaming Market Gamers Demographics

3.7 Global Video Gaming Market - Global Video Gaming Statistics

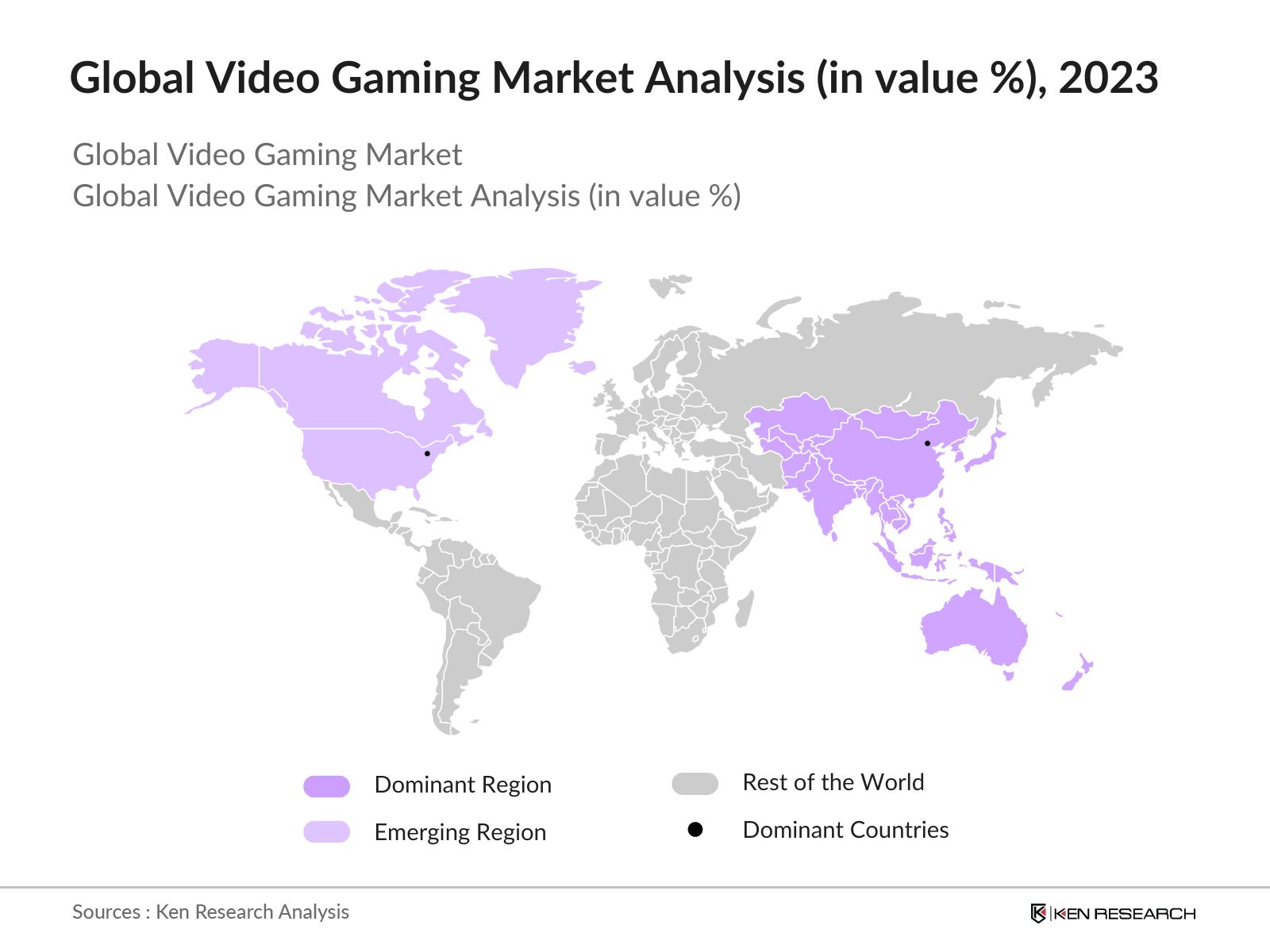

5.1 Global Video Gaming Market Segmentation by Region (in value %), 2018-2023

5.2 Global Video Gaming Market Segmentation by Business Model (in value %), 2018-2023

5.3 Global Video Gaming Market Segmentation by Platform (in value %), 2018-2023

5.4 Global Video Gaming Market Segmentation by Technology (in value%), 2018-2023

6.1 Global Video Gaming Market Share Analysis

6.2 Global Video Gaming Market Heat Map Analysis

6.3 Global Video Gaming Market Cross Comparison

6.4 Global Video Gaming Market Comparison Matrix

7.1 Global Video Gaming Market Growth Drivers

7.2 Global Video Gaming Market Challenges

7.3 Global Video Gaming Market Trends

7.4 Global Video Gaming Market Case Studies

7.5 Global Video Gaming Market Strategic Initiatives

5.1 Global Video Gaming Future Market Segmentation by Region (in value %), 2023-2029

5.2 Global Video Gaming Future Market Segmentation by Business Model (in value %), 2023-2029

5.3 Global Video Gaming Future Market Segmentation by Platform (in value %), 2023-2029

5.4 Global Video Gaming Future Market Segmentation by Technology (in value%), 2023-2029

Identified a comprehensive ecosystem of international and local players in the video games industry. This step involved mapping out key stakeholders, including gaming software development companies, publishers, distributors, and content creators. The objective was to establish a clear understanding of the industry's landscape and the various entities operating within it.

Conducted Computer-Assisted Telephone Interviews (CATIs) with key industry stakeholders, including gaming software developers, publishers, distributors, and content creators. The interviews aimed to collect detailed data on operating and financial metrics, such as product portfolios (gaming titles and genres), value chains, gross profit margins, and segment revenues by distribution channel. The discussions also covered future strategies and additional value-adding insights. After data collection, a bottom-to-top approach was used to assess country-level and regional trends, as well as market shares by platform and technology. The market size was determined based on revenues from major players and their global market shares.

Employed a combination of bottom-to-top and top-to-bottom approaches to evaluate overall historical and forecasted revenue figures. This comprehensive analysis included validating the findings through sanity checks with industry veterans, gaming professionals, publishing platforms, and proxy variables. These validation steps ensured the accuracy and reliability of the final revenue figures and provided a robust understanding of the market's financial dynamics.

The global video gaming market was valued at USD 220 Bn in 2023, is driven by increasing popularity of mobile and online gaming, advancements in gaming technology, and the expansion of the gamer demographic, including both casual and professional gamers.

Challenges in global video gaming market include regulatory restrictions such as gaming time limits for minors, cybersecurity threats with increasing cyber-attacks on gaming platforms, high development costs for producing AAA games, and intellectual property issues leading to legal disputes and financial losses.

Key players in global video gaming market include Tencent Games, Sony Interactive Entertainment, Microsoft Xbox, Nintendo, and Electronic Arts (EA). These companies lead due to their strong portfolios, innovative technologies, strategic partnerships, and substantial market presence.

The global video gaming market is driven by the rise in mobile gaming with a growing number of smartphone users, the expansion of esports attracting a large audience and revenue, the adoption of cloud gaming offering high-quality games on various devices, and the development of VR and AR technologies enhancing immersive gaming experiences.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.