India Biopharmaceutical Market Outlook to 2030

Region:India

Author(s):Naman Rohilla

Product Code:KROD3553

Region:India

Author(s):Naman Rohilla

Product Code:KROD3553

November 2024

99

The India biopharmaceutical market is dominated by a mix of domestic and international players, with companies focused on R&D, manufacturing, and commercialization. Several key players have established research facilities and manufacturing capacities, benefiting from government policies like the 'Make in India' initiative and investment in biotechnology clusters like Genome Valley. The competition is shaped by innovation in biosimilars, strategic partnerships, and collaborations with research institutions.

|

Company |

Year Established |

Headquarters |

No. of Employees |

R&D Investment (USD) |

Key Product Segment |

Global Presence |

Revenue from Biopharma (USD) |

|

Biocon Limited |

1978 |

Bangalore |

- |

- |

- |

- |

- |

|

Dr. Reddys Laboratories |

1984 |

Hyderabad |

- |

- |

- |

- |

- |

|

Sun Pharmaceutical |

1983 |

Mumbai |

- |

- |

- |

- |

- |

|

Serum Institute of India |

1966 |

Pune |

- |

- |

- |

- |

- |

|

Cipla Limited |

1935 |

Mumbai |

- |

- |

- |

- |

- |

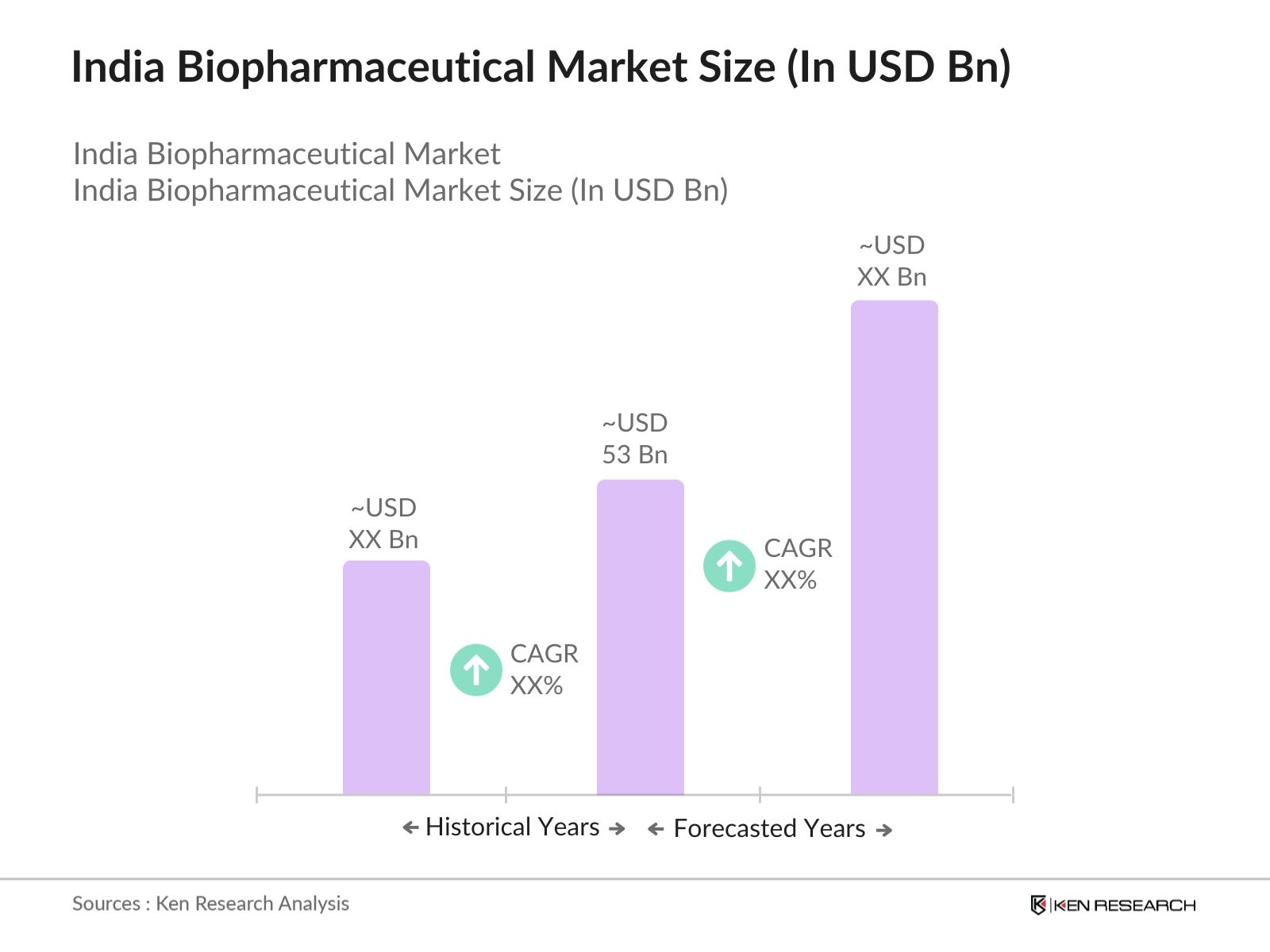

The India biopharmaceutical market is expected to show substantial growth over the next five years. This growth is driven by the increasing demand for innovative biologic therapies, continuous advancements in gene and cell therapies, and a rapidly expanding biosimilars market. Additionally, favorable government policies, such as the National Biopharma Mission, and public-private partnerships will play a key role in driving this expansion. The rising investments in biotechnology research and the development of state-of-the-art manufacturing facilities will further strengthen India's position in the global market.

|

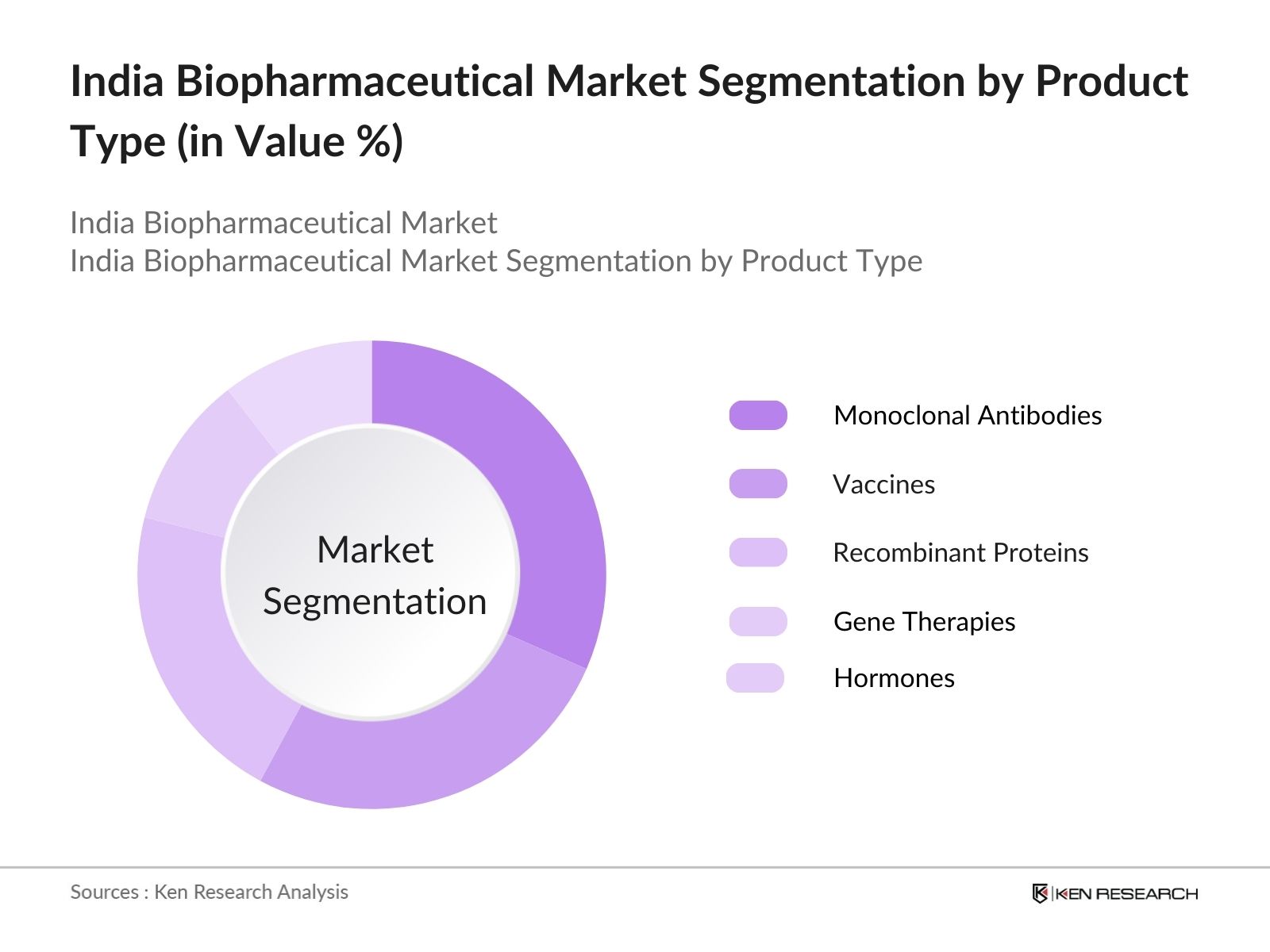

By Product Type |

Monoclonal Antibodies Vaccines Hormones Enzymes Gene Therapy Products |

|

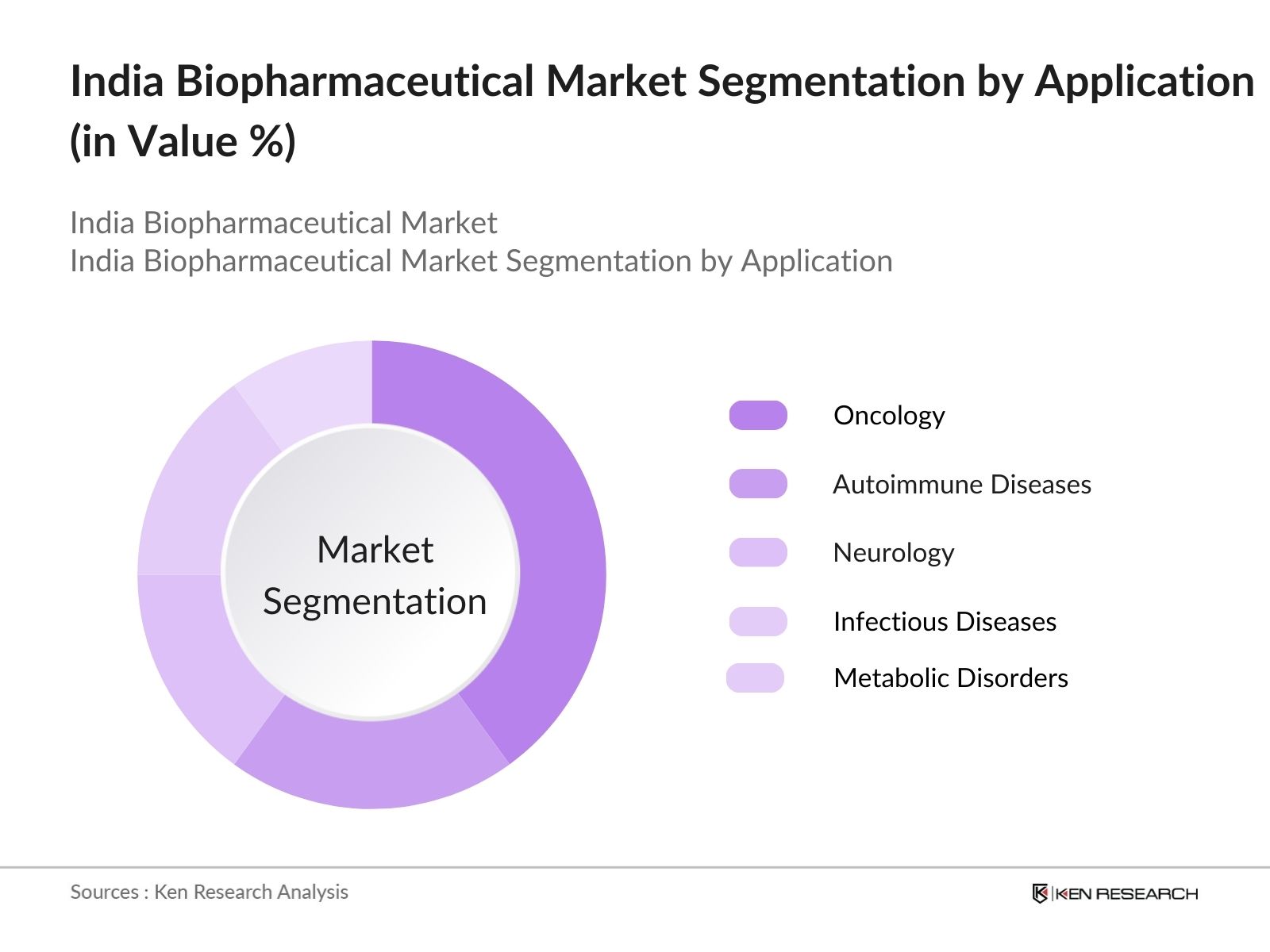

By Application |

Oncology Autoimmune Diseases Metabolic Disorders Neurology Infectious Diseases |

|

By Technology |

Recombinant DNA Technology Hybridoma Technology Gene Editing Cell Culture Technology Protein Purification Technology |

|

By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies Specialty Clinics |

|

By Region |

North India South India West India East India |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Regulatory environment, R&D intensity, Public-Private Partnerships)

1.4. Market Segmentation Overview

2.1. Historical Market Size (Product pipeline, R&D expenditures, Drug commercialization timelines)

2.2. Year-On-Year Growth Analysis (Clinical trial outcomes, Biologic approvals)

2.3. Key Market Developments and Milestones (Breakthrough therapies, Biosimilar introductions, Biologic patent expiries)

3.1. Growth Drivers

3.1.1. Increasing Prevalence of Chronic Diseases

3.1.2. Rising Healthcare Expenditure

3.1.3. Strong Government Initiatives (e.g., National Biopharma Mission)

3.1.4. Technological Advancements (Bioprocessing innovations, mRNA technology)

3.1.5. Growth of Personalized Medicine

3.1.6. Collaborations and Strategic Partnerships

3.2. Market Challenges

3.2.1. High Manufacturing Costs

3.2.2. Complex Regulatory Approvals

3.2.3. Skilled Workforce Deficiency

3.2.4. Patent Expirations and Market Competition

3.2.5. Limited Infrastructure for Advanced Therapies

3.3. Opportunities

3.3.1. Expanding Contract Manufacturing Organizations (CMOs)

3.3.2. Biosimilar Growth Potential

3.3.3. Outsourcing R&D Activities

3.3.4. Emerging Markets for Biopharmaceuticals

3.4. Trends

3.4.1. Expansion of mRNA and Gene Therapy

3.4.2. Shift towards Continuous Manufacturing

3.4.3. Increasing Investments in Oncology Biopharmaceuticals

3.4.4. Rise in Biologics for Autoimmune Diseases

3.5. Government Regulation

3.5.1. Drug Pricing Controls

3.5.2. Biopharma-specific Regulatory Guidelines (Biosimilars, Cell & Gene Therapies)

3.5.3. Clinical Trial Reforms

3.5.4. Fast-track Approvals for Breakthrough Therapies

3.6. SWOT Analysis

3.6.1. Strengths (Skilled Workforce, R&D Capabilities)

3.6.2. Weaknesses (Regulatory Delays, Lack of Infrastructure)

3.6.3. Opportunities (Global Export Potential, Growing Domestic Demand)

3.6.4. Threats (International Competition, Price Pressures)

3.7. Stakeholder Ecosystem

3.7.1. Manufacturers

3.7.2. Distributors

3.7.3. Research Institutions

3.7.4. Regulatory Bodies (CDSCO, DBT)

3.8. Porters Five Forces Analysis

3.8.1. Bargaining Power of Suppliers (Raw Materials, APIs)

3.8.2. Bargaining Power of Buyers (Hospitals, Distributors, Retail Pharmacies)

3.8.3. Threat of New Entrants (Barriers to Entry, Patent Protections)

3.8.4. Threat of Substitutes (Small Molecule Drugs, Generic Medicines)

3.8.5. Competitive Rivalry (Market Consolidation, M&A Activity)

4.1. By Product Type (In Value %)

4.1.1. Monoclonal Antibodies

4.1.2. Vaccines

4.1.3. Hormones

4.1.4. Enzymes

4.1.5. Gene Therapy Products

4.2. By Application (In Value %)

4.2.1. Oncology

4.2.2. Autoimmune Diseases

4.2.3. Metabolic Disorders

4.2.4. Neurology

4.2.5. Infectious Diseases

4.3. By Technology (In Value %)

4.3.1. Recombinant DNA Technology

4.3.2. Hybridoma Technology

4.3.3. Gene Editing

4.3.4. Cell Culture Technology

4.3.5. Protein Purification Technology

4.4. By Distribution Channel (In Value %)

4.4.1. Hospital Pharmacies

4.4.2. Retail Pharmacies

4.4.3. Online Pharmacies

4.4.4. Specialty Clinics

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. West India

4.5.4. East India

5.1. Detailed Profiles of Major Companies

5.1.1. Biocon Limited

5.1.2. Dr. Reddys Laboratories

5.1.3. Sun Pharmaceutical Industries

5.1.4. Zydus Cadila

5.1.5. Cipla Limited

5.1.6. Wockhardt Ltd.

5.1.7. Lupin Limited

5.1.8. Serum Institute of India

5.1.9. Panacea Biotec

5.1.10. Bharat Biotech

5.1.11. Intas Pharmaceuticals

5.1.12. Gland Pharma

5.1.13. Aurobindo Pharma

5.1.14. Hetero Drugs

5.1.15. Glenmark Pharmaceuticals

5.2. Cross Comparison Parameters (No. of Employees, Manufacturing Capacity, Clinical Trial Network, R&D Investments, Regulatory Approvals, Product Portfolio, Revenue Contribution from Biopharma, Global Presence)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Drug Approval Process

6.2. Intellectual Property Rights (IPR) for Biopharmaceuticals

6.3. Clinical Trial Regulations

6.4. Compliance and Certification Standards

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThe initial step involves mapping the key stakeholders in the India biopharmaceutical market. This is achieved through extensive desk research using proprietary databases and secondary sources. The focus is to identify the primary variables influencing the market, such as regulatory frameworks, R&D investments, and technological advancements.

This step includes compiling historical data and analyzing trends in the biopharmaceutical market, particularly focusing on the development of biosimilars, gene therapies, and other biologic drugs. This data is used to build a comprehensive analysis of the market's past performance and revenue generation patterns.

Hypotheses about market growth and challenges are developed based on initial data and then validated through interviews with industry experts. These interviews provide insight into operational trends and strategic developments from leading biopharma firms.

In the final step, we consolidate all gathered information through a bottom-up approach, ensuring a validated and complete analysis of the biopharmaceutical market. This process includes collaboration with manufacturers to cross-check production data and market forecasts.

The India biopharmaceutical market is valued at USD 53 billion, driven by increasing demand for biologic treatments and government initiatives supporting biotechnology.

Challenges include high production costs, stringent regulatory approvals, and the need for skilled professionals in advanced biotechnology processes.

Key players include Biocon Limited, Dr. Reddys Laboratories, Sun Pharmaceutical Industries, Cipla Limited, and Serum Institute of India, all of which have investments in biosimilars and biologics.

The market is driven by increased R&D in biologics, rising healthcare expenditures, government support for biotechnology, and the growth of personalized medicine.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.