India Data Center Cooling Market Outlook to 2030

Region:India

Author(s):Yogita Sahu

Product Code:KROD3783

Region:India

Author(s):Yogita Sahu

Product Code:KROD3783

October 2024

92

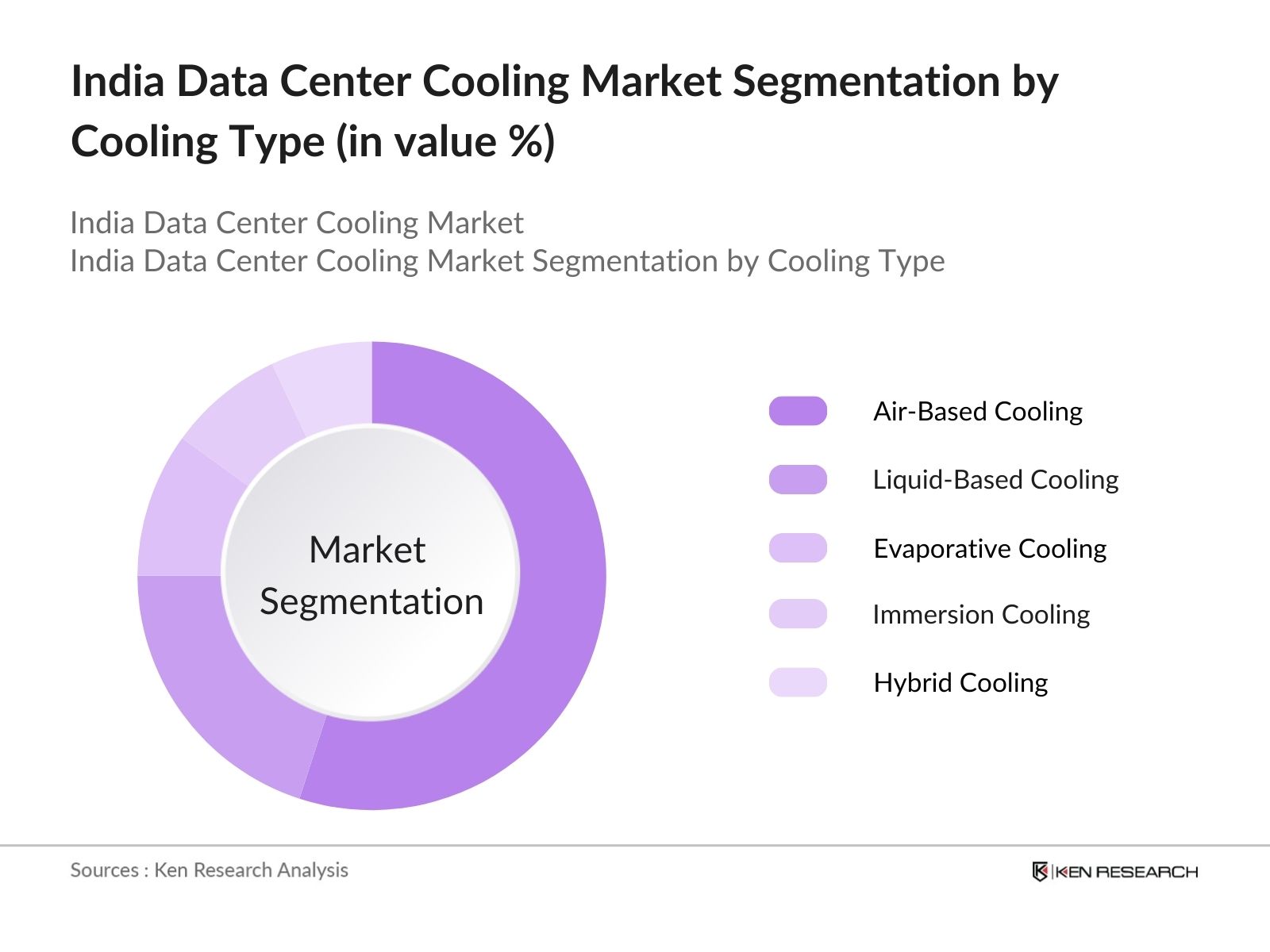

By Cooling Type: The market is segmented by cooling type into air-based cooling, liquid-based cooling, evaporative cooling, immersion cooling, and hybrid cooling. Air-based cooling remains the dominant segment, driven by its established presence and ease of deployment in existing data centers. This segment is highly popular due to its cost-efficiency and compatibility with various data center sizes, including hyperscale facilities.

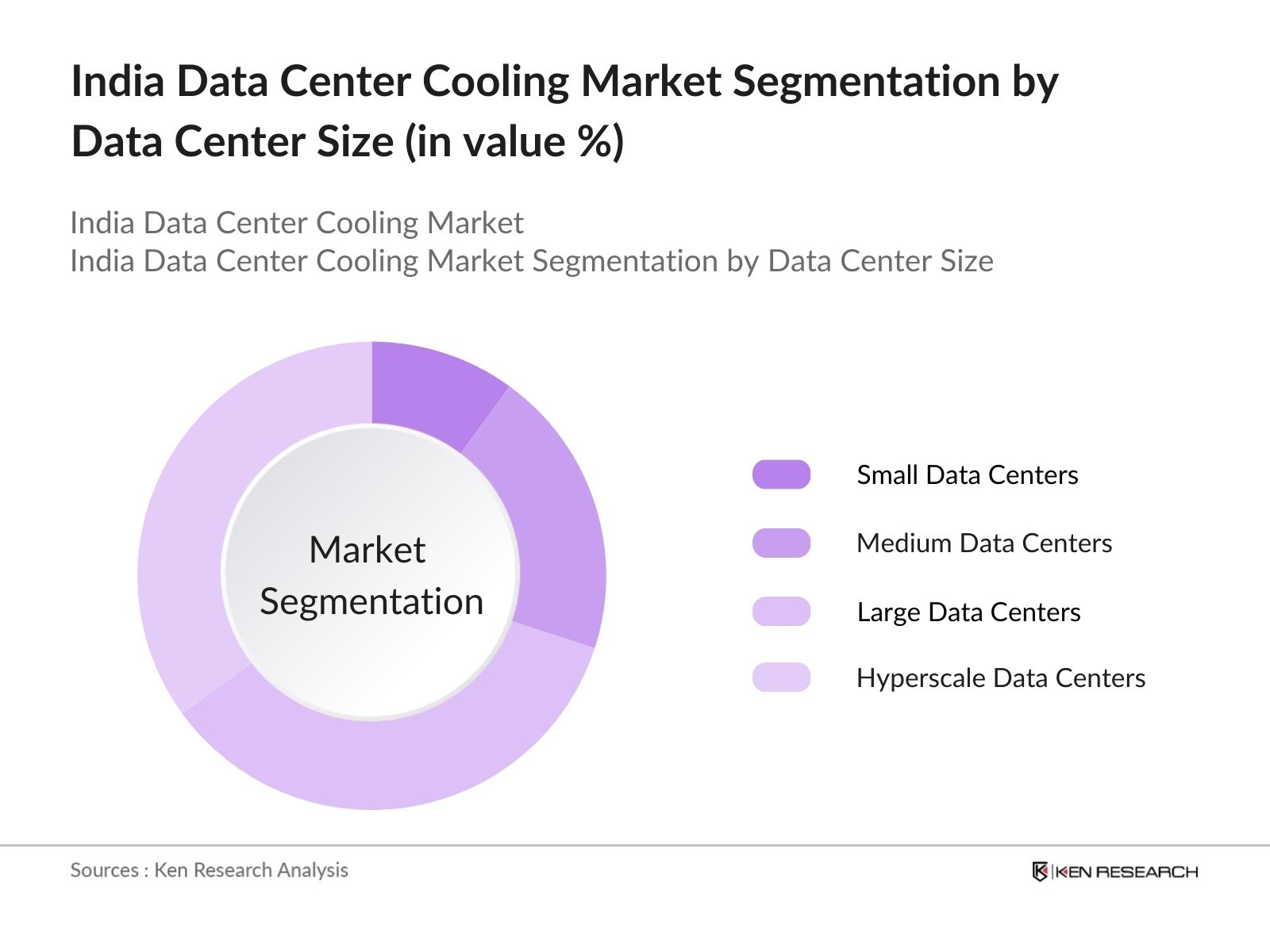

By Data Center Size: The market is further segmented by data center size into small, medium, large, and hyperscale data centers. Large and hyperscale data centers dominate the market, as they house massive server racks that generate heat, requiring specialized cooling solutions to maintain optimal temperatures. The hyperscale data center segment is particularly growing due to increased investments by global technology companies in India, drawn by the countrys strategic importance as a data hub.

The market is dominated by both international and domestic players, with leading companies specializing in energy-efficient cooling technologies. The market competition is characterized by the push for sustainability, as players innovate to reduce the carbon footprint of data center operations.

|

Company |

Year Established |

Headquarters |

Cooling Type Focus |

Energy Efficiency Innovations |

Product Portfolio Size |

Key Data Center Partnerships |

Revenue (INR Bn) |

Technology Integration |

Presence in India |

|

Vertiv Group Corp. |

1946 |

Ohio, USA |

|||||||

|

Schneider Electric |

1836 |

Rueil-Malmaison, France |

|||||||

|

STULZ GmbH |

1947 |

Hamburg, Germany |

|||||||

|

Mitsubishi Electric Corp. |

1921 |

Tokyo, Japan |

|||||||

|

Huawei Technologies Co., Ltd. |

1987 |

Shenzhen, China |

Over the next five years, the India Data Center Cooling industry is expected to experience robust growth, driven by the increasing demand for digital services, cloud adoption, and continued investments in hyperscale data centers. Government support for data localization and policies favoring energy-efficient cooling systems will further boost the market.

|

Cooling Type |

Air-Based Cooling |

|

Liquid-Based Cooling |

|

|

Evaporative Cooling |

|

|

Immersion Cooling |

|

|

Hybrid Cooling |

|

|

Component |

Chillers |

|

Air Handling Units (AHUs) |

|

|

Computer Room Air Conditioners (CRACs) |

|

|

Pumps |

|

|

Cooling Towers |

|

|

Data Center Size |

Small Data Centers |

|

Medium Data Centers |

|

|

Large and Hyperscale Data Centers |

|

|

End-User |

IT & Telecom |

|

BFSI |

|

|

Healthcare |

|

|

Government and Defense |

|

|

Retail and E-commerce |

|

|

Region |

North |

|

South |

|

|

East |

|

|

West |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Increasing Digitalization

3.1.2 Government Initiatives for Data Localization

3.1.3 Rising Demand for Energy-Efficient Solutions

3.1.4 Expansion of Cloud Services and Hyperscale Data Centers

3.2 Market Challenges

3.2.1 High Initial Setup Costs

3.2.2 Energy Consumption Regulations (Energy efficiency standards)

3.2.3 Lack of Skilled Workforce for Maintenance

3.2.4 High Heat Dissipation Requirements

3.3 Opportunities

3.3.1 Emergence of Green Data Centers

3.3.2 Increasing Adoption of Liquid Cooling Systems

3.3.3 Strategic Partnerships with Technology Providers

3.3.4 Government Incentives for Energy-Efficient Cooling Solutions

3.4 Trends

3.4.1 Adoption of IoT for Real-Time Monitoring

3.4.2 Integration with Smart Power Distribution Units

3.4.3 Use of Renewable Energy for Cooling (Renewable energy sources integration)

3.4.4 Modular Data Center Design

3.5 Government Regulation

3.5.1 Cooling System Efficiency Regulations

3.5.2 Energy Consumption Standards

3.5.3 Green Data Center Policies

3.5.4 Environmental Impact Assessment Regulations

3.6 SWOT Analysis

3.7 Stake Ecosystem (Key stakeholders: operators, equipment manufacturers, regulators)

3.8 Porters Five Forces (Bargaining power of suppliers, threat of substitutes, etc.)

3.9 Competition Ecosystem

4.1 By Cooling Type (In Value %)

4.1.1 Air-Based Cooling

4.1.2 Liquid-Based Cooling

4.1.3 Evaporative Cooling

4.1.4 Immersion Cooling

4.1.5 Hybrid Cooling

4.2 By Component (In Value %)

4.2.1 Chillers

4.2.2 Air Handling Units (AHUs)

4.2.3 Computer Room Air Conditioners (CRACs)

4.2.4 Pumps

4.2.5 Cooling Towers

4.3 By Data Center Size (In Value %)

4.3.1 Small Data Centers

4.3.2 Medium Data Centers

4.3.3 Large and Hyperscale Data Centers

4.4 By End-User (In Value %)

4.4.1 IT & Telecom

4.4.2 BFSI

4.4.3 Healthcare

4.4.4 Government and Defense

4.4.5 Retail and E-commerce

4.5 By Region (In Value %)

4.5.1 North

4.5.2 South

4.5.3 East

4.5.4 West

5.1 Detailed Profiles of Major Companies

5.1.1 Vertiv Group Corp.

5.1.2 Schneider Electric

5.1.3 STULZ GmbH

5.1.4 Mitsubishi Electric Corporation

5.1.5 Nortek Air Solutions

5.1.6 Rittal GmbH & Co. KG

5.1.7 Fujitsu General

5.1.8 Daikin Industries Ltd.

5.1.9 CoolIT Systems Inc.

5.1.10 Asetek A/S

5.1.11 Huawei Technologies Co., Ltd.

5.1.12 ABB Group

5.1.13 Delta Electronics, Inc.

5.1.14 Trane Technologies

5.1.15 Hitachi, Ltd.

5.2 Cross Comparison Parameters (Cooling efficiency, data center footprint, technology partnerships, regional presence, etc.)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Energy-Efficiency Standards (Government regulations on energy usage)

6.2 Compliance Requirements

6.3 Certification Processes

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Cooling Type (In Value %)

8.2 By Component (In Value %)

8.3 By Data Center Size (In Value %)

8.4 By End-User (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

In the first phase, we map out all stakeholders within the India Data Center Cooling Market. This includes identifying relevant companies, technologies, and government policies. Secondary data is gathered through extensive desk research, utilizing proprietary databases and industry reports to pinpoint market dynamics.

This step involves gathering historical data on data center cooling technologies and evaluating their market penetration in different regions of India. We also analyze key metrics like operational efficiency and energy consumption to derive revenue estimates and trends.

Market hypotheses are validated by engaging with industry experts through telephone interviews and online consultations. Experts from top data center firms provide key insights on market challenges, cooling technology advancements, and upcoming trends.

The final step involves synthesizing all the collected data into a comprehensive report, ensuring that the insights gathered are accurate and well-validated. Data center operators and technology providers are consulted directly to confirm findings.

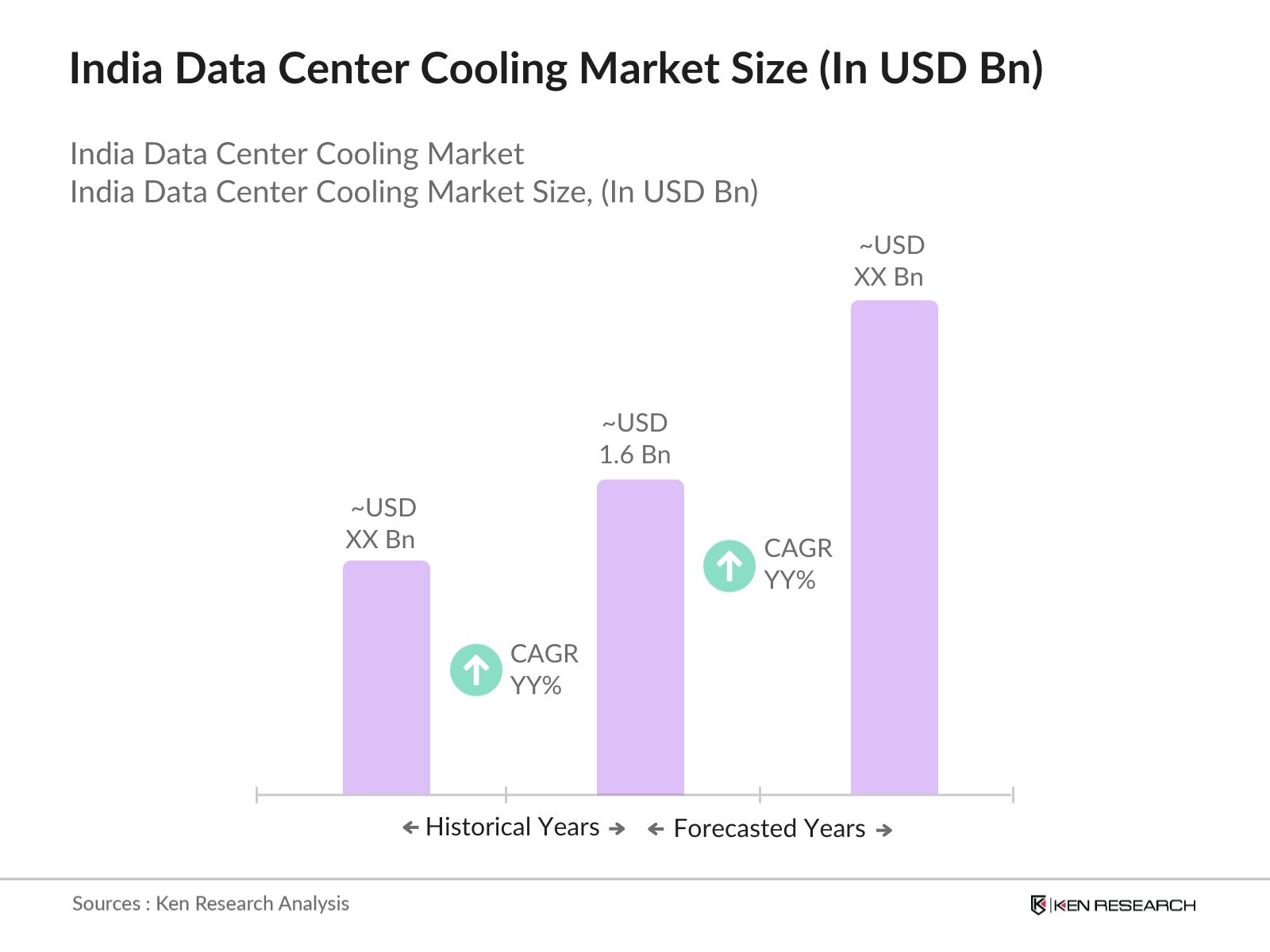

The India Data Center Cooling market is valued at USD 1.6 billion, driven by rapid digitalization, cloud services, and government initiatives for data localization.

Key challenges in the India Data Center Cooling market include high initial investment costs, energy efficiency regulations, and the lack of skilled workforce to manage advanced cooling solutions.

Major players in the India Data Center Cooling market include Vertiv Group Corp., Schneider Electric, STULZ GmbH, Mitsubishi Electric Corporation, and Huawei Technologies Co., Ltd.

The India Data Center Cooling market is propelled by increasing digitalization, rising demand for energy-efficient data centers, and the expansion of cloud services in India.

Key trends in the India Data Center Cooling market include the adoption of liquid cooling technologies, green data centers, and the integration of AI and IoT for real-time monitoring and optimization of cooling systems.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.