India Computer Storage Devices and Servers Market Outlook to 2030

Region:Asia

Author(s):Paribhasha Tiwari

Product Code:KROD10853

December 2024

87

About the Report

India Computer Storage Devices and Servers Market Overview

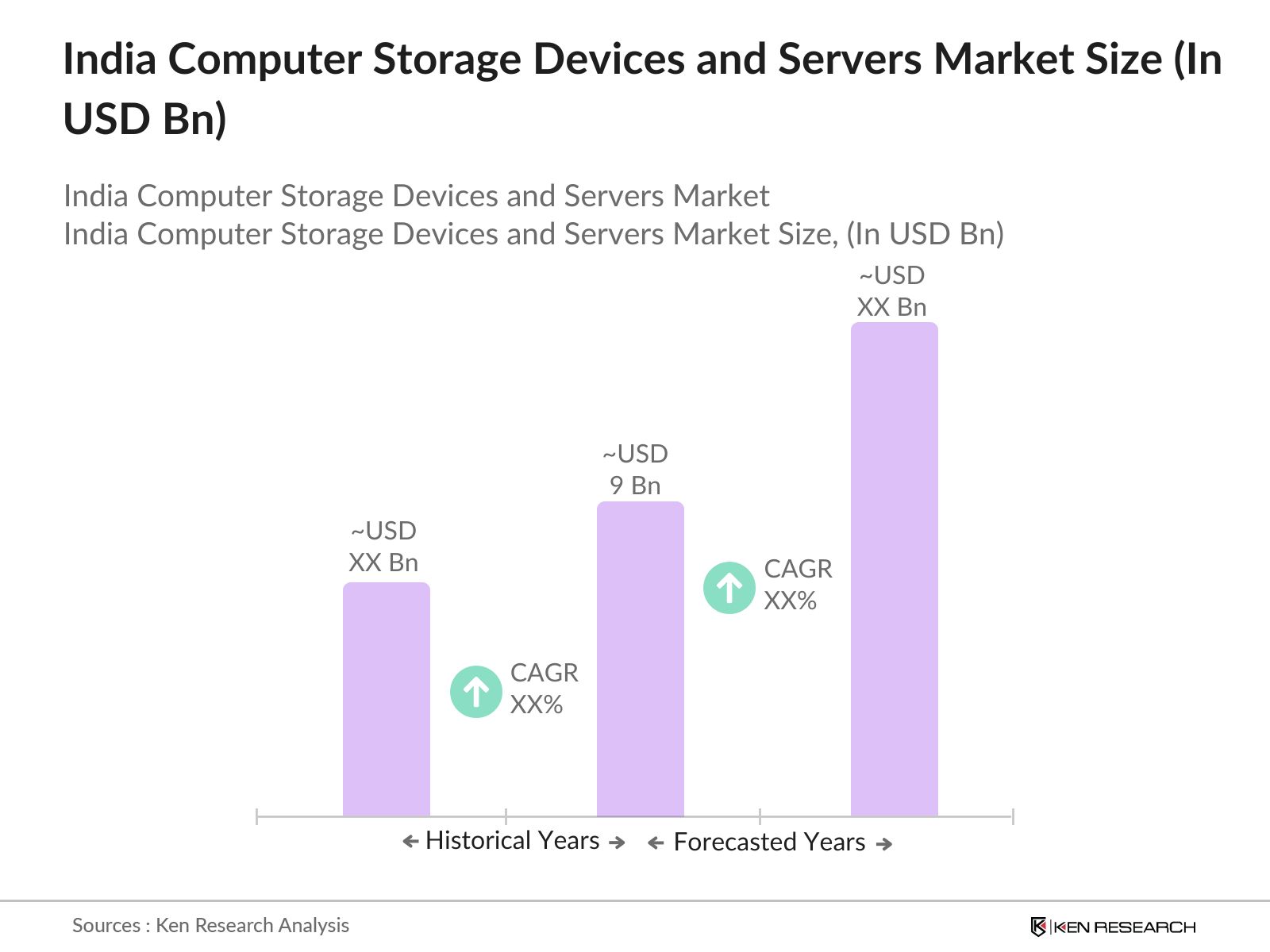

- The India computer storage devices and servers market is experiencing significant growth, driven by the rapid digitization across various sectors and the increasing adoption of cloud computing. The market was valued at USD 9 billion, reflecting a compound annual growth rate (CAGR) of 12.56% over the past five years.This expansion is attributed to the surge in data generation, necessitating advanced storage solutions and robust server infrastructures.

- Major metropolitan areas such as Mumbai, Bengaluru, and Hyderabad dominate the market due to their status as IT hubs, housing numerous data centers and technology firms. These cities offer robust infrastructure, skilled labor, and favorable government policies, making them attractive destinations for investments in storage and server technologies.

- In the India computer storage devices and servers market, there has been a notable 22% year-over-year increase in shipments during the first quarter of 2024, primarily driven by the consumer storage segment. The flash drive market now accounts for 62% of the overall consumer storage market, with MicroSD card shipments experiencing an impressive 60% growth year-over-year and SD cards seeing a 7% increase.

India Computer Storage Devices and Servers Market Segmentation

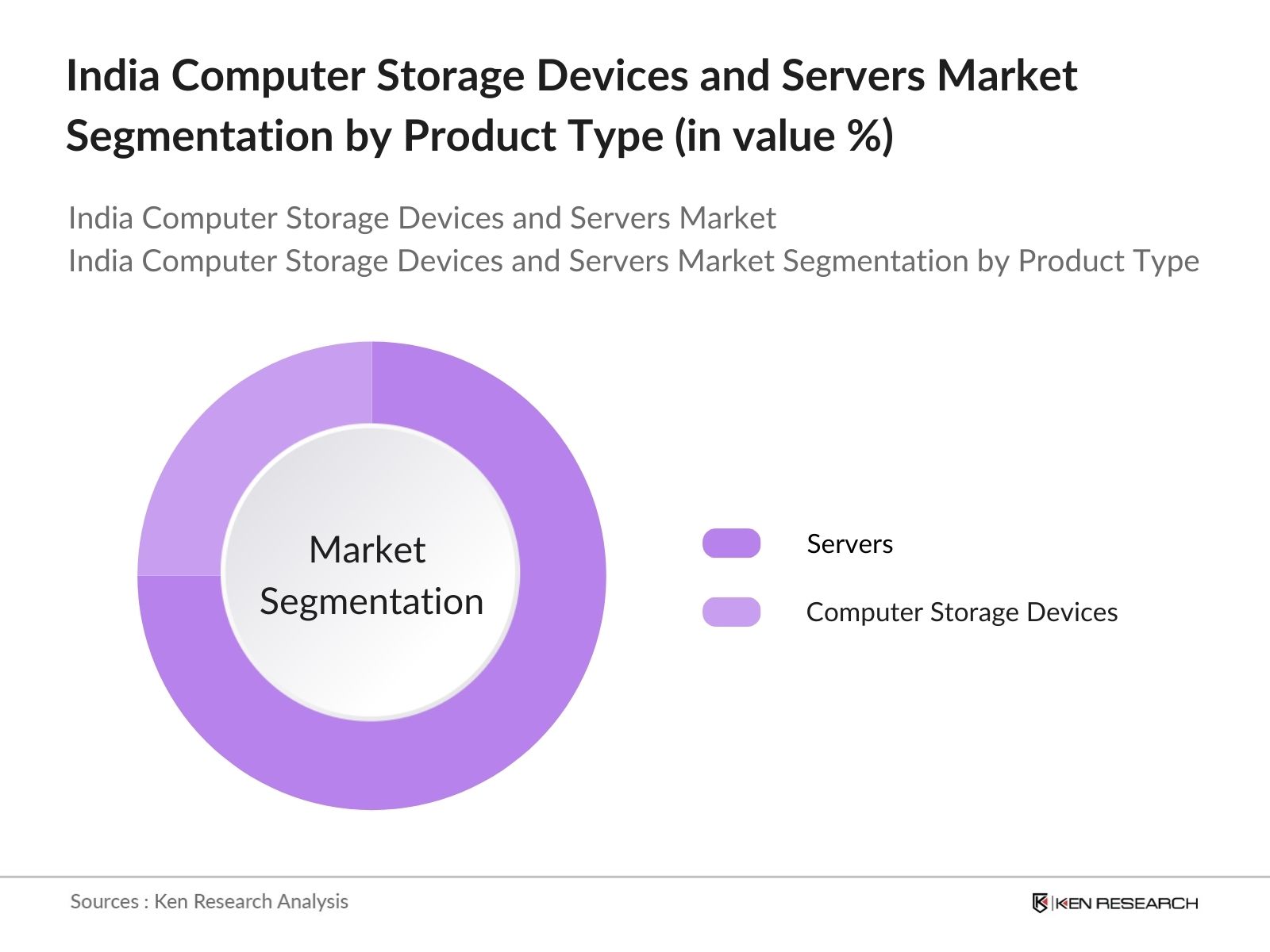

By Product Type: The India computer storage devices and servers market is segmented by product type into servers and computer storage devices. Servers hold a dominant market share within this segmentation, primarily due to the escalating demand for data centers and cloud services. The proliferation of internet usage and the surge in digital transactions have necessitated robust server infrastructures to manage and process vast amounts of data efficiently.

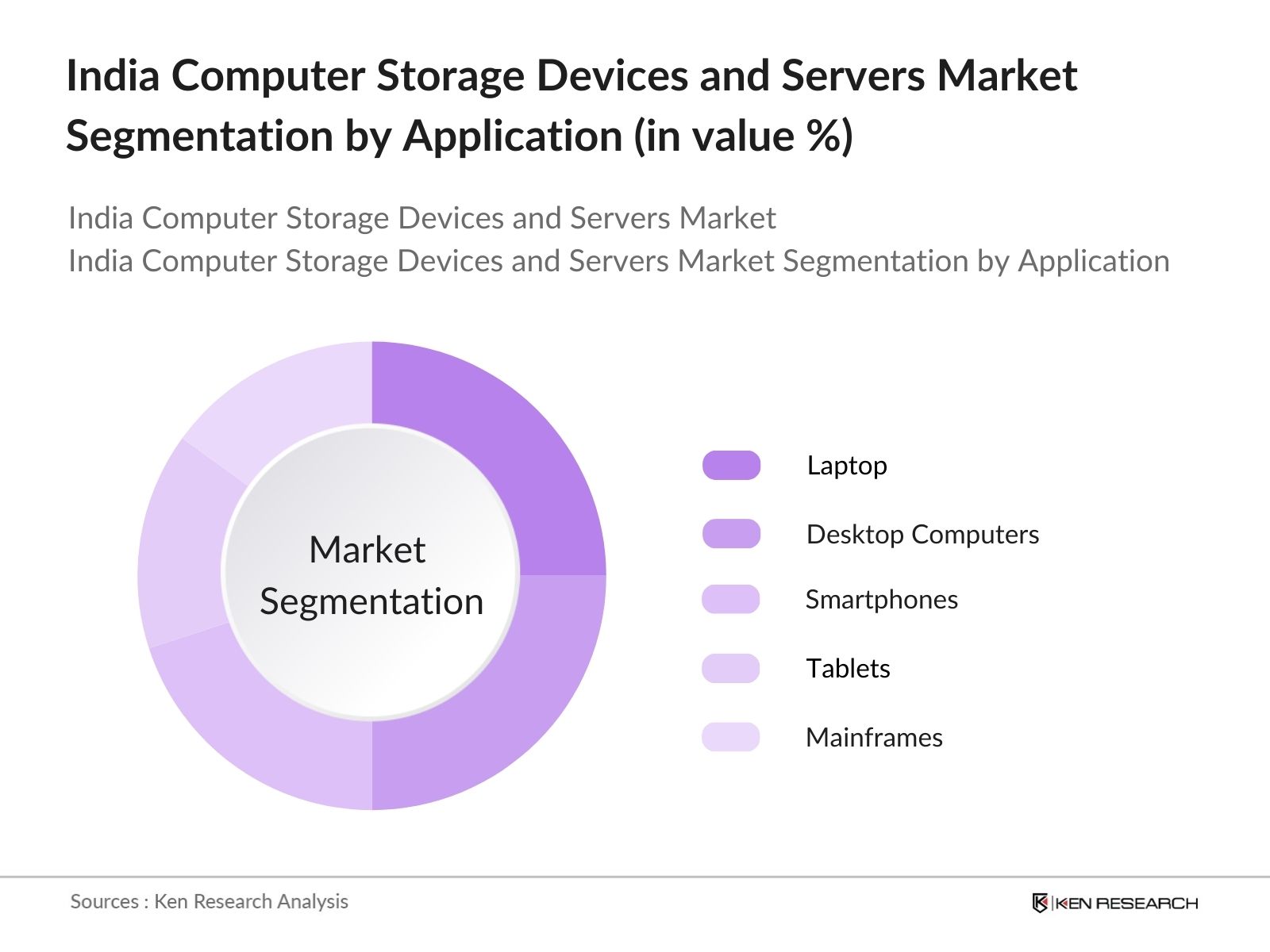

By Application: The market is further segmented by application into mainframes, laptops, desktop computers, tablets, and smartphones. Within this category, laptops have emerged as the leading sub-segment, driven by the increasing adoption of remote work and online education. The need for portable computing devices that offer high performance and substantial storage capacity has led to a surge in demand for laptops, thereby boosting the market for associated storage devices and servers.

India Computer Storage Devices and Servers Market Competitive Landscape

The India computer storage devices and servers market is characterized by the presence of several key players, both domestic and international. These companies are engaged in continuous innovation and strategic partnerships to enhance their market position.

|

Company Name |

Establishment Year |

Headquarters |

Market Presence |

Technology Integration |

Regional Focus |

Revenue (USD) |

Sustainability Initiatives |

|---|---|---|---|---|---|---|---|

|

IBM Corporation |

1911 |

Armonk, USA |

- |

- |

- |

- |

- |

|

Dell Technologies Inc. |

1984 |

Round Rock, USA |

- |

- |

- |

- |

- |

|

Hewlett Packard Enterprise (HPE) |

2015 |

Houston, USA |

- |

- |

- |

- |

- |

|

Lenovo Group Limited |

1984 |

Beijing, China |

- |

- |

- |

- |

- |

|

Cisco Systems, Inc. |

1984 |

San Jose, USA |

- |

- |

- |

- |

- |

India Computer Storage Devices and Servers Market Analysis

Growth Drivers

- Increasing Data Generation Across Industries: Industries are generating vast amounts of data across sectors such as finance, healthcare, retail, and manufacturing. According to recent reports, industries worldwide generate over 64 zettabytes of data annually, with projections of this volume exceeding 180 zettabytes in the next five years. The need to store, manage, and analyze this vast amount of information has driven demand for robust storage solutions. For instance, the healthcare industry alone is expected to generate 2.3 zettabytes of data in 2024, driven by increasing use of digital health records and imaging data.

- Adoption of Cloud Computing and Big Data Analytics: The global investment in cloud computing and big data analytics surpassed $300 billion in 2024, reflecting enterprises' reliance on these technologies for scaling operations and deriving insights from large datasets. Cloud adoption in particular is accelerating as it offers scalability and flexibility to handle large datasets. For example, major cloud service providers have reported client increases of over 150 million users globally, spurring demand for secure and scalable storage solutions within these infrastructures.

- Government Initiatives Promoting Digitalization: Governments are investing heavily in digital transformation across sectors to improve efficiency and public service delivery. For example, public sector digital spending in North America and Europe alone has exceeded $120 billion in 2024. Initiatives such as smart city projects, public sector cloud adoption, and digital health initiatives have increased data storage demands. In the Asia-Pacific region, governments are introducing policies that support digital business models, with projected government spending on digital infrastructure reaching over $60 billion by the end of the year.

Market Challenges

- High Initial Investment Costs: Initial capital expenditure for advanced storage solutions remains high, making it a challenge for smaller organizations to adopt these systems. In 2024, typical enterprise storage infrastructure setup costs ranged from $500,000 to $5 million, depending on storage capacity and security features. Smaller enterprises often find these costs prohibitive, limiting broader adoption despite a demonstrated need for data storage.

- Data Security and Privacy Concerns: In 2024, data breaches cost organizations worldwide over $4 billion, with each breach costing an average of $4.5 million per incident. With the increasing frequency of cyberattacks, enterprises are hesitant to adopt storage solutions that may not fully address security risks. The healthcare and finance sectors, in particular, face stringent regulatory requirements for data protection, further complicating storage adoption without comprehensive security.

India Computer Storage Devices and Servers Market Future Outlook

Over the next five years, the India computer storage devices and servers market is expected to witness substantial growth, driven by the continuous expansion of digital infrastructure, increased investments in data centers, and the adoption of emerging technologies such as artificial intelligence and the Internet of Things. Government initiatives promoting digitalization and favorable policies for IT infrastructure development are also anticipated to play a pivotal role in propelling market growth.

Market Opportunities

- Emergence of Edge Computing: The emergence of edge computing is driving demand for decentralized storage solutions. By 2024, enterprises allocated over $15 billion toward edge computing infrastructure, facilitating real-time data processing closer to data sources. Edge storage solutions allow faster data access and reduce latency, especially beneficial in sectors such as manufacturing and transportation, where real-time decision-making is essential.

- Integration of Artificial Intelligence in Storage Solutions: AI-enhanced storage solutions have gained traction, with enterprises investing over $30 billion in AI for storage and data management. AI can optimize storage allocation, predict usage patterns, and enhance data retrieval speeds. For example, automated tiered storage, powered by AI, can reduce operational costs by 20% by moving infrequently accessed data to lower-cost storage.

Scope of the Report

|

By Product Type |

Servers |

|

By Application |

Mainframes |

|

By Technology |

Hard Disk Drives (HDD) |

|

By End-User Industry |

Information Technology and Telecommunications |

|

By Region |

North |

Products

Key Target Audience

IT Infrastructure Providers

Data Center Operators

Cloud Service Providers

Enterprise IT Departments

Government and Regulatory Bodies (e.g., Ministry of Electronics and Information Technology)

Investors and Venture Capitalist Firms

Telecommunications Companies

Educational Institutions

Companies

Players Mentioned in the Report:

IBM Corporation

Dell Technologies Inc.

Hewlett Packard Enterprise (HPE)

Lenovo Group Limited

Cisco Systems, Inc.

Oracle Corporation

Fujitsu Limited

Huawei Technologies Co., Ltd.

NetApp, Inc.

Western Digital Corporation

Table of Contents

1. India Computer Storage Devices and Servers Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. India Computer Storage Devices and Servers Market Size (In USD Billion)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. India Computer Storage Devices and Servers Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Data Generation Across Industries

3.1.2. Adoption of Cloud Computing and Big Data Analytics

3.1.3. Government Initiatives Promoting Digitalization

3.1.4. Expansion of IT Infrastructure in Enterprises

3.2. Market Challenges

3.2.1. High Initial Investment Costs

3.2.2. Data Security and Privacy Concerns

3.2.3. Rapid Technological Advancements Leading to Obsolescence

3.3. Opportunities

3.3.1. Emergence of Edge Computing

3.3.2. Integration of Artificial Intelligence in Storage Solutions

3.3.3. Growing Demand for Energy-Efficient Storage Devices

3.4. Trends

3.4.1. Shift Towards Solid-State Drives (SSDs)

3.4.2. Adoption of Hyper-Converged Infrastructure

3.4.3. Increased Investment in Data Centers

3.5. Government Regulations

3.5.1. Data Localization Laws

3.5.2. Incentives for IT Hardware Manufacturing

3.5.3. Standards for Data Security and Privacy

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

4. India Computer Storage Devices and Servers Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Servers

4.1.2. Computer Storage Devices

4.2. By Application (In Value %)

4.2.1. Mainframes

4.2.2. Laptops

4.2.3. Desktop Computers

4.2.4. Tablets

4.2.5. Smartphones

4.3. By Technology (In Value %)

4.3.1. Hard Disk Drives (HDD)

4.3.2. Solid-State Drives (SSD)

4.3.3. Network-Attached Storage (NAS)

4.3.4. Storage Area Network (SAN)

4.3.5. Direct-Attached Storage (DAS)

4.4. By End-User Industry (In Value %)

4.4.1. Information Technology and Telecommunications

4.4.2. Banking, Financial Services, and Insurance (BFSI)

4.4.3. Government

4.4.4. Healthcare

4.4.5. Media and Entertainment

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. East India

4.5.4. West and Central India

5. India Computer Storage Devices and Servers Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. IBM Corporation

5.1.2. Dell Technologies Inc.

5.1.3. Hewlett Packard Enterprise Development LP

5.1.4. Lenovo Group Limited

5.1.5. Cisco Systems, Inc.

5.1.6. Oracle Corporation

5.1.7. Fujitsu Limited

5.1.8. Huawei Technologies Co., Ltd.

5.1.9. NetApp, Inc.

5.1.10. Western Digital Corporation

5.1.11. Seagate Technology Holdings PLC

5.1.12. Toshiba Corporation

5.1.13. Samsung Electronics Co., Ltd.

5.1.14. Micron Technology, Inc.

5.1.15. Hitachi Vantara LLC

5.2. Cross Comparison Parameters

5.2.1. Number of Employees

5.2.2. Headquarters Location

5.2.3. Year of Establishment

5.2.4. Annual Revenue

5.2.5. Product Portfolio

5.2.6. Market Share

5.2.7. R&D Investment

5.2.8. Regional Presence

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. India Computer Storage Devices and Servers Market Regulatory Framework '

6.1. Data Protection and Privacy Laws

6.2. Compliance Requirements for Storage Devices

6.3. Certification Processes for Servers and Storage Solutions

7. India Computer Storage Devices and Servers Future Market Size (In USD Billion)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. India Computer Storage Devices and Servers Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By End-User Industry (In Value %)

8.5. By Region (In Value %)

9. India Computer Storage Devices and Servers Market Analysts Recommendations

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the India computer storage devices and servers market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the India computer storage devices and servers market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple manufacturers and service providers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the India computer storage devices and servers market.

Frequently Asked Questions

01. How big is the India computer storage devices and servers market?

The India computer storage devices and servers market was valued at USD 9 billion in 2023, driven by rapid digitization and increased data generation across various sectors.

02. What are the challenges in the India computer storage devices and servers market?

Challenges include high initial investment costs, data security and privacy concerns, and the rapid pace of technological advancements leading to potential obsolescence of existing systems.

03. Who are the major players in the India computer storage devices and servers market?

Key players include IBM Corporation, Dell Technologies Inc., Hewlett Packard Enterprise (HPE), Lenovo Group Limited, and Cisco Systems, Inc.

04. What are the growth drivers of the India computer storage devices and servers market?

Growth drivers encompass increasing data generation, adoption of cloud computing and big data analytics, government initiatives promoting digitalization, and the expansion of IT infrastructure in enterprises.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.