India Automotive Engine Oils Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD11143

December 2024

82

About the Report

India Automotive Engine Oils Market Overview

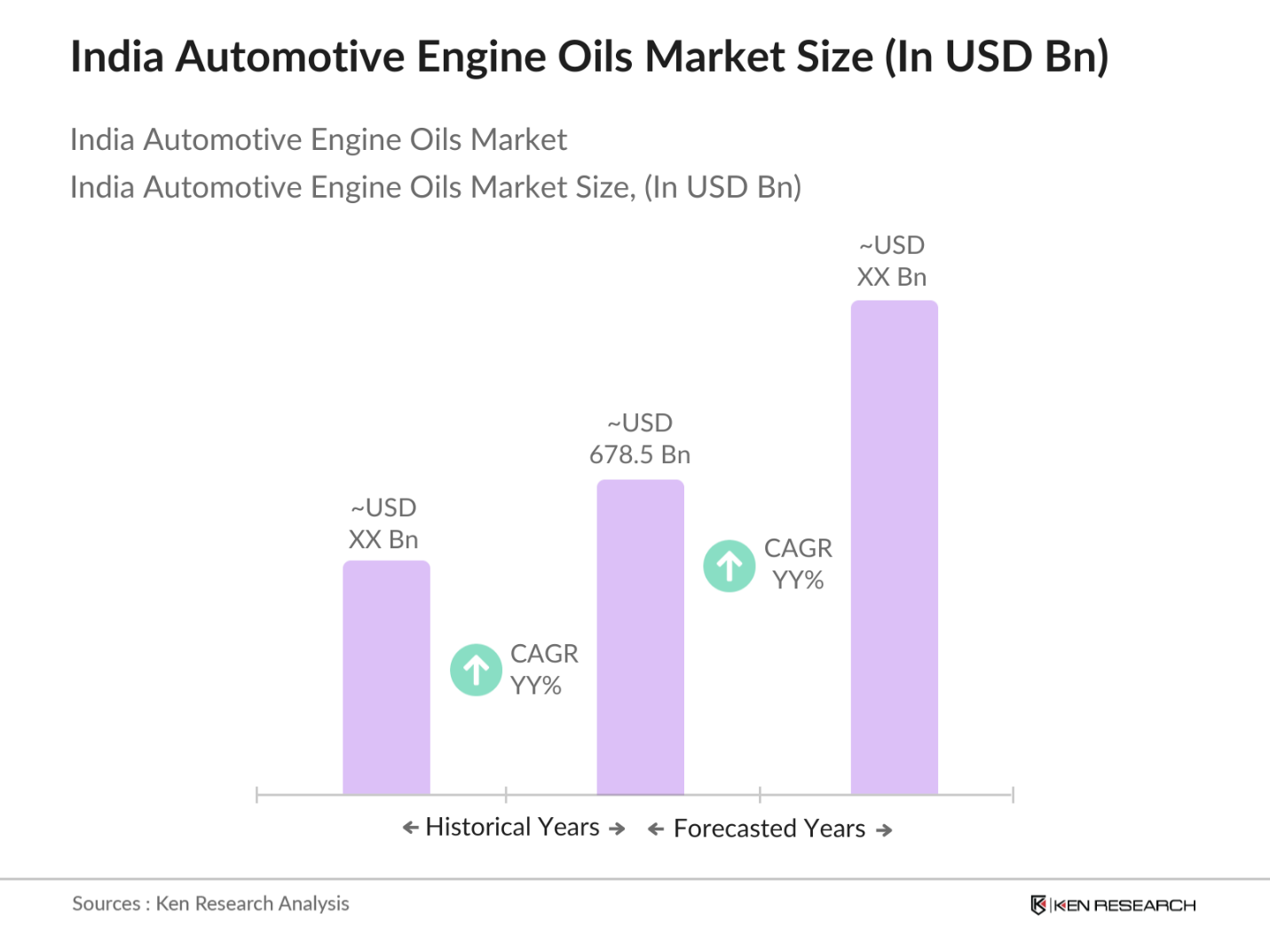

- The India automotive engine oils market is valued at approximately USD 678.5 billion, driven primarily by the country's growing vehicle population and the increasing penetration of advanced engine technologies. The demand for synthetic and semi-synthetic oils has also grown due to their superior performance and longer lifespan. The automotive sector's expansion, supported by infrastructure development and government initiatives, further fuels the demand for engine oils, particularly in the commercial vehicle segment. These factors highlight the robust market growth.

- In India, cities such as Delhi, Mumbai, and Bengaluru dominate the automotive engine oils market due to their high vehicle density and large urban population. These regions have a higher concentration of passenger and commercial vehicles, leading to increased consumption of engine oils. Additionally, their developed infrastructure and the presence of numerous service centers and automotive workshops enhance their market dominance.

- The Indian government has been offering subsidies and tax reductions for companies producing eco-friendly lubricants, including low-emission and biodegradable engine oils. Under the Green Energy initiative, companies manufacturing lubricants that comply with environmental regulations are eligible for financial benefits, encouraging more widespread production and use of eco-friendly products. This initiative supports the shift towards sustainability in the automotive sector, contributing to reduced carbon emissions. In 2023, this policy helped increase the adoption of eco-friendly lubricants by various automotive manufacturers and consumers across the country.

India Automotive Engine Oils Market Segmentation

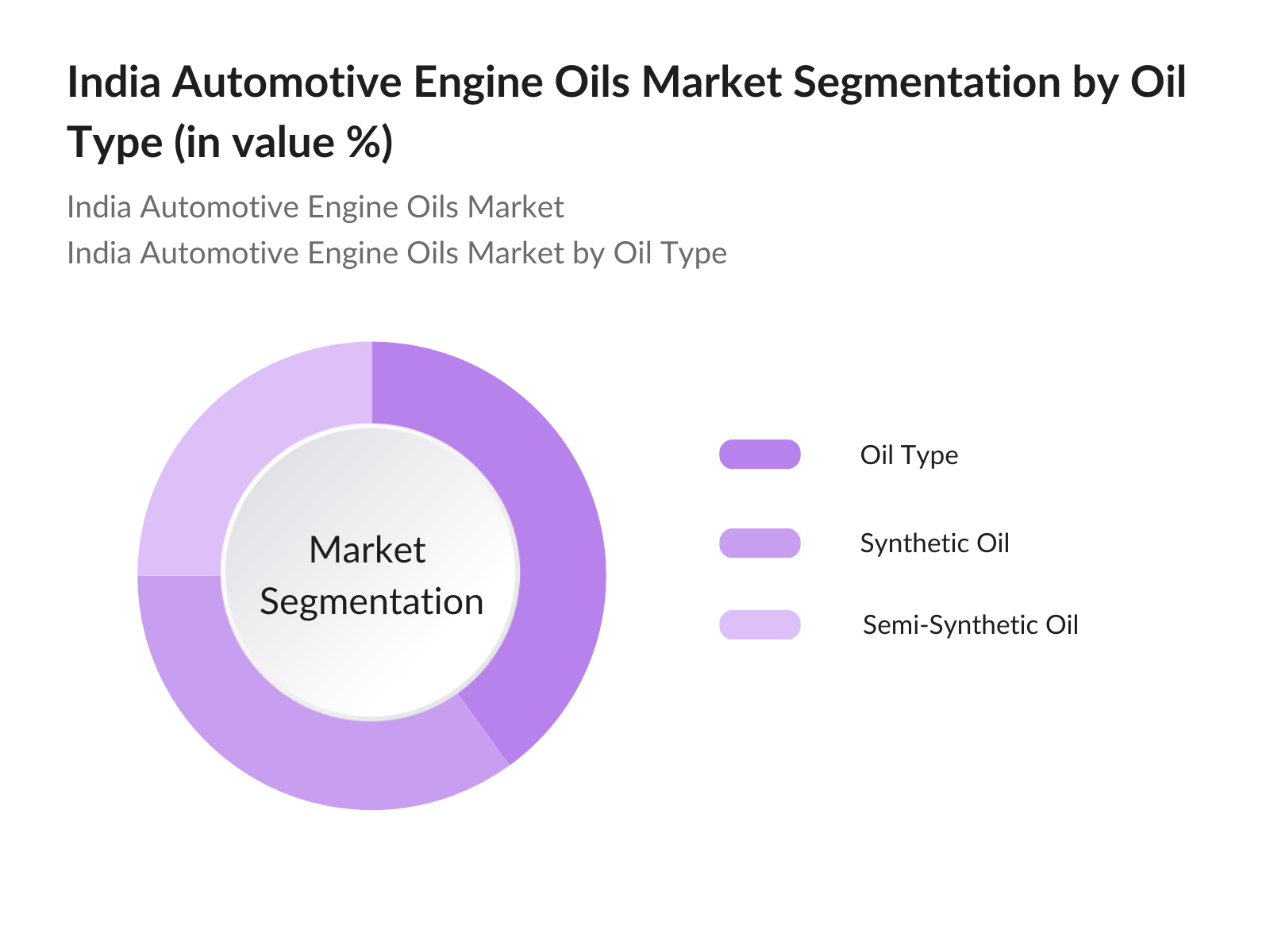

By Oil Type: The Indias automotive engine oils market is segmented by oil type into mineral oils, synthetic oils, and semi-synthetic oils. Synthetic oils are increasingly dominating the market due to their enhanced engine protection and extended oil life, which make them a preferred choice for high-performance vehicles and heavy-duty applications. Synthetic oils' ability to function effectively in extreme temperatures has further contributed to their popularity, particularly in regions with varied climates across India.

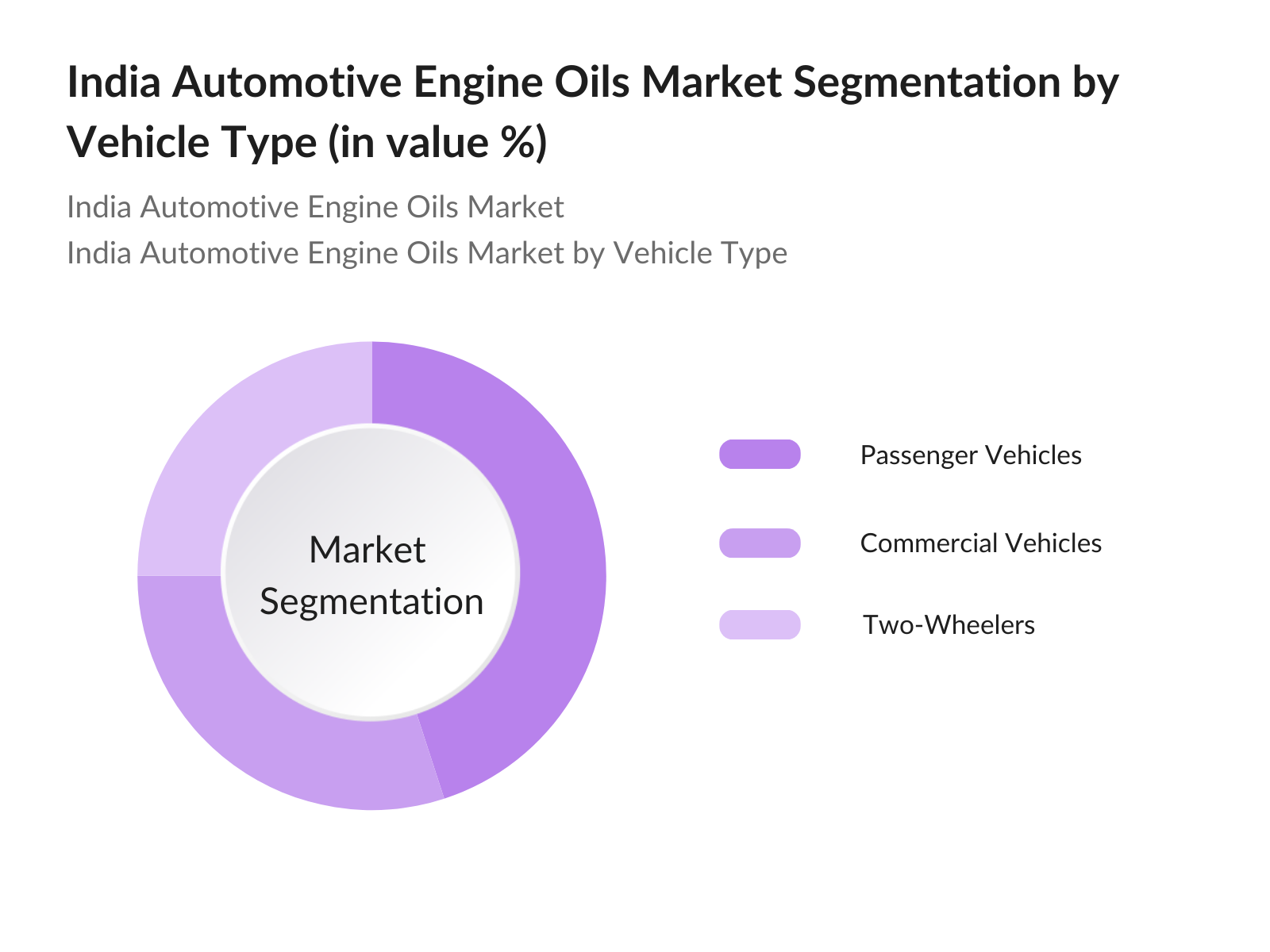

By Vehicle Type: The market is segmented by vehicle type into passenger vehicles, commercial vehicles, and two-wheelers. Passenger vehicles dominate the market, driven by the increasing number of personal vehicle ownership and rising disposable incomes in urban areas. Commercial vehicles, including trucks and delivery vans, play a significant role, particularly in the context of Indias expanding e-commerce and logistics sectors. Two-wheelers, which account for a significant portion of Indias total vehicle fleet, also contribute substantially to the demand for engine oils, particularly in rural and semi-urban regions.

India Automotive Engine Oils Market Competitive Landscape

The India automotive engine oils market is consolidated with a few dominant players that have strong distribution networks and brand recognition. Major companies in the sector include Indian Oil Corporation, Castrol India, and Bharat Petroleum, each contributing significantly to the market through innovations in product offerings and strategic partnerships.

|

Company |

Established |

Headquarters |

Revenue (INR Crore) |

Number of Employees |

Product Range |

Sustainability Initiatives |

Regional Presence |

|

Indian Oil Corporation Ltd. |

1959 |

New Delhi, India |

- |

- |

- |

- |

- |

|

Bharat Petroleum Corporation Ltd. |

1952 |

Mumbai, India |

- |

- |

- |

- |

- |

|

Castrol India Ltd. |

1919 |

Mumbai, India |

- |

- |

- |

- |

- |

|

Hindustan Petroleum Corporation |

1974 |

Mumbai, India |

- |

- |

- |

- |

- |

|

Shell India Markets Pvt. Ltd. |

1907 |

Bengaluru, India |

- |

- |

- |

- |

- |

India Automotive Engine Oils Market Analysis

Market Growth Drivers

- Increase in Vehicle Sales (Passenger, Commercial, Two-Wheelers): The Indian automotive industry is witnessing robust growth in vehicle sales, primarily driven by increasing consumer demand for passenger and commercial vehicles. According to the Ministry of Road Transport and Highways, India saw the registration of over 295 million vehicles in 2023, with 3.8 million new passenger vehicles and 3.2 million commercial vehicles added during the year. Rising middle-class income, urbanization, and increasing access to finance have spurred demand for both two-wheelers and four-wheelers. This surge directly contributes to the rising demand for automotive engine oils in 2024, as engine oils remain essential for vehicle maintenance and longevity.

- Rising Infrastructure Development (Logistics Growth, Highway Expansion): Indias focus on infrastructure development has led to a significant increase in logistics activities, fueling demand for commercial vehicles and, consequently, automotive engine oils. The National Highways Authority of India (NHAI) reported that over 13,327 kilometers of national highways were constructed in 2023, enabling more efficient transportation routes. Additionally, the growth of e-commerce logistics has pushed commercial vehicle sales to new heights. This uptick in logistics directly correlates with the demand for high-performance engine oils, which are crucial in sustaining the increasing vehicle load across Indias expanding highway network.

- Government Regulations on Emission Standards (BS6 Norms, Fuel Efficiency): The introduction of Bharat Stage 6 (BS6) norms in April 2020, aimed at reducing vehicular emissions, has necessitated the use of cleaner, more efficient engine oils. As of 2023, all vehicles in India are required to comply with BS6 emission standards, which significantly lower NOx emissions for both diesel and petrol vehicles. The Indian government continues to monitor emissions strictly, which pushes manufacturers to produce lubricants that enhance fuel efficiency and lower emission levels. This regulatory change is driving the adoption of higher-quality synthetic and semi-synthetic engine oils.

Market Challenges:

- Fluctuating Crude Oil Prices (Impact on Base Oil Production): Crude oil price volatility continues to challenge the automotive engine oil market due to its direct impact on base oil production costs. As of September 2024, Brent crude prices hovered around $88 per barrel, following fluctuations driven by geopolitical tensions and supply disruptions. Since base oils, a primary component of engine oils, are derived from crude oil, these fluctuations directly impact the manufacturing costs of lubricants. The Indian Oil Corporation reported that refining costs have increased from 2022 to 2024, affecting the overall pricing and availability of engine oils in India.

- Presence of Counterfeit Engine Oils (Brand Protection, Consumer Trust): The proliferation of counterfeit automotive engine oils in India remains a significant challenge for industry players. According to the Federation of Indian Chambers of Commerce & Industry (FICCI), the counterfeit market for automotive lubricants was estimated to account for approximately $1.3 billion in 2023. Fake engine oils not only harm vehicle performance but also diminish consumer trust in branded products. Industry participants must invest in brand protection measures such as advanced packaging, tamper-evident seals, and public awareness campaigns to maintain consumer confidence and safeguard market share.

India Automotive Engine Oils Market Future Outlook

Over the next five years, the India automotive engine oils market is expected to experience steady growth, driven by advancements in engine technology, the rising popularity of synthetic oils, and government regulations promoting eco-friendly practices. Increasing vehicle sales, especially in rural areas, and the expansion of e-commerce delivery fleets are likely to boost demand. Furthermore, the emergence of electric vehicles may moderately slow demand for traditional engine oils, but innovative oil formulations for hybrid vehicles will sustain market growth.

Market Opportunities:

- Expansion into Rural Markets (Increased Vehicle Penetration in Tier-2, Tier-3 Cities): Indias rural markets present substantial growth opportunities for the automotive engine oils sector. In 2023, vehicle penetration in Tier-2 and Tier-3 cities increased by 12%, as reported by the Society of Indian Automobile Manufacturers (SIAM). Improved road infrastructure and rising incomes in these regions have driven demand for two-wheelers and passenger vehicles. With the increase in vehicle ownership comes a corresponding demand for engine oils, particularly those suited for rural driving conditions. Companies targeting rural markets with affordable and durable engine oil options are well-positioned to capitalize on this expanding customer base.

- Rise in Demand for Low-Viscosity Oils (Fuel Efficiency Focus, Eco-friendly Initiatives): Low-viscosity engine oils, known for their ability to improve fuel efficiency, are gaining traction in India as consumers and manufacturers prioritize eco-friendly initiatives. The Indian governments push for improved fuel efficiency, combined with Bharat Stage 6 norms, has encouraged the adoption of low-viscosity oils. As of 2023, major oil companies, including Indian Oil, reported a 20% increase in the production of low-viscosity synthetic oils, which offer lower friction and better fuel economy. These oils are especially popular among environmentally conscious consumers and fleet operators seeking cost-effective solutions.

Scope of the Report

|

By Product Type |

Planetary Gears Helical Gears Bevel Gears Spur Gears Hypoid Gears |

|

By Application |

Passenger Vehicles Commercial Vehicles Electric Vehicles Heavy-Duty Trucks |

|

By Material Type |

Steel Aluminum Composite Materials Others |

|

By Manufacturing Process |

Forged Machined Moulded |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East and Africa |

Products

Key Target Audience

Automotive manufacturers

OEMs (Original Equipment Manufacturers)

Aftermarket service providers

Vehicle fleet operators

Lubricant manufacturers

Distributors and retailers

Government and regulatory bodies (Ministry of Petroleum and Natural Gas, Bureau of Indian Standards)

Investments and venture capitalist firms

Companies

Players Mention in the Report

Indian Oil Corporation Ltd.

Bharat Petroleum Corporation Ltd.

Castrol India Ltd.

Hindustan Petroleum Corporation Ltd.

Shell India Markets Pvt. Ltd.

Gulf Oil Lubricants India Ltd.

ExxonMobil Lubricants Pvt. Ltd.

Total Oil India Pvt. Ltd.

Valvoline Cummins Pvt. Ltd.

Savita Oil Technologies Ltd.

Apar Industries Ltd.

Tide Water Oil Co. India Ltd.

Fuchs Lubricants India Pvt. Ltd.

Veedol International Ltd.

Lubrizol India Pvt. Ltd.

Table of Contents

01. Global Automotive Gears Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

02. Global Automotive Gears Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

03. Global Automotive Gears Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Vehicle Production

3.1.2. Advancements in Transmission Technologies

3.1.3. Government Regulations on Fuel Efficiency and Emissions

3.2. Market Challenges

3.2.1. High Cost of Raw Materials (Steel, Aluminum, Titanium)

3.2.2. Complex Manufacturing Process

3.2.3. Volatility in the Automotive Industry (Chip Shortage Impact)

3.3. Opportunities

3.3.1. Growth of Electric Vehicles (EV Gear Design)

3.3.2. Demand for Lightweight Gears in Automotive Industry

3.3.3. Expansion of Aftermarket Sales

3.4. Trends

3.4.1. Adoption of Precision Gear Manufacturing

3.4.2. Increased Use of Additive Manufacturing

3.4.3. Automation in Gear Production

3.5. Technological Advancements

3.5.1. Integration of AI in Gear Design

3.5.2. Hybrid Powertrain Gears

3.5.3. Digital Twin Technology in Gear Testing

3.6. Government Regulations

3.6.1. Fuel Efficiency Standards

3.6.2. Emission Norms for Passenger and Commercial Vehicles

3.6.3. Tax Incentives for Green Gears Manufacturing

3.7. SWOT Analysis

3.8. Porters Five Forces

3.9. Stakeholder Ecosystem

04. Global Automotive Gears Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Planetary Gears

4.1.2. Helical Gears

4.1.3. Bevel Gears

4.1.4. Spur Gears

4.1.5. Hypoid Gears

4.2. By Application (In Value %)

4.2.1. Passenger Vehicles

4.2.2. Commercial Vehicles

4.2.3. Electric Vehicles

4.2.4. Heavy-Duty Trucks

4.3. By Material Type (In Value %)

4.3.1. Steel

4.3.2. Aluminum

4.3.3. Composite Materials

4.3.4. Others

4.4. By Manufacturing Process (In Value %)

4.4.1. Forged

4.4.2. Machined

4.4.3. Moulded

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East and Africa

05. Global Automotive Gears Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. ZF Friedrichshafen AG

5.1.2. Dana Incorporated

5.1.3. GKN Automotive

5.1.4. American Axle & Manufacturing

5.1.5. BorgWarner Inc.

5.1.6. Robert Bosch GmbH

5.1.7. Magna International Inc.

5.1.8. Eaton Corporation

5.1.9. Schaeffler Group

5.1.10. Linamar Corporation

5.1.11. NSK Ltd.

5.1.12. Meritor, Inc.

5.1.13. Oerlikon Graziano

5.1.14. Aisin Seiki Co., Ltd.

5.1.15. Bharat Gears Ltd.

5.2. Cross Comparison Parameters (Revenue, R&D Expenditure, Product Portfolio, Market Reach, Innovations, Strategic Alliances, M&A Activity, Employee Strength)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers & Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

06. Global Automotive Gears Market Regulatory Framework

6.1. Emission Control Standards

6.2. Automotive Gear Manufacturing Certifications

6.3. Compliance with International Safety Standards

07. Global Automotive Gears Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

08. Global Automotive Gears Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Material Type (In Value %)

8.4. By Manufacturing Process (In Value %)

8.5. By Region (In Value %)

09. Global Automotive Gears Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involved mapping the ecosystem of stakeholders within the India Automotive Engine Oils Market. This included extensive secondary research through reliable government data sources, such as the Ministry of Petroleum and Natural Gas and industry reports, to gather key variables that affect the market, including vehicle ownership trends and oil consumption rates.

Step 2: Market Analysis and Construction

Historical data from sources such as government agencies and industry associations was analyzed to identify market penetration and consumer buying patterns. Specific metrics such as oil type preferences and vehicle types were included to ensure accuracy in market size and segmentation.

Step 3: Hypothesis Validation and Expert Consultation

To validate the hypotheses, we conducted interviews with automotive experts, lubricant manufacturers, and distributors. These industry practitioners provided real-world insights into the operational and financial trends shaping the engine oils market.

Step 4: Research Synthesis and Final Output

The final phase included direct consultations with leading oil manufacturers and retailers. Their input provided additional market insights into distribution strategies, product performance, and future innovation trends. These consultations helped to confirm the conclusions drawn from data analysis.

Frequently Asked Questions

01. How big is the India Automotive Engine Oils Market?

The India automotive engine oils market is valued at USD 678.5 billion, driven by the increasing vehicle population and rising demand for high-performance oils.

02. What are the key challenges in the India Automotive Engine Oils Market?

Challenges include fluctuating crude oil prices, the growing popularity of electric vehicles, and the presence of counterfeit products, which may undermine brand trust.

03. Who are the major players in the India Automotive Engine Oils Market?

Key players include Indian Oil Corporation Ltd., Bharat Petroleum Corporation Ltd., Castrol India Ltd., Hindustan Petroleum Corporation Ltd., and Shell India Markets Pvt. Ltd., among others.

04. What are the growth drivers of the India Automotive Engine Oils Market?

Growth is driven by increasing vehicle sales, advancements in synthetic oil formulations, and stricter government regulations on emission standards.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.