India Aircraft Seating Market Outlook to 2030

Region:Asia

Author(s):Vijay Kumar

Product Code:KROD3386

December 2024

85

About the Report

India Aircraft Seating Market Overview

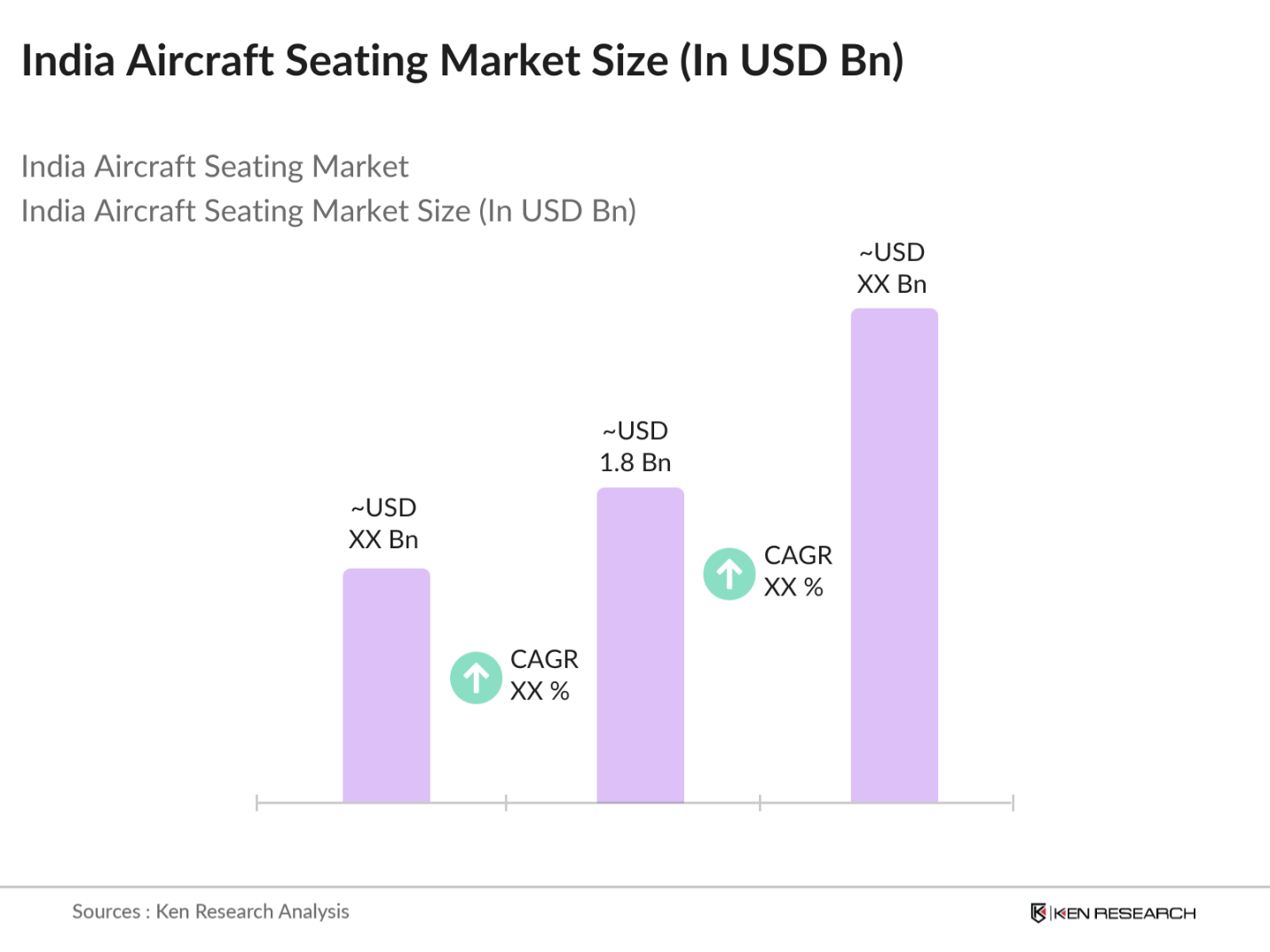

- The India Aircraft Seating Market has witnessed substantial growth, paralleling the expansion of the aviation sector, with the market reaching USD 1.8 billion in 2023. This growth is driven by the increasing number of air travelers, fleet modernization by airlines, and the rise of low-cost carriers in the country. The market is further supported by government initiatives aimed at enhancing regional connectivity and the overall aviation infrastructure.

- Key players in the India Aircraft Seating Market include Zodiac Aerospace, Recaro Aircraft Seating, Geven, B/E Aerospace, and Acro Aircraft Seating. These companies dominate the market due to their advanced seating solutions, strong relationships with major airlines, and continuous investment in R&D. Their focus on innovation and customer satisfaction has helped them maintain a significant market share in India.

- In 2024, Recaro Aircraft Seating secured a major contract with IndiGo to supply its new lightweight economy-class seats across the airlines expanding fleet. This partnership is expected to enhance IndiGo's operational efficiency and passenger comfort, reflecting the growing demand for advanced seating solutions in India's rapidly growing aviation sector.

- Delhi and Mumbai dominate the India Aircraft Seating Market due to their well-established aviation infrastructure and high passenger traffic. Delhi, with the Indira Gandhi International Airport, serves as a key hub for both domestic and international flights, while Mumbais Chhatrapati Shivaji Maharaj International Airport is a central hub for several airlines. These cities' significant investments in airport facilities and fleet expansion drive the demand for advanced seating solutions.

India Aircraft Seating Market Segmentation

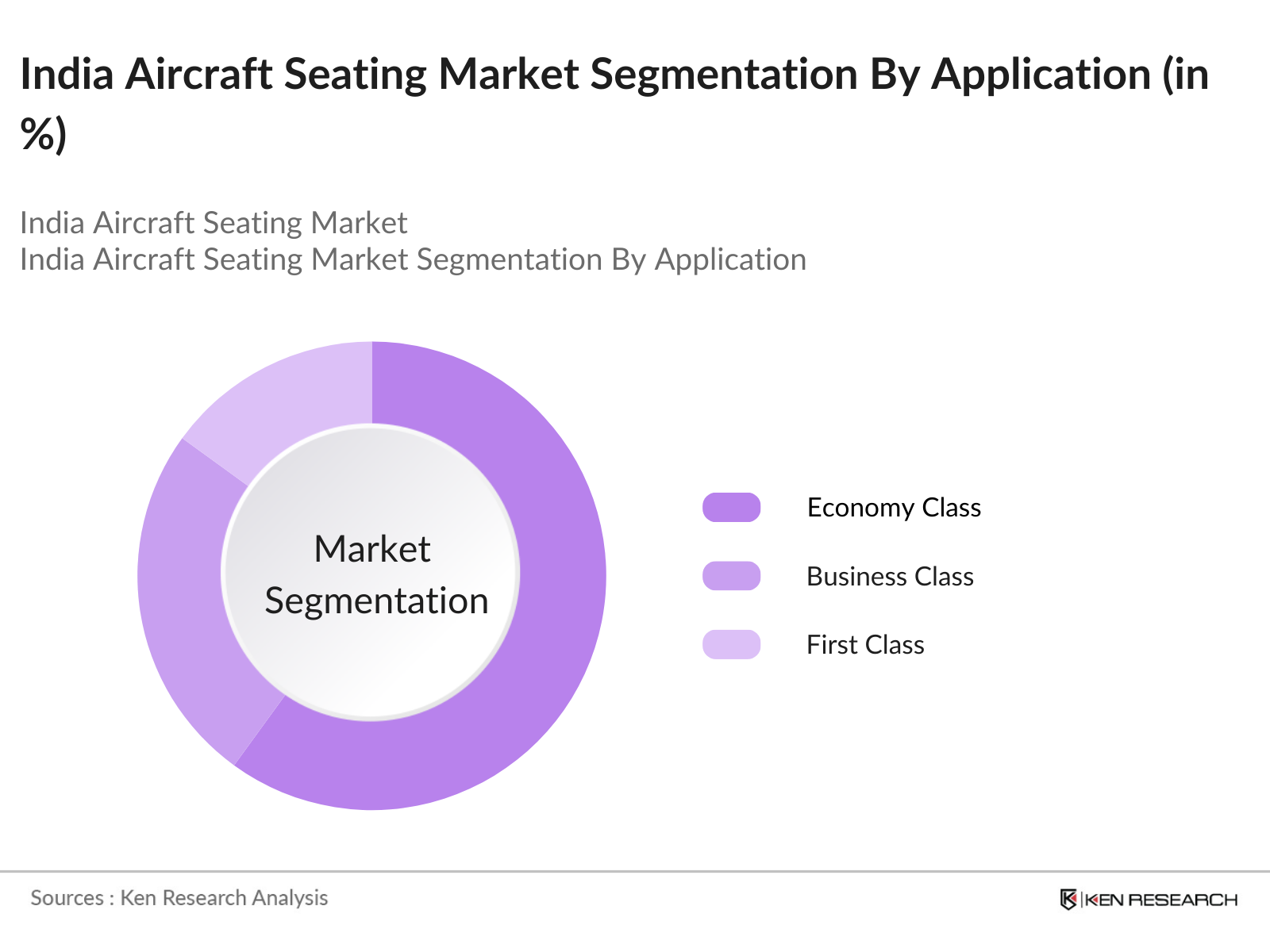

By Application: The India Aircraft Seating Market is segmented by application into Economy Class, Business Class, and First Class. In 2023, the Economy Class segment dominated the market due to its widespread use across both domestic and international flights. The demand for cost-effective seating options, driven by the rise of low-cost carriers, is a major factor contributing to the dominance of this segment.

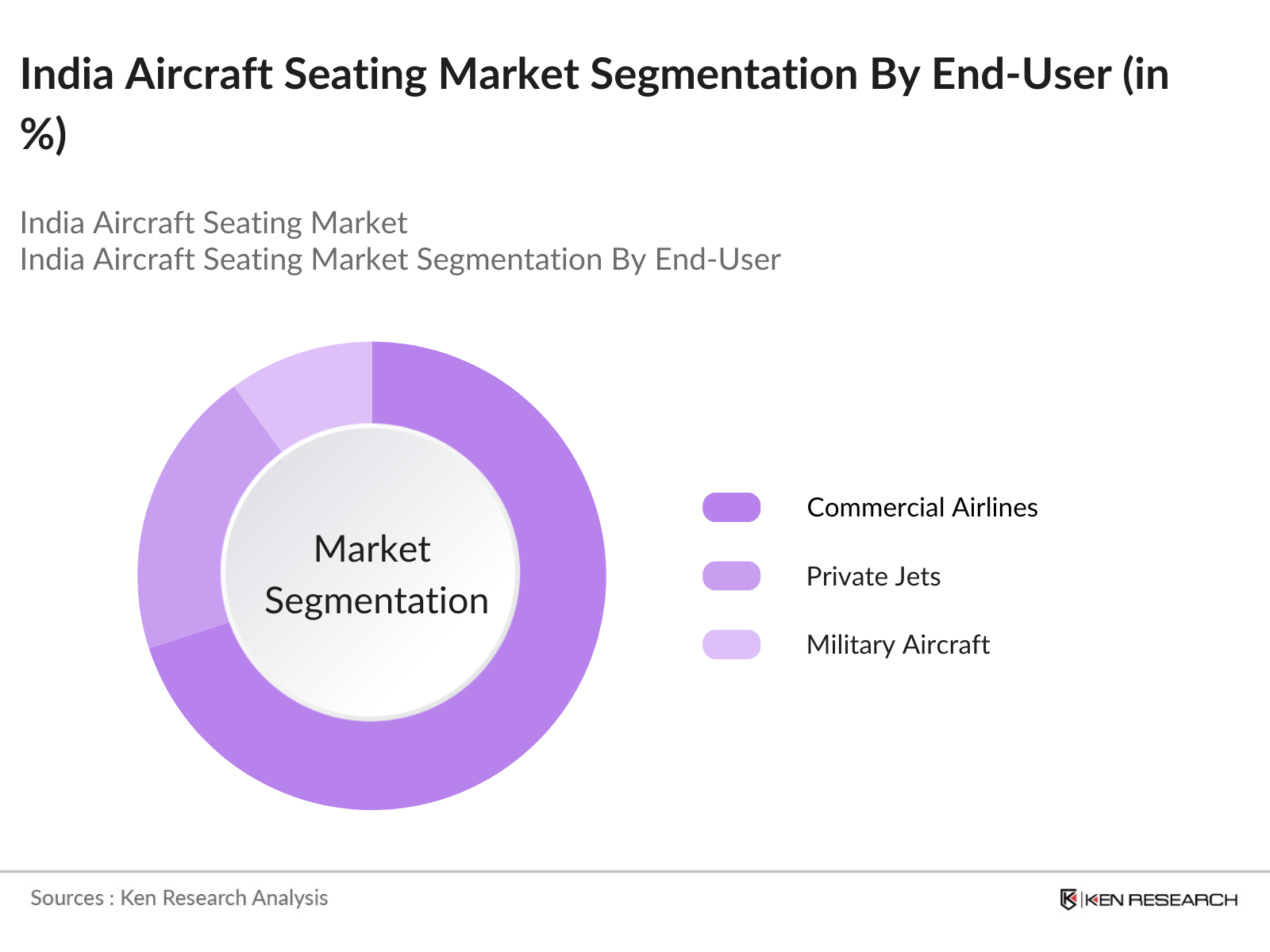

By End-User: The market is segmented by end-user into Commercial Airlines, Private Jets, and Military Aircraft. Commercial Airlines held the largest market share in 2023, driven by the growing number of domestic and international flights in India. The continuous expansion of airline fleets, along with increasing passenger traffic, supports the dominance of this segment.

By Region: The India Aircraft Seating Market is segmented by region into North, South, East, and West. In 2023, the Northern region, which includes major cities like Delhi and Chandigarh, dominated the market due to its extensive aviation infrastructure and high air traffic. The region's strategic importance as a hub for both domestic and international flights contribute to its leading position.

India Aircraft Seating Market Competitive Landscape Overview

|

Company |

Establishment Year |

Headquarters |

|

Zodiac Aerospace |

1896 |

Paris, France |

|

Recaro Aircraft Seating |

1925 |

Kirchheim unter Teck, Germany |

|

Geven |

1952 |

Naples, Italy |

|

B/E Aerospace |

1987 |

Miami, USA |

|

Acro Aircraft Seating |

2007 |

London, UK |

- Zodiac Aerospace: In 2024, Zodiac Aerospace introduced a new line of modular aircraft seats designed for easy reconfiguration between different classes. This innovation is aimed at providing airlines with greater flexibility in seating arrangements, enhancing their ability to meet diverse passenger needs and optimize cabin layouts.

- Recaro Aircraft Seating: Recaro launched its latest economy class seat, the "CL3710," in early 2024, designed to reduce weight while improving passenger comfort. This new model is already being adopted by major Indian airlines, including SpiceJet and Air India, reflecting the growing demand for efficient and comfortable seating solutions.

India Aircraft Seating Market Analysis

Market Growth Drivers

- Increasing Air Travel Demand: The rapid growth in air travel demand in India, with passenger numbers expected to reach 350 million by 2025, is a significant driver for the aircraft seating market. This surge in demand necessitates the expansion and modernization of airline fleets, driving the need for advanced seating solutions.

- Fleet Modernization: Indian airlines are investing heavily in fleet modernization, with projections indicating an order of over 500 new aircraft by 2028. This investment includes upgrading to modern seating systems that offer better comfort and efficiency, fueling market growth.

- Expansion of Low-Cost Carriers: The rise of low-cost carriers in India is driving the demand for affordable and efficient seating solutions. With over 60% of new aircraft deliveries expected to go to low-cost carriers, this trend is boosting the demand for cost-effective seating options.

India Aircraft Seating Market Challenges

- High Costs of Advanced Seating Technologies: The high cost associated with advanced seating technologies, including the latest ergonomic designs and materials, poses a challenge for airlines, especially budget carriers. The initial investment required for installing premium and high-tech seating solutions can be substantial, impacting market adoption.

- Regulatory Compliance: Compliance with stringent aviation safety and comfort regulations can be a significant challenge for manufacturers. Ensuring that seating solutions meet both national and international standards requires substantial investment in research and development.

- Supply Chain Disruptions: Disruptions in the supply chain, including shortages of raw materials and logistical challenges, can impact the timely delivery of aircraft seats. These disruptions can lead to delays and increased costs for manufacturers and airlines.

India Aircraft Seating Government Initiatives

- UDAN Scheme: The UDAN (Ude Desh ka Aam Nagrik) scheme aims to enhance regional connectivity and increase the number of operational airports in India. This initiative is expected to drive demand for new aircraft and seating solutions, supporting market growth.

- National Civil Aviation Policy 2016: This policy focuses on improving aviation infrastructure, increasing passenger capacity, and supporting the growth of the aviation sector. The policy's emphasis on expanding air travel and modernizing airport facilities benefits the aircraft seating market.

- Aircraft Manufacturing Policy: The Indian governments Aircraft Manufacturing Policy encourages the development of domestic aircraft manufacturing capabilities. This policy aims to enhance the local production of aircraft components, including seating systems, supporting the growth of the aircraft seating market.

India Aircraft Seating Market Future Outlook

The India Aircraft Seating Market is expected to continue its growth, driven by ongoing investments, government support, and increasing demand for advanced seating solutions.

Future Market Trends

- Advancements in Seating Technology: By 2028, the India Aircraft Seating Market is expected to see significant advancements in seating technology, including the integration of smart features such as adjustable settings and in-seat entertainment systems. These innovations will enhance passenger comfort and offer a more personalized travel experience.

- Sustainability Initiatives: The trend towards sustainable and eco-friendly seating materials will gain momentum. By 2028, the use of recyclable and biodegradable materials in aircraft seating will become more common, aligning with global efforts to reduce the environmental impact of the aviation industry.

- Expansion of Premium Seating Solutions: The demand for premium seating solutions, such as business and first-class seats with advanced features, will rise. As Indian airlines continue to upgrade their fleets, the market will see increased investment in high-end seating options to cater to the growing segment of affluent travelers.

Scope of the Report

|

By Application |

Economy Class Business Class First Class |

|

By End-User |

Commercial Airlines Private Jets Military Aircraft |

|

By Region |

North South East West |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

Aircraft Seat Manufacturers

Commercial Airlines

Aircraft Leasing Companies

Aviation Regulatory Bodies (e.g., DGCA)

Government and Regulatory Bodies

Aircraft Maintenance Organizations

Investment and Venture Capitalist Firms

Time Period Captured in the Report:

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

Zodiac Aerospace

Recaro Aircraft Seating

Geven

B/E Aerospace

Acro Aircraft Seating

Stelia Aerospace

Thompson Aero Seating

HAECO

Collins Aerospace

Safran Seats

Table of Contents

1. India Aircraft Seating Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. India Aircraft Seating Market Size (In USD Billion)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. India Aircraft Seating Market Analysis

3.1. Growth Drivers

3.1.1. Expansion of Domestic Airlines

3.1.2. Rising Passenger Traffic

3.1.3. Government Initiatives in Aviation

3.1.4. Fleet Modernization Efforts

3.2. Market Challenges

3.2.1. High Production Costs

3.2.2. Stringent Regulatory Standards

3.2.3. Supply Chain Disruptions

3.3. Opportunities

3.3.1. Technological Innovations in Seating

3.3.2. Collaborations with Global Manufacturers

3.3.3. Growth in Low-Cost Carrier Segment

3.4. Trends

3.4.1. Lightweight Material Adoption

3.4.2. Customization for Passenger Comfort

3.4.3. Integration of In-Flight Entertainment Systems

3.5. Government Regulations

3.5.1. Directorate General of Civil Aviation (DGCA) Guidelines

3.5.2. Make in India Initiative

3.5.3. Regional Connectivity Scheme (UDAN)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

4. India Aircraft Seating Market Segmentation

4.1. By Seat Class (In Value %)

4.1.1. Economy Class

4.1.2. Premium Economy Class

4.1.3. Business Class

4.1.4. First Class

4.2. By Aircraft Type (In Value %)

4.2.1. Narrow-Body Aircraft

4.2.2. Wide-Body Aircraft

4.2.3. Regional Jets

4.2.4. Business Jets

4.3. By Component (In Value %)

4.3.1. Seat Structures

4.3.2. Seat Actuators

4.3.3. Seat Foams & Fittings

4.3.4. In-Flight Entertainment Systems

4.4. By End Use (In Value %)

4.4.1. OEM

4.4.2. Aftermarket

4.5. By Material (In Value %)

4.5.1. Aluminum

4.5.2. Composites

4.5.3. Steel

4.5.4. Others

5. India Aircraft Seating Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Safran Seats

5.1.2. Recaro Aircraft Seating GmbH & Co. KG

5.1.3. Collins Aerospace

5.1.4. Geven S.p.A.

5.1.5. JAMCO Corporation

5.1.6. Thompson Aero Seating Ltd.

5.1.7. ZIM Flugsitz GmbH

5.1.8. Acro Aircraft Seating

5.1.9. Aviointeriors S.p.A.

5.1.10. Stelia Aerospace

5.1.11. Mirus Aircraft Seating Ltd.

5.1.12. Haeco Cabin Solutions

5.1.13. Expliseat

5.1.14. Lufthansa Technik AG

5.1.15. AIM Altitude

5.2. Cross Comparison Parameters (Number of Employees, Headquarters Location, Year of Establishment, Annual Revenue, Product Portfolio, Key Clients, Regional Presence, Recent Developments)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.6.1. Venture Capital Funding

5.6.2. Government Grants

5.6.3. Private Equity Investments

6. India Aircraft Seating Market Regulatory Framework

6.1. Aviation Safety Standards

6.2. Compliance Requirements

6.3. Certification Processes

7. India Aircraft Seating Future Market Size (In USD Billion)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. India Aircraft Seating Future Market Segmentation

8.1. By Seat Class (In Value %)

8.2. By Aircraft Type (In Value %)

8.3. By Component (In Value %)

8.4. By End Use (In Value %)

8.5. By Material (In Value %)

9. India Aircraft Seating Market Analysts Recommendations

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identifying Key Variables

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around the market to collate industry-level information.

Step 2: Market Building

Collating statistics on the India Aircraft Seating Market over the years, analyzing the penetration of marketplaces, and the ratio of service providers to compute revenue generated for the India Aircraft Seating Market. We will also review service quality statistics to understand revenue generation, ensuring accuracy behind the data points shared.

Step 3: Validating and Finalizing

Building market hypotheses and conducting CATIs with industry experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Step 4: Research Output

Our team will approach multiple essential aircraft seating companies and understand the nature of product segments, sales, consumer preferences, and other parameters, which will support validating statistics derived through a bottom-to-top approach from aircraft seating companies.

Frequently Asked Questions

1. How big is the India Aircraft Seating Market?

The India Aircraft Seating Market was valued at USD 1.8 billion in 2023. This growth is driven by the increasing number of air travelers and the modernization of airline fleets.

2. What are the challenges in the India Aircraft Seating Market?

Challenges include the high cost of advanced materials used in seat manufacturing, stringent regulatory compliance requirements, and supply chain disruptions affecting component availability and production timelines.

3. Who are the major players in the India Aircraft Seating Market?

Major players include Zodiac Aerospace, Recaro Aircraft Seating, Geven, and B/E Aerospace. These companies are prominent due to their innovative seat designs and strong industry presence.

4. What are the growth drivers of the India Aircraft Seating Market?

Key growth drivers include the rising demand for air travel, ongoing fleet modernization by airlines, and the expansion of low-cost carriers which increases the need for cost-effective and comfortable seating solutions.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.