Global Wood Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD2877

Region:Global

Author(s):Shivani Mehra

Product Code:KROD2877

December 2024

85

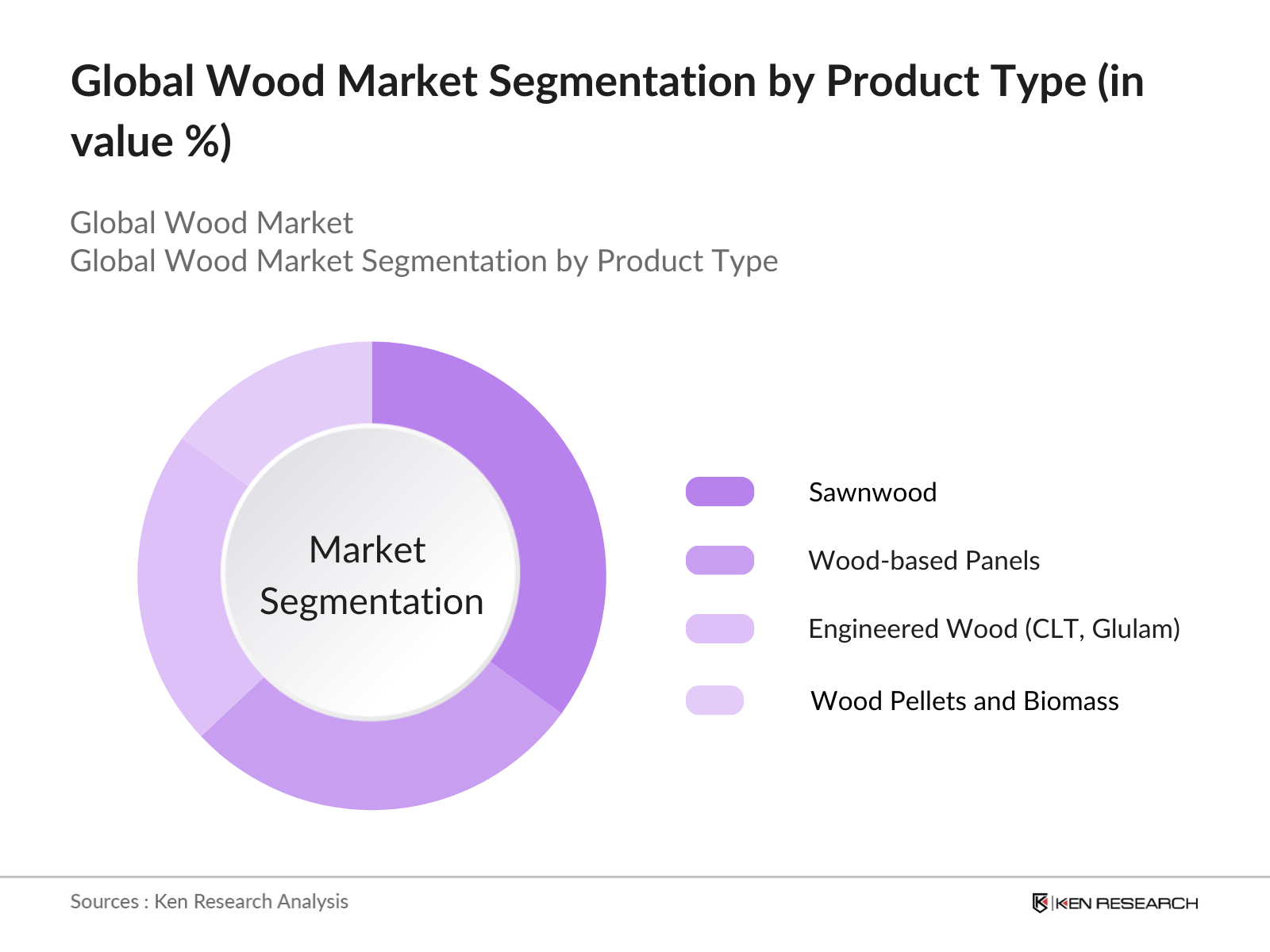

By Product Type: The global wood market is segmented by product type into sawnwood, wood-based panels, engineered wood, and wood pellets. Engineered wood products such as cross-laminated timber (CLT) and glulam have a dominant market share due to their increasing adoption in the construction industry. These products offer superior strength, flexibility, and sustainability compared to traditional wood. Their eco-friendly attributes, along with government incentives for green building practices, have further fueled their growth in regions such as North America and Europe.

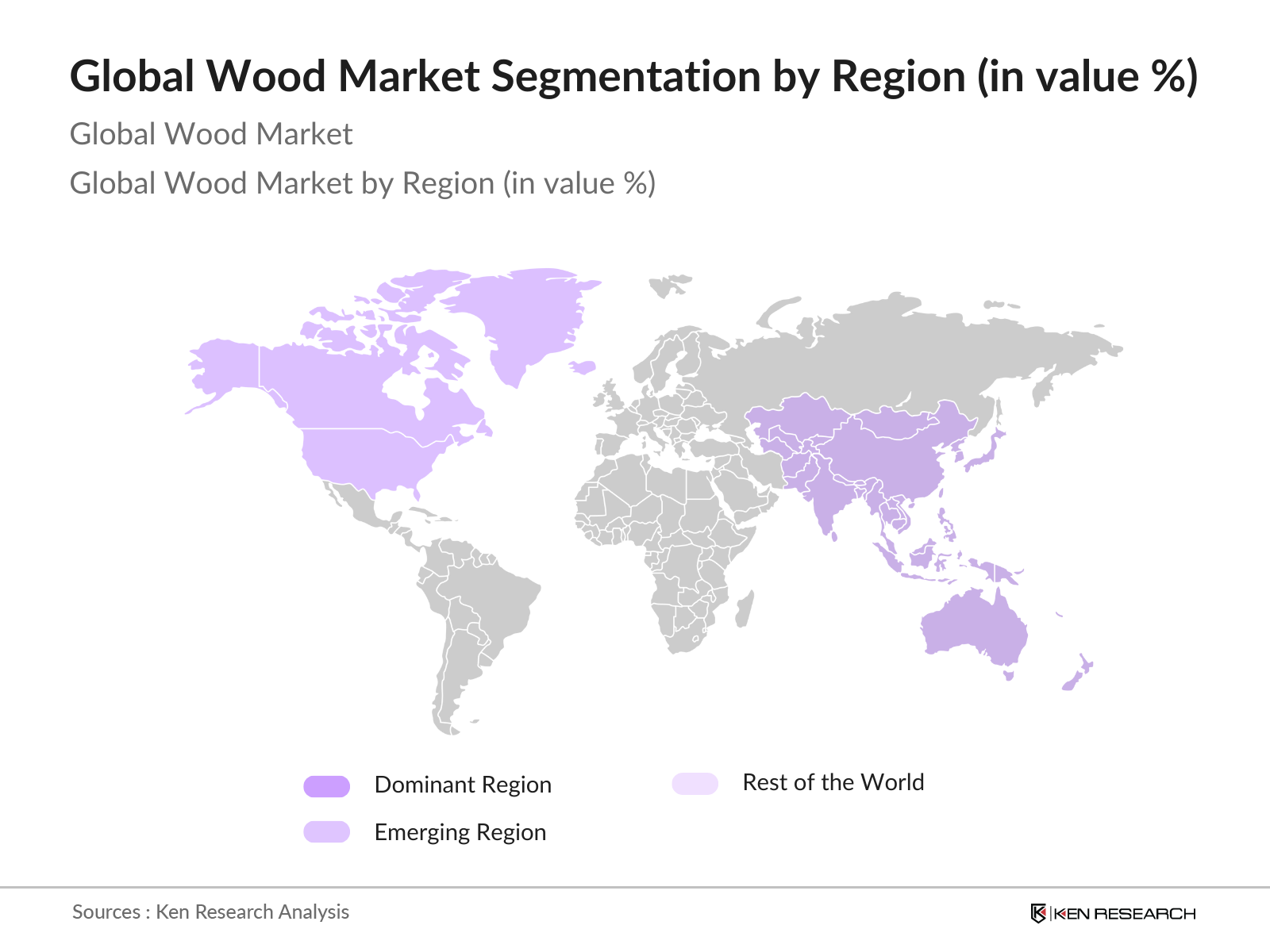

By Region: The global wood market is segmented by region intoAsia-Pacific,North America,Europe,Latin America, andMiddle East & Africa. In 2023, Asia-Pacific emerged as the largest region in the wood products market, followed by North America as the second largest. North America's strong timber industry and vast forest resources contribute significantly to its market position, along with its adoption of sustainable forestry practices and engineered wood products in construction. Europe follows closely, with Germany recognized as a major hub for wood product manufacturing, particularly in engineered wood and sustainable forest management practices.

The global wood market is dominated by a mix of large multinational companies and regional players. These companies have a significant influence on the market due to their extensive product portfolios, sustainable forestry initiatives, and advanced wood processing technologies. The competitive landscape is marked by consolidation as major players expand their capabilities through mergers and acquisitions, partnerships, and innovations in engineered wood products. This consolidation reflects the growing importance of sustainable forestry and the need for advanced wood materials in the global construction industry.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (USD) |

Number of Employees |

Product Portfolio |

Sustainability Initiatives |

Global Reach |

R&D Investments |

Mergers & Acquisitions |

|

West Fraser Timber Co. |

1955 |

Vancouver, Canada |

- |

- |

- |

- |

- |

- |

- |

|

Weyerhaeuser Company |

1900 |

Seattle, USA |

- |

- |

- |

- |

- |

- |

- |

|

Canfor Corporation |

1938 |

Vancouver, Canada |

- |

- |

- |

- |

- |

- |

- |

|

Stora Enso Oyj |

1998 |

Helsinki, Finland |

- |

- |

- |

- |

- |

- |

- |

|

UPM-Kymmene Corporation |

1996 |

Helsinki, Finland |

- |

- |

- |

- |

- |

- |

- |

Market Growth Drivers

Market Challenges

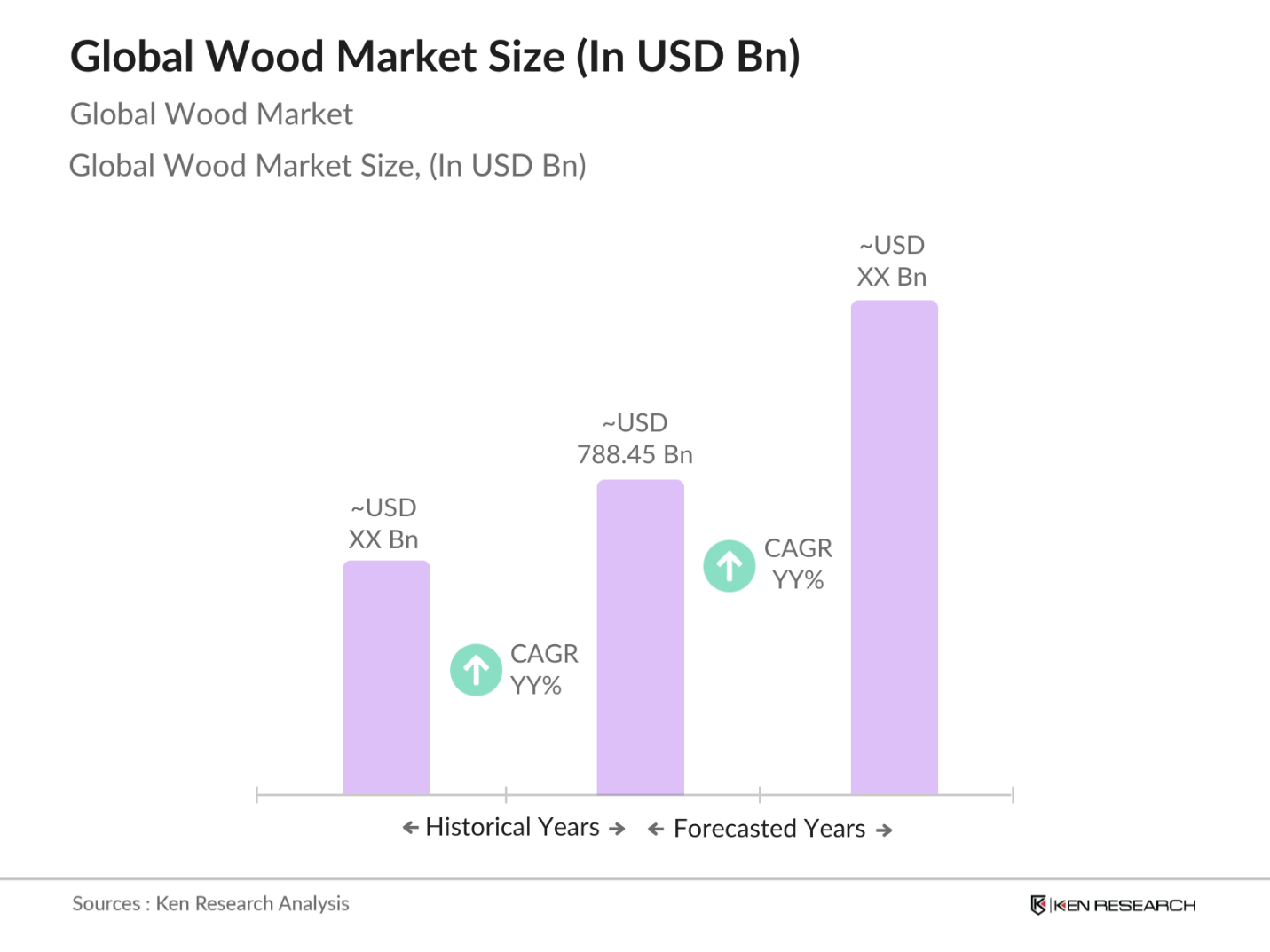

Over the next five years, the global wood market is expected to show significant growth, driven by rising demand for sustainable construction materials, increased government support for eco-friendly forestry, and the expansion of engineered wood applications in both residential and commercial buildings. Additionally, advancements in wood processing technology, such as automated sawmills and digitized supply chains, will further streamline production and reduce costs, bolstering the markets growth trajectory.

Market Opportunities:

|

By Product Type |

Sawnwood Wood-Based Panels Engineered Wood Wood Pellets Reclaimed Wood |

|

By Application |

Construction Furniture Packaging Pulp & Paper Energy (Wood Pellets) |

|

By Channel Type |

Direct Sales Distributors E-Commerce Wholesalers OEM Partnerships |

|

By End-User |

Furniture Manufacturers Construction Companies Pulp & Paper Industries Retail Consumers Interior Designers |

|

By Region |

North America Europe Asia-Pacific Middle East & Africa Latin America |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Size and Growth Trends

1.4 Market Segmentation Overview

2.1 Historical Market Size (2018-2023)

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Rising Demand in Construction and Furniture

3.1.2 Adoption of Sustainable Forestry Practices

3.1.3 Government Policies Supporting Sustainable Materials

3.2 Market Challenges

3.2.1 Raw Material Price Volatility

3.2.2 Stringent Environmental Regulations

3.2.3 Deforestation Concerns

3.3 Market Opportunities

3.3.1 Growing Popularity of Reclaimed and Recycled Wood

3.3.2 Expansion of Engineered Wood Applications

3.4 Trends

3.4.1 Digitalization of Wood Supply Chains

3.4.2 Integration of IoT and Blockchain in Wood Industry

4.1 By Product Type

4.1.1 Sawnwood

4.1.2 Wood-Based Panels

4.1.3 Engineered Wood

4.1.4 Wood Pellets

4.2 By Application

4.2.1 Construction

4.2.2 Furniture

4.2.3 Packaging

4.2.4 Pulp and Paper

4.2.5 Energy (Wood Pellets)

4.3 By Region

4.3.1 North America

4.3.2 Europe

4.3.3 Asia-Pacific

4.3.4 Middle East & Africa

4.3.5 Latin America

4.4 By End-User

4.4.1 Furniture Manufacturers

4.4.2 Construction Companies

4.4.3 Pulp & Paper Industries

4.4.4 Retail Consumers

4.4.5 Interior Designers

5.1 Detailed Profiles of Major Companies

5.2 Market Share Analysis

5.3 Strategic Initiatives

5.1.4 Stora Enso Oyj (Finland)

5.1.5 UPM-Kymmene Corporation (Finland)

5.1.6 Georgia-Pacific LLC (USA)

5.1.7 Boise Cascade Company (USA)

5.1.8 Interfor Corporation (Canada)

5.1.9 Rayonier Advanced Materials (USA)

5.1.10 Norbord Inc. (Canada)

5.1.11 Kronospan Limited (Austria)

5.1.12 Pfleiderer Group (Germany)

5.1.13 Holmen AB (Sweden)

5.1.14 Resolute Forest Products (Canada)

5.1.15 Sveaskog AB (Sweden)

5.2 Market Share Analysis

5.3 Strategic Initiatives

6.1 Environmental Compliance and Forest Management Standards

6.2 Certifications (FSC, PEFC)

6.3 International Trade and Tariff Regulations

7.1 Market Projections to 2028

7.2 Key Trends Shaping the Future

8.1 Investment Opportunities in Sustainable Forestry

8.2 Adoption of Engineered and Reclaimed Wood

8.3 Expansion Strategies in Emerging Markets

9.1 Identification of Key Variables

9.2 Market Analysis and Validation

9.3 Expert Consultation

9.4 Research Synthesis

The research process began with the identification of major stakeholders within the global wood market ecosystem, which includes timber producers, wood processing firms, construction companies, and government regulatory bodies. Extensive desk research was conducted to gather information on market drivers, challenges, and the competitive landscape.

In this step, historical data related to market size, growth drivers, and challenges were analyzed to understand the current market dynamics. A bottom-up approach was employed to assess market share for different product types and regions.

Market hypotheses were formulated based on desk research and validated through interviews with industry experts, including key executives from wood manufacturing companies and forestry organizations. These consultations helped refine the data, ensuring accuracy and industry relevance.

The final stage involved synthesizing the collected data and expert insights into a comprehensive market report, which was peer-reviewed by industry professionals to ensure it accurately reflects the trends, growth drivers, and opportunities in the global wood market.

The global wood market is valued at USD 788.45 billion, driven by increasing demand from the construction sector and innovations in wood processing technologies.

Challenges in the global wood market include the volatility of raw material prices, environmental regulations concerning deforestation, and the lack of skilled labor in emerging markets.

Key players in the global wood market include West Fraser Timber Co., Weyerhaeuser Company, Canfor Corporation, Stora Enso Oyj, and UPM-Kymmene Corporation. These companies lead the market due to their extensive global reach, sustainability initiatives, and advanced wood processing capabilities.

The global wood market is propelled by the rising demand for eco-friendly construction materials, government incentives for sustainable forestry, and technological advancements in engineered wood products.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.