India Diabetes Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD9083

December 2024

96

About the Report

India Diabetes Market Overview

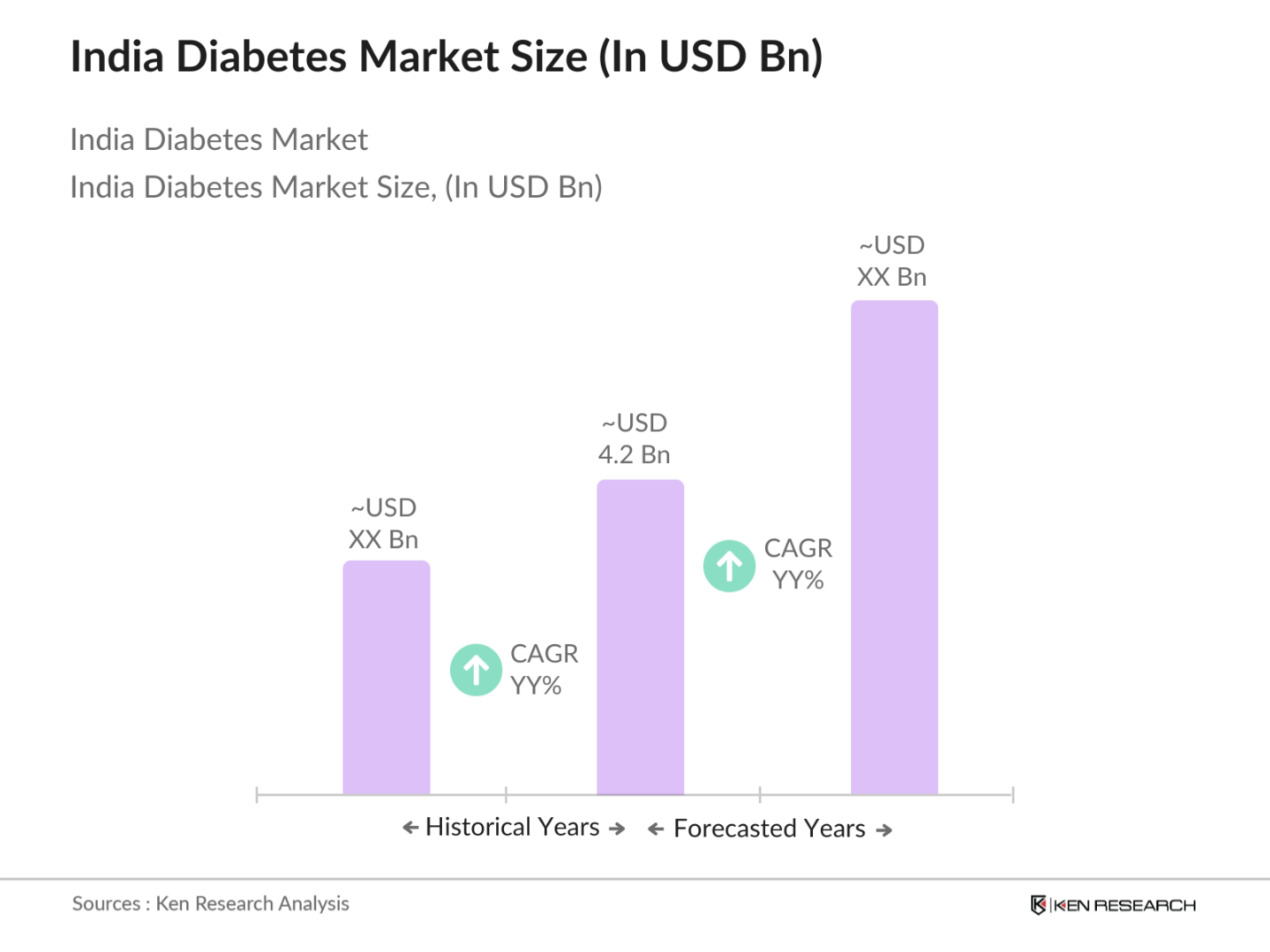

- The India diabetes market is valued at USD 4.2billion, driven by the increasing prevalence of diabetes, particularly type 2 diabetes, which is fueled by factors such as urbanization, sedentary lifestyles, and unhealthy diets. Rising healthcare expenditures and advancements in diabetes diagnostics and treatment are also contributing to market growth.

- Indias diabetes market is dominated by regions such as the Western and Northern parts of the country, largely due to better healthcare infrastructure, higher urbanization rates, and increasing awareness regarding diabetes management. These regions also see higher penetration of advanced medical devices and treatments, making them pivotal in the market's expansion.

- The Indian government has implemented several national health programs aimed at preventing diabetes. These initiatives focus on promoting early diagnosis, raising public awareness, and encouraging lifestyle interventions to manage and prevent diabetes. The programs aim to provide screening and healthcare access in both rural and urban areas, targeting high-risk populations and ensuring more comprehensive coverage. The governments focus is on reducing the long-term burden of non-communicable diseases, including diabetes, through sustained national campaigns and partnerships with healthcare organizations.

India Diabetes Market Segmentation

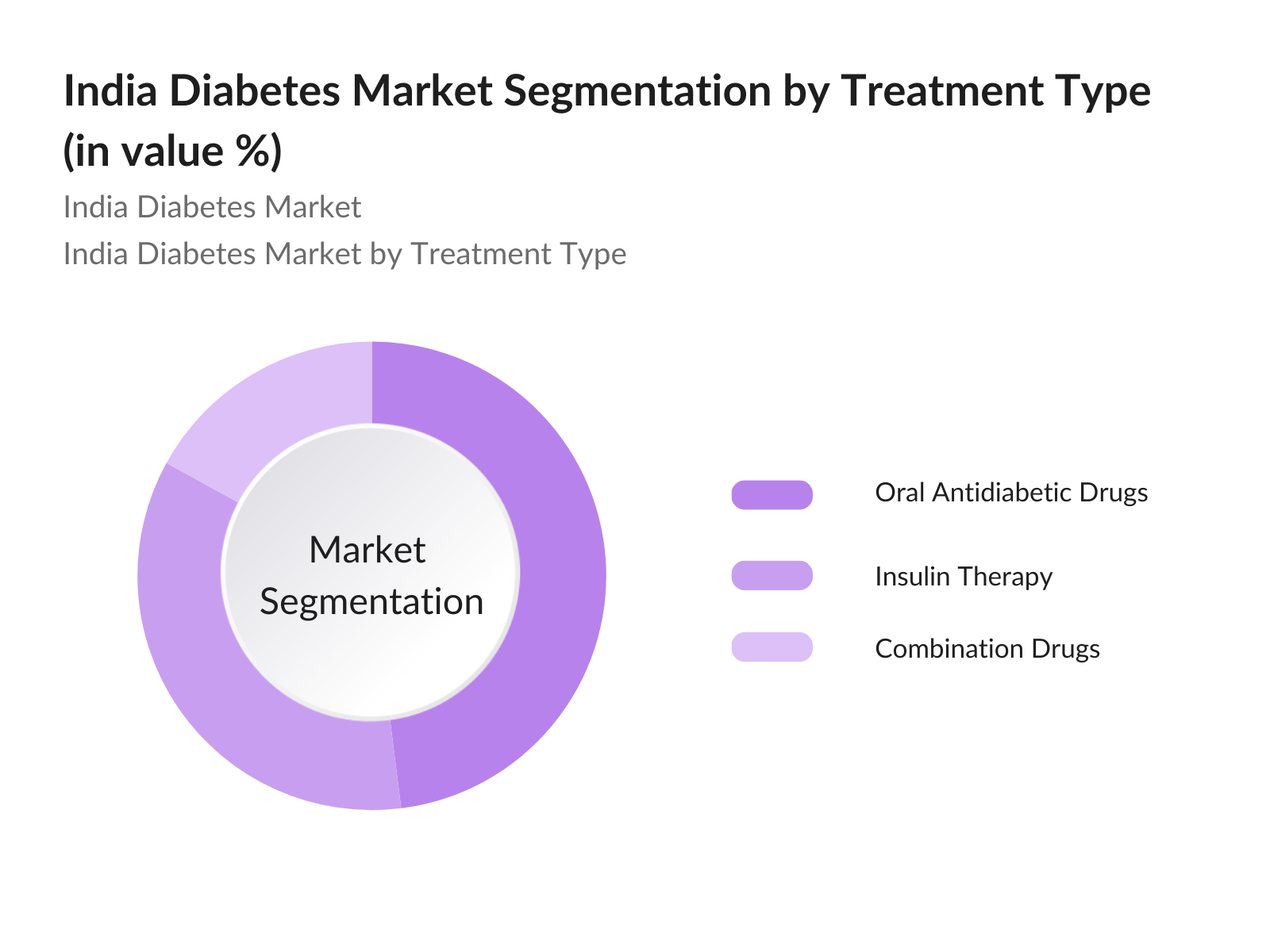

By Treatment Type: India's diabetes market is segmented by treatment type into oral antidiabetic drugs, insulin therapy, and combination drugs. Oral antidiabetic drugs hold a dominant market share due to their affordability and widespread use in managing type 2 diabetes. The convenience and non-invasive nature of oral medications make them more popular among patients. Drugs like Metformin and Sulfonylureas are often the first line of treatment.

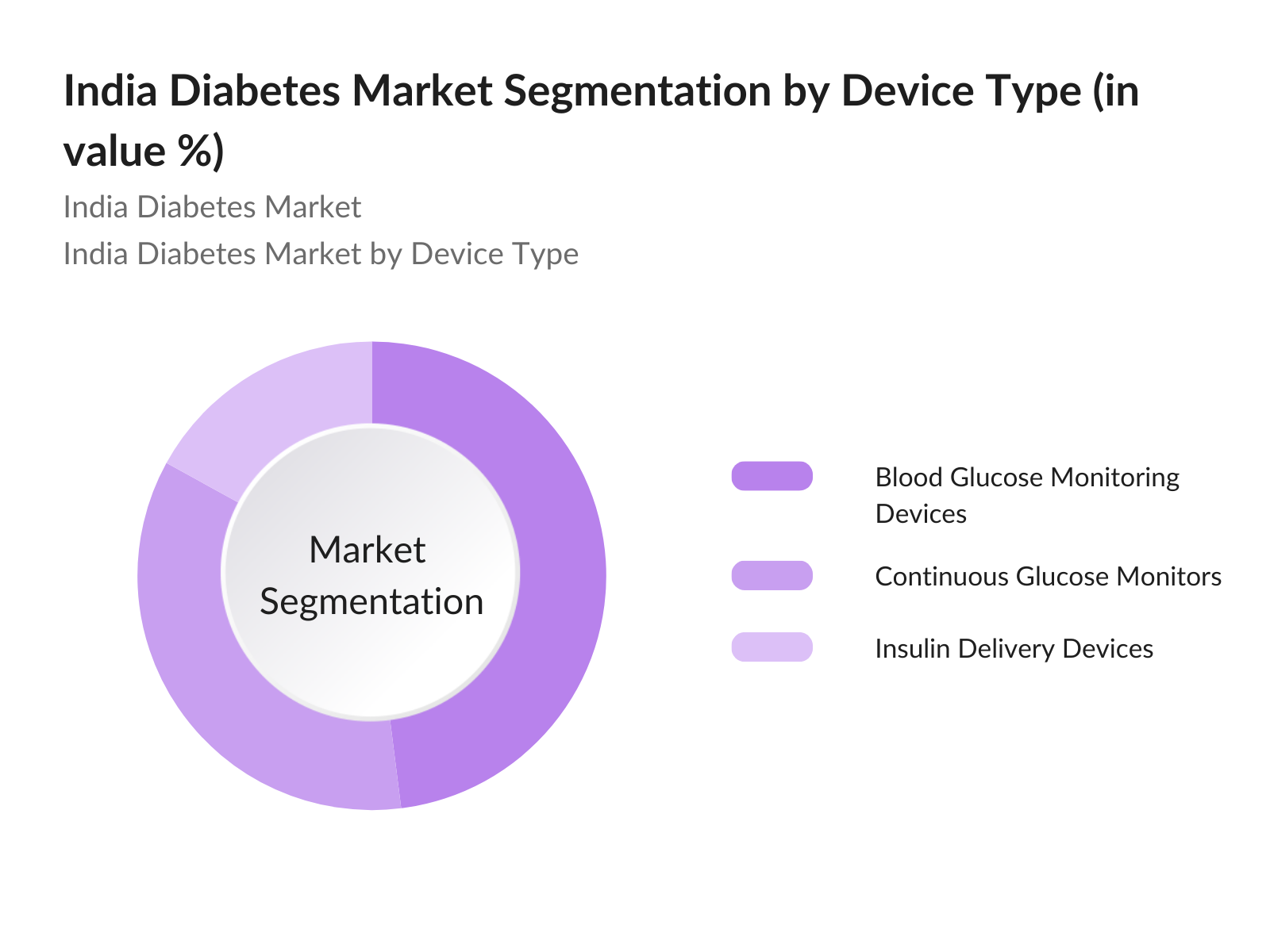

By Device Type: The market is also segmented by device type into blood glucose monitoring devices, continuous glucose monitors (CGM), and insulin delivery devices (insulin pumps and pens). Blood glucose monitoring devices dominate the market due to their essential role in diabetes management. These devices allow for frequent monitoring, which is crucial for maintaining optimal glucose levels and reducing complications associated with diabetes.

India Diabetes Market Competitive Landscape

The India diabetes market is dominated by global and domestic players. Leading companies have been involved in strategic partnerships, mergers, and innovative product developments to strengthen their market positions. These companies leverage technology advancements and R&D investments to introduce effective diabetes management solutions.

|

Company Name |

Established |

Headquarters |

Products |

R&D Investment |

Market Share |

Strategic Collaborations |

Global Presence |

Distribution Network |

Key Patents |

|

Novo Nordisk A/S |

1923 |

Denmark |

Insulin |

- |

- |

- |

- |

- |

- |

|

Medtronic |

1949 |

USA |

CGMs |

- |

- |

- |

- |

- |

- |

|

Eli Lilly and Co. |

1876 |

USA |

Insulin |

- |

- |

- |

- |

- |

- |

|

Roche Diabetes Care |

1896 |

Switzerland |

Devices |

- |

- |

- |

- |

- |

- |

|

Sanofi |

1973 |

France |

Insulin |

- |

- |

- |

- |

- |

- |

India Diabetes Market Analysis

Market Growth Drivers

- Increasing Urbanization: Indias rapid urbanization has had a direct impact on lifestyle diseases, including diabetes. By 2024, it is estimated that over 600 million people will live in urban areas in India, leading to higher rates of sedentary lifestyles and unhealthy dietskey factors contributing to the rise in diabetes. According to the World Bank, this shift towards urban living brings an increased demand for better healthcare infrastructure to address chronic conditions like diabetes. Urban centers also see higher demand for modern diagnostic tools and treatments to manage the disease.

- Adoption of Advanced Diagnostic Devices: Indias adoption of advanced diagnostic devices, particularly Continuous Glucose Monitoring (CGM) systems, has surged due to increased healthcare awareness and demand for better diabetes management tools. The Indian healthcare sector is seeing growing investment in cutting-edge technology, particularly in major cities, with diagnostic laboratories witnessing an increase in glucose monitoring equipment. Recent reports indicate that 20,000 CGM units were distributed across Indian hospitals in 2023, improving early diagnosis rates for diabetes complications. Government policies promoting digital health further strengthen this trend.

- Public and Private Healthcare Investments: Indias healthcare sector has seen significant investment from both public and private entities, with over INR 2.23 trillion allocated for healthcare in the 2023 budget. This investment supports the growing demand for diabetes care through the establishment of more healthcare centers and diagnostic facilities across the country. Private investment in the Indian healthcare industry is projected to grow, with an emphasis on expanding diabetic care services. The National Health Mission and state governments are collaborating on improving access to essential diabetes treatments, particularly in underserved areas.

Market Challenges:

- High Cost of Insulin Devices: The high cost of insulin devices remains a significant barrier for many in India, especially in rural and semi-urban areas. On average, an insulin pump costs between INR 150,000 to 200,000, which is unaffordable for a large portion of Indias population. This price point restricts widespread usage of such devices, leading patients to rely on traditional methods. Government interventions to subsidize insulin devices and make them accessible through public health programs are limited but crucial. Access to low-cost alternatives is critical for scaling diabetes management in the country.

- Insufficient Access to Healthcare Infrastructure: Indias healthcare infrastructure struggles to keep pace with the growing demand for diabetes care, particularly in tier-2 and tier-3 cities. Despite investments, there are only 1.34 hospital beds available per 1,000 people, which falls short of the WHOs recommended ratio of 5 beds per 1,000 people. Additionally, there are gaps in the availability of trained endocrinologists and diabetic care specialists, limiting the treatment options for patients, especially in rural areas. Lack of healthcare centers with specialized diabetes units further adds to the challenge.

India Diabetes Market Future Outlook

Over the next five years, the India diabetes market is expected to experience substantial growth. Key drivers include continuous advancements in diabetes management technologies, increasing government initiatives to improve healthcare infrastructure, and a rising number of diabetic patients. The growing adoption of digital health solutions such as continuous glucose monitoring devices and the integration of AI in healthcare will play a pivotal role in shaping the future of the market.

Market Opportunities:

- Increased Usage of Insulin Delivery Devices: The usage of insulin delivery devices, such as insulin pens and pumps, has been increasing in India. In 2023, sales of insulin pens reached approximately 8 million units, reflecting a shift toward more advanced and efficient diabetes management tools. The ease of use and the ability to control dosage have made these devices popular among both patients and healthcare providers. Government initiatives aimed at reducing import duties on medical devices in 2023 further contributed to the accessibility of insulin delivery systems across various healthcare settings.

- Integration of Artificial Intelligence for Diabetes Management: Artificial intelligence (AI) is being integrated into diabetes care in India, with AI-powered diagnostic tools and predictive models becoming more common in healthcare settings. AI solutions can predict diabetic complications by analyzing patient data, improving treatment outcomes. In 2023, several hospitals and diagnostic labs in India adopted AI-based technologies to enhance diabetes management, with approximately 500 facilities implementing AI for early detection. This trend is expected to revolutionize the approach to personalized diabetes care in the country.

Scope of the Report

|

By Treatment Type |

Insulin Therapy Oral Antidiabetic Drugs Combination Drugs |

|

By Device Type |

Blood Glucose Monitoring Devices Continuous Glucose Monitors Insulin Delivery Devices |

|

By Test Type |

Random Blood Sugar Test Fasting Blood Sugar Test Oral Glucose Tolerance Test |

|

By End-User |

Hospitals and Clinics Home Care Settings Diagnostic Centers |

|

By Region |

North-East Midwest West Coast Southern States |

Products

Key Target Audience

Government and regulatory bodies (Ministry of Health and Family Welfare, National Health Mission)

Pharmaceutical manufacturers

Diabetes device manufacturers

Healthcare providers (Hospitals, Clinics)

Insurance companies

Investments and venture capital firms

Retail pharmacies

Private diabetes research institutions

Companies

Players Mention in the Report

Novo Nordisk A/S

Abbott Laboratories

Sanofi S.A.

Roche Diabetes Care

Medtronic PLC

Eli Lilly and Co.

Glenmark Pharmaceuticals

Pfizer Inc.

AstraZeneca PLC

Novartis AG

USV Pvt. Ltd.

Johnson & Johnson Services, Inc.

Becton Dickinson and Co.

Ypsomed Holding AG

Sun Pharmaceutical Industries Ltd.

Table of Contents

1. India Diabetes Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Drivers (Government Initiatives, Rising Diabetes Prevalence, Sedentary Lifestyles)

1.4 Market Segmentation Overview

2. India Diabetes Market Size (In INR Billion)

2.1 Historical Market Size

2.2 Key Market Developments and Milestones

2.3 Future Market Growth Analysis (Focus on Urban vs Rural Penetration)

3. India Diabetes Market Dynamics

3.1 Growth Drivers

Increasing Urbanization

Adoption of Advanced Diagnostic Devices

Public and Private Healthcare Investments

3.2 Challenges

High Cost of Insulin Devices

Lack of Awareness in Rural Areas

Insufficient Access to Healthcare Infrastructure

3.3 Opportunities

Rising Use of Digital Health Tools (e.g., Continuous Glucose Monitoring Systems)

Expansion into Untapped Markets

Public-Private Collaborations

3.4 Trends

Increased Usage of Insulin Delivery Devices

Integration of Artificial Intelligence for Diabetes Management

Growth in Wearable Diabetes Devices

3.5 Government Regulations

National Health Programs for Diabetes Prevention

Regulatory Guidelines for Diagnostic Devices

Public Awareness Campaigns

4. India Diabetes Market Segmentation (Market-Specific Parameters)

4.1 By Treatment Type (In Value %)

Insulin Therapy

Oral Antidiabetic Drugs

Combination Drugs

4.2 By Device Type (In Value %)

Blood Glucose Monitoring Devices

Continuous Glucose Monitors

Insulin Delivery Devices (Pumps, Pens)

4.3 By Test Type (In Value %)

Random Blood Sugar Test

Oral Glucose Tolerance Test

Fasting Blood Sugar Test

4.4 By End-User (In Value %)

Hospitals and Clinics

Home Care Settings

Diagnostic Centers

4.5 By Region (In Value %)

Western Region

Northern Region

Southern Region

Eastern Region

5. India Diabetes Competitive Landscape

5.1 Key Competitor Profiles

Novo Nordisk A/S

Abbott Laboratories

Sanofi S.A.

Roche Diabetes Care

Medtronic PLC

Eli Lilly and Co.

Glenmark Pharmaceuticals

Pfizer Inc.

AstraZeneca PLC

Novartis AG

USV Pvt. Ltd.

Johnson & Johnson Services, Inc.

Becton Dickinson and Co.

Ypsomed Holding AG

Sun Pharmaceutical Industries Ltd.

5.2 Market Share Analysis

5.3 Strategic Initiatives

5.4 Mergers and Acquisitions

5.5 Investment and Funding Analysis

5.6 Competitive Benchmarking (Cross-Comparison Parameters: Revenue, R&D Investments, Technological Advancements, Global Reach, Patient Penetration, Product Portfolio, Sales Channels, Employee Strength)

6. India Diabetes Regulatory Landscape

6.1 National Guidelines for Diabetes Care

6.2 Regulatory Approvals for Diabetes Devices

6.3 Compliance Framework for Pharmaceutical Drugs

7. India Diabetes Future Market Size Projections (In INR Billion)

7.1 Growth Drivers for Future Market Expansion

7.2 Role of Technology in Future Market Growth

8. India Diabetes Market Analysts Recommendations

8.1 TAM/SAM/SOM Analysis

8.2 Key Market Entry Strategies for New Entrants

8.3 Future White Space Opportunities

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

We began by constructing a comprehensive map of stakeholders in the India diabetes market. This involved extensive desk research to gather industry-level information from credible sources. Key variables such as treatment adoption rates, device usage, and patient demographics were identified.

Step 2: Market Analysis and Construction

Historical market data from 2018-2023 was compiled and analyzed to assess the growth dynamics of the market. Key metrics such as penetration of glucose monitoring devices and insulin therapy trends were evaluated to build reliable market projections.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses regarding future growth patterns were validated through consultations with industry experts, including endocrinologists and healthcare providers. These interviews provided qualitative insights into emerging trends in the diabetes management market.

Step 4: Research Synthesis and Final Output

The final phase involved synthesizing data from multiple primary and secondary sources. This was followed by statistical validation to ensure the accuracy of revenue estimates and market share breakdowns.

Frequently Asked Questions

01. How big is the India Diabetes Market?

The India diabetes market is valued at USD 4.2billion, driven by the rising prevalence of diabetes and increasing government initiatives to improve healthcare infrastructure

02. What are the challenges in the India Diabetes Market?

Key challenges include the high cost of advanced insulin delivery devices, limited healthcare access in rural areas, and low awareness of diabetes management

03. Who are the major players in the India Diabetes Market?

Major players include Novo Nordisk, Abbott, Sanofi, Roche, and Medtronic, all of whom have significant investments in R&D and strategic partnerships within India

04. What are the growth drivers of the India Diabetes Market?

The market is driven by increasing healthcare expenditures, urbanization, and advancements in diabetes diagnostic and treatment technologies

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.