India Coffee Market Outlook to 2030

Region:India

Author(s):Mukul

Product Code:KROD4462

Region:India

Author(s):Mukul

Product Code:KROD4462

October 2024

98

The India coffee market is dominated by several key players, both domestic and international. Major competitors include brands like Tata Coffee Ltd., Hindustan Unilever (Bru), and Nestl India (Nescaf), which have established a strong market presence through a combination of extensive distribution networks, branding, and product innovation. These companies compete not only in instant and filter coffee but also in the growing premium and specialty coffee segments. The market also sees competition from new-age roasters like Blue Tokai and The Flying Squirrel, who cater to the niche premium market.

|

Company Name |

Establishment Year |

Headquarters |

Production Capacity |

Global Presence |

Distribution Channels |

Product Range |

Sustainability Initiatives |

|

Tata Coffee Ltd. |

1922 |

Bangalore, India |

|||||

|

Hindustan Unilever (Bru) |

1933 |

Mumbai, India |

|||||

|

Nestl India (Nescaf) |

1961 |

Gurugram, India |

|||||

|

Coffee Day Enterprises (CCD) |

1996 |

Bangalore, India |

|||||

|

Blue Tokai Coffee Roasters |

2013 |

New Delhi, India |

Market Growth Drivers

Market Restraints

The India coffee market is expected to witness strong growth driven by increasing coffee consumption, rising caf culture, and expanding e-commerce platforms. The premium and specialty coffee segments are anticipated to grow rapidly, fueled by consumer demand for unique flavors and high-quality coffee beans. Additionally, the coffee processing industry will see technological advancements that could improve yield and sustainability practices in coffee farming, further boosting production.

Market Opportunities

|

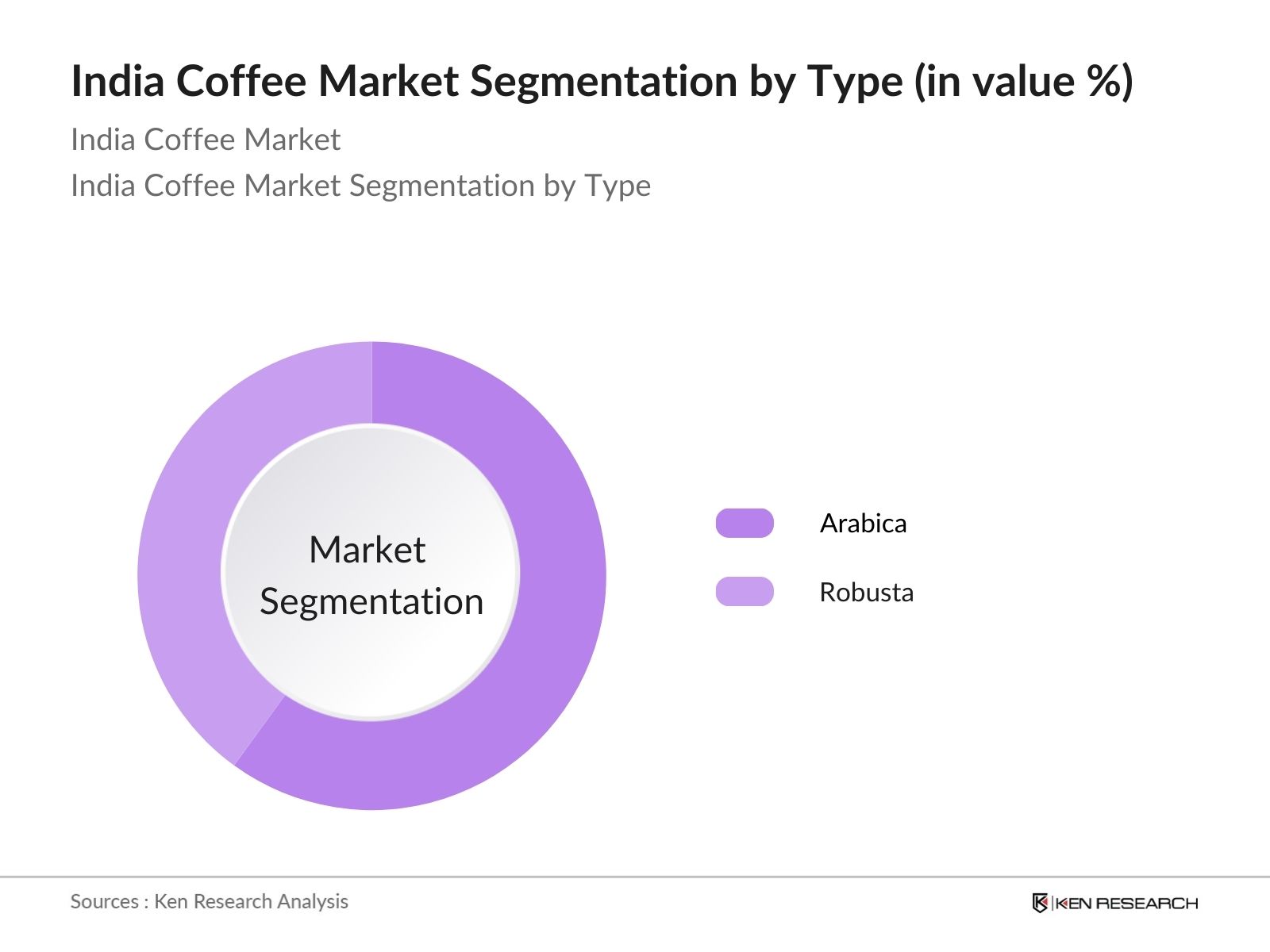

Type |

Arabica, Robusta |

|

Form |

Whole Bean, Ground Coffee, Instant Coffee |

|

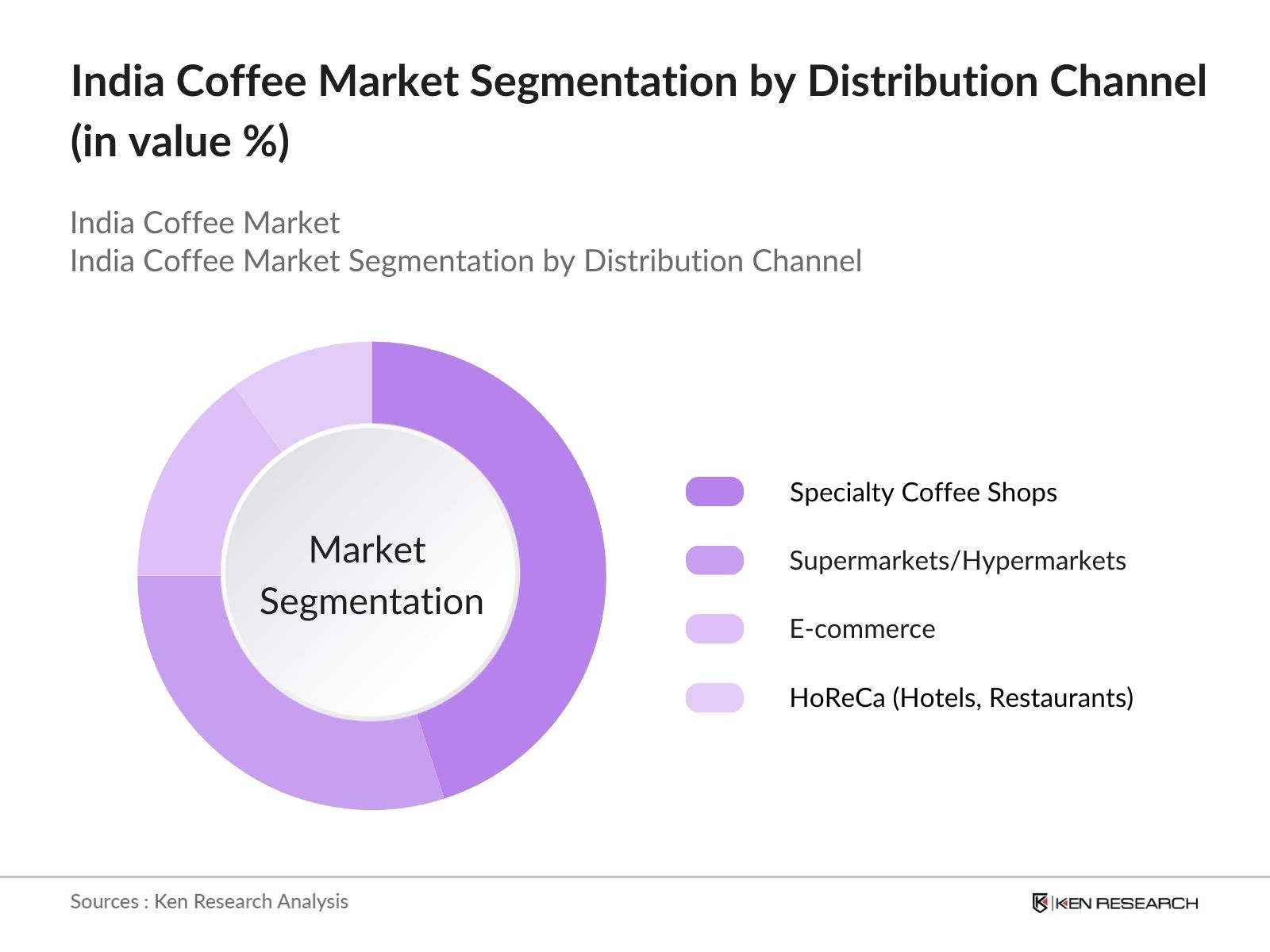

Distribution Channel |

Supermarkets/Hypermarkets, Specialty Coffee Shops, E-Commerce, HoReCa |

|

End-Use |

Commercial, Residential |

|

Region |

Southern India, Northern India, Eastern India, Western India |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate (Domestic Coffee Consumption, Export Volume)

1.4 Market Segmentation Overview (Type, Form, Distribution Channel, End-Use, Region)

2.1 Historical Market Size (Value and Volume)

2.2 Year-On-Year Growth Analysis (Volume Growth, Value Growth)

2.3 Key Market Developments and Milestones (New Production Facilities, Export Agreements)

3.1 Growth Drivers

3.1.1 Increasing Coffee Consumption (Domestic Demand, Specialty Coffee)

3.1.2 Expansion of Coffee Cultivation (Arabica vs Robusta Production)

3.1.3 Rising Exports (Key Export Markets, Coffee Trade Agreements)

3.1.4 Changing Consumer Preferences (Specialty Coffee, Instant Coffee)

3.2 Market Challenges

3.2.1 Impact of Climate Change (Yield Fluctuations, Crop Diseases)

3.2.2 Price Volatility (International Coffee Prices, Exchange Rate Risks)

3.2.3 Labor Shortage in Coffee Plantations

3.3 Opportunities

3.3.1 Growing Domestic Coffee Chains

3.3.2 Expansion of Premium Coffee Segment

3.3.3 Technological Advancements in Coffee Processing (Value Addition)

3.4 Trends

3.4.1 Rise of Coffee Culture in Urban Areas

3.4.2 Organic Coffee Certification Growth

3.4.3 Use of E-commerce for Coffee Sales

3.5 Government Regulations and Policies

3.5.1 Coffee Board of India Initiatives

3.5.2 Export Subsidies and Tax Exemptions

3.5.3 Environmental and Sustainability Standards

3.6 SWOT Analysis (India Coffee Market)

3.7 Stakeholder Ecosystem (Farmers, Coffee Processors, Traders, Retailers)

3.8 Porters Five Forces Analysis

3.9 Competitive Ecosystem

4.1 By Type (In Value and Volume %)

4.1.1 Arabica

4.1.2 Robusta

4.2 By Form (In Value and Volume %)

4.2.1 Whole Bean

4.2.2 Ground Coffee

4.2.3 Instant Coffee

4.3 By Distribution Channel (In Value and Volume %)

4.3.1 Supermarkets/Hypermarkets

4.3.2 Specialty Coffee Shops

4.3.3 E-Commerce

4.3.4 HoReCa (Hotels, Restaurants, Cafes)

4.4 By End-Use (In Value and Volume %)

4.4.1 Commercial

4.4.2 Residential

4.5 By Region (In Value and Volume %)

4.5.1 Southern India

4.5.2 Northern India

4.5.3 Eastern India

4.5.4 Western India

5.1 Detailed Profiles of Major Competitors

5.1.1 Tata Coffee Ltd.

5.1.2 Hindustan Unilever Ltd. (Bru)

5.1.3 Nestl India Ltd. (Nescaf)

5.1.4 Coffee Day Enterprises Ltd. (Caf Coffee Day)

5.1.5 Tata Starbucks Private Ltd.

5.1.6 Levista Coffee

5.1.7 Blue Tokai Coffee Roasters

5.1.8 The Flying Squirrel Coffee

5.1.9 Koinonia Coffee Roasters

5.1.10 Continental Coffee Ltd.

5.1.11 ITC Ltd. (Sunbean)

5.1.12 Indian Coffee House

5.1.13 Narasus Coffee Company

5.1.14 Halli Berri

5.1.15 Seven Beans Coffee Company

5.2 Cross Comparison Parameters (Production Volume, Market Share, Revenue, Market Presence, Processing Facilities, Sustainability Initiatives, Distribution Network, Product Range)

5.3 Market Share Analysis (Arabica vs Robusta, Branded vs Non-branded)

5.4 Strategic Initiatives

5.4.1 Product Launches

5.4.2 Market Expansion

5.4.3 Sustainability Initiatives

5.5 Mergers And Acquisitions (Domestic and International Acquisitions)

5.6 Investment Analysis

5.7 Venture Capital Funding in Specialty Coffee Segment

5.8 Government Grants for Coffee Plantations and Exports

5.9 Private Equity Investments in Coffee Startups

6.1 Coffee Certification and Licensing Requirements

6.2 Export Regulations and Compliance (Including FSSAI, APEDA Guidelines)

6.3 Environmental Standards for Sustainable Coffee Cultivation

7.1 Future Market Size Projections (Export and Domestic Consumption Growth)

7.2 Key Factors Driving Future Market Growth (Technological Adoption, Consumer Preferences)

8.1 By Type (In Value and Volume %)

8.2 By Form (In Value and Volume %)

8.3 By Distribution Channel (In Value and Volume %)

8.4 By End-Use (In Value and Volume %)

8.5 By Region (In Value and Volume %)

9.1 TAM/SAM/SOM Analysis (Total Addressable Market, Serviceable Available Market, Serviceable Obtainable Market)

9.2 Customer Cohort Analysis (Age Demographics, Coffee Preferences)

9.3 Marketing Initiatives for Premium Coffee Brands

9.4 White Space Opportunity Analysis (New Market Segments, Untapped Regions)

The initial phase involves constructing an ecosystem map covering all stakeholders in the India coffee market. This includes key producers, exporters, retailers, and end-consumers. Data is gathered from secondary sources and government reports to identify critical market drivers such as demand, pricing, and production.

In this step, historical data from 2018-2023 is analyzed to understand coffee production, export trends, and domestic consumption. Additionally, market penetration of various coffee types (Arabica, Robusta) is assessed.

Industry experts, including plantation owners and coffee chain operators, are consulted through interviews and surveys to validate the market hypotheses. Their insights provide a deeper understanding of market trends, challenges, and opportunities.

In the final phase, findings from all the previous steps are synthesized to provide a comprehensive view of the India coffee market. This includes cross-referencing with government data to ensure accuracy.

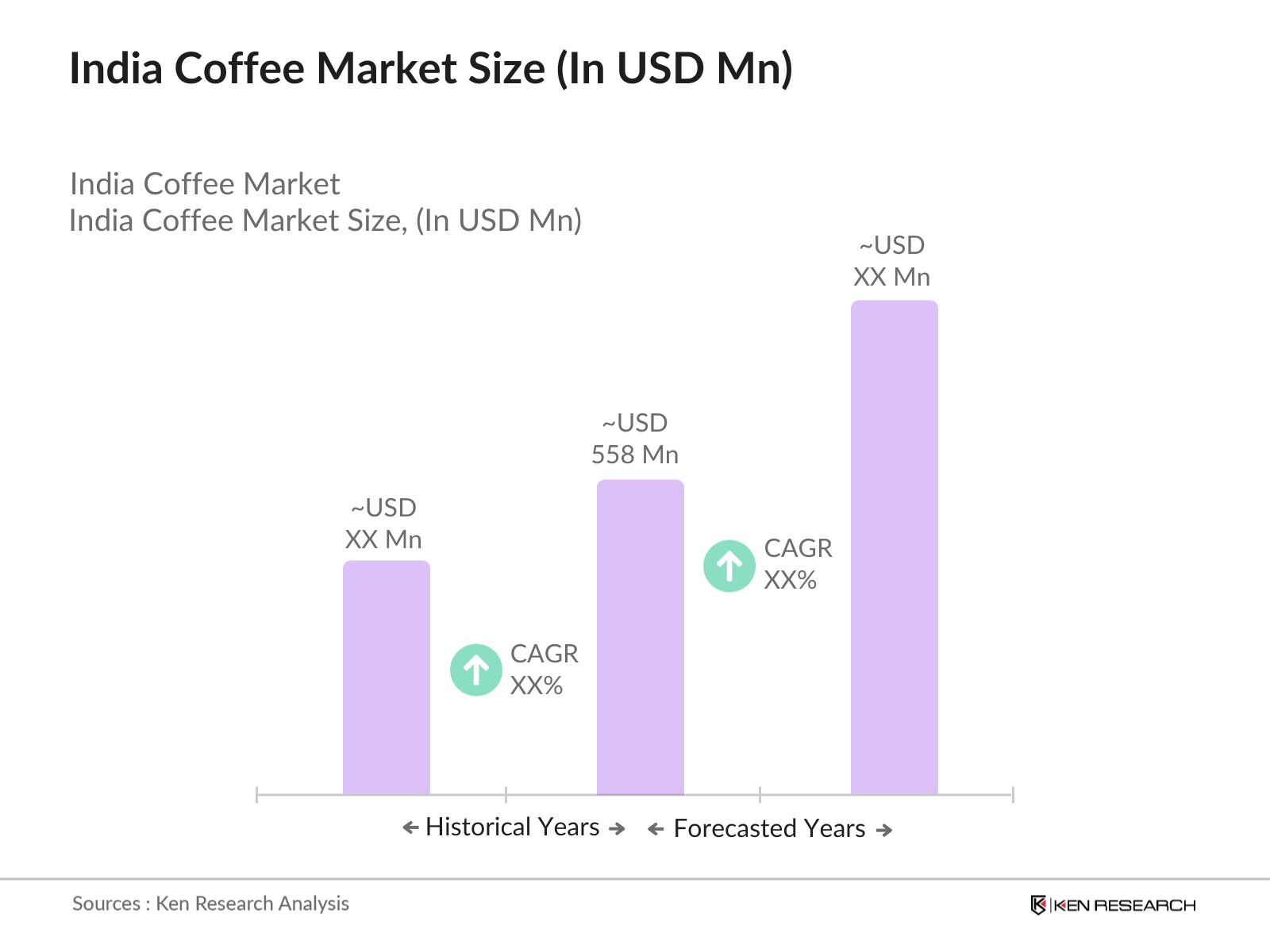

The India coffee market is valued at USD 558 million, driven by increasing coffee consumption, expanding caf culture, and a growing preference for premium coffee brands.

Challenges in the India coffee market include fluctuating coffee prices due to international market conditions, labor shortages, and climate-related issues affecting yield and quality.

Key players in the market include Tata Coffee Ltd., Hindustan Unilever Ltd. (Bru), Nestl India Ltd. (Nescaf), Coffee Day Enterprises Ltd., and Blue Tokai Coffee Roasters, each leveraging strong distribution networks and brand loyalty.

The market is propelled by increasing consumer preference for coffee over tea, rising disposable incomes, and the growth of specialty coffee consumption in urban areas, particularly among millennials.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.