India Cancer Immunotherapy Market Outlook to 2030

Region:India

Author(s):Sanjeev

Product Code:KROD9692

Region:India

Author(s):Sanjeev

Product Code:KROD9692

November 2024

94

Listen to the audio summary

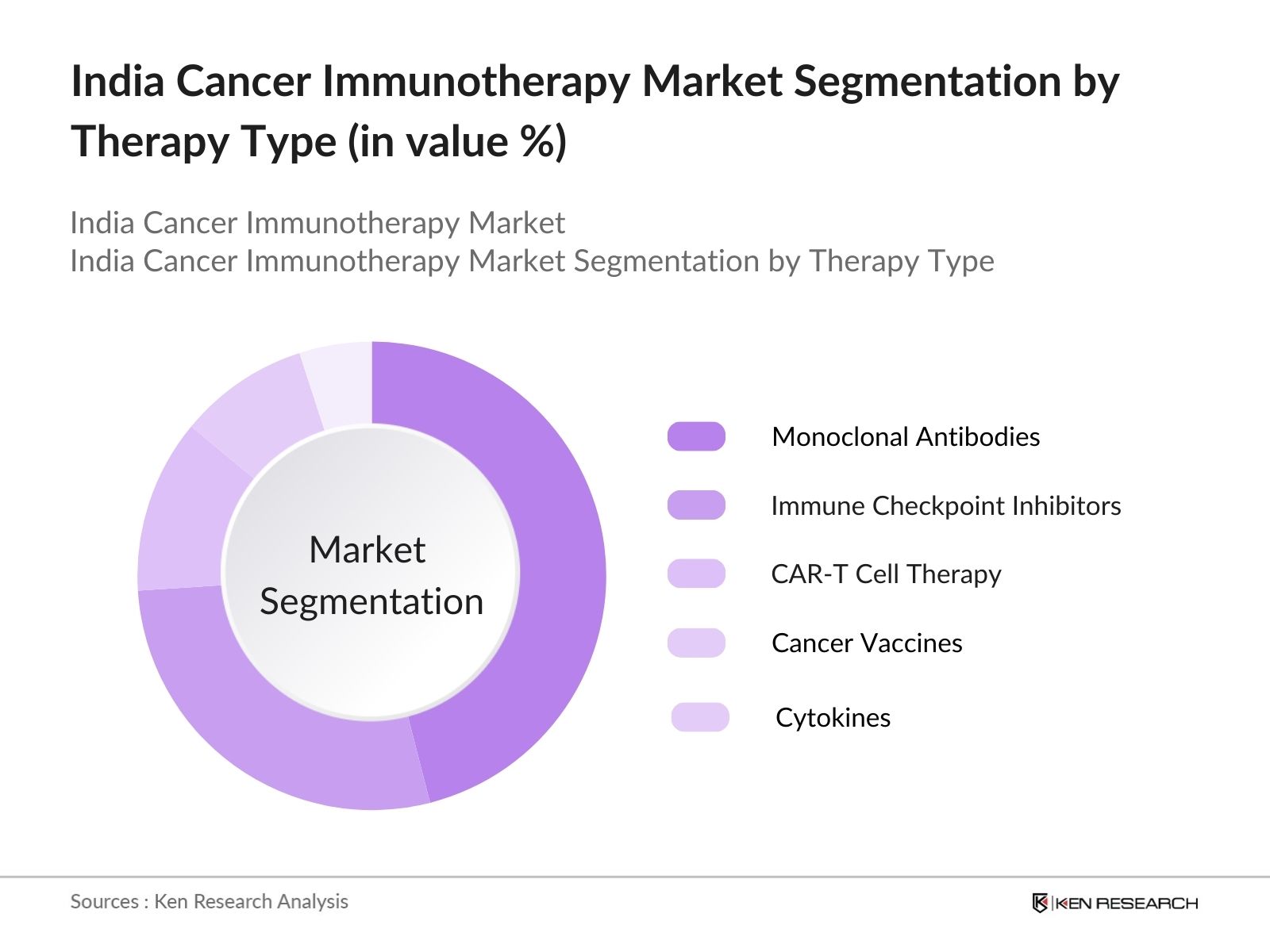

The India Cancer Immunotherapy Market is segmented by therapy type and by therapy type.

The India Cancer Immunotherapy Market is led by multinational corporations and domestic players. Companies such as Bristol-Myers Squibb, Merck, and Roche dominate with robust R&D investments and substantial clinical trials. This concentration highlights their influence due to expertise in oncology and advanced distribution networks.

The India Cancer Immunotherapy Market is projected to experience substantial growth due to increasing awareness and demand for targeted cancer therapies. Technological advancements, particularly in biologics, and government support for healthcare initiatives are expected to accelerate market expansion. Additionally, collaborations between multinational pharmaceutical companies and Indian institutions will support local production, improving accessibility and reducing costs for Indian patients.

|

Monoclonal Antibodies Immune Checkpoint Inhibitors CAR-T Cell Therapy Cancer Vaccines Cytokines |

|

|

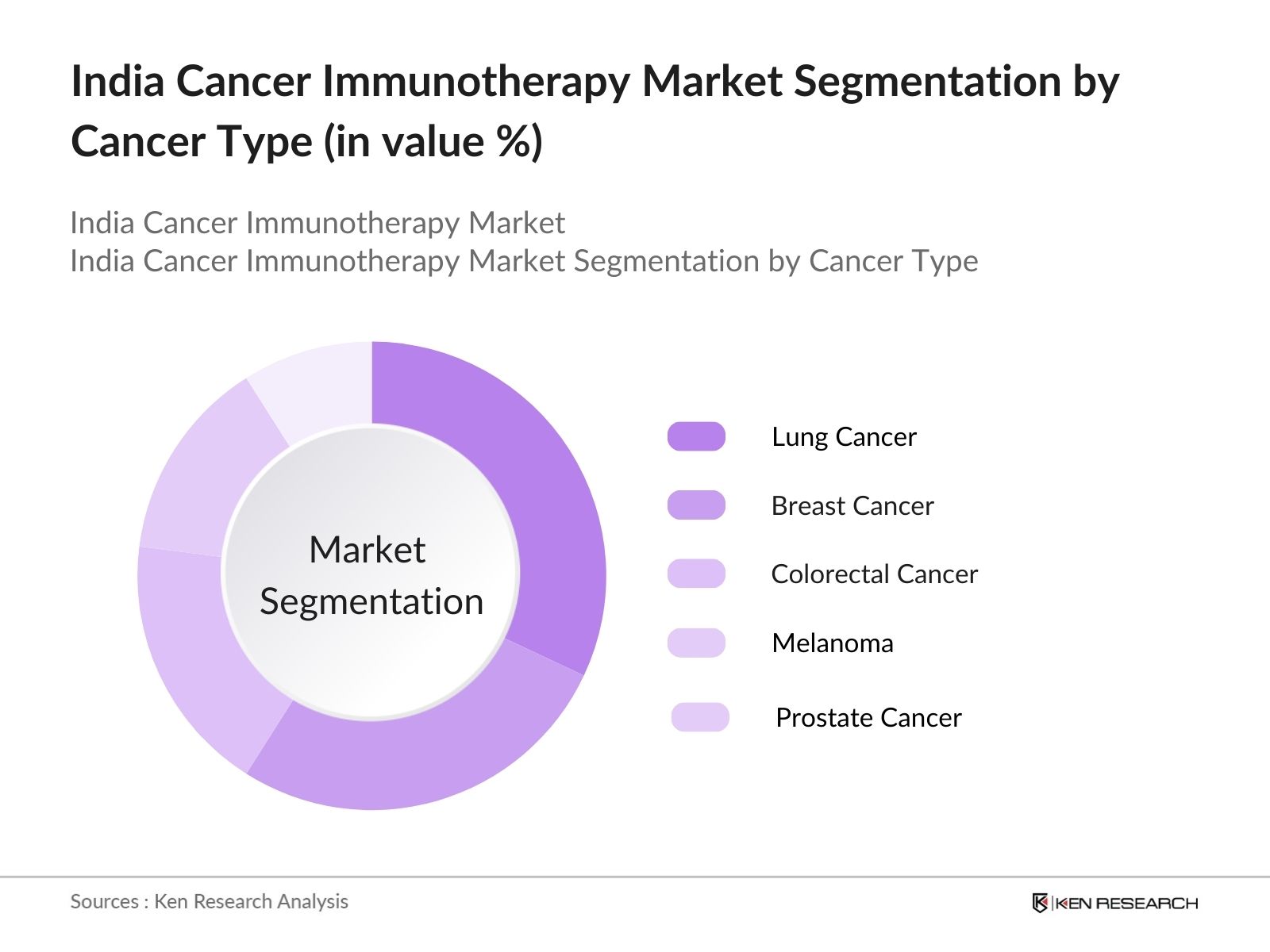

By Cancer Type |

Lung Cancer Breast Cancer Colorectal Cancer Melanoma Prostate Cancer |

|

By Distribution Channel |

Hospitals Cancer Treatment Centers Research Institutes Specialized Clinics |

|

By Administration Mode |

Intravenous Subcutaneous Oral Intramuscular |

|

By Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rise in Cancer Incidence

3.1.2. Increasing Adoption of Immuno-Oncology

3.1.3. Government Healthcare Initiatives

3.1.4. Expansion of Clinical Trials and R&D Investments

3.2. Market Challenges

3.2.1. High Cost of Immunotherapy Treatment

3.2.2. Limited Access to Specialized Healthcare

3.2.3. Regulatory Approval Constraints

3.3. Opportunities

3.3.1. Technological Advancements in Cancer Immunotherapy

3.3.2. Expanding Patient Population Eligible for Immunotherapy

3.3.3. Collaborations with International Pharma Companies

3.4. Trends

3.4.1. Precision Medicine and Personalized Immunotherapy

3.4.2. Rise in Monoclonal Antibodies Usage

3.4.3. Development of Immune Checkpoint Inhibitors

3.4.4. Immunotherapy in Combination with Chemotherapy

3.5. Government Regulation

3.5.1. National Cancer Control Programs

3.5.2. Drug Approval Pathways for Biologics

3.5.3. Price Control Measures for Cancer Treatments

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Therapy Type (in Value %)

4.1.1. Monoclonal Antibodies

4.1.2. Immune Checkpoint Inhibitors

4.1.3. CAR-T Cell Therapy

4.1.4. Cancer Vaccines

4.1.5. Cytokines

4.2. By Cancer Type (in Value %)

4.2.1. Lung Cancer

4.2.2. Breast Cancer

4.2.3. Colorectal Cancer

4.2.4. Melanoma

4.2.5. Prostate Cancer

4.3. By Distribution Channel (in Value %)

4.3.1. Hospitals

4.3.2. Cancer Treatment Centers

4.3.3. Research Institutes

4.3.4. Specialized Clinics

4.4. By Region (in Value %)

4.4.1. North

4.4.2. South

4.4.3. East

4.4.4. West

4.5. By Administration Mode (in Value %)

4.5.1. Intravenous

4.5.2. Subcutaneous

4.5.3. Oral

4.5.4. Intramuscular

5.1. Detailed Profiles of Major Companies

5.1.1. Bristol-Myers Squibb

5.1.2. Merck & Co.

5.1.3. Roche Holding AG

5.1.4. Novartis International AG

5.1.5. Pfizer Inc.

5.1.6. AstraZeneca

5.1.7. GlaxoSmithKline

5.1.8. Amgen Inc.

5.1.9. Takeda Pharmaceutical

5.1.10. Eli Lilly and Company

5.1.11. Gilead Sciences

5.1.12. Sanofi

5.1.13. Incyte Corporation

5.1.14. Exelixis Inc.

5.1.15. Astellas Pharma Inc.

5.2. Cross Comparison Parameters (Product Portfolio, Clinical Trials, Regulatory Approvals, Strategic Partnerships, R&D Investment, Regional Presence, Oncology Expertise, Revenue from Immunotherapy)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Drug Approval Pathways

6.2. Biologics Certification Standards

6.3. Clinical Trial Regulations

6.4. Import and Export Regulations for Biologics

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Therapy Type (in Value %)

8.2. By Cancer Type (in Value %)

8.3. By Distribution Channel (in Value %)

8.4. By Region (in Value %)

8.5. By Administration Mode (in Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

In the initial stage, we mapped the India Cancer Immunotherapy Market ecosystem by analyzing regulatory influences, competitive dynamics, and technological advancements to define critical variables affecting market growth.

This phase involved gathering historical data on market size and growth trends, evaluating immunotherapy adoption rates, and analyzing revenue contributions across cancer types.

Market hypotheses were validated through CATI (computer-assisted telephone interviews) with oncologists and industry specialists, ensuring accuracy and depth in treatment trends and regional challenges.

The final synthesis included direct consultations with key stakeholders, refining our data insights for strategic accuracy. This thorough process delivers a complete analysis for decision-makers in the India Cancer Immunotherapy Market.

The India Cancer Immunotherapy Market is valued at USD 2.4 billion, fueled by rising cancer incidences and increasing adoption of immunotherapy as a treatment option.

Key challenges include the high cost of immunotherapies, limited availability in rural areas, and regulatory hurdles associated with new biologics and treatment protocols.

Leading companies in the market include Bristol-Myers Squibb, Merck, Roche, Novartis, and Pfizer, which dominate due to robust product portfolios and R&D investments.

Major drivers include a high cancer burden, increasing government investment in healthcare, and a shift towards targeted cancer therapies with fewer side effects.

Maharashtra, Karnataka, and Tamil Nadu are key regions due to well-established healthcare infrastructure, a high concentration of cancer treatment facilities, and active research institutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.