India Baby Toys Market Outlook to 2030

Region:India

Author(s):Sanjeev

Product Code:KROD9846

Region:India

Author(s):Sanjeev

Product Code:KROD9846

October 2024

99

Listen to the audio summary

India Baby Toys Market Segmentation

Indias baby toys market is segmented by product type and by age group.

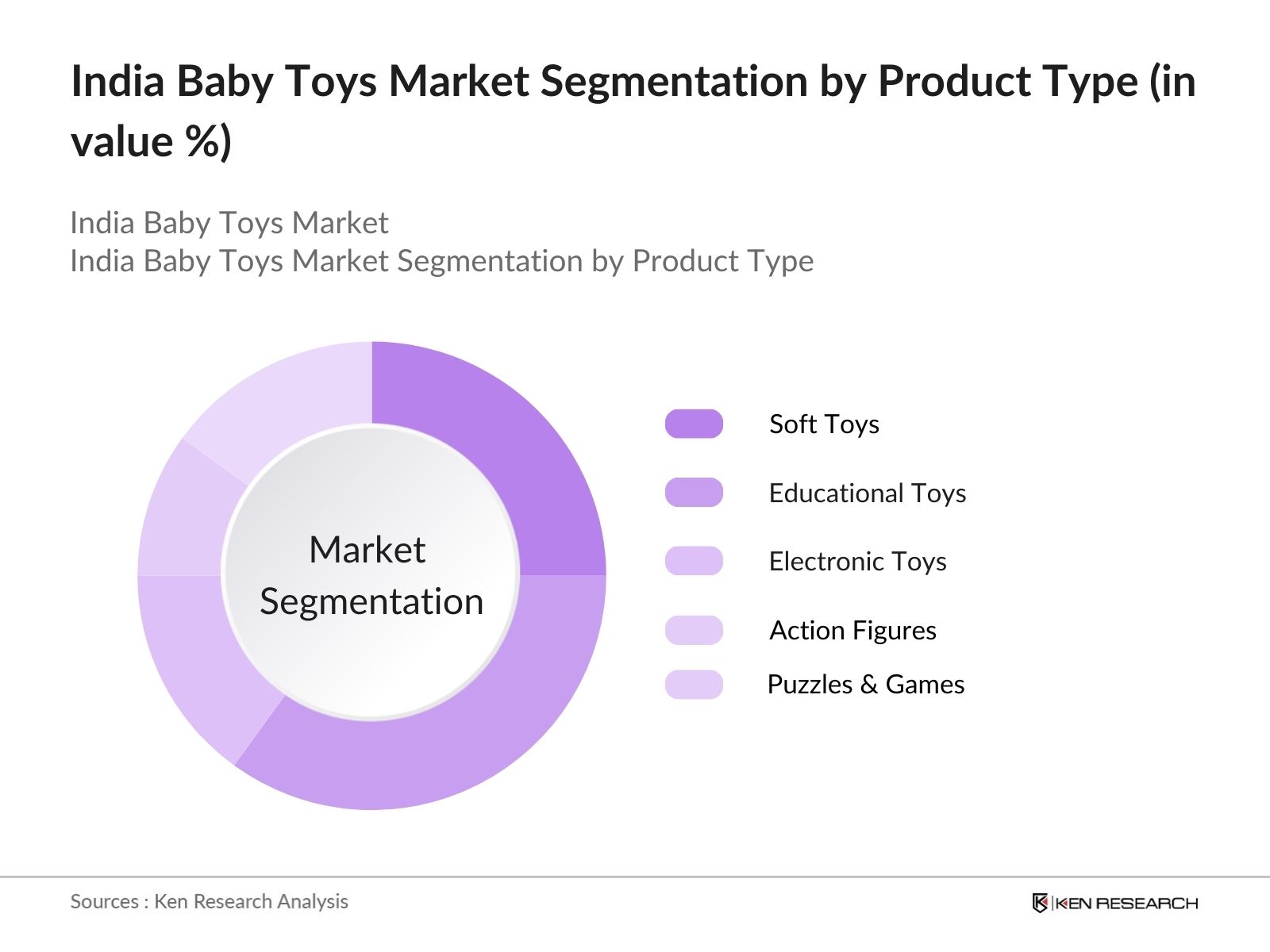

By Product Type: The market is segmented by product type into soft toys, educational toys, electronic toys, action figures, and puzzles & board games. Among these, educational toys have seen a dominant market share in India, driven by an increasing focus on cognitive and motor skill development among young children. Parents are increasingly inclined toward purchasing toys that enhance learning and development, backed by various early childhood education programs initiated by both private and public institutions. This has made educational toys a preferred option among parents, especially in urban areas.

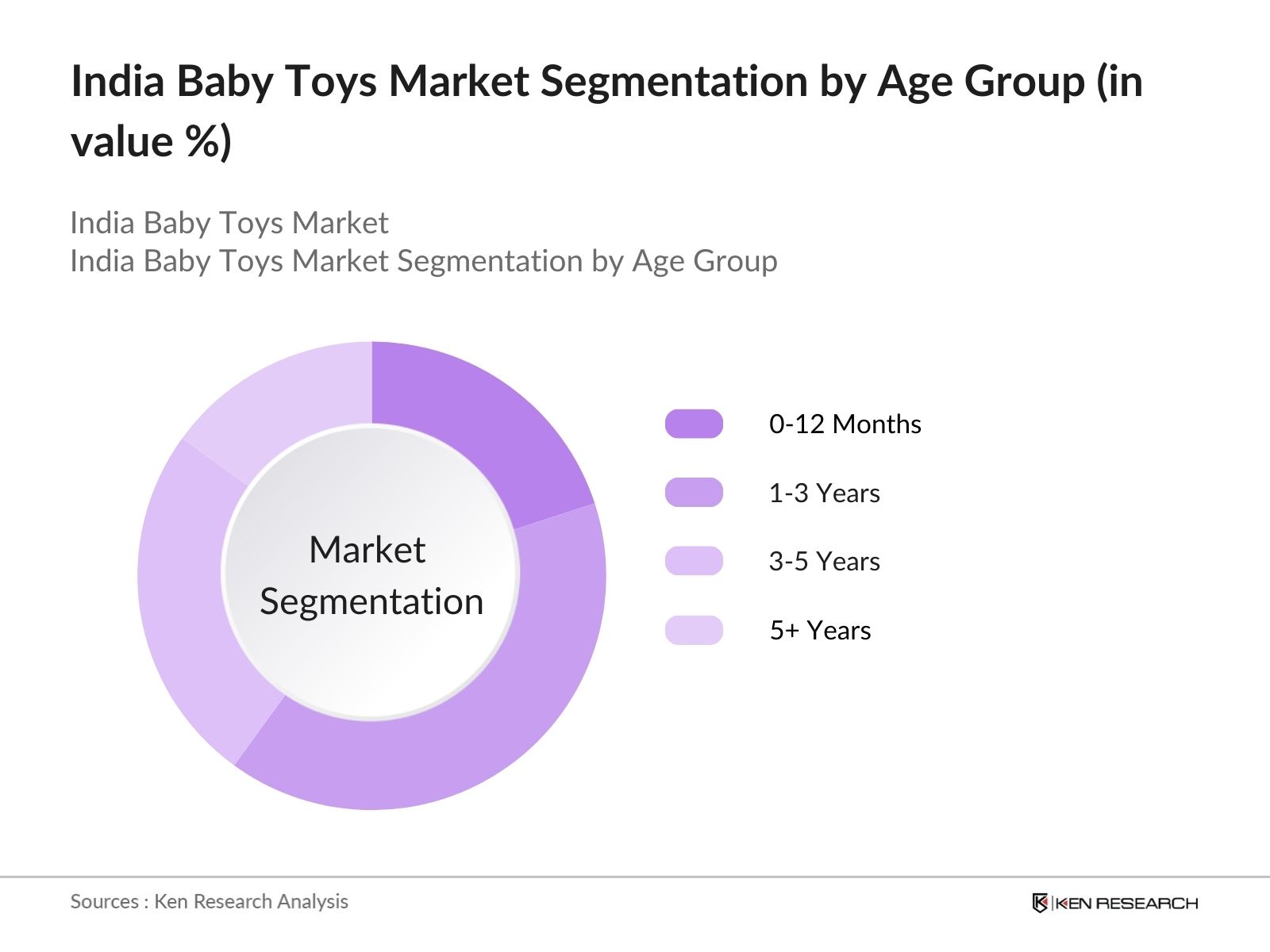

By Age Group: The market is also segmented by age group into 0-12 months, 1-3 years, 3-5 years, and 5+ years. The 1-3 years age group dominates the market, as this is the period when most parents focus on the rapid cognitive and motor development of their children. Toys designed for this age group are generally focused on learning, engagement, and creativity. With the introduction of more interactive and sensory toys, this segment continues to drive the overall market. Toy companies are also heavily marketing to this group through vibrant and age-appropriate products, which cater to both educational and entertainment needs.

India Baby Toys Market Competitive Landscape

The India Baby Toys market is dominated by both domestic and international players. Major players like Funskool, Lego India, and Mattel have a significant presence, supported by their extensive distribution networks and brand loyalty. Indian companies such as Funride and Centy Toys have also carved out a strong niche, focusing on affordable and safe toys designed specifically for Indian children. The consolidation of key companies highlights their market influence, with both local and global brands actively participating in shaping the industry's future.

|

Company |

Establishment Year |

Headquarters |

Revenue (INR Cr) |

No. of Employees |

Product Range |

Brand Presence |

R&D Investments |

Distribution Network |

Market Penetration |

|

Funskool (India) Ltd. |

1987 |

Chennai, India |

|||||||

|

Lego India Pvt Ltd |

2003 |

Mumbai, India |

|||||||

|

Mattel Toys India Pvt Ltd |

1988 |

Mumbai, India |

|||||||

|

Simba Toys India Pvt Ltd |

1995 |

Delhi, India |

|||||||

|

Funride Toys |

1990 |

Mumbai, India |

India Baby Toys Industry Analysis

Growth Drivers

Market Challenges

India Baby Toys Market Future Outlook

The India Baby Toys market is expected to witness significant growth over the next five years, driven by a growing population, increasing parental focus on early childhood development, and rising disposable income. Additionally, government initiatives to support local toy manufacturers under the Make in India campaign are anticipated to reduce reliance on imports and boost domestic production. The shift toward eco-friendly and educational toys is also expected to create new growth avenues for manufacturers.

Market Opportunities

|

||||

|

By Distribution Channel |

Offline Retail Online Channels Specialty Stores Supermarkets & Hypermarkets |

|||

|

By Age Group |

0-12 Months 1-3 Years 3-5 Years 5+ Years |

|||

|

By Material |

Plastic Fabric Wood Metal |

|||

|

By Region |

North East West South |

Funskool (India) Ltd.

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Birth Rate (Indian Census Data)

3.1.2. Rising Disposable Income (NSSO Data)

3.1.3. E-Commerce Penetration (Indias Digital Economy Report)

3.1.4. Expansion of Organized Retail (Ministry of Commerce)

3.2. Market Challenges

3.2.1. Lack of Quality Standards (Bureau of Indian Standards)

3.2.2. High Import Dependency (Directorate General of Commercial Intelligence and Statistics)

3.2.3. Price Sensitivity of Consumers (NCAER Data)

3.3. Opportunities

3.3.1. Growing Awareness on Early Childhood Development (National Early Childhood Care Policy)

3.3.2. Adoption of Educational Toys (NCERT Guidelines on Education)

3.3.3. Government Initiatives for Local Manufacturing (Make in India Campaign)

3.4. Trends

3.4.1. Eco-friendly and Sustainable Toys (FICCI Reports)

3.4.2. Rise in STEM Toys Demand (NITI Aayog STEM Education Insights)

3.4.3. Increase in Customizable and Personalized Toys (Consumer Behavior Report by ASSOCHAM)

3.5. Government Regulation

3.5.1. BIS Certification for Toys

3.5.2. Import Regulations and Tariffs (DGFT Policies)

3.5.3. Indian Toy Industry Development Initiatives (Ministry of MSME)

3.5.4. Compliance with Child Safety Laws (The Consumer Protection Act)

3.6. SWOT Analysis

3.7. Stake Ecosystem (Manufacturers, Distributors, Retailers, and End-Users)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Soft Toys

4.1.2. Educational Toys

4.1.3. Electronic Toys

4.1.4. Action Figures

4.1.5. Puzzles & Board Games

4.2. By Age Group (In Value %)

4.2.1. 0-12 Months

4.2.2. 1-3 Years

4.2.3. 3-5 Years

4.2.4. 5+ Years

4.3. By Distribution Channel (In Value %)

4.3.1. Offline Retail (Organized and Unorganized)

4.3.2. Online Channels (E-Commerce)

4.3.3. Specialty Stores

4.3.4. Supermarkets & Hypermarkets

4.4. By Material (In Value %)

4.4.1. Plastic

4.4.2. Fabric

4.4.3. Wood

4.4.4. Metal

4.5. By Region (In Value %)

4.5.1. North

4.5.2. South

4.5.3. West

4.5.4. East

5.1 Detailed Profiles of Major Companies

5.1.1. Funskool (India) Ltd.

5.1.2. Lego India Pvt Ltd

5.1.3. Mattel Toys India Pvt Ltd

5.1.4. Simba Toys India Pvt Ltd

5.1.5. Fisher-Price (Mattel India)

5.1.6. Hamleys India (Reliance Brands Ltd.)

5.1.7. Hasbro India LLP

5.1.8. Chicco India

5.1.9. Frank Educational Aids Pvt Ltd

5.1.10. Zephyr Toymakers Pvt Ltd

5.1.11. Funride Toys

5.1.12. Centy Toys

5.1.13. Winmagic Toys Pvt Ltd

5.1.14. Green Gold Animation Pvt Ltd (Chhota Bheem Merchandise)

5.1.15. Toykraft Pvt Ltd

5.2 Cross Comparison Parameters (Revenue, Number of Employees, Product Offerings, Production Capacity, R&D Investments, Brand Penetration, Market Share, Inception Year)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1. BIS Certification

6.2. Compliance with Safety Standards

6.3. Environmental Standards (Plastic Ban Regulations)

6.4. Import Restrictions and Duties

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Age Group (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By Material (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The first phase involves creating a comprehensive ecosystem map of stakeholders in the India Baby Toys market. Desk research, using both secondary sources and proprietary databases, helps in gathering broad market-level information. The aim is to identify crucial variables affecting the market dynamics.

This step focuses on analyzing historical data from the India Baby Toys market, assessing market penetration, revenue generation from retailers, and overall demand. This also includes service quality analysis, which helps verify the accuracy of data.

Market assumptions are validated through consultations with key industry stakeholders, including manufacturers and retailers. These interviews help refine market insights and provide additional operational and financial data to cross-verify findings.

The final step entails a detailed engagement with toy manufacturers to collect insights on product segments, consumer behavior, and sales trends. This phase ensures a comprehensive, accurate, and validated market analysis through both top-down and bottom-up approaches.

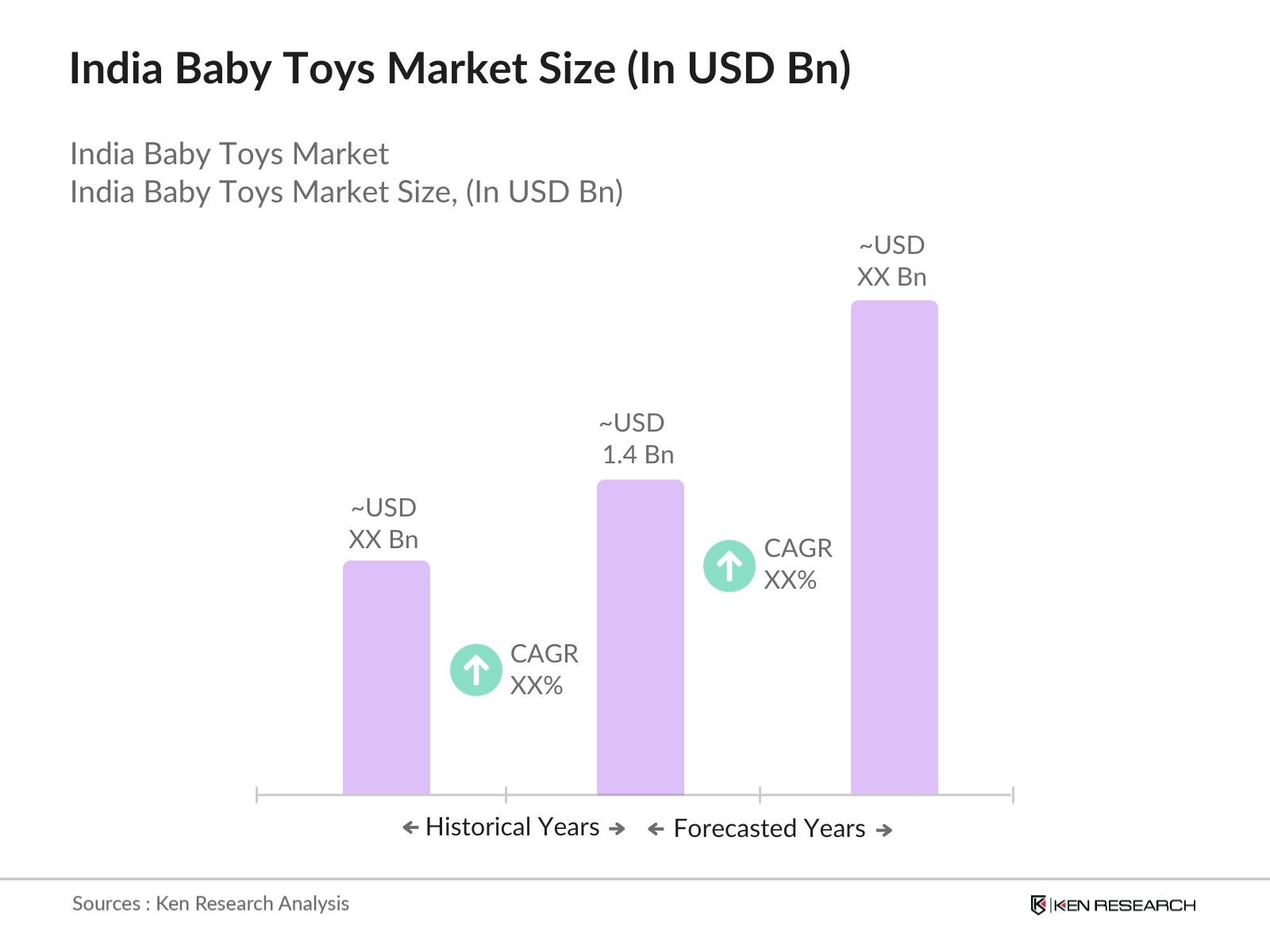

The India Baby Toys market is valued at USD 1.4 billion, driven by rising disposable incomes and increasing focus on early childhood education.

Challenges in India Baby Toys market include import dependency, lack of quality standards, and the rising cost of raw materials, which affects the production of toys.

Key players in India Baby Toys market include Funskool (India) Ltd, Lego India, Mattel Toys India Pvt Ltd, Simba Toys India Pvt Ltd, and Fisher-Price (Mattel India), all dominating through their strong distribution networks.

The India Baby Toys market is driven by increased disposable income, a growing population, and the penetration of e-commerce platforms providing greater access to a variety of toy options.

Recent trends in India Baby Toys markeinclude the rise in demand for eco-friendly toys and the growing interest in educational toys aimed at developing cognitive skills.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.