India Automotive Glass Market Outlook to 2030

Region:India

Author(s):Sanjeev

Product Code:KROD2359

Region:India

Author(s):Sanjeev

Product Code:KROD2359

November 2024

83

Listen to the audio summary

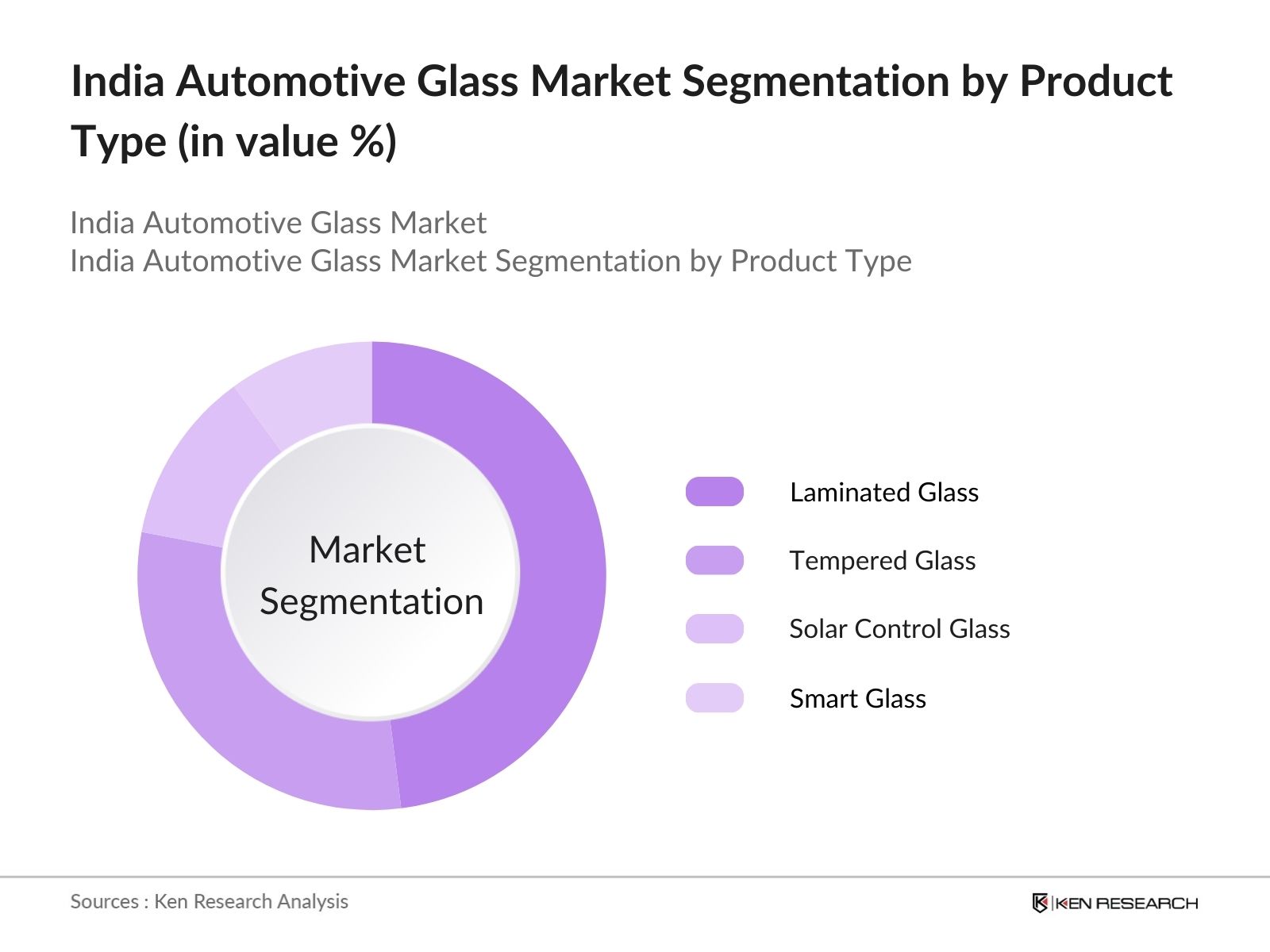

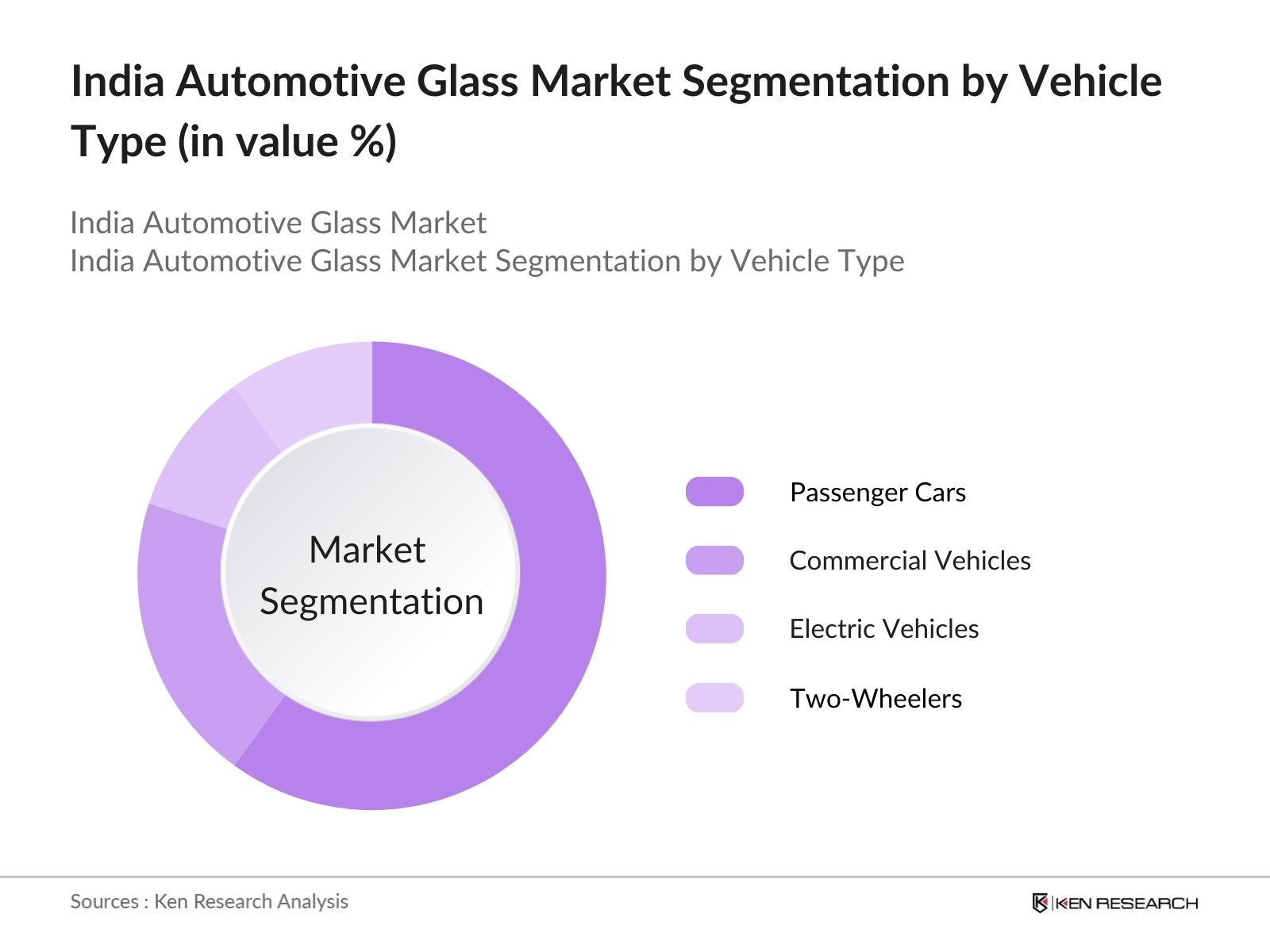

The India Automotive Glass Market is segmented into product and vehicle.

The India automotive glass market is led by major companies such as Asahi India Glass Ltd., Saint-Gobain Sekurit India Ltd., and Gujarat Borosil Limited. These companies dominate the market due to their established manufacturing capacities, extensive distribution networks, and continuous investment in research and development (R&D) to produce innovative glass products. Additionally, the presence of global players like Nippon Sheet Glass and Xinyi Glass Holdings further intensifies competition, driving technological advancements and price competitiveness.

|

Company Name |

Establishment Year |

Headquarters |

Product Portfolio |

R&D Investment (INR Mn) |

Manufacturing Locations |

Revenue (INR Bn) |

Technological Innovations |

|

Asahi India Glass Ltd. |

1984 |

Gurugram, India |

|||||

|

Saint-Gobain Sekurit India |

1997 |

Chennai, India |

|||||

|

Gujarat Borosil Limited |

1988 |

Gujarat, India |

|||||

|

Nippon Sheet Glass Co., Ltd. |

1918 |

Tokyo, Japan |

|||||

|

Xinyi Glass Holdings Ltd. |

1988 |

Hong Kong |

The India automotive glass market is expected to experience significant growth over the next five years, driven by advancements in glass technology, the rising production of electric vehicles, and the increasing adoption of safety standards. Innovations in lightweight and energy-efficient glass will play a pivotal role in the markets expansion, particularly in the passenger car segment. The growing trend towards electric and autonomous vehicles will further fuel demand for advanced glass solutions such as solar control and smart glass.

|

By Product Type |

Laminated Glass Tempered Glass Solar Control Glass Smart Glass |

|

By Vehicle Type |

Passenger Cars Commercial Vehicles Electric Vehicles Two-Wheelers |

|

By Application |

Windshields Side Windows Rear Windows Sunroofs |

|

By End-User Industry |

OEMs Aftermarket |

|

By Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Vehicle Production (OEM demand, Aftermarket demand)

3.1.2. Rising Automotive Safety Standards (Safety glass regulations, Windshield safety standards)

3.1.3. Government Regulations on Automotive Safety (AIS-037, BSVI norms)

3.1.4. Growth in Electric Vehicles (EV market penetration, EV glass needs)

3.2. Market Challenges

3.2.1. High Manufacturing Costs (Raw material pricing, Supply chain constraints)

3.2.2. Environmental Regulations (Emission standards, Sustainable glass production)

3.2.3. Dependence on Import of Raw Materials (Global supply chain disruption, Import duties)

3.3. Opportunities

3.3.1. Development of Smart Glass Technology (Electrochromic glass, Self-tinting glass)

3.3.2. Expansion in Rural Markets (Demand from Tier-2 and Tier-3 cities, Aftermarket opportunities)

3.3.3. Strategic Partnerships with OEMs (Automotive partnerships, Localization strategies)

3.4. Trends

3.4.1. Use of Lightweight Glass for Fuel Efficiency (Tempered glass, Laminated glass)

3.4.2. Integration of Solar Glass in EVs (Solar roofs, Energy-efficient glass)

3.4.3. Growing Adoption of Windshield HUD (Head-Up Display, AR integration in windshields)

3.5. Government Regulation

3.5.1. Automotive Industry Standards (AIS-037 compliance, Road safety norms)

3.5.2. Emission Reduction Initiatives (BSVI, EV incentives)

3.5.3. National Safety Standards for Glass Manufacturing

3.5.4. Public-Private Partnerships for Localization of Glass Production

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Laminated Glass

4.1.2. Tempered Glass

4.1.3. Solar Control Glass

4.1.4. Smart Glass

4.2. By Vehicle Type (In Value %)

4.2.1. Passenger Cars

4.2.2. Commercial Vehicles

4.2.3. Electric Vehicles

4.2.4. Two-Wheelers

4.3. By Application (In Value %)

4.3.1. Windshields

4.3.2. Side Windows

4.3.3. Rear Windows

4.3.4. Sunroofs

4.4. By End-User (In Value %)

4.4.1. OEMs

4.4.2. Aftermarket

4.5. By Region (In Value %)

4.5.1. Northern India

4.5.2. Southern India

4.5.3. Western India

4.5.4. Eastern India

5.1 Detailed Profiles of Major Companies

5.1.1. Asahi India Glass Ltd.

5.1.2. Saint-Gobain Sekurit India Ltd.

5.1.3. Gujarat Borosil Limited

5.1.4. Nippon Sheet Glass Co., Ltd.

5.1.5. Xinyi Glass Holdings Limited

5.1.6. Fuyao Glass Industry Group Co., Ltd.

5.1.7. Pilkington Automotive Ltd.

5.1.8. Guardian Industries

5.1.9. AGC Glass Europe

5.1.10. Vitro, S.A.B. de C.V.

5.1.11. Central Glass Co., Ltd.

5.1.12. PPG Industries

5.1.13. Magna International Inc.

5.1.14. Independent Glass Co. Ltd.

5.1.15. Glavostek Group

5.2 Cross Comparison Parameters (Product Portfolio, Production Capacity, Manufacturing Locations, R&D Investment, Key Patents, Strategic Partnerships, Supply Chain Integration, Revenue Breakdown)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Safety Standards for Glass (Crash test standards, Windshield safety standards)

6.2. Compliance Requirements (AIS standards, Emission regulations)

6.3. Certification Processes (ISO certification, Industry approvals)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Vehicle Type (In Value %)

8.3. By Application (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The research process begins by mapping out key variables that impact the India automotive glass market, including vehicle production trends, technological advancements, and regulatory requirements. This is done through a combination of secondary research, utilizing proprietary databases and government reports.

Historical market data is analyzed to evaluate the growth trajectory of the India automotive glass market. The analysis focuses on market penetration, vehicle production, and the ratio of OEM demand to aftermarket demand. Data from trusted sources, such as the Ministry of Road Transport and Highways, is used to ensure accuracy.

Interviews with industry experts, including manufacturers and OEM representatives, are conducted to validate market assumptions and refine data estimates. These insights help address operational and financial challenges faced by the industry.

The final stage involves synthesizing insights from expert consultations, historical data, and secondary research to produce a comprehensive analysis. This ensures the accuracy and relevance of the final report.

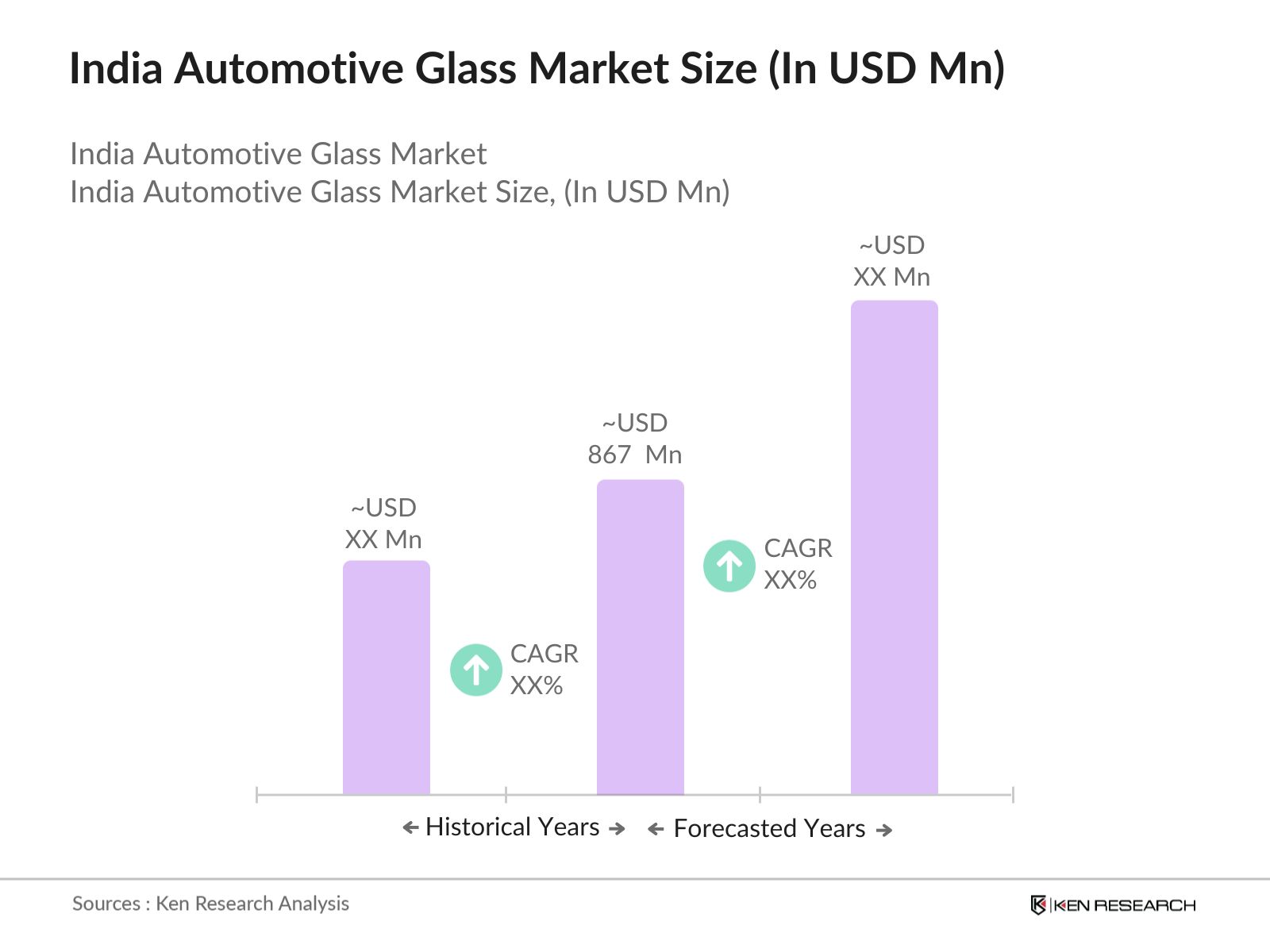

The India Automotive Glass Market is valued at 867 million, driven by rising vehicle production and increasing demand for advanced glass technologies.

Key challenges include high manufacturing costs for advanced glass products and supply chain disruptions, particularly in the sourcing of raw materials.

Major players include Asahi India Glass Ltd., Saint-Gobain Sekurit India Ltd., Gujarat Borosil Limited, Nippon Sheet Glass Co., Ltd., and Xinyi Glass Holdings Ltd.

The market is driven by rising vehicle production, government regulations mandating safety glass, and the growing adoption of electric vehicles in India.

Laminated glass dominates the market, especially in windshields, due to its safety benefits and soundproofing capabilities.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.