India Dry Fruits Market Outlook to 2030

Region:India

Author(s):Paribhasha Tiwari

Product Code:KROD4659

Region:India

Author(s):Paribhasha Tiwari

Product Code:KROD4659

December 2024

90

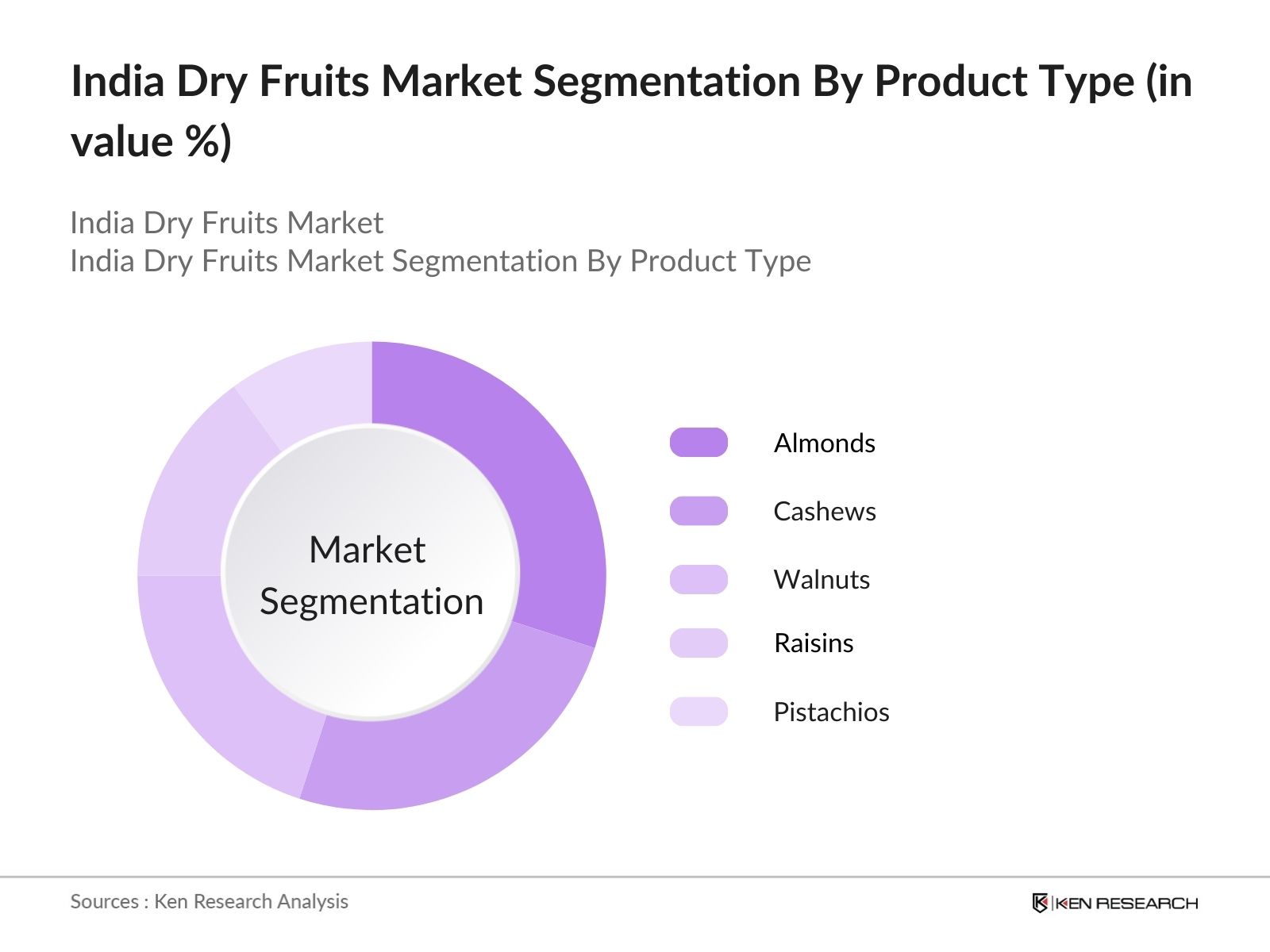

By Product Type: The India dry fruits market is segmented by product type into almonds, cashews, walnuts, raisins, and pistachios. Almonds currently hold the dominant market share due to their versatile usage in both snacking and culinary applications. They are consumed raw, roasted, or processed into almond milk and other products. The growing consumer preference for plant-based alternatives, such as almond-based milk and flour, has further contributed to the dominance of this sub-segment. Moreover, almonds are often marketed as a premium, healthy option with high protein content, making them a favorite among health-conscious individuals.

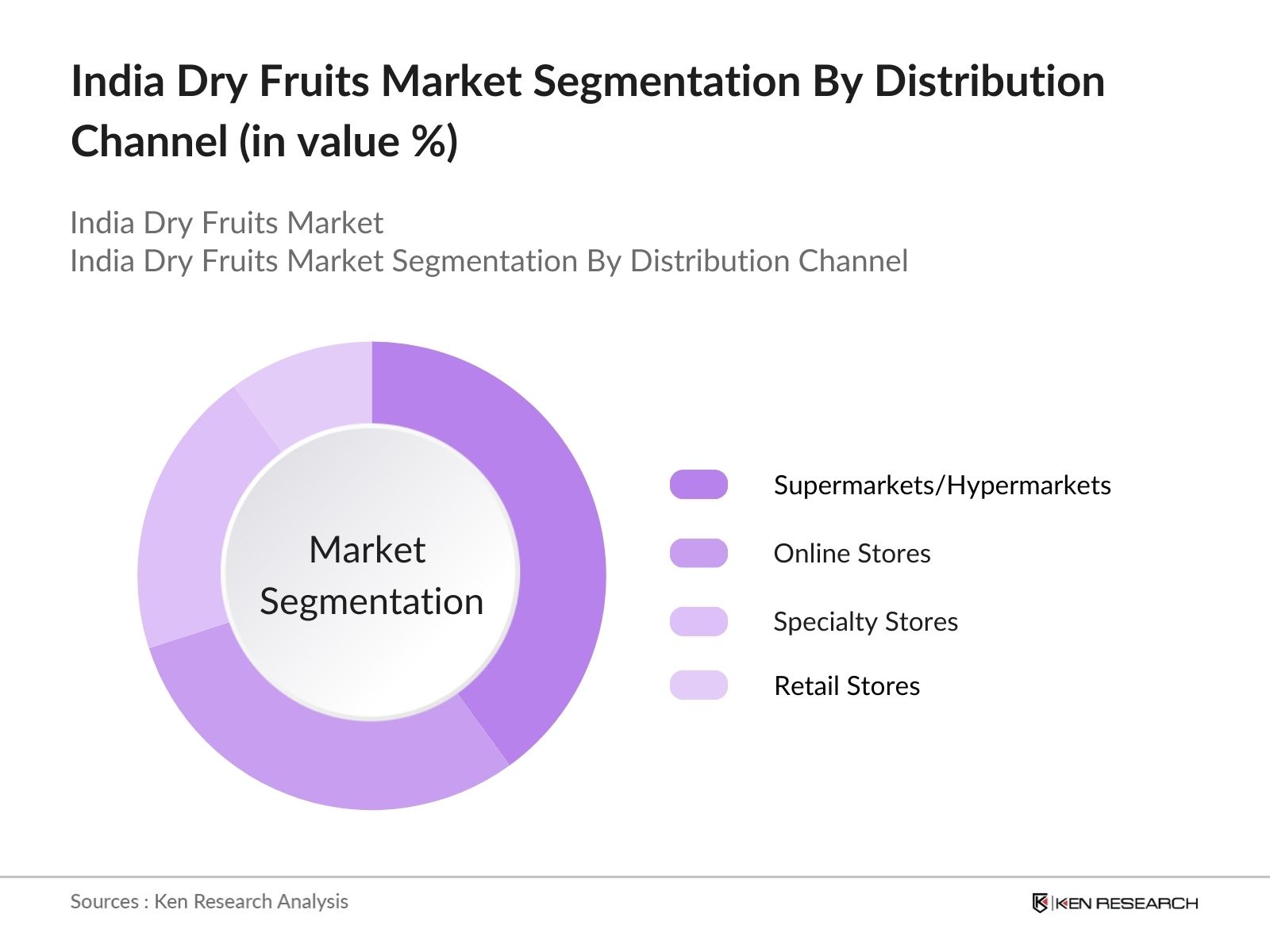

By Distribution Channel: The market is segmented by distribution channel into supermarkets/hypermarkets, online stores, specialty stores, and retail stores. Online stores have witnessed a significant surge in market share recently due to the convenience they offer to consumers and the growing penetration of e-commerce platforms like Amazon and Flipkart. The availability of a wide variety of products, coupled with discounts and fast delivery options, has made online shopping a popular choice. Additionally, the pandemic-induced shift to online shopping has further cemented this channel's dominance in the market.

The India dry fruits market is dominated by both local and international players, each striving to gain a competitive edge through product innovation, brand positioning, and distribution expansion. The market is relatively fragmented, with both premium and budget segments competing for consumer attention. Some of the key players in the market include:

|

Company Name |

Establishment Year |

Headquarters |

Revenue (INR Bn) |

No. of Employees |

Product Range |

Distribution Network |

Market Share (%) |

R&D Investments |

Geographical Presence |

|

Haldirams |

1937 |

Nagpur, India |

- | - | - | - | - | - | - |

|

Bikanervala Foods Pvt Ltd |

1950 |

Delhi, India |

- | - | - | - | - | - | - |

|

Sahyadri Farms |

2010 |

Nashik, India |

- | - | - | - | - | - | - |

|

Royal Dry Fruits Pvt Ltd |

1985 |

Mumbai, India |

- | - | - | - | - | - | - |

|

Vijayalakshmi Cashew Company |

1957 |

Karnataka, India |

- | - | - | - | - | - | - |

Over the next five years, the India dry fruits market is expected to show significant growth driven by rising health awareness, increased demand for ready-to-eat snacks, and the penetration of online retail platforms. Consumers are increasingly opting for healthy snack options, such as dry fruits, which offer high nutritional value, leading to a steady rise in their consumption. Additionally, the growing preference for plant-based and organic food products will continue to shape the market dynamics.

|

By Product Type |

Almonds Cashews Walnuts Raisins Pistachios |

|

By Form |

Whole Powdered Sliced Flavored |

|

By Distribution Channel |

Supermarkets/Hypermarkets Online Stores Specialty Stores Retail Stores |

|

By End-User |

Household Consumers Food & Beverage Industry Foodservice Industry Nutraceuticals |

|

By Region |

North South West East |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Health Consciousness (Increase in Demand for Nutrient-Rich Foods)

3.1.2. Expansion of Retail Chains (Growth of E-Commerce and Organized Retail)

3.1.3. Favorable Government Policies (Agri Export Policies)

3.1.4. Seasonal Festivities and Gifting Trends (Increase in Seasonal Consumption)

3.2. Market Challenges

3.2.1. Fluctuating Prices of Raw Materials (Volatile Commodity Prices)

3.2.2. High Dependence on Imports (Supply Chain Disruptions)

3.2.3. Lack of Cold Storage Infrastructure (Storage and Preservation Issues)

3.3. Opportunities

3.3.1. Growth in Healthy Snacks Segment (Increased Consumer Focus on Healthy Snacking)

3.3.2. Expanding Urbanization (Rising Disposable Income in Urban Areas)

3.3.3. Product Innovation (Introduction of Value-Added Dry Fruits Products)

3.4. Trends

3.4.1. Shift Towards Organic Products (Demand for Chemical-Free Dry Fruits)

3.4.2. Sustainable Packaging (Eco-Friendly Packaging Solutions)

3.4.3. Premiumization of Products (High-Quality Packaging and Branding)

3.5. Government Regulation

3.5.1. Agricultural Produce Market Committee (APMC) Regulations

3.5.2. FSSAI Standards (Food Safety and Standards Authority of India)

3.5.3. Import Tariff Policies

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.7.1. Farmers and Suppliers

3.7.2. Distributors and Wholesalers

3.7.3. Retailers

3.7.4. Exporters

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Almonds

4.1.2. Cashews

4.1.3. Walnuts

4.1.4. Raisins

4.1.5. Pistachios

4.2. By Form (In Value %)

4.2.1. Whole

4.2.2. Powdered

4.2.3. Sliced

4.2.4. Flavored

4.3. By Distribution Channel (In Value %)

4.3.1. Supermarkets/Hypermarkets

4.3.2. Online Stores

4.3.3. Specialty Stores

4.3.4. Retail Stores

4.4. By End-User (In Value %)

4.4.1. Household Consumers

4.4.2. Food & Beverage Industry

4.4.3. Foodservice Industry

4.4.4. Nutraceuticals

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. West India

4.5.4. East India

5.1. Detailed Profiles of Major Companies

5.1.1. Haldirams

5.1.2. Bikanervala Foods Pvt Ltd

5.1.3. Vijayalakshmi Cashew Company

5.1.4. Agrocel Industries Pvt Ltd

5.1.5. Sahyadri Farms

5.1.6. Royal Dry Fruits Pvt Ltd

5.1.7. Adani Wilmar

5.1.8. Reliance Fresh

5.1.9. Patanjali Ayurved Ltd

5.1.10. Jabs International Pvt Ltd

5.1.11. Gujarat Cooperative Milk Marketing Federation Ltd (GCMMF)

5.1.12. Badamwala Dry Fruits

5.1.13. Baidyanath Ayurved Bhawan Pvt Ltd

5.1.14. Amazon India (Private Label)

5.1.15. TATA Sampann

5.2. Cross Comparison Parameters

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity Investments

6.1. FSSAI Guidelines

6.2. Import and Export Regulations

6.3. Labeling and Packaging Standards

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Form (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. Market Penetration Strategies

9.2. Customer Segmentation Analysis

9.3. Innovation and Product Development

9.4. Geographic Expansion Opportunities

In the first phase, an ecosystem map of the India dry fruits market was constructed, focusing on major stakeholders such as manufacturers, distributors, and consumers. Desk research was used to gather comprehensive industry-level information, identifying critical variables that influence market dynamics such as price fluctuations, supply chains, and consumer preferences.

The second phase involved analyzing historical market data, including production volumes, distribution channels, and revenue generated. Market penetration was assessed, along with the ratio of domestic to imported dry fruits. This analysis provided an accurate overview of market performance and key growth drivers.

Key market hypotheses were validated through interviews with industry experts and stakeholders, ensuring that data collected from secondary sources was accurate and reflective of real market conditions. These consultations helped refine revenue estimates and highlighted emerging trends in product innovation and consumer preferences.

Finally, direct engagement with manufacturers and distributors was conducted to obtain detailed insights into the performance of different product segments. This information was used to finalize the report, ensuring a holistic and validated analysis of the India dry fruits market.

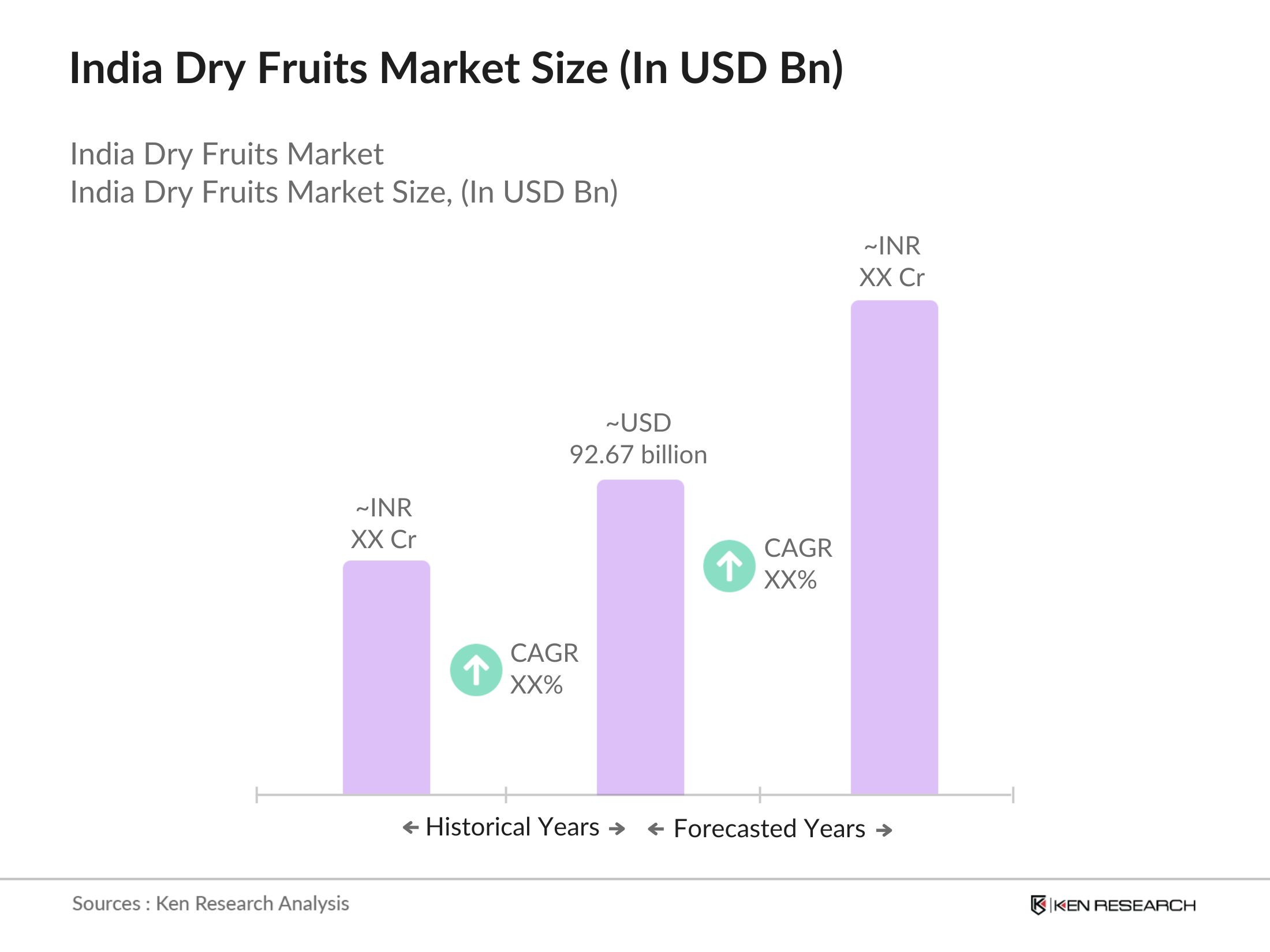

The India dry fruits market is valued at USD 92.67 billion, driven by rising consumer health awareness and increasing demand for nutrient-dense snack options.

Challenges in the India dry fruits market include fluctuating raw material prices due to dependence on imports, inadequate cold storage infrastructure, and volatility in supply chains that can disrupt market stability.

Key players in the India dry fruits market include Haldiram’s, Bikanervala Foods Pvt Ltd, Royal Dry Fruits Pvt Ltd, and Sahyadri Farms, which dominate through their expansive distribution networks and strong brand presence.

Key players in the India dry fruits market include Haldiram’s, Bikanervala Foods Pvt Ltd, Royal Dry Fruits Pvt Ltd, and Sahyadri Farms, which dominate through their expansive distribution networks and strong brand presence.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.