India Electric Car Market Outlook to 2030

Region:Asia

Author(s):Paribhasha Tiwari

Product Code:KROD2796

Region:Asia

Author(s):Paribhasha Tiwari

Product Code:KROD2796

October 2024

96

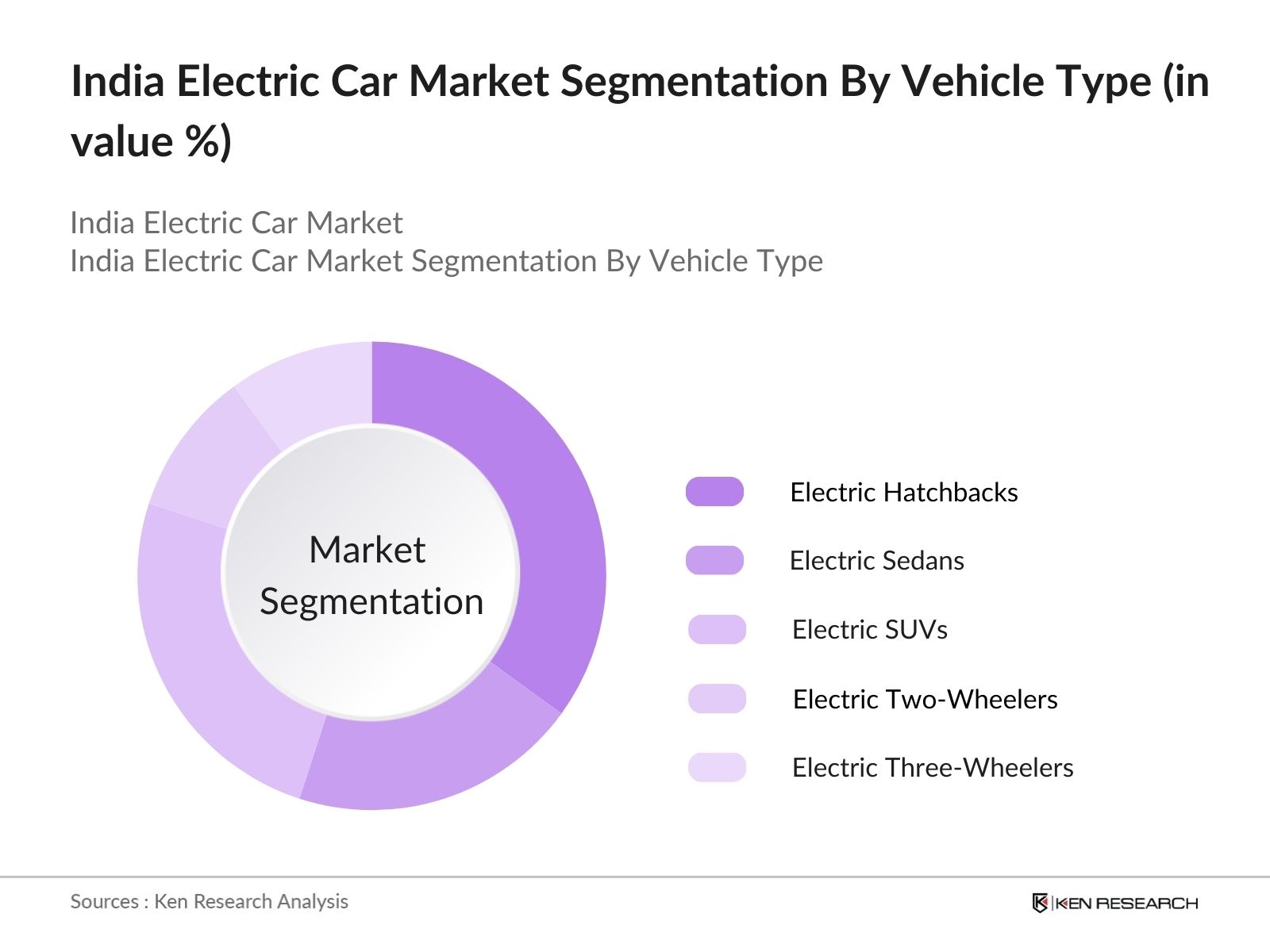

By Vehicle Type: The Indian electric car market is segmented by vehicle type into electric hatchbacks, electric sedans, electric SUVs, electric two-wheelers, and electric three-wheelers. Electric hatchbacks hold a dominant market share due to their affordability and compact size, making them ideal for city commutes. Popular models like the Tata Tigor EV have carved out a substantial market by offering a cost-effective solution for urban transportation, especially in densely populated metropolitan areas.

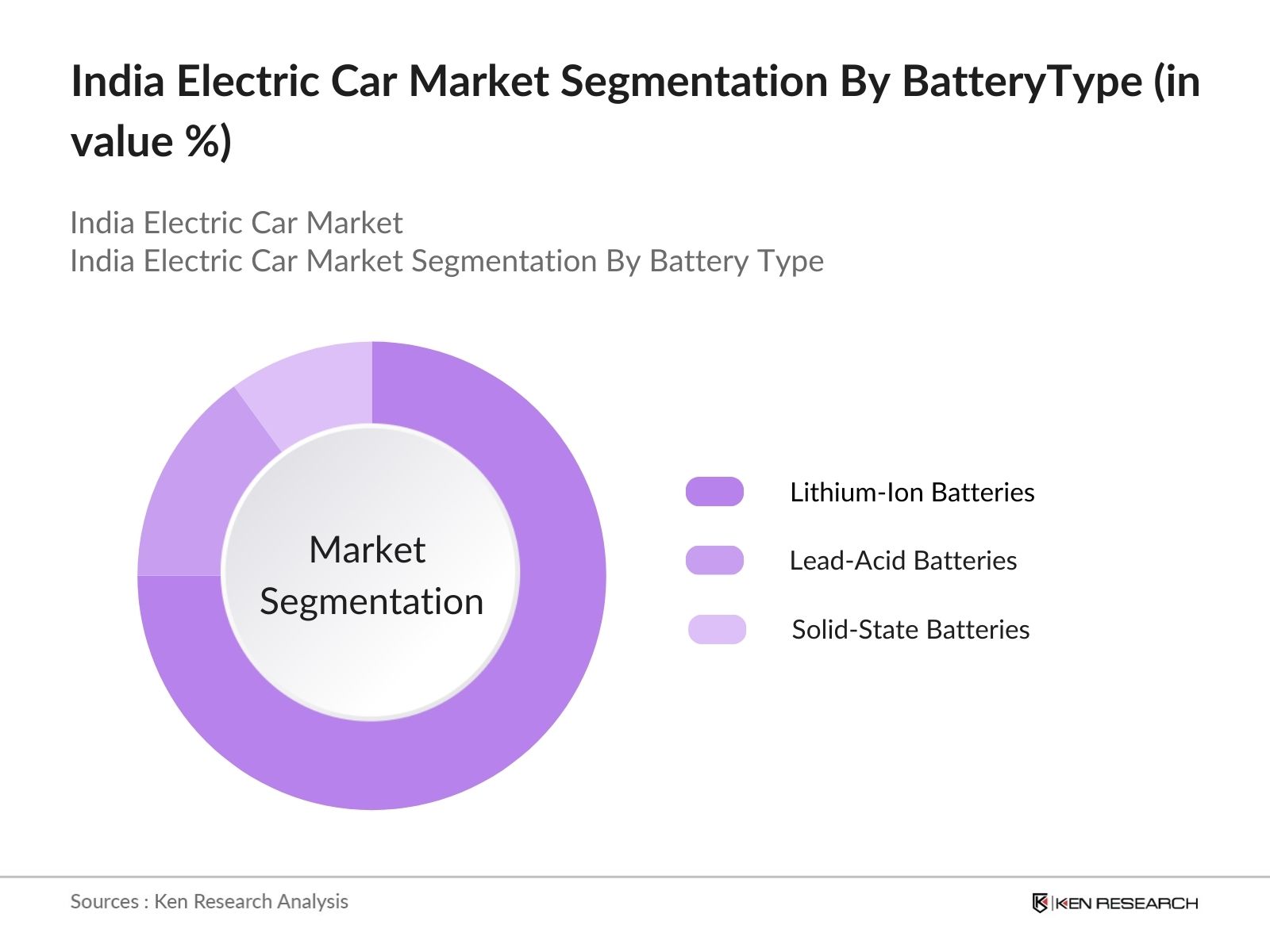

By Battery Type: The market is segmented by battery type into lithium-ion batteries, lead-acid batteries, and solid-state batteries. Lithium-ion batteries dominate the market, largely due to their superior energy density and longer life cycle compared to other battery types. With advancements in lithium-ion technology driving down costs and improving performance, they have become the go-to option for most electric vehicle manufacturers in India, including Tata Motors and Mahindra Electric.

The India electric car market is highly competitive, with a mix of domestic and international players contributing to the rapid growth. Tata Motors, Mahindra Electric, and Ather Energy are key domestic players, while international brands like Hyundai and Tesla have gained traction with premium electric vehicles. These companies continue to innovate in terms of battery technology, charging infrastructure, and vehicle design, contributing to their stronghold in the market.

|

Company Name |

Establishment Year |

Headquarters |

Vehicle Portfolio |

Battery Technology |

R&D Expenditure |

Sustainability Initiatives |

Market Strategy |

Production Capacity |

Company Name |

|

Tata Motors Ltd. |

1945 |

Mumbai, India |

|||||||

|

Mahindra Electric Mobility |

1945 |

Bengaluru, India |

|||||||

|

Hyundai Motor India Ltd. |

1996 |

Chennai, India |

|||||||

|

Ather Energy Pvt. Ltd. |

2013 |

Bengaluru, India |

|||||||

|

Tesla Inc. |

2003 |

Palo Alto, USA |

Over the next five years, the Indian electric car market is expected to show significant growth, driven by continuous government support, advancements in EV technology, and increasing consumer demand for eco-friendly transportation solutions. Initiatives like the FAME-II scheme, investments in charging infrastructure, and growing public awareness around climate change are likely to boost market expansion. Furthermore, the domestic manufacturing sectors focus on building cost-effective EV solutions will play a critical role in making electric cars accessible to the wider population.

|

Segment |

Sub-Segments |

|

By Vehicle Type |

Electric Hatchbacks Electric Sedans Electric SUVs Electric Two-Wheelers Electric Three-Wheelers |

|

By Battery Type |

Lithium-Ion Batteries Lead-Acid Batteries Solid-State Batteries |

|

By Charging Infrastructure |

Home Charging Public Charging Fast Charging Stations Battery Swapping Stations |

|

By Application |

Personal Use Commercial Use (Fleet, Taxi, Ride-Hailing) Government and Public Transport |

|

By Region |

North India South India East India West India |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Government EV Policies and Subsidies (FAME-II, State EV Policies)

3.1.2 Increasing Fuel Prices (Inflation-Linked Crude Oil Prices)

3.1.3 Consumer Shift Towards Sustainability (Environmental Awareness)

3.1.4 Rise in Domestic EV Manufacturing (PLI Scheme for Auto Industry)

3.2 Market Challenges

3.2.1 High Initial Purchase Cost (Price Parity with ICE Vehicles)

3.2.2 Underdeveloped Charging Infrastructure (Low Charging Station Penetration)

3.2.3 Range Anxiety (Limited Battery Capacity and Range)

3.2.4 Supply Chain Bottlenecks (Lithium-Ion Battery Sourcing)

3.3 Opportunities

3.3.1 Expansion of Charging Networks (Government-Private Collaborations)

3.3.2 Growth in EV Financing Options (Zero-Interest Loans, Leasing Models)

3.3.3 Integration of Renewable Energy in Charging Stations (Solar-Powered Charging)

3.3.4 Development of Battery Recycling Solutions (Circular Economy)

3.4 Trends

3.4.1 Rise in Electric Two-Wheelers and Three-Wheelers (Cost-Effective Urban Transport)

3.4.2 Introduction of New Battery Technologies (Solid-State, Fast-Charging Solutions)

3.4.3 Emergence of Connected EV Solutions (Telematics, IoT, Vehicle-to-Grid Technology)

3.4.4 Partnerships Between OEMs and Tech Companies (For AI, Autonomous Driving Integration)

3.5 Government Regulation

3.5.1 FAME-II (Faster Adoption and Manufacturing of Hybrid and EV Scheme)

3.5.2 State-Level EV Policies (Delhi, Maharashtra, Karnataka)

3.5.3 Corporate Average Fuel Efficiency (CAFE) Norms

3.5.4 National Electric Mobility Mission Plan (NEMMP)

3.6 SWOT Analysis

3.7 Stake Ecosystem (OEMs, Charging Infrastructure Providers, Government Bodies, Battery Suppliers)

3.8 Porter’s Five Forces

3.9 Competition Ecosystem

4.1 By Vehicle Type (In Value %)

4.1.1 Electric Hatchbacks

4.1.2 Electric Sedans

4.1.3 Electric SUVs

4.1.4 Electric Two-Wheelers

4.1.5 Electric Three-Wheelers

4.2 By Battery Type (In Value %)

4.2.1 Lithium-Ion Batteries

4.2.2 Lead-Acid Batteries

4.2.3 Solid-State Batteries

4.3 By Charging Infrastructure (In Value %)

4.3.1 Home Charging

4.3.2 Public Charging

4.3.3 Fast Charging Stations

4.3.4 Battery Swapping Stations

4.4 By Application (In Value %)

4.4.1 Personal Use

4.4.2 Commercial Use (Fleet, Taxi, Ride-Hailing)

4.4.3 Government and Public Transport

4.5 By Region (In Value %)

4.5.1 North India

4.5.2 South India

4.5.3 East India

4.5.4 West India

5.1 Detailed Profiles of Major Companies

5.1.1 Tata Motors Ltd.

5.1.2 Mahindra Electric Mobility Ltd.

5.1.3 Hyundai Motor India Ltd.

5.1.4 MG Motor India Pvt. Ltd.

5.1.5 Tesla Inc.

5.1.6 Ashok Leyland Electric Vehicles

5.1.7 Hero Electric Vehicles Pvt. Ltd.

5.1.8 Ather Energy Pvt. Ltd.

5.1.9 Ola Electric Mobility Pvt. Ltd.

5.1.10 TVS Motor Company

5.1.11 Bajaj Auto Ltd.

5.1.12 Okinawa Autotech Pvt. Ltd.

5.1.13 JBM Auto Ltd.

5.1.14 Greaves Cotton Limited (Ampere Electric)

5.1.15 Revolt Motors

5.2 Cross Comparison Parameters (Market Share, Production Capacity, Battery Technology, Pricing Strategy, Customer Satisfaction Ratings, Sustainability Initiatives, R&D Expenditure, EV Model Portfolio)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Central and State EV Policies

6.2 Environmental Standards (BS-VI, Emission Norms)

6.3 Compliance Requirements for EV Manufacturing

6.4 Certification Processes for Electric Vehicles

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Vehicle Type (In Value %)

8.2 By Battery Type (In Value %)

8.3 By Charging Infrastructure (In Value %)

8.4 By Application (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

The first step in our research methodology was to identify key variables influencing the Indian Electric Car Market, including government policies, consumer trends, and battery technology developments. Extensive secondary research was conducted using proprietary databases, government reports, and industry publications.

We analyzed historical data and growth drivers specific to the electric car market, including the penetration of EVs in major cities, production capacity of manufacturers, and infrastructure support. This analysis also involved comparing EV adoption rates across various vehicle segments.

Our hypotheses, such as the potential for future EV growth in Tier-II cities, were validated through expert interviews with industry professionals from leading EV manufacturers, battery suppliers, and government agencies. Their input was invaluable in fine-tuning our market analysis.

The final phase synthesized all the data and insights gathered from the above steps, including expert consultations and secondary research. The output was validated through direct interactions with EV manufacturers to ensure accurate representation of market trends, vehicle types, and consumer preferences.

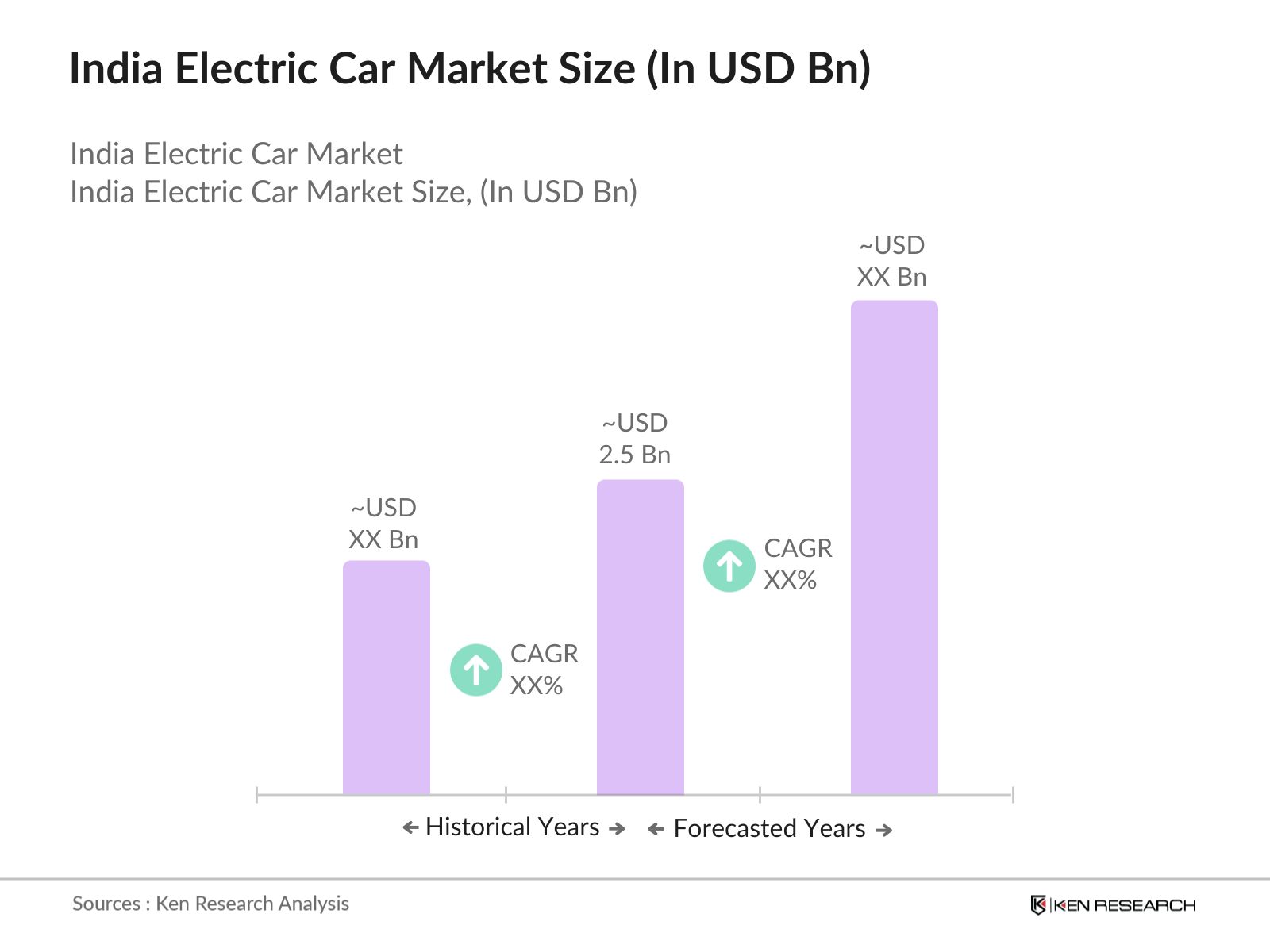

The India Electric Car Market was valued at USD 2.5 billion, driven by favorable government policies and the growing demand for sustainable transportation.

Challenges in the India Electric Car Market include underdeveloped charging infrastructure, high upfront costs, and supply chain issues related to lithium-ion batteries, which hinder market growth.

Key players in the India Electric Car Market include Tata Motors, Mahindra Electric, Hyundai, Ather Energy, and Tesla, all of which dominate through innovations in vehicle design, battery technology, and charging infrastructure.

Growth drivers in the India Electric Car Market include government incentives, rising fuel costs, and increased consumer awareness around the environmental impact of conventional vehicles, leading to higher EV adoption rates.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.