India Earphones and Headphones Market Outlook to 2030

Region:Asia

Author(s):Shubham Kashyap

Product Code:KROD4663

October 2024

94

About the Report

India Earphones and Headphones Market Overview

-

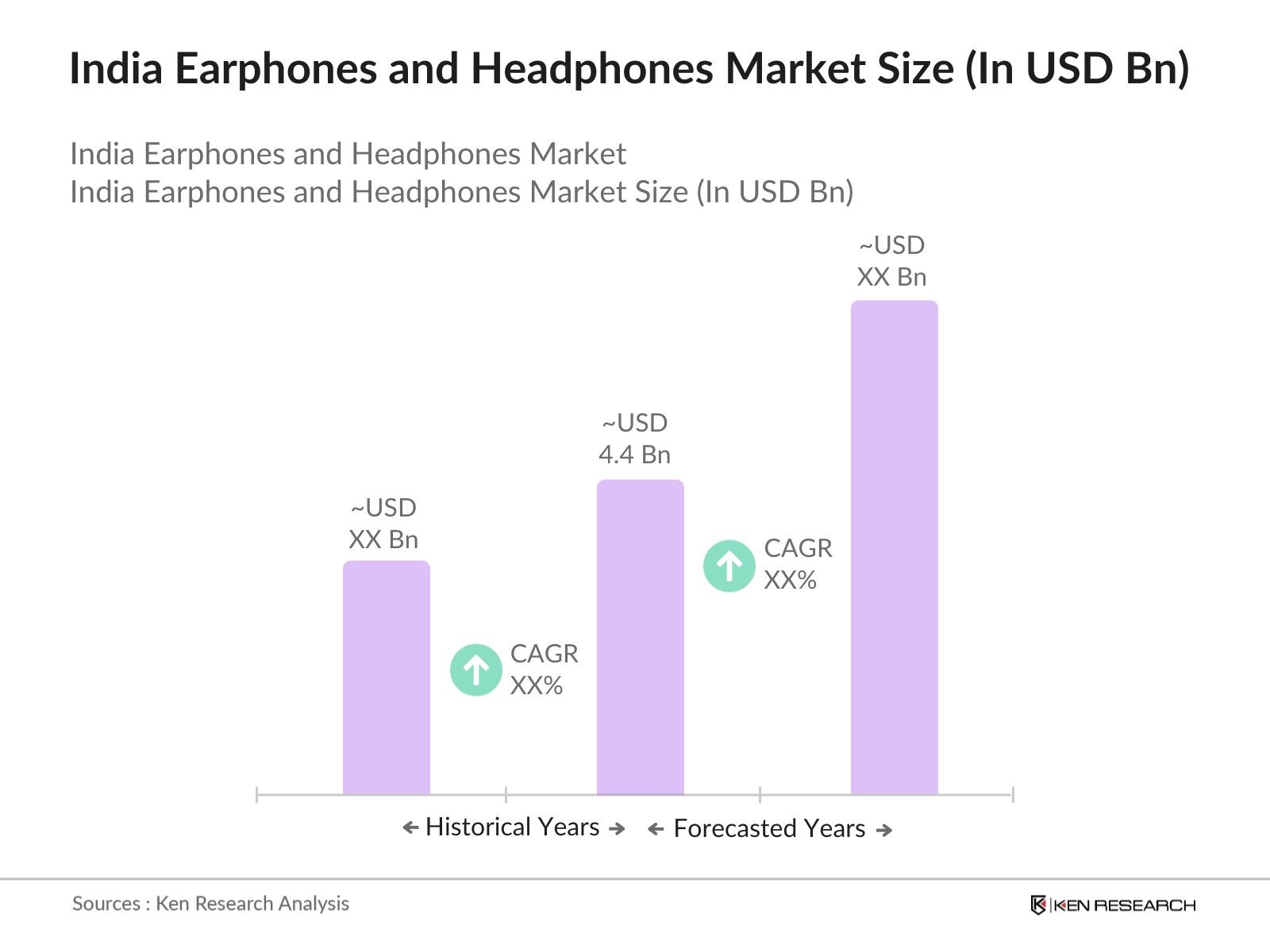

The India earphones and headphones market is valued at USD 4.4 billion, driven by the increasing demand for high-quality audio products, a growing base of smartphone users, and a shift towards wireless technology. The rise of mobile gaming, music streaming services, and virtual meetings are contributing significantly to this market's growth. Consumers are becoming more discerning about sound quality, noise cancellation, and ergonomic design, driving innovation in the sector.

-

Regions such as Delhi, Mumbai, Bangalore, and Hyderabad are leading the demand for premium earphones and headphones due to higher disposable income and tech-savvy consumers. The proliferation of online platforms, discounts, and product reviews has made it easier for consumers to compare and purchase audio devices. Additionally, the growing adoption of true wireless stereo (TWS) earbuds and Bluetooth headphones has been fueled by the reduction in prices and advancements in Bluetooth technology.

-

The Indian market is also benefiting from the presence of numerous global and local brands offering a wide range of products catering to different consumer segments. Brands like boAt, JBL, Sony, and OnePlus are continuously innovating with new designs and features, targeting the millennial and Gen Z demographics. The market’s growth is further supported by the rise of audio content consumption such as podcasts, audiobooks, and streaming media.

India Earphones and Headphones Market Segmentation

-

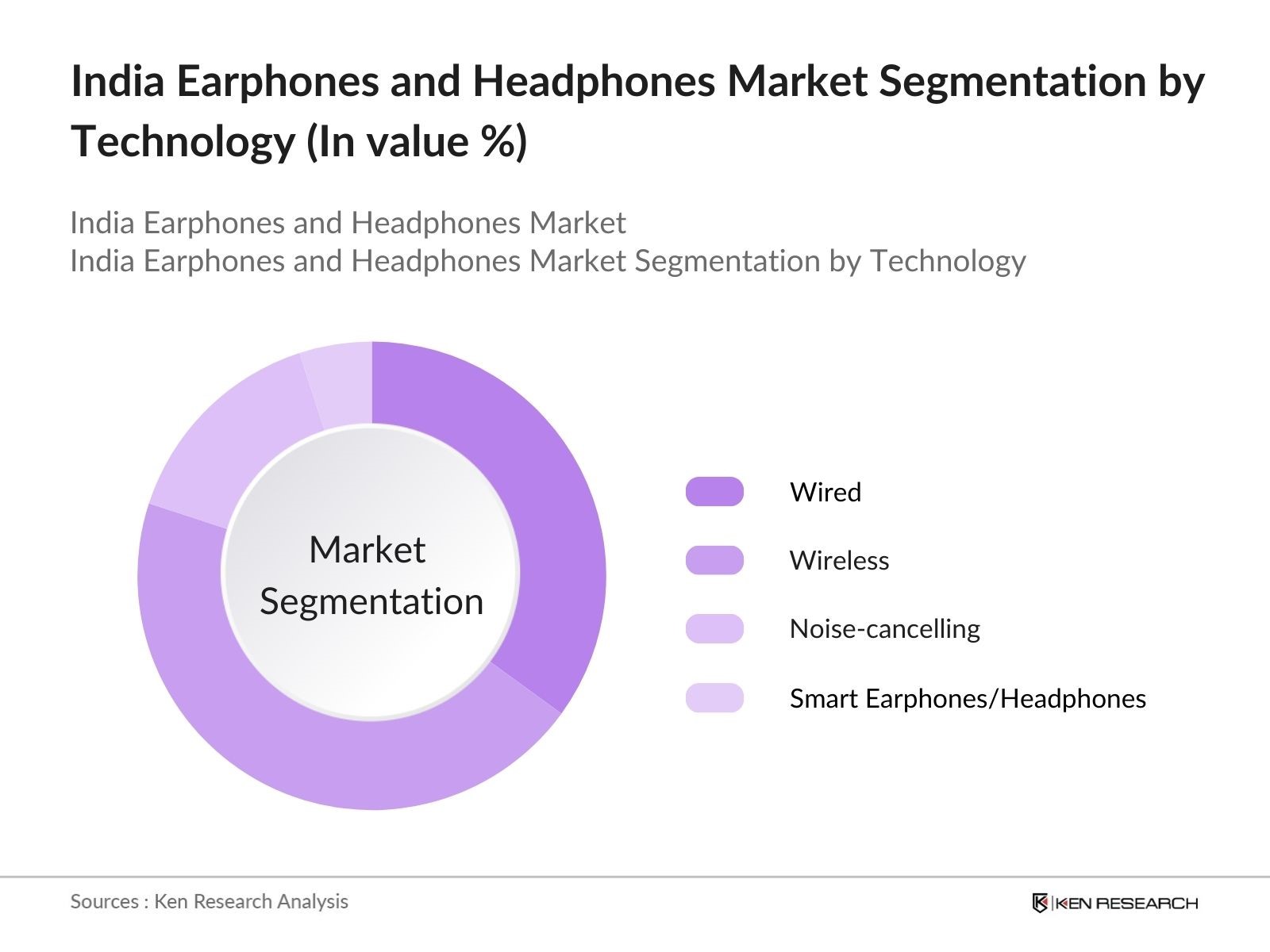

By Technology: The market is segmented by technology into Wired, Wireless, Noise-cancelling, and Smart Earphones/Headphones. Wireless earphones and headphones dominate the market due to the growing preference for cable-free convenience, especially among fitness enthusiasts and commuters. Noise-cancelling technology is increasingly popular, particularly in urban areas, where consumers seek devices that block out ambient noise during commutes or remote work.

-

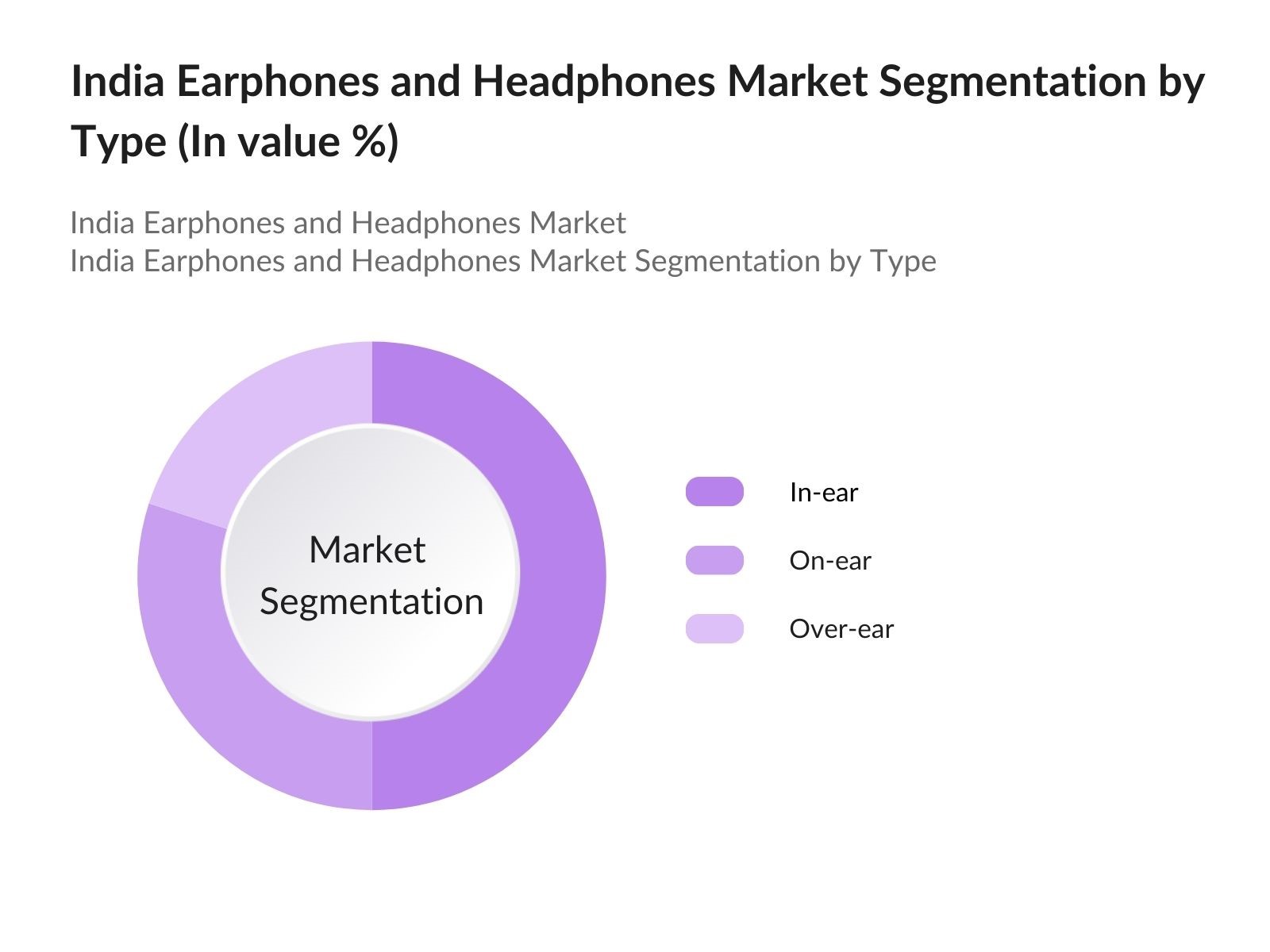

By Type: The market is segmented by type into In-ear, On-ear, and Over-ear headphones. In-ear headphones lead the market due to their portability, affordability, and versatility. On-ear and over-ear headphones are gaining traction among audiophiles and gamers who prioritize sound quality and comfort over portability. These segments are particularly popular among music producers, content creators, and gamers.

India Earphones and Headphones Market Competitive Landscape

The earphones and headphones market in India is highly competitive, with numerous global and local players competing for market share. Key companies such as boAt, JBL, Sony, and Realme are introducing new models with advanced features like active noise cancellation, voice assistants, and improved battery life to cater to different consumer needs. Local brands are also gaining traction by offering affordable options tailored to the Indian consumer base.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD) |

Product Portfolio |

Market Presence |

R&D Investment |

|

boAt |

2016 |

India |

- |

- |

- |

- |

|

JBL |

1946 |

USA |

- |

- |

- |

- |

|

Sony |

1946 |

Japan |

- |

- |

- |

- |

|

Realme |

2018 |

China |

- |

- |

- |

- |

|

Apple |

1976 |

USA |

- |

- |

- |

- |

India Earphones and Headphones Industry Analysis

Growth Drivers

-

Increasing Smartphone Penetration: The rapid increase in smartphone penetration is a significant driver for the earphones and headphones market in India. As of 2023, India has 931 million smartphone users, with projections suggesting this number could reach around 1.1 billion by 2025. This surge is projected to create a substantial demand for audio accessories as consumers increasingly rely on smartphones for media consumption, gaming, and communication. The expanding smartphone user base is expected to enhance audio device adoption, driving overall market growth as users seek compatible audio solutions to enhance their mobile experience.

-

Rising Demand for Wireless Audio Devices: The demand for wireless audio devices has witnessed a notable increase, driven by changing consumer preferences towards convenience and mobility. In 2023, the share of wireless audio devices in the overall audio market reached all-time high. This trend is fueled by advancements in Bluetooth technology and the growing popularity of True Wireless Stereo (TWS) headphones. The convenience of untethered listening experiences aligns with the on-the-go lifestyles of modern consumers, reinforcing the shift towards wireless audio solutions in the Indian market.

-

Popularity of Music Streaming and Online Entertainment: The popularity of music streaming services is a significant growth driver in the earphones and headphones market. In 2023, India recorded over 11 million music streaming subscribers, a significant rise from million in 2022. This surge can be attributed to the increased availability of affordable data plans, with mobile data usage reaching 22.8 GB per month per user in urban areas. The growing engagement with online entertainment platforms further elevates the demand for high-quality audio devices, as consumers seek to enhance their listening experience while accessing a wide array of content.

Market Challenges

-

Price Sensitivity of Indian Consumers: Price sensitivity remains a formidable challenge in the Indian earphones and headphones market. A substantial portion of the Indian population, particularly in semi-urban and rural areas, is cautious about spending on non-essential items. Many consumers lean towards affordable audio solutions, which restricts the growth potential of premium brands. This sensitivity impacts market penetration strategies, as brands must carefully balance quality with affordability to attract cost-conscious consumers. Consequently, companies may need to implement strategic pricing and marketing approaches to effectively engage with this price-sensitive demographic.

-

Counterfeit Products and Market Competition: The presence of counterfeit products poses a significant challenge to the legitimate earphones and headphones market in India. The counterfeit audio device market undermines the sales of authentic brands and affects overall industry growth. The proliferation of online marketplaces has facilitated the availability of counterfeit goods, leading to intense competition among legitimate brands. As a result, companies are compelled to invest in marketing and anti-counterfeit measures to safeguard their market share, which can impact their profitability and long-term sustainability in the Indian market. This situation necessitates robust strategies to combat counterfeiting and maintain brand integrity.

India Earphones and Headphones Market Future Outlook

The India earphones and headphones market is expected to grow robustly over the next five years, fueled by the increasing adoption of wireless technology, the rise of mobile gaming, and the growing demand for high-quality audio experiences. The trend toward working from home and the expansion of online learning platforms will also drive the market's growth, as more consumers invest in audio devices for personal and professional use.

Future Market Opportunities

- Expansion of Premium and Smart Audio Products: The current market presents significant opportunities for the expansion of premium and smart audio products. As of 2023, the market for premium audio devices is projected to witness a steady growth trajectory, driven by consumer interest in innovative features. The rise of smart home devices, coupled with advancements in audio technology, creates a favorable environment for brands to introduce high-end audio solutions with enhanced functionalities, such as voice control and integration with smart ecosystems. This trend is expected to attract tech-savvy consumers seeking premium audio experiences.

- Integration of Smart Features like Voice Assistants: The integration of smart features such as voice assistants in audio devices is becoming a lucrative opportunity in the Indian market. By 2023, over 30 million smart speakers have been sold in India, indicating a growing preference for devices with voice recognition capabilities. The incorporation of voice assistants in earphones and headphones not only enhances user experience but also aligns with the increasing demand for smart home technologies. Manufacturers can leverage this trend to create innovative audio solutions that cater to the evolving preferences of consumers seeking seamless connectivity and hands-free operation.

Scope of the Report

| By Currency Type |

Bitcoin Ethereum Ripple Stablecoins |

|

By Application |

Peer-to-Peer Transactions Remittances Investments E-commerce Payments |

| By Platform Type |

Exchange Platforms Wallet Platforms Decentralized Finance Platforms |

|

By Regio |

Riyadh Jeddah Eastern Province |

|

By End User |

Retail Investors Institutional Investors Government Entities |

Products

Key Target Audience

- Retail and E-commerce Platforms

- Audio Equipment Distributors

- Consumer Electronics Retailers

- Investments and Venture Capitalist Firms

- Banks and Financial Institutions

- Government and Regulatory Bodies (Department of Consumer Affairs, Ministry of Electronics and Information Technology)

Companies

Major Players in the Market

- boAt

- JBL

- Sony

- Realme

- Apple

- Sennheiser

- Philips

- Noise

- Xiaomi (Mi)

- Skullcandy

- Bose

- OnePlus

- Oppo

- Corsair

- Boult Audio

Table of Contents

1. India Earphones and Headphones Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Growth Rate and Market Dynamics

1.4. Overview of Market Segmentation

2. India Earphones and Headphones Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Technological Advancements

3. India Earphones and Headphones Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Smartphone Penetration

3.1.2. Rising Demand for Wireless Audio Devices

3.1.3. Popularity of Music Streaming and Online Entertainment

3.1.4. Evolving Consumer Preferences for High-Quality Audio

3.2. Market Challenges

3.2.1. Price Sensitivity of Indian Consumers

3.2.2. Counterfeit Products and Market Competition

3.2.3. High Dependence on Imports for Components

3.3. Opportunities

3.3.1. Expansion of Premium and Smart Audio Products

3.3.2. Integration of Smart Features like Voice Assistants

3.3.3. Emergence of Local Manufacturing and Assembly

3.4. Market Trends

3.4.1. Shift Towards True Wireless Stereo (TWS) Devices

3.4.2. Growth of Gaming and Fitness-Focused Audio Solutions

3.4.3. Demand for Personalized and Customizable Sound Experiences

3.5. Regulatory Environment

3.5.1. Government Initiatives Supporting Consumer Electronics Manufacturing

3.5.2. Import Regulations and Trade Tariffs

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porter’s Five Forces Analysis

3.9. Competition Landscape

4. India Earphones and Headphones Market Segmentation

4.1. By Technology (In Value %)

4.1.1. Wired

4.1.2. Wireless

4.1.3. Noise-cancelling

4.1.4. Smart Earphones/Headphones

4.2. By Type (In Value %)

4.2.1. In-ear

4.2.2. On-ear

4.2.3. Over-ear

4.3. By Price Range (In Value %)

4.3.1. Budget

4.3.2. Mid-range

4.3.3. Premium

4.4. By Distribution Channel (In Value %)

4.4.1. Online

4.4.2. Offline

4.5. By Application (In Value %)

4.5.1. Music & Entertainment

4.5.2. Sports & Fitness

4.5.3. Gaming

5. India Earphones and Headphones Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. boAt

5.1.2. JBL

5.1.3. Sony

5.1.4. Realme

5.1.5. OnePlus

5.1.6. Samsung

5.1.7. Apple

5.1.8. Sennheiser

5.1.9. Philips

5.1.10. Noise

5.1.11. Mi (Xiaomi)

5.1.12. Skullcandy

5.1.13. Oppo

5.1.14. Boult Audio

5.1.15. Zebronics

5.2. Cross Comparison Parameters (Revenue, Headquarters, Product Portfolio, Market Share, Employee Strength, R&D Investments, Key Partnerships, Technological Differentiation)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Trends

5.7. Private Equity and Venture Capital Funding

5.8. Government Support and Grants

6. India Earphones and Headphones Market Regulatory Framework

6.1. Consumer Electronics Regulations

6.2. Compliance with Health and Safety Standards

6.3. Import and Export Regulations

6.4. Tariff and Trade Barriers

7. India Earphones and Headphones Future Market Size (In USD Bn)

7.1. Future Market Projections

7.2. Key Factors Driving Future Growth

8. India Earphones and Headphones Future Market Segmentation

8.1. By Technology (In Value %)

8.2. By Type (In Value %)

8.3. By Price Range (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Application (In Value %)

9. India Earphones and Headphones Market Analyst’s Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Behavior and Market Penetration Strategies

9.3. Product Differentiation Strategies

9.4. Competitive Positioning and White Space Opportunities

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the India earphones and headphones market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the India earphones and headphones market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the India earphones and headphones market.

Frequently Asked Questions

How big is the India Earphones and Headphones Market?

The India earphones and headphones market is valued at USD 4.4 billion, driven by an increasing demand for high-quality audio experiences and the proliferation of mobile devices.

What are the challenges in the India Earphones and Headphones Market?

Challenges in the India earphones and headphones market include high competition among brands, regulatory hurdles, and the counterfeit products market. Additionally, the increasing cost of components poses a threat to market profitability.

Who are the major players in the India Earphones and Headphones Market?

Key players in the India earphones and headphones market include boAt, JBL, Sony, Realme, and Apple. These companies dominate due to their extensive distribution networks, strong brand presence, and diverse product portfolios.

What are the growth drivers of the India Earphones and Headphones Market?

The India earphones and headphones market is propelled by factors such as increasing disposable incomes, advancements in audio technology, and growing consumer preferences for high-quality sound experiences.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.