India Cardiovascular Devices Market Outlook to 2030

Region:India

Author(s):Paribhasha Tiwari

Product Code:KROD2575

Region:India

Author(s):Paribhasha Tiwari

Product Code:KROD2575

October 2024

91

Listen to the audio summary

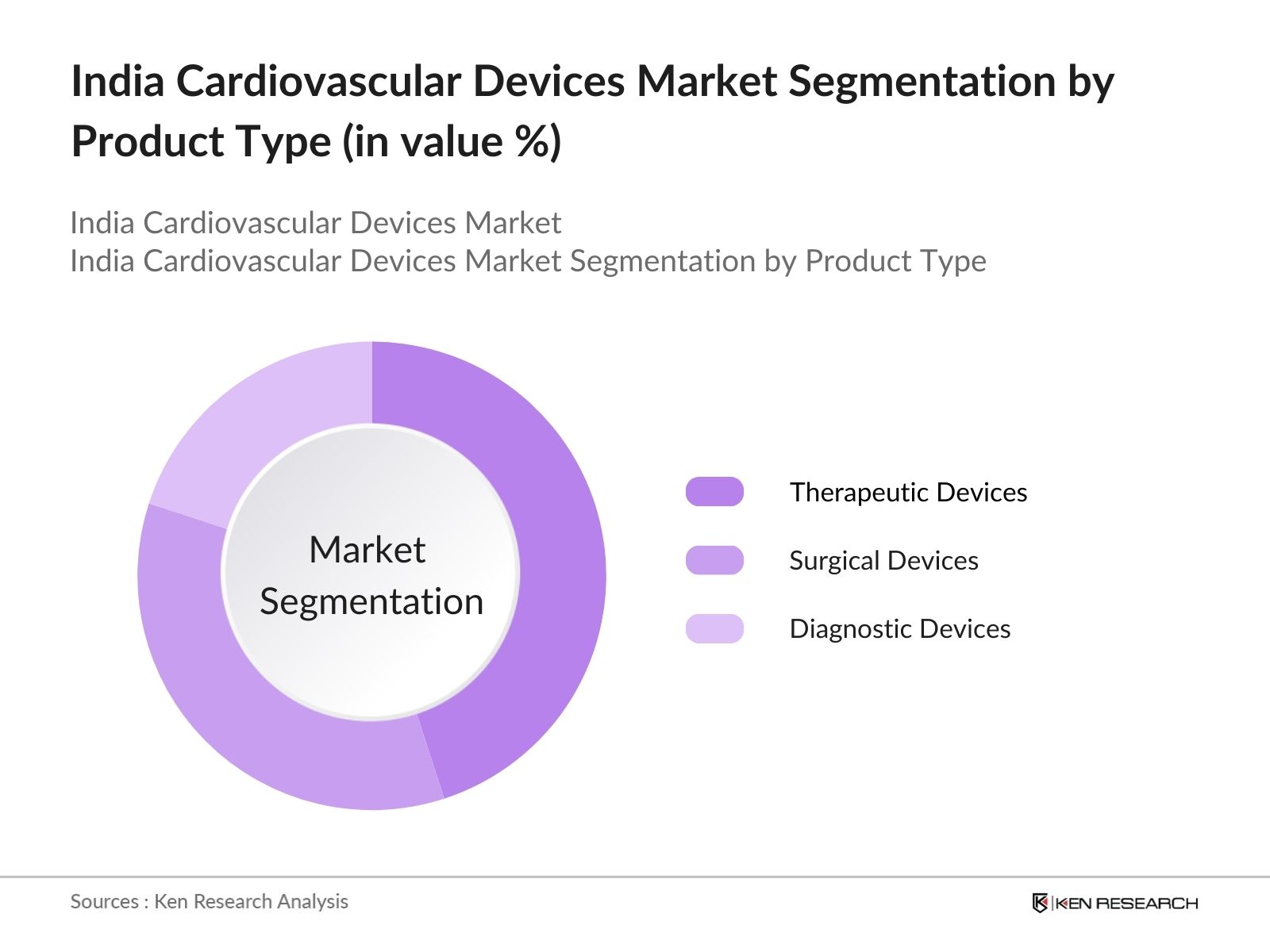

By Product Type: The India cardiovascular devices market is segmented by product type into diagnostic and monitoring devices, surgical devices, and therapeutic devices. In 2023, therapeutic devices held the dominant market share due to their widespread use in treating critical cardiovascular conditions. The increasing demand for products like pacemakers, stents, and defibrillators is driven by advancements in minimally invasive surgery techniques and a growing preference for efficient post-operative recovery options.

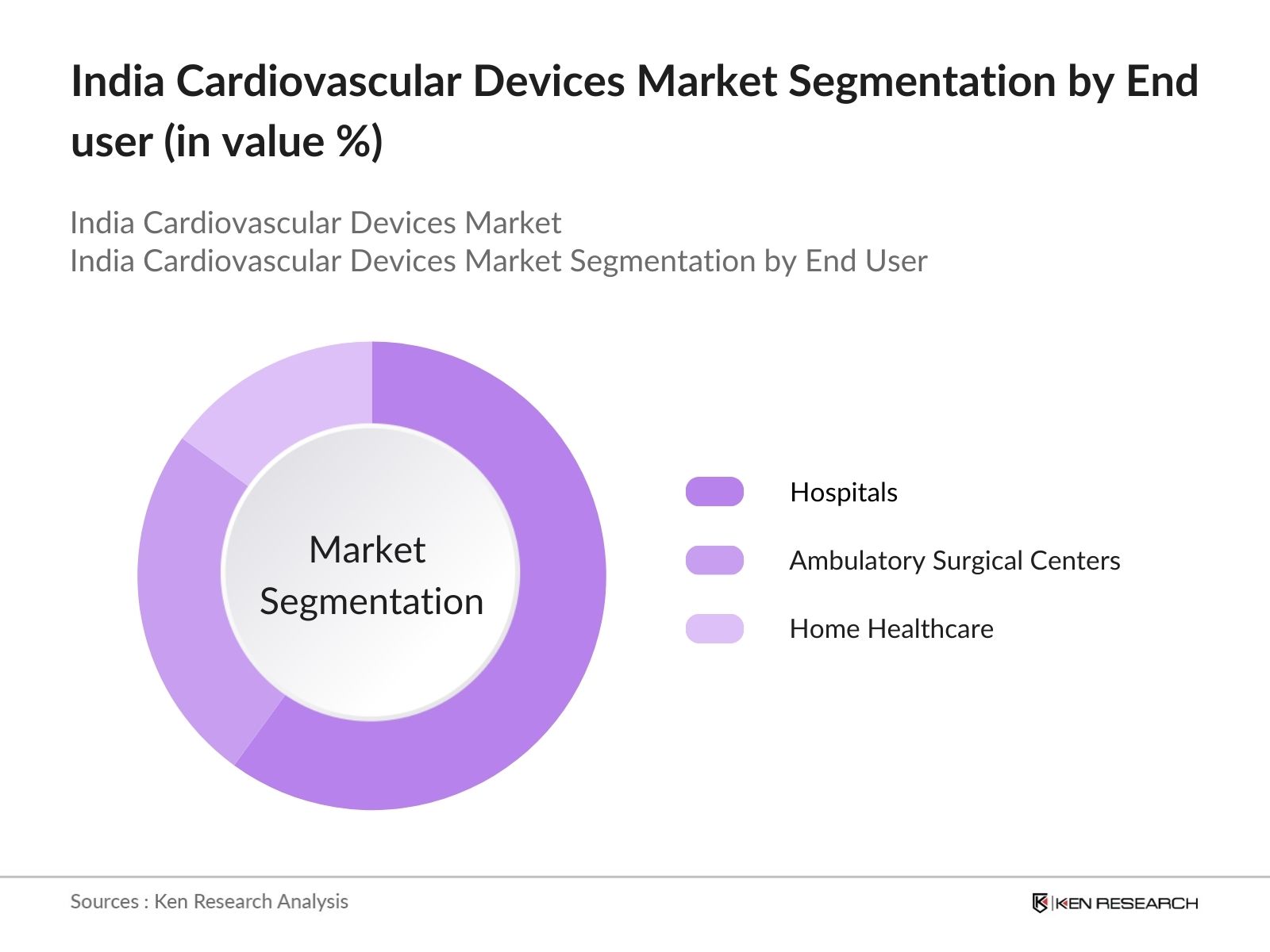

By End-User: The market is segmented into hospitals, ambulatory surgical centers, and home healthcare. Hospitals held the highest market share in 2023 due to their advanced infrastructure, specialized healthcare professionals, and high patient turnover. Major government and private hospitals, particularly in metro cities, have heavily invested in sophisticated cardiovascular treatment equipment, leading to the segment's dominance.

By Region: The India cardiovascular devices market is segmented into North, South, East, and West. The northern region holds the largest market share in 2023 due to the presence of top-tier hospitals and the high disposable income of the population. Government schemes and private insurance coverage have also improved access to advanced cardiovascular treatments in the region.

|

Company |

Year Established |

Headquarters |

|---|---|---|

|

Medtronic |

1949 |

Dublin, Ireland |

|

Abbott Laboratories |

1888 |

Chicago, USA |

|

Boston Scientific Corporation |

1979 |

Marlborough, USA |

|

GE Healthcare |

1892 |

Chicago, USA |

|

Johnson & Johnson |

1886 |

New Jersey, USA |

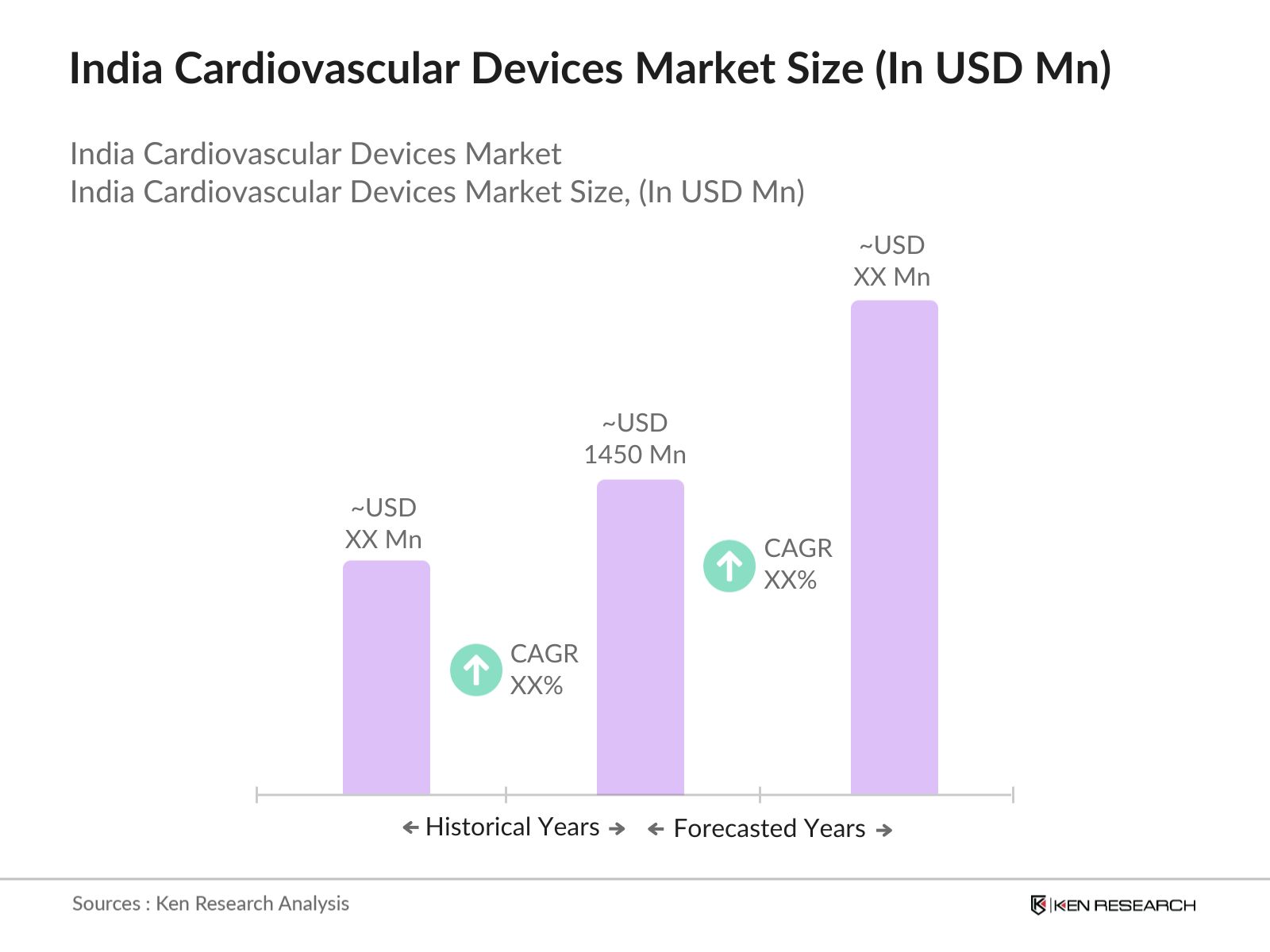

The India Cardiovascular Devices Market is projected to grow exponentially in future. This growth will be driven by rising cardiovascular disease incidence, increased government healthcare spending and growing elderly population.

Growing Demand for Wearable Cardiac Monitoring Devices: Over the next five years, the market for wearable cardiac monitoring devices in India is expected to grow rapidly. According to a report by the Ministry of Health, these devices will play a key role in preventive healthcare by offering real-time monitoring for patients at risk of cardiovascular diseases. The Indian government is likely to introduce incentives for domestic manufacturers to produce these devices, aiming to reduce the overall healthcare burden.

|

By Product Type |

Diagnostic and monitoring devices Surgical devices Therapeutic devices |

|

By End-User Type |

Hospitals Ambulatory surgical centers Home healthcare |

|

By Region |

North South East West |

1.1. Definition and Scope

1.2. Market Structure & Dynamics

1.3. Market Taxonomy

1.4. Market Growth Rate (Financial Metrics: Y-o-Y Growth Analysis)

1.5. Market Segmentation Overview

2.1. Historical Market Size (Financial Parameters)

2.2. Market Growth Analysis (Operational Parameters)

2.3. Key Developments and Milestones (Notable Events and Investments)

2.4. Year-on-Year Growth

2.5. Drivers and Restraints Impact on Market Size

3.1. Key Growth Drivers

3.1.1. Rising Cardiovascular Disease Incidence

3.1.2. Increased Government Healthcare Spending

3.1.3. Growing Elderly Population

3.2. Challenges

3.2.1. High Costs of Advanced Cardiovascular Devices

3.2.2. Shortage of Trained Cardiac Surgeons

3.2.3. Regulatory Delays in Device Approvals

3.3. Opportunities

3.3.1. Growing Demand for Wearable Monitoring Devices

3.3.2. Expansion in Tier 2 and Tier 3 Cities (Infrastructure Development)

3.3.3. Government Initiatives Promoting Local Device Manufacturing

3.4. Trends

3.4.1. AI and Machine Learning in Cardiac Care

3.4.2. Remote Monitoring and Telecardiology Growth

3.4.3. Public-Private Partnerships in Healthcare Expansion

3.5. SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.6. Stakeholder Ecosystem (Healthcare Providers, Device Manufacturers, Distributors)

4.1. By Product Type (Market Share % of Sub-segments)

4.1.1. Diagnostic and Monitoring Devices (ECG, Holter Monitors, Event Monitors)

4.1.2. Surgical Devices (Stents, Catheters, Valves)

4.1.3. Therapeutic Devices (Pacemakers, Defibrillators)

4.2. By End-User (Hospitals, Home Care, Ambulatory Surgical Centers)

4.2.1. Hospitals (Multi-specialty, Cardiac Centers)

4.2.2. Home Healthcare (Remote Monitoring, Post-Surgery Care)

4.2.3. Ambulatory Surgical Centers (Cardiac Procedures)

4.3. By Region (Market Share % for Sub-segments)

4.3.1. North (Delhi NCR, Chandigarh)

4.3.2. South (Bengaluru, Chennai, Hyderabad)

4.3.3. East (Kolkata, Bhubaneswar)

4.3.4. West (Mumbai, Pune, Ahmedabad)

5. India Cardiovascular Devices Market Cross-Comparison

5.1. Detailed Profiles of Major Players (Operational and Financial Metrics)

5.1.1. Medtronic

5.1.2. Abbott Laboratories

5.1.3. Boston Scientific Corporation

5.1.4. GE Healthcare

5.1.5. Johnson & Johnson

5.1.6. Siemens Healthineers

5.1.7. Philips Healthcare

5.1.8. Wipro GE Healthcare

5.1.9. Tata Group (Healthcare Division)

5.1.10. Terumo Corporation

5.1.11. B. Braun Melsungen

5.1.12. Stryker Corporation

5.1.13. Biotronik

5.1.14. Nihon Kohden

5.1.15. Dräger

5.2. Cross-Comparison Parameters (Revenue, Number of Employees, R&D Investments)

5.3. Competitive Landscape (Strategies, Market Shares, Brand Presence)

5.4. Company-Specific Developments (Product Launches, Partnerships, M&A)

6.1. Market Share Analysis (Leading Players and New Entrants)

6.2. Strategic Initiatives (Partnerships, Collaborations, Product Launches)

6.3. Mergers and Acquisitions (Noteworthy Transactions in Cardiovascular Devices)

6.4. Investment Analysis (Government Grants, Venture Capital, PE Investment)

7.1. Regulatory Bodies and Certifications (CDSCO, FSSAI)

7.2. Compliance Standards for Cardiovascular Devices (Safety, Quality Control)

7.3. Import and Export Regulations (Tariffs, Incentives for Local Manufacturing)

7.4. Domestic Manufacturing Policies (PLI Scheme, Aatmanirbhar Bharat)

8.1. Future Market Size Projections (Growth Trajectory Based on Macroeconomic Indicators)

8.2. Key Factors Driving Future Growth (Government Initiatives, Demand Drivers)

8.3. Forecasted Market Growth by Product Type, End-User, and Region

9.1. By Product Type (Market Forecast for Diagnostic, Surgical, Therapeutic Devices)

9.2. By End-User (Hospitals, Home Care, Surgical Centers – Projections)

9.3. By Technology (Invasive, Non-Invasive – Future Trends)

9.4. By Device Type (Market Outlook for Implants, External Devices)

9.5. By Region (North, South, East, West – Growth Projections)

10.1. TAM/SAM/SOM Analysis (Total Addressable, Serviceable Available, Serviceable Obtainable Market)

10.2. Customer Segment Analysis (Key User Profiles, Decision-Making Insights)

10.3. Marketing Initiatives (Targeting Strategies, Growth Opportunities)

10.4. White Space Analysis (Opportunities for Expansion)

10.5. Actionable Insights for Investors, Manufacturers, and Healthcare Providers

The India cardiovascular devices market was valued at USD 1450 million in 2023, driven by a rise in cardiovascular diseases, increasing healthcare spending, and the growing elderly population.

Challenges include the high cost of advanced cardiovascular devices, a shortage of trained cardiologists, and regulatory delays in approving new medical devices. These factors affect the accessibility and adoption of life-saving treatments.

Key players in the market include Medtronic, Abbott Laboratories, Boston Scientific Corporation, GE Healthcare, and Johnson & Johnson. These companies have established a strong presence through partnerships and advanced product offerings.

The market is driven by rising cardiovascular disease incidence, increased government healthcare spending and growing elderly population.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.