India Cereal Market Outlook to 2030

Region:India

Author(s):Shreya Garg

Product Code:KROD3755

Region:India

Author(s):Shreya Garg

Product Code:KROD3755

November 2024

90

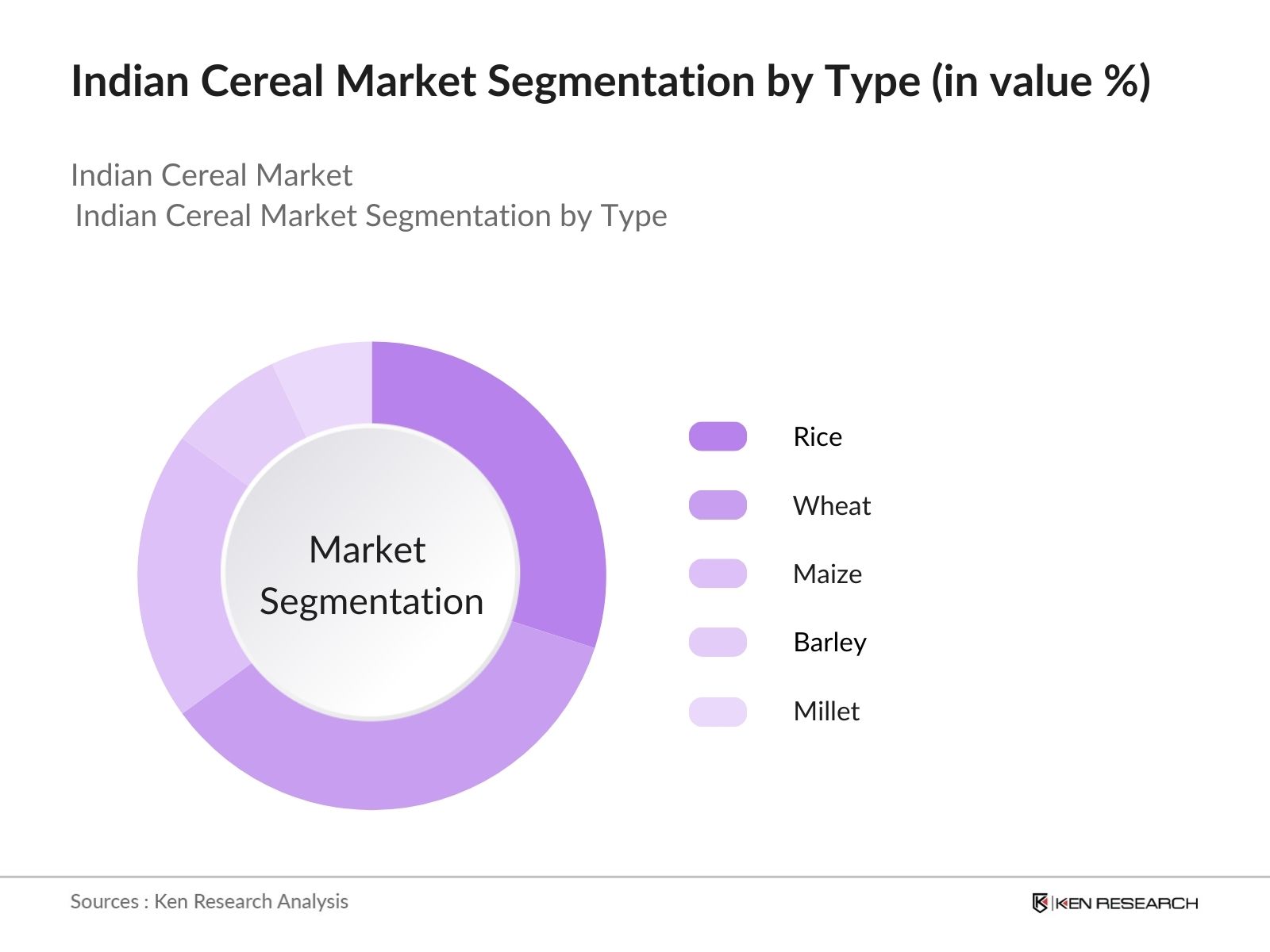

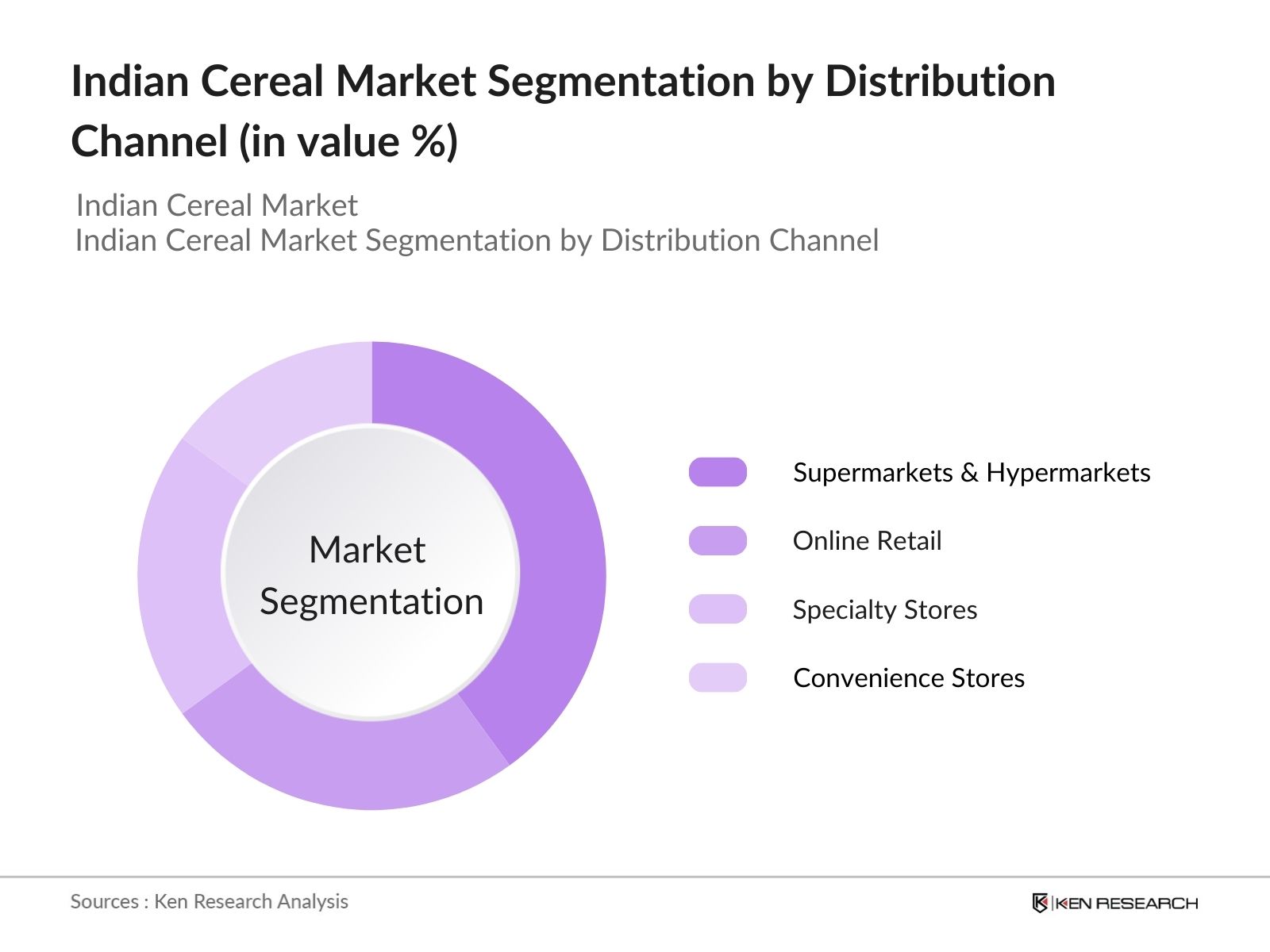

By Type: The market is segmented by type into rice, wheat, maize, barley, and millet. Recently, wheat has gained a dominant market share under the type segmentation, primarily due to its widespread consumption across India as a staple food. Wheat-based products, such as flour, are essential in many Indian diets, and the strong agricultural foundation in key wheat-producing states like Punjab and Uttar Pradesh ensures a steady supply. Additionally, government initiatives supporting wheat production through subsidies have further bolstered its dominance in the market.  By Distribution Channel: The market is also segmented by distribution channels, including supermarkets & hypermarkets, online retail, specialty stores, and convenience stores. Supermarkets and hypermarkets hold a dominant market share, driven by the growing preference for one-stop shopping experiences and the extensive availability of a variety of cereal products. The organized retail sector has expanded rapidly, and with the convenience of packaged and branded cereals available in large quantities, this channel continues to lead the market.

By Distribution Channel: The market is also segmented by distribution channels, including supermarkets & hypermarkets, online retail, specialty stores, and convenience stores. Supermarkets and hypermarkets hold a dominant market share, driven by the growing preference for one-stop shopping experiences and the extensive availability of a variety of cereal products. The organized retail sector has expanded rapidly, and with the convenience of packaged and branded cereals available in large quantities, this channel continues to lead the market.

The Indian cereal market is dominated by both local and global players, with significant consolidation among the major brands. These companies offer a wide range of products catering to different consumer needs, from conventional staples to premium organic cereals. The competitive landscape also reflects the growing focus on innovation in product formulation, with many brands launching health-focused and fortified cereals. The dominance of ITC Limited and Nestl India showcases the strong hold of diversified product portfolios, backed by vast distribution networks and robust marketing strategies.

|

Company |

Establishment Year |

Headquarters |

Product Diversity |

Market Penetration |

Revenue (INR Mn) |

Number of Employees |

Brand Equity |

Pricing Strategy |

Digital Presence |

|

ITC Limited |

1910 |

Kolkata, India |

|||||||

|

Kelloggs India |

1994 |

Mumbai, India |

|||||||

|

Nestl India |

1961 |

Gurgaon, India |

|||||||

|

Patanjali Ayurved |

2006 |

Haridwar, India |

|||||||

|

Britannia Industries |

1892 |

Bengaluru, India |

Over the next five years, the India Cereal Market is expected to continue its growth trajectory driven by increased demand for healthy and nutritious breakfast options, growing consumer awareness about health, and a rise in disposable incomes, especially in urban centers. Additionally, the market will see more innovations with new ingredients, including organic and fortified cereals, catering to the growing health-conscious population.

|

By Type |

Rice Wheat Maize Barley Millet |

|

By Form |

Whole Grain Flakes Powdered Puffed |

|

By Application |

Food Processing Household Animal Feed Export |

|

By Distribution Channel |

Supermarkets Online Specialty Convenience |

|

By Region |

North South East West |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Health Awareness (Consumer Behavior)

3.1.2. Urbanization and Rising Disposable Income (Macroeconomic)

3.1.3. Expansion of Organized Retail (Retail Dynamics)

3.1.4. Demand for Nutritional and Organic Cereals (Consumer Preferences)

3.2. Market Challenges

3.2.1. Fluctuations in Raw Material Costs (Supply Chain)

3.2.2. High Competition from Alternative Foods (Market Penetration)

3.2.3. Seasonality of Crop Production (Agricultural Impact)

3.3. Opportunities

3.3.1. Growth of Online Retailing (E-Commerce)

3.3.2. Technological Advancements in Food Processing (Innovation)

3.3.3. Expansion in Rural Markets (Rural Penetration)

3.4. Trends

3.4.1. Increasing Demand for Gluten-Free Cereals (Health Trends)

3.4.2. Shift Towards Ready-to-Eat Cereals (Convenience Factor)

3.4.3. Sustainability in Cereal Packaging (Environmental Concerns)

3.5. Government Regulation

3.5.1. Agricultural Policies and Subsidies (Policy Impact)

3.5.2. Food Safety and Standards Authority of India (FSSAI) Regulations (Compliance)

3.5.3. Minimum Support Price (MSP) for Cereals (Pricing Impact)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Type (In Value %)

4.1.1. Rice

4.1.2. Wheat

4.1.3. Maize

4.1.4. Barley

4.1.5. Millet

4.2. By Form (In Value %)

4.2.1. Whole Grain

4.2.2. Flakes

4.2.3. Powdered

4.2.4. Puffed

4.3. By Application (In Value %)

4.3.1. Food Processing Industry

4.3.2. Household Consumption

4.3.3. Animal Feed

4.3.4. Export

4.4. By Distribution Channel (In Value %)

4.4.1. Supermarkets & Hypermarkets

4.4.2. Online Retail

4.4.3. Specialty Stores

4.4.4. Convenience Stores

4.5. By Region (In Value %)

4.5.1. North

4.5.2. South

4.5.3. East

4.5.4. West

5.1. Detailed Profiles of Major Companies

5.1.1. ITC Limited

5.1.2. Kelloggs India

5.1.3. Nestl India

5.1.4. Patanjali Ayurved

5.1.5. Britannia Industries

5.1.6. Marico Limited

5.1.7. PepsiCo India

5.1.8. General Mills India

5.1.9. Hindustan Unilever Limited

5.1.10. Parle Agro

5.1.11. Tata Consumer Products

5.1.12. Anmol Industries

5.1.13. MTR Foods

5.1.14. LT Foods

5.1.15. Emami Group

5.2. Cross Comparison Parameters

No. of Employees

Headquarters Location

Market Revenue

Product Portfolio Diversity

Brand Equity

Pricing Strategies

Market Penetration Rate

Consumer Demographics

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Subsidies

5.9. Private Equity Investments

6.1. Food Safety and Standards Regulations

6.2. Agricultural Export Policy

6.3. Compliance Certifications

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Type (In Value %)

8.2. By Form (In Value %)

8.3. By Application (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Segmentation

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase focuses on constructing an ecosystem map encompassing all major stakeholders within the Indian Cereal Market. Extensive desk research, utilizing both secondary and proprietary databases, will be conducted to gather comprehensive industry-level information. The primary goal is to identify and define the critical variables influencing market dynamics.

In this phase, historical data related to the Indian Cereal Market is compiled and analyzed. The assessment includes market penetration, the ratio of producers to distributors, and the resultant revenue generation. Further, service quality statistics are evaluated to ensure reliability and accuracy in revenue estimates.

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts from a diverse array of companies. These consultations will provide valuable operational and financial insights, aiding in the refinement and corroboration of market data.

The final phase involves direct engagement with multiple cereal manufacturers to acquire detailed insights into product segments, sales performance, and consumer preferences. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, ensuring a comprehensive and validated analysis of the Indian Cereal Market.

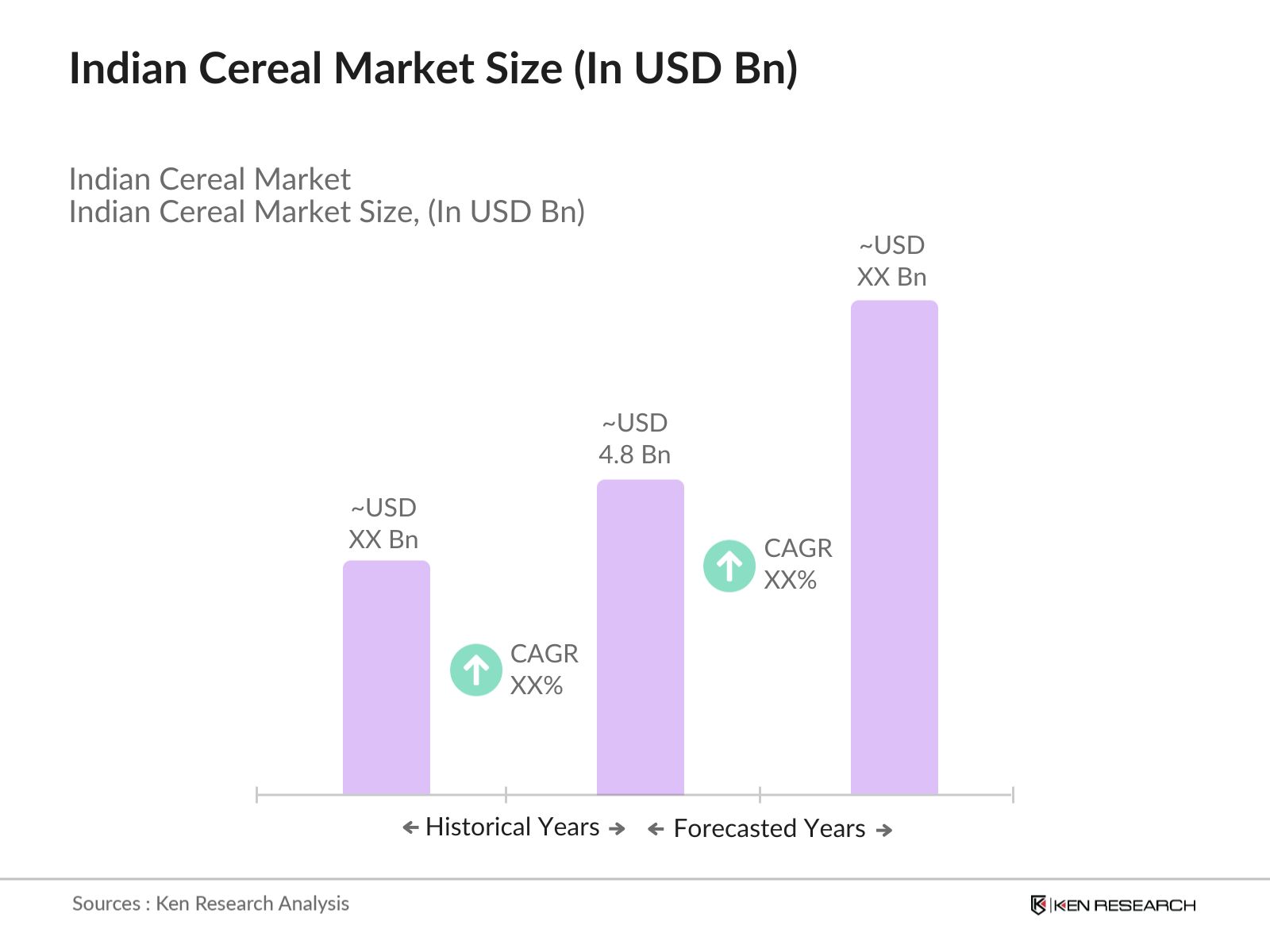

The Indian cereal market is valued at USD 4.8 billion, primarily driven by the rising demand for health-conscious products and organic cereals. The expanding middle-class population and government support have also contributed to this growth.

Challenges in the Indian cereal market includes fluctuating raw material costs, high competition from alternative food products, and the seasonal nature of cereal crop production, which can affect supply consistency.

Major players in the Indian cereal market include ITC Limited, Kelloggs India, Nestl India, Patanjali Ayurved, and Britannia Industries. These companies dominate due to their vast product offerings, strong distribution networks, and well-established brand loyalty.

The Indian cereal market is driven by increasing health awareness, a growing demand for organic and whole-grain cereals, and government initiatives aimed at boosting cereal production. Furthermore, the rise of organized retail and online shopping has facilitated easier access to a wider variety of cereal products.

Over the next five years, the Indian cereal market is expected to grow significantly due to continuous government support, advancements in food technology, and an increasing preference for health-focused and convenience-based cereal products.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.