India Autonomous Vehicle Market Outlook to 2030

Region:India

Author(s):Paribhasha Tiwari

Product Code:KROD3518

Region:India

Author(s):Paribhasha Tiwari

Product Code:KROD3518

December 2024

85

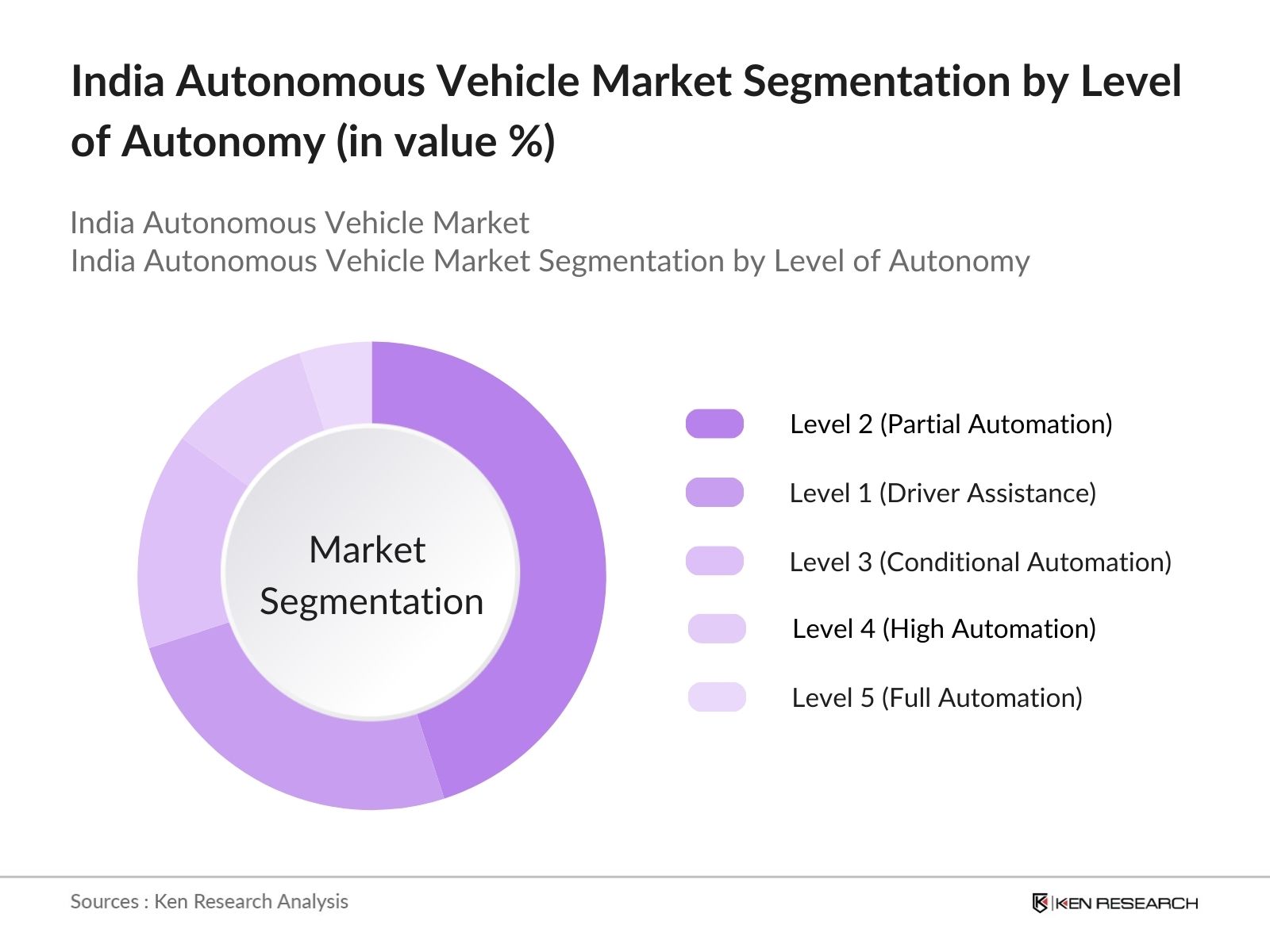

By Level of Autonomy: The India Autonomous Vehicle market is segmented by the level of autonomy into Level 1 (Driver Assistance), Level 2 (Partial Automation), Level 3 (Conditional Automation), Level 4 (High Automation), and Level 5 (Full Automation). Level 2 vehicles currently hold a dominant market share, driven by the increasing adoption of advanced driver-assistance systems (ADAS) in passenger vehicles. The popularity of Level 2 automation is largely due to its affordability and availability in a wide range of vehicle models, making it accessible to a broader consumer base. Furthermore, safety features such as lane-keeping assistance, adaptive cruise control, and automated emergency braking have driven customer demand for these vehicles.

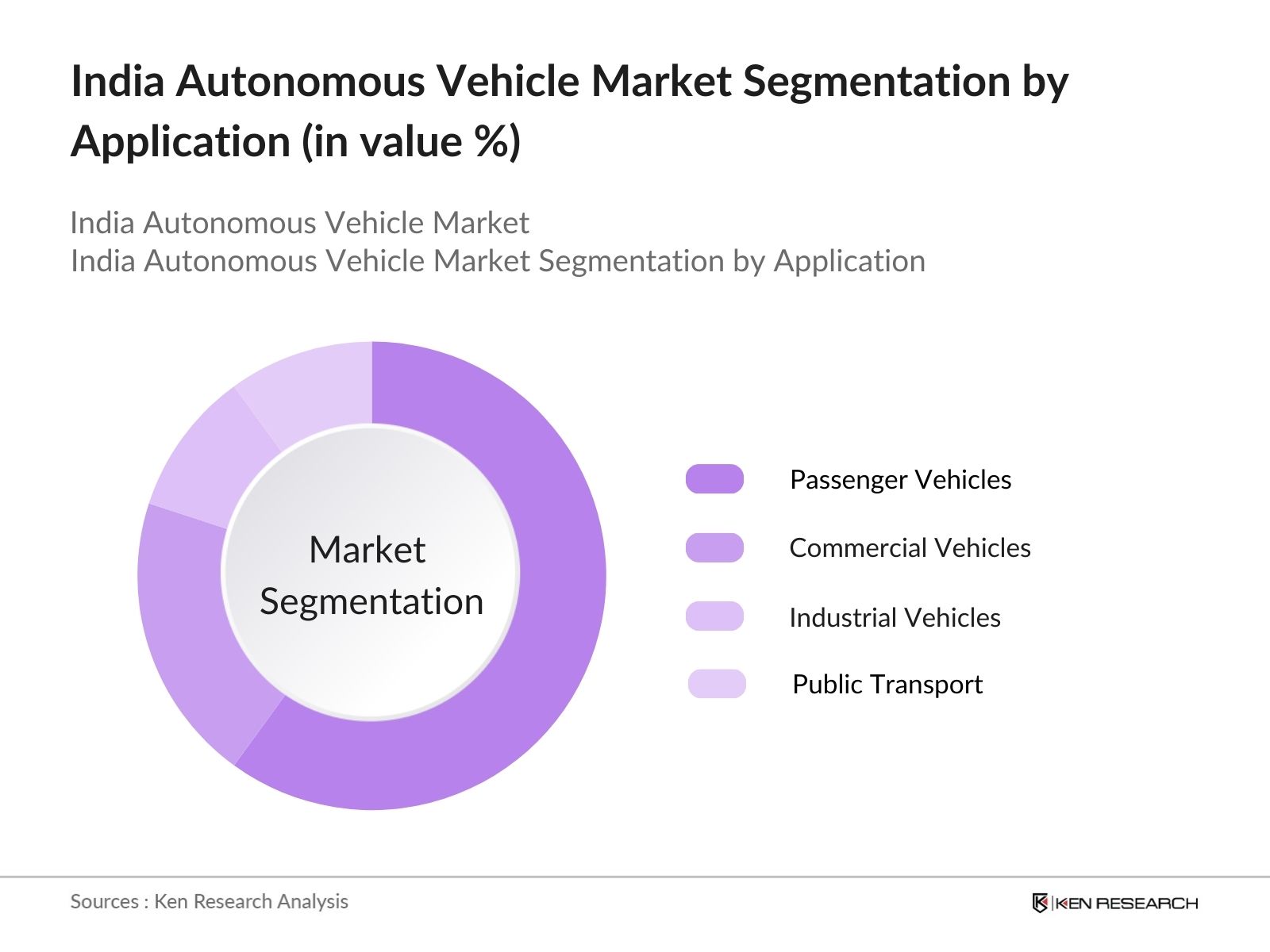

By Application: The India Autonomous Vehicle market is segmented by application into passenger vehicles, commercial vehicles, industrial vehicles, and public transport. Passenger vehicles dominate the market under this segmentation, accounting for the largest share. This is primarily due to the rising demand for personal mobility solutions in metropolitan areas and the growing inclination toward safer, more efficient modes of transportation. The integration of semi-autonomous features in high-end passenger cars, especially from luxury car brands, is also contributing to the dominance of this segment.

The India Autonomous Vehicle market is dominated by a mix of domestic automakers and global technology companies. Established players are forming strategic partnerships with tech firms to accelerate R&D in autonomous driving technologies, such as AI, sensor fusion, and machine learning.

|

Company Name |

Establishment Year |

Headquarters |

R&D Expenditure (USD Mn) |

Market Presence |

Revenue (2023) |

Product Range |

Partnerships |

Patents Held |

|

Tata Motors |

1945 |

Mumbai |

- | - | - | - | - | - |

|

Mahindra & Mahindra |

1945 |

Mumbai |

- | - | - | - | - | - |

|

Ashok Leyland |

1948 |

Chennai |

- | - | - | - | - | - |

|

Tata Elxsi |

1989 |

Bengaluru |

- | - | - | - | - | - |

|

Tech Mahindra |

1986 |

Pune |

- | - | - | - | - | - |

Growth Drivers

Market Challenges

Over the next five years, the India Autonomous Vehicle market is expected to experience robust growth, driven by continuous investments in technology infrastructure, growing public awareness of the benefits of autonomous driving, and supportive government policies. The Indian governments focus on smart cities, coupled with increased research and development by domestic and international automakers, is poised to further drive the adoption of autonomous vehicles. Additionally, advancements in AI, sensor technology, and 5G networks are expected to make autonomous vehicles more reliable and efficient, fueling market demand.

Opportunities

|

By Level of Autonomy |

Level 1 (Driver Assistance) Level 2 (Partial Automation) Level 3 (Conditional Automation) Level 4 (High Automation) Level 5 (Full Automation) |

|

By Application |

Passenger Vehicles Commercial Vehicles Industrial Vehicles Public Transport |

|

By Technology |

Radar-Based Systems Lidar-Based Systems Camera-Based Systems Sensor Fusion Systems |

|

By Mobility Type |

Personal Mobility Shared Mobility Goods Mobility |

|

By Region |

North South East West |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Key Stakeholders Overview

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Current Market Size

2.3. Year-On-Year Growth Analysis

2.4. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Advancements in AI and Machine Learning (Autonomous Decision-Making Capabilities)

3.1.2. Government Initiatives for Smart Transportation (Policies such as National Electric Mobility Mission)

3.1.3. Increasing Investments in Connected Vehicle Infrastructure (IoT and V2X Technology)

3.1.4. Growing Demand for Safety and Reduction in Traffic Accidents (Reduction in Human Error)

3.2. Market Challenges

3.2.1. High Initial Costs and R&D Expenditure (Lidar, Sensor Technology)

3.2.2. Regulatory Hurdles (Lack of Unified Autonomous Driving Laws)

3.2.3. Cybersecurity Threats in Connected Vehicles (Hacking and Data Privacy Issues)

3.2.4. Limited Road Infrastructure Readiness (Smart Infrastructure)

3.3. Opportunities

3.3.1. Expansion of Fleet and Mobility-as-a-Service (Self-Driving Taxis and Ride-Hailing Services)

3.3.2. Technological Advancements in Sensor Fusion and Real-Time Mapping (AI-driven Sensor Systems)

3.3.3. Collaborations Between Automakers and Tech Companies (Strategic Partnerships for AV Development)

3.3.4. Penetration into Tier-2 and Tier-3 Cities (Expanding Roadmaps for Autonomous Solutions)

3.4. Trends

3.4.1. Integration with Electric Vehicles (Autonomous EV Development)

3.4.2. Rise in 5G Deployment for Vehicle-to-Everything (V2X) Communication (High-Speed Data Transmission)

3.4.3. Shift Towards Level 4 and Level 5 Automation (Fully Autonomous Driving)

3.4.4. Increased Adoption of Autonomous Vehicles in Logistics and Freight Transport (Automated Trucks and Drones)

4.1. By Level of Autonomy (In Value %)

4.1.1. Level 1 (Driver Assistance)

4.1.2. Level 2 (Partial Automation)

4.1.3. Level 3 (Conditional Automation)

4.1.4. Level 4 (High Automation)

4.1.5. Level 5 (Full Automation)

4.2. By Application (In Value %)

4.2.1. Passenger Vehicles

4.2.2. Commercial Vehicles

4.2.3. Industrial Vehicles

4.2.4. Public Transport

4.3. By Technology (In Value %)

4.3.1. Radar-Based Systems

4.3.2. Lidar-Based Systems

4.3.3. Camera-Based Systems

4.3.4. Sensor Fusion Systems

4.4. By Mobility Type (In Value %)

4.4.1. Personal Mobility

4.4.2. Shared Mobility

4.4.3. Goods Mobility

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. East India

4.5.4. West India

5.1. Detailed Profiles of Major Companies

5.1.1. Tata Motors Ltd.

5.1.2. Mahindra & Mahindra

5.1.3. Maruti Suzuki India Ltd.

5.1.4. Ashok Leyland

5.1.5. Tech Mahindra Ltd.

5.1.6. Tata Elxsi

5.1.7. Infosys Limited

5.1.8. Wipro Limited

5.1.9. Hyundai Mobis India

5.1.10. Bosch India

5.1.11. Continental Automotive India

5.1.12. ZF Friedrichshafen AG

5.1.13. NVIDIA India

5.1.14. Waymo India

5.1.15. Intel India Pvt. Ltd.

5.2. Cross Comparison Parameters

5.2.1. Number of Employees

5.2.2. Headquarters

5.2.3. R&D Expenditure

5.2.4. Partnerships and Collaborations

5.2.5. Investment in Autonomous Driving Solutions

5.2.6. Product Innovation and Patents

5.2.7. Market Share (In Value %)

5.2.8. Strategic Initiatives

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. National Electric Mobility Mission (NEMM)

6.2. Ministry of Road Transport and Highways (MoRTH) Initiatives

6.3. Autonomous Vehicle Testing Standards

6.4. Safety and Compliance Regulations

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Level of Autonomy (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Mobility Type (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Behavior and Adoption Analysis

9.3. Key Market Entry Strategies

9.4. Competitive Positioning Strategies

The initial stage involves mapping out key stakeholders within the India Autonomous Vehicle market ecosystem. A combination of desk research and proprietary databases was used to identify key variables affecting market dynamics, including technological advancements, government initiatives, and industry collaborations.

This phase involved gathering and analyzing historical data related to the India Autonomous Vehicle market. Parameters such as adoption rates of autonomous features, penetration in different vehicle types, and infrastructure development were assessed to create reliable revenue models.

Market hypotheses were validated through consultations with industry experts from automakers and technology providers. These interviews were conducted via Computer-Assisted Telephone Interviews (CATI), providing real-time insights into market trends and technological advancements.

This step involved integrating the insights gathered from primary research with data from industry databases, ensuring comprehensive coverage of the market. Detailed inputs from OEMs and tech firms helped validate the final market analysis.

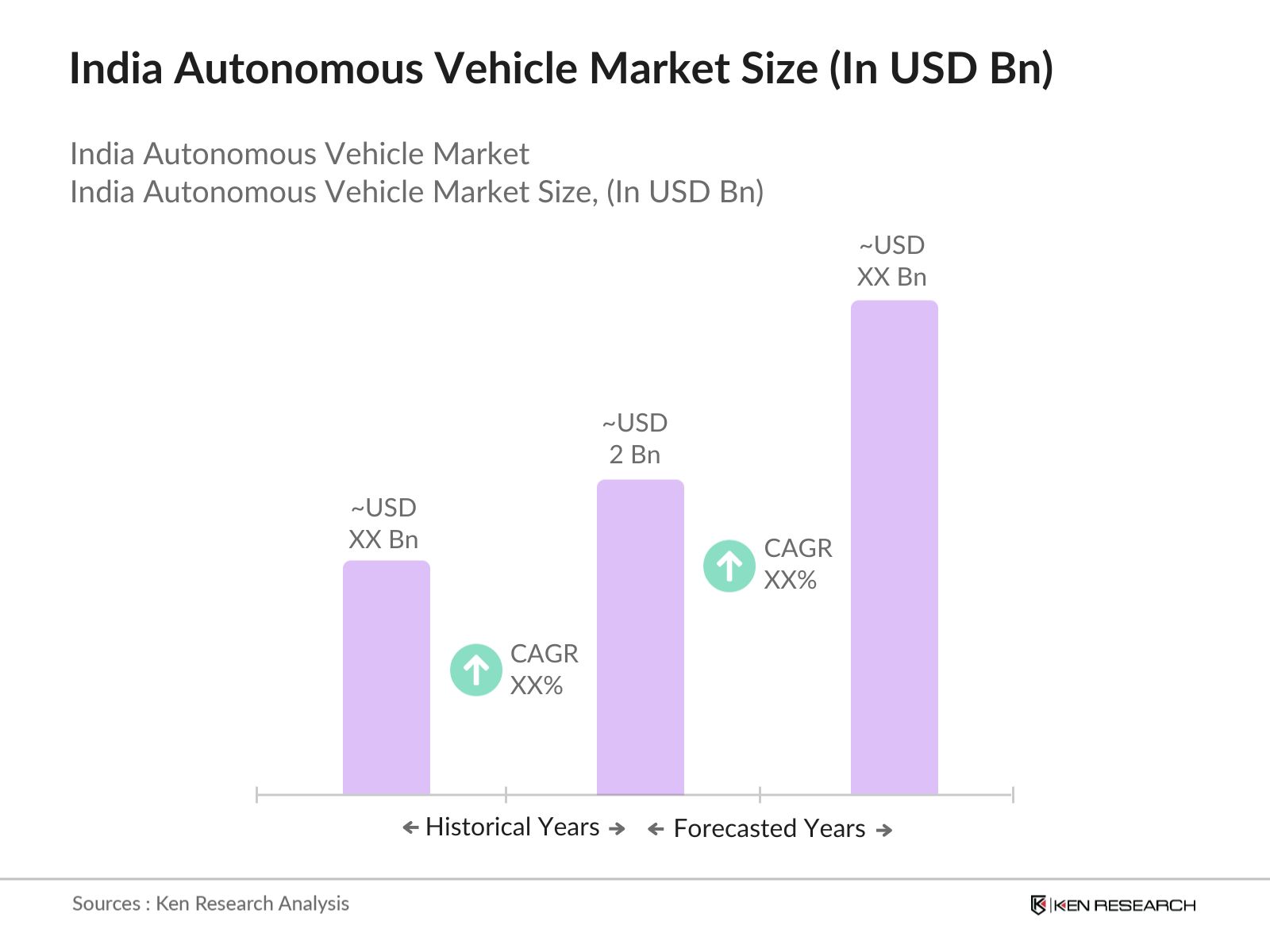

The India Autonomous Vehicle Market is valued at USD 2 billion, driven by increased investments in autonomous technologies, collaborations between automotive and tech companies, and supportive government initiatives.

The India Autonomous Vehicle Market faces challenges such as high initial R&D costs, regulatory complexities, and cybersecurity concerns. Additionally, the lack of smart infrastructure in certain regions is slowing down market adoption.

Key players in the India Autonomous Vehicle Market include Tata Motors, Mahindra & Mahindra, Ashok Leyland, Tata Elxsi, and Tech Mahindra. These companies dominate due to their significant investments in autonomous technologies and strong market presence.

Growth drivers in the India Autonomous Vehicle Market include advancements in AI, sensor fusion technology, government initiatives to reduce emissions, and the increasing demand for safe and efficient transportation solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.