India Electric Two-Wheeler Market Outlook to 2030

Region:India

Author(s):Sanjeev

Product Code:KROD10126

Region:India

Author(s):Sanjeev

Product Code:KROD10126

November 2024

90

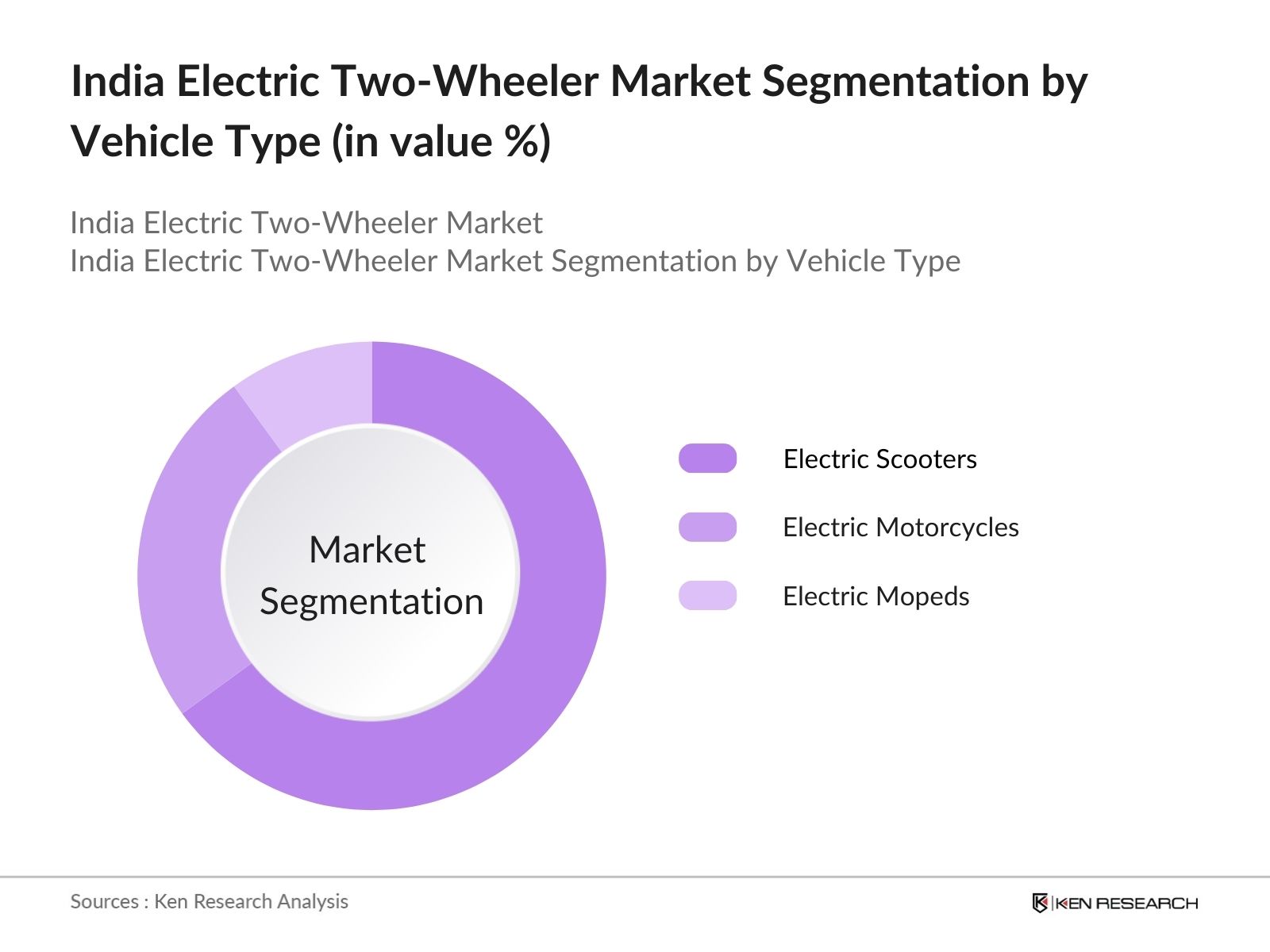

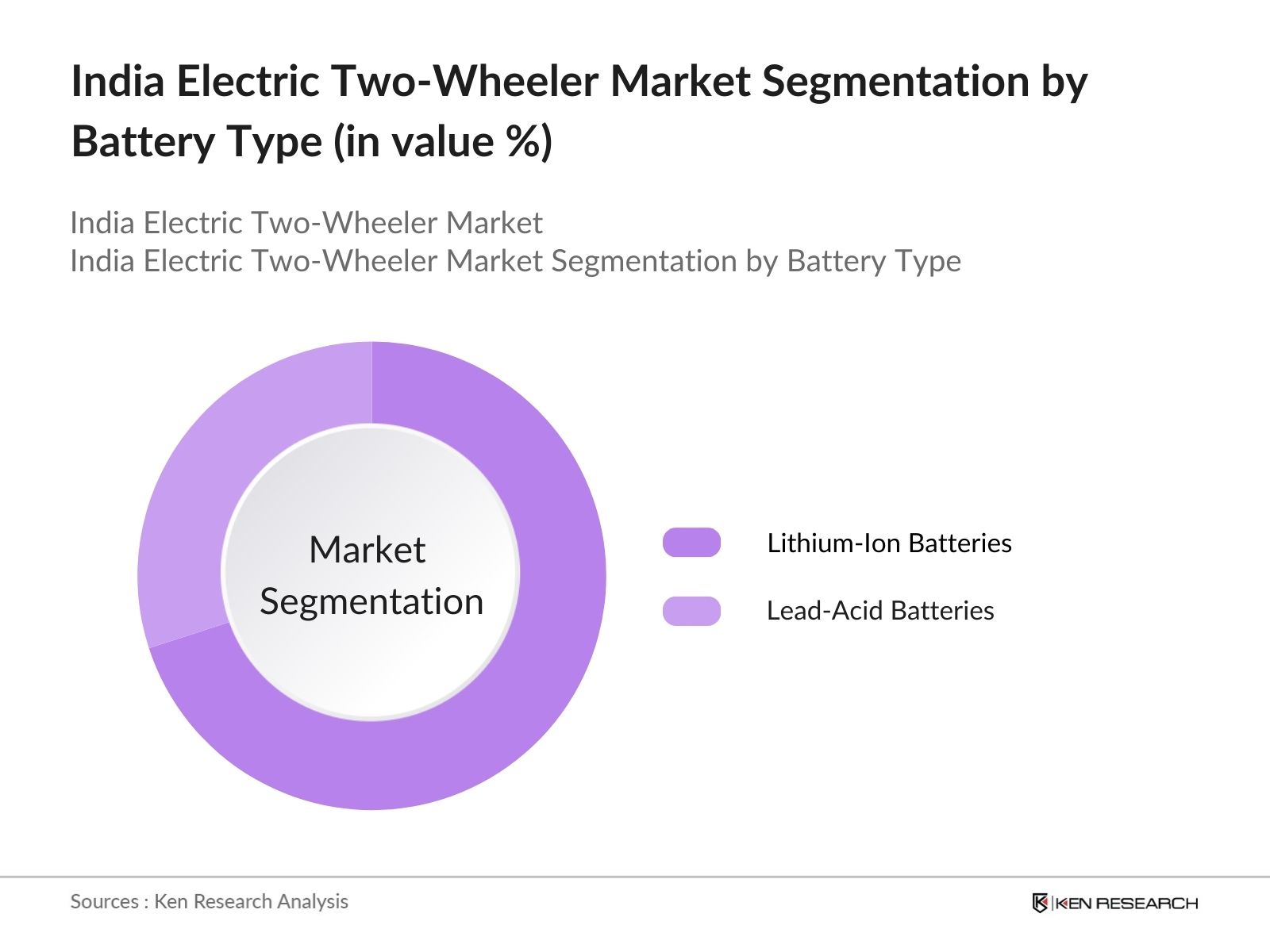

Indias electric two-wheeler market is segmented by vehicle type and by battery type.

The India Electric Two-Wheeler market is dominated by a few key players, including both legacy manufacturers and emerging startups. Companies like Hero Electric and Ather Energy have established themselves as front-runners in the electric scooter segment, while brands like Bajaj and TVS are leveraging their extensive dealer networks to penetrate deeper into the market. Furthermore, the rise of Ola Electric as a disruptor with large-scale production capabilities has added competitive pressure, forcing traditional companies to innovate and expand their product lines.

|

Company |

Establishment Year |

Headquarters |

Production Capacity |

Battery Technology |

Sales Network |

|

Hero Electric |

1956 |

New Delhi |

|||

|

Ather Energy |

2013 |

Bengaluru |

|||

|

Bajaj Auto |

1945 |

Pune |

|||

|

Ola Electric |

2017 |

Bengaluru |

|||

|

TVS Motor Company |

1978 |

Hosur |

Over the next five years, the India Electric Two-Wheeler market is poised to witness significant expansion driven by technological advancements, increasing urbanization, and the ongoing support from the government through subsidies and incentives. The growing concern over environmental sustainability, combined with rising fuel prices, will further push the adoption of electric two-wheelers across the country. This sector is expected to experience robust growth, particularly in metropolitan areas where charging infrastructure and government initiatives are more prevalent.

|

Electric Scooters Electric Motorcycles Electric Mopeds

|

|

|

By Battery Type |

Lithium-Ion Batteries Lead-Acid Batteries |

|

By End-Use |

Personal Use Commercial (Last-Mile Delivery, E-commerce) |

|

By Charging Infrastructure |

Home Charging Public Charging Battery-Swapping Stations |

|

By Region |

North East West South |

1.1. Definition and Scope

1.2. Market Taxonomy (By Vehicle Type, Battery Type, Charging Infrastructure, Power Output, and End-Use)

1.3. Market Growth Rate (Growth in Urbanization, Electrification Push, Government Initiatives, Rising Consumer Awareness)

1.4. Market Segmentation Overview (Detailed Segmentation across Key Parameters)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Vehicle Sales, Production Capacities, EV Infrastructure Development)

3.1. Growth Drivers

3.1.1. Government Subsidies and Incentives

3.1.2. Increasing Fuel Prices

3.1.3. Rising Environmental Awareness

3.1.4. Growing Adoption of E-Commerce and Last-Mile Delivery Solutions

3.2. Market Challenges

3.2.1. High Initial Costs of EVs

3.2.2. Limited Charging Infrastructure

3.2.3. Battery Recycling and Disposal Issues

3.3. Opportunities

3.3.1. Technological Advancements in Battery Systems

3.3.2. Expanding Rural Electrification

3.3.3. Growth of Battery-Swapping Models

3.3.4. Collaboration with International OEMs

3.4. Trends

3.4.1. Use of Lithium-Ion Batteries (Battery Efficiency and Energy Density)

3.4.2. Increased Adoption of Connected and Smart Vehicles (IoT-enabled Systems)

3.4.3. Rise of Subscription-based EV Ownership Models

3.5. Regulatory Landscape (National and State-level Policies)

3.5.1. FAME II Scheme

3.5.2. Battery Standardization and Safety Regulations

3.5.3. Incentives for Domestic Manufacturing

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (OEMs, Battery Manufacturers, Charging Station Providers, Consumers)

3.8. Porters Five Forces Analysis (Bargaining Power of Suppliers, Threat of Substitutes, etc.)

3.9. Competition Ecosystem (Leading OEMs, Supply Chain Integration, Aftermarket Services)

4.1. By Vehicle Type (In Value %)

4.1.1. Electric Scooters

4.1.2. Electric Motorcycles

4.1.3. Electric Mopeds

4.2. By Battery Type (In Value %)

4.2.1. Lithium-Ion Batteries

4.2.2. Lead-Acid Batteries

4.3. By Region (In Value %)

4.3.1. North

4.3.2. East

4.3.3. West

South

4.4. By Charging Infrastructure (In Value %)

4.4.1. Home Charging

4.4.2. Public Charging

4.4.3. Battery-Swapping Stations

4.5. By End-Use (In Value %)

4.5.1. Personal Use

4.5.2. Commercial (Last-Mile Delivery, E-commerce)

5.1. Detailed Profiles of Major Companies

5.1.1. Hero Electric

5.1.2. Ather Energy

5.1.3. Ola Electric

5.1.4. Bajaj Auto

5.1.5. TVS Motor Company

5.1.6. Okinawa Autotech

5.1.7. Revolt Motors

5.1.8. Ampere Electric

5.1.9. Pure EV

5.1.10. Tork Motors

5.1.11. Mahindra Electric

5.1.12. Etrio

5.1.13. Jitendra New EV Tech

5.1.14. Nexzu Mobility

5.1.15. Avan Motors

5.2. Cross Comparison Parameters (Headquarters, Market Share, Production Capacity, Revenue, Product Range, Expansion Strategies, Battery Technology Used, Charging Infrastructure Investment)

5.3. Market Share Analysis (Top Players and Regional Distribution)

5.4. Strategic Initiatives (Product Launches, Partnerships, Technological Advancements)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Private and Government Investments)

5.7. Venture Capital Funding

5.8. Government Grants and Support

5.9. Private Equity Investments

6.1. FAME II Policy Implementation and Impact

6.2. State-Level Electric Vehicle Policies (Maharashtra, Karnataka, Gujarat, etc.)

6.3. Battery Recycling and E-Waste Regulations

6.4. Import Duties on EV Components

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Technological Innovations, Green Energy Push)

8.1. By Vehicle Type (In Value %)

8.2. By Battery Type (In Value %)

8.3. By Region (In Value %)

8.4. By Charging Infrastructure (In Value %)

8.5. By End-Use (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Preferences and Behavior Analysis

9.3. Market Penetration Strategies

9.4. White Space Opportunity Identification

In the initial phase, we identified the major stakeholders in the India Electric Two-Wheeler Market, including manufacturers, suppliers, and government bodies. Extensive desk research was conducted using proprietary databases and secondary sources to map out critical variables that impact market growth and dynamics.

The second phase involved analyzing historical data related to electric two-wheeler sales, vehicle registrations, and charging infrastructure development. This was complemented by evaluating technological advancements and government policies that have shaped the market.

To ensure data accuracy, we conducted computer-assisted telephone interviews (CATI) with industry experts, including OEM executives, charging station operators, and government officials. These consultations provided insights into operational challenges, consumer behavior, and market potential.

The final stage involved synthesizing the research data to create a comprehensive report that includes detailed insights into vehicle segments, battery technologies, and market challenges. This data was cross-verified with manufacturers and suppliers to ensure its reliability.

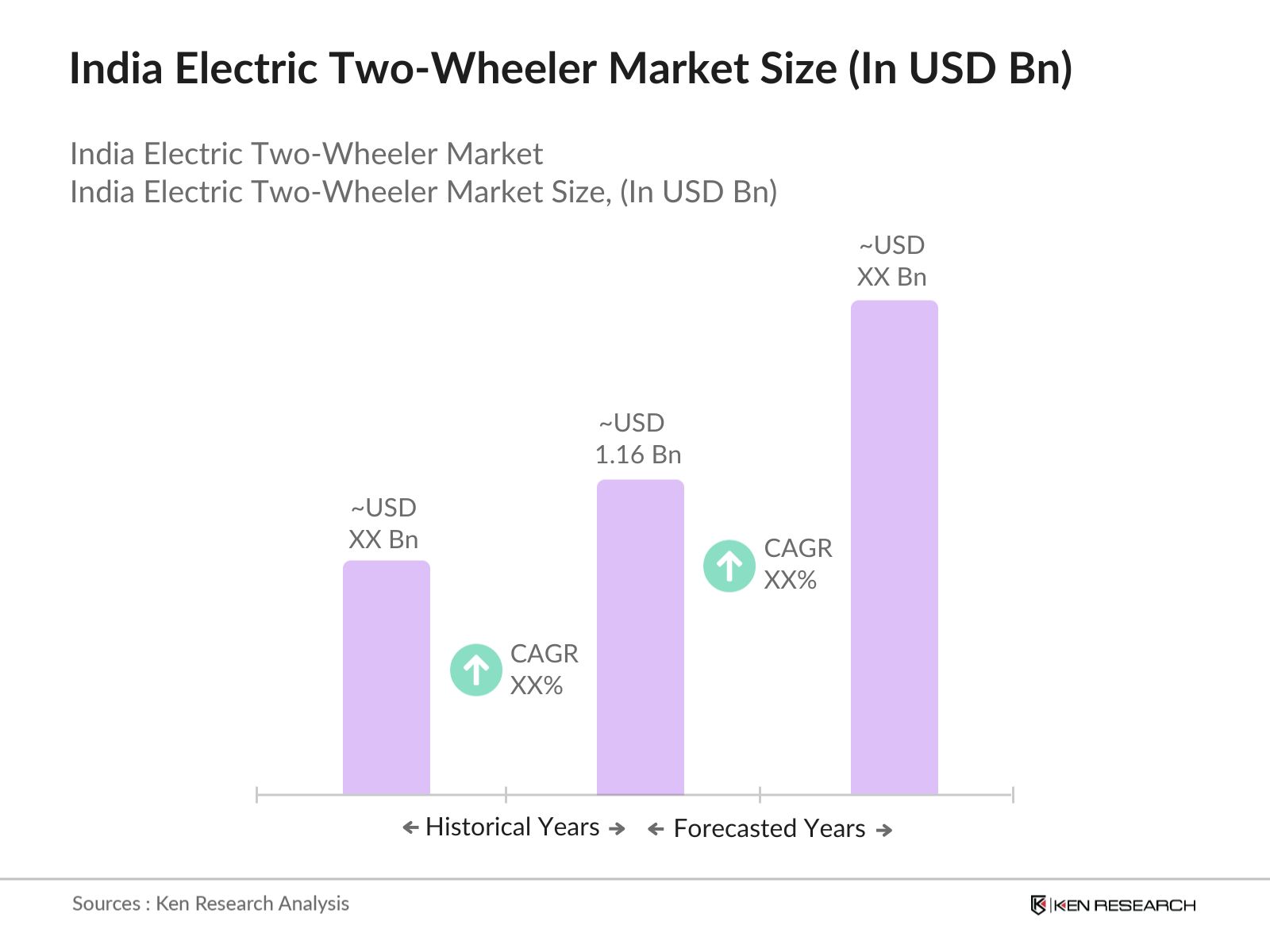

The India Electric Two-Wheeler market is currently valued at 1.16 million, driven by growing demand for affordable, eco-friendly transportation solutions, government subsidies, and the rising cost of petrol.

Challenges in India Electric Two-Wheeler market include the high cost of lithium-ion batteries, lack of widespread charging infrastructure, and consumer hesitation due to concerns over battery longevity and vehicle range.

Key players in India Electric Two-Wheeler market include Hero Electric, Ather Energy, Ola Electric, Bajaj Auto, and TVS Motor Company. These companies dominate the market through a combination of strong brand presence, extensive sales networks, and ongoing innovation.

Growth drivers in India Electric Two-Wheeler market include government incentives under schemes like FAME II, rising environmental awareness, advancements in battery technology, and the increasing adoption of electric vehicles in last-mile delivery services.

Opportunities lie in the expansion of battery-swapping infrastructure, increasing rural electrification, and partnerships between domestic manufacturers and international OEMs.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.