India E-learning Market Outlook to FY 2030

India E-learning Market: Growth Drivers, Segmentation, and Future Outlook to 2030

Region:India

Author(s):Harsh Saxena

Product Code:KR74

Region:India

Author(s):Harsh Saxena

Product Code:KR74

August 2013

60

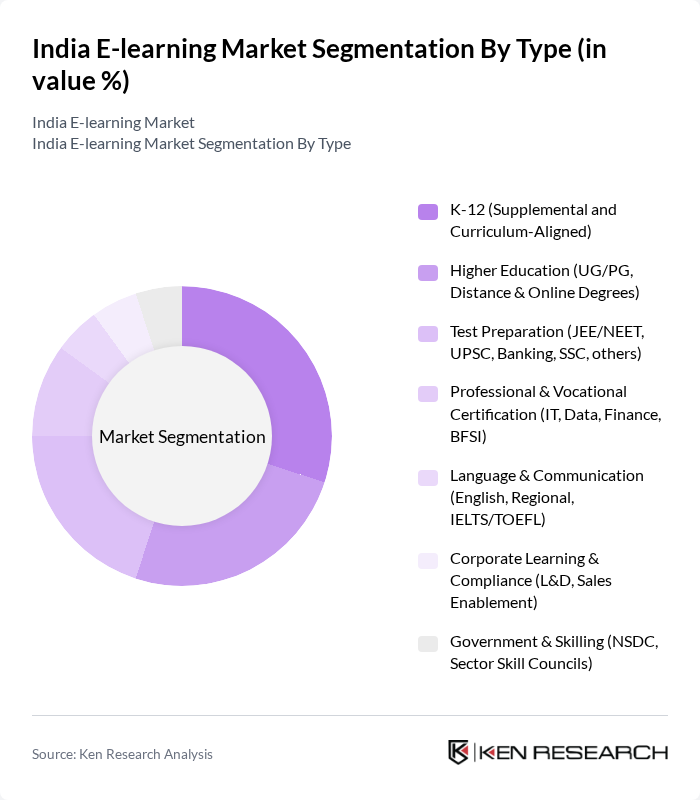

By Type: The e-learning market can be segmented into various types, including K-12, Higher Education, Test Preparation, Professional & Vocational Certification, Language & Communication, Corporate Learning & Compliance, and Government & Skilling. Among these, the K-12 segment is witnessing significant growth due to the increasing adoption of digital learning tools in schools, while the Test Preparation segment is also thriving, driven by the competitive nature of entrance exams in India. Recent trends include rapid growth of mobile e-learning, dominance of content providers, and strong academic demand, aligning with the K-12 and test-prep momentum.

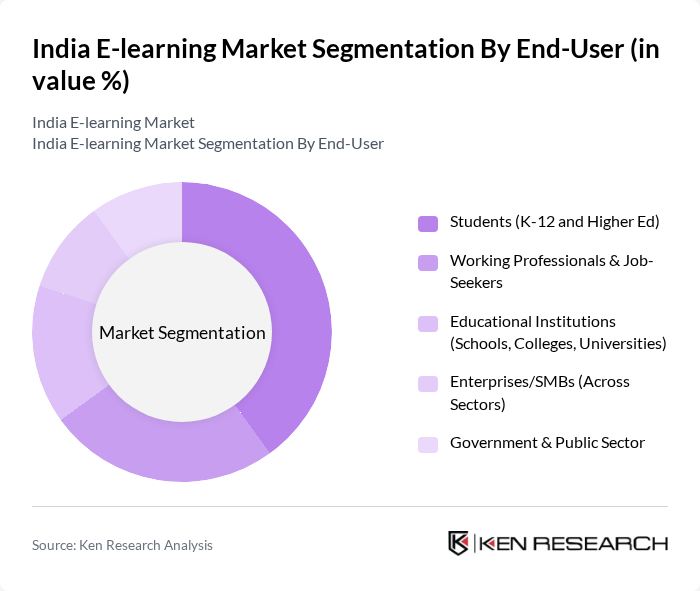

By End-User: The end-user segmentation includes Students, Working Professionals & Job-Seekers, Educational Institutions, Enterprises/SMBs, and Government & Public Sector. The student segment, particularly K-12 and higher education students, is the largest consumer of e-learning services, driven by the need for supplementary learning resources and exam preparation tools. Strong mobile-first usage and academic dominance support the student-heavy mix, while corporate training continues to expand through online programs.

The India E-learning Market is characterized by a dynamic mix of regional and international players. Leading participants such as BYJU'S, Unacademy, Vedantu, upGrad, Simplilearn, NIIT Ltd, Coursera, edX, Great Learning, PhysicsWallah (PW), Khan Academy, Allen Digital, NextEducation India Pvt. Ltd., TalentSprint, Eruditus (Emeritus India) contribute to innovation, geographic expansion, and service delivery in this space.

| BYJU'S | 2011 | Bengaluru, India | – | – | – | – | – | – |

| Unacademy | 2015 | Bengaluru, India | – | – | – | – | – | – |

| Vedantu | 2011 | Bengaluru, India | – | – | – | – | – | – |

| upGrad | 2015 | Mumbai, India | – | – | – | – | – | – |

| Simplilearn | 2010 | Bengaluru, India | – | – | – | – | – | – |

| Company | Establishment Year | Headquarters | Scale Tier (Unicorn/Large, Mid, Emerging) | Monthly Active Users (MAUs) / Enrolled Learners | Paid Subscribers / Conversion Rate (Free-to-Paid) | Course Completion Rate | Customer Acquisition Cost (CAC) | Customer Lifetime Value (LTV) and LTV:CAC |

|---|

Additional validated insights and trends - Mobile e-learning exhibits clear dominance as a delivery mode, reflecting India’s mobile-first usage patterns and low-cost data access. - Content providers represent the largest share among providers, underscoring the importance of localized, exam-aligned, and skills-focused content libraries. - Academic applications account for the majority share versus corporate and government, consistent with strong adoption across K-12, test prep, and higher education.

The future of the India e-learning market appears promising, driven by technological advancements and evolving educational needs. The integration of artificial intelligence and machine learning is expected to enhance personalized learning experiences, making education more accessible and effective. Additionally, the shift towards hybrid learning models, combining online and offline methods, will cater to diverse learning preferences. As government support continues, the market is poised for significant growth, fostering innovation and expanding access to quality education across the country.

| By Type |

K-12 (Supplemental and Curriculum-Aligned) Higher Education (UG/PG, Distance & Online Degrees) Test Preparation (JEE/NEET, UPSC, Banking, SSC, others) Professional & Vocational Certification (IT, Data, Finance, BFSI) Language & Communication (English, Regional, IELTS/TOEFL) Corporate Learning & Compliance (L&D, Sales Enablement) Government & Skilling (NSDC, Sector Skill Councils) |

| By End-User |

Students (K-12 and Higher Ed) Working Professionals & Job-Seekers Educational Institutions (Schools, Colleges, Universities) Enterprises/SMBs (Across Sectors) Government & Public Sector |

| By Region |

North India South India East India West & Central India |

| By Application |

Online E-learning (Self-paced, Instructor-led) Mobile E-learning (Apps, Offline Access) Virtual/Classroom & Live Learning (Webinars, Live Classes) Learning Management Systems (LMS/LXP) Rapid E-learning & Microlearning Assessment, Proctoring & Analytics |

| By Investment Source |

Domestic Investment Foreign Direct Investment (FDI) Public-Private Partnerships (PPP) Government Schemes (DIKSHA, SWAYAM, PMKVY, eVidya) |

| By Policy Support |

NEP 2020 & UGC Online/ODL Guidelines Data Protection & EdTech Self-Regulation (DPDP Act, ASCI) Grants for Research, Digital Infrastructure & Teacher Training |

| By Pricing Strategy |

Subscription (B2C/B2B SaaS) Pay-Per-Course / Cohort-Based Freemium & Ad-Supported Bundled/Pathways & Degree Partnerships |

E-learning, Virtual Classroom, E-Learning Softwares, Hardwares and Technologies, Technology, Content, ICT, Education, Content Authoring Tools

| Scope Item/Segment | Sample Size | Target Respondent Profiles |

|---|---|---|

| K-12 E-learning Platforms | 120 | Teachers, School Administrators, Parents |

| Higher Education Online Courses | 100 | University Professors, Students, Course Coordinators |

| Corporate Training Solutions | 80 | HR Managers, Training Coordinators, Employees |

| EdTech Startups | 70 | Founders, Product Managers, Investors |

| Government E-learning Initiatives | 60 | Policy Makers, Educational Planners, NGO Representatives |

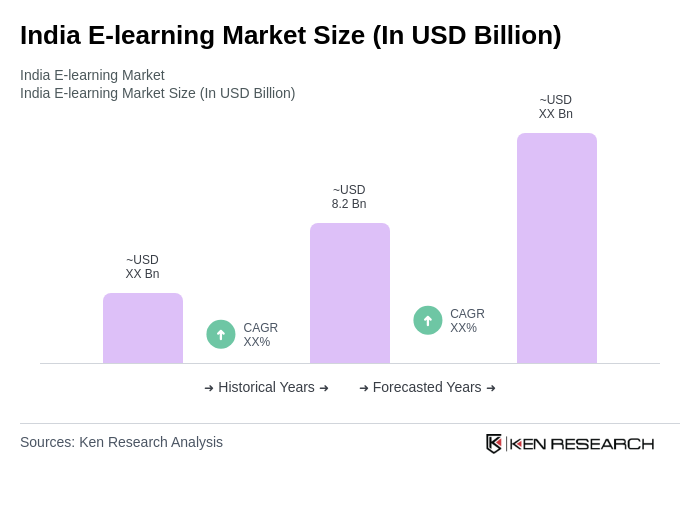

The India E-learning Market is valued at approximately USD 8.2 billion, reflecting significant growth driven by increased internet penetration, smartphone usage, and the demand for flexible learning options across various educational segments.

Key growth drivers include increasing internet penetration, rising demand for skill development, and substantial government initiatives aimed at enhancing digital education through policies like the National Education Policy (NEP) 2020.

Metropolitan areas such as Bengaluru, Delhi, and Mumbai lead the India E-learning Market due to their robust technology ecosystems and high concentrations of educational institutions, with South India currently holding the largest market share.

The market is segmented into K-12, Higher Education, Test Preparation, Professional & Vocational Certification, Language & Communication, Corporate Learning, and Government & Skilling, with K-12 and Test Preparation witnessing significant growth.

The pandemic accelerated the shift to online learning platforms as educational institutions transitioned to digital formats, significantly boosting the adoption of e-learning tools and services across academic and professional sectors.

Challenges include limited digital infrastructure in rural areas, high competition among numerous e-learning platforms, and resistance to change from traditional learning methods, which can hinder market growth and accessibility.

The Indian government supports the E-learning Market through substantial funding for digital education initiatives, such as the NEP 2020, and programs like SWAYAM and DIKSHA, which provide free access to quality educational resources.

The future of the India E-learning Market looks promising, with expected growth driven by technological advancements, the integration of AI for personalized learning, and a shift towards hybrid learning models that cater to diverse educational needs.

Key players include BYJU'S, Unacademy, Vedantu, upGrad, Simplilearn, and international platforms like Coursera and edX, all contributing to innovation and service delivery in the e-learning space.

Mobile e-learning is significant in India due to the country's mobile-first usage patterns and affordable data access, making it a preferred mode of learning for many users, especially in remote areas.

The E-learning Market is segmented by end-users into Students (K-12 and higher education), Working Professionals, Educational Institutions, Enterprises/SMBs, and Government/Public Sector, with students being the largest consumer group.

There is a growing opportunity for corporate training programs as companies increasingly recognize the value of continuous learning, with significant investments being made in online training modules to enhance employee skills and competencies.

Trends include the rise of gamification in learning, increased focus on microlearning, the shift towards hybrid learning models, and the use of data analytics to improve learning outcomes and user engagement.

The NEP 2020 emphasizes technology integration in education, promoting online learning and digital repositories, which enhances access and quality in K-12 and higher education, significantly impacting the E-learning landscape in India.

The pricing strategy in the E-learning Market varies, including subscription models, pay-per-course, freemium options, and bundled partnerships, which influence user engagement and accessibility to educational resources.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.