India Electric Vans Market Outlook 2030

Region:Asia

Author(s):Shivani Mehra

Product Code:KROD4668

October 2024

97

About the Report

India Electric Vans Market Overview

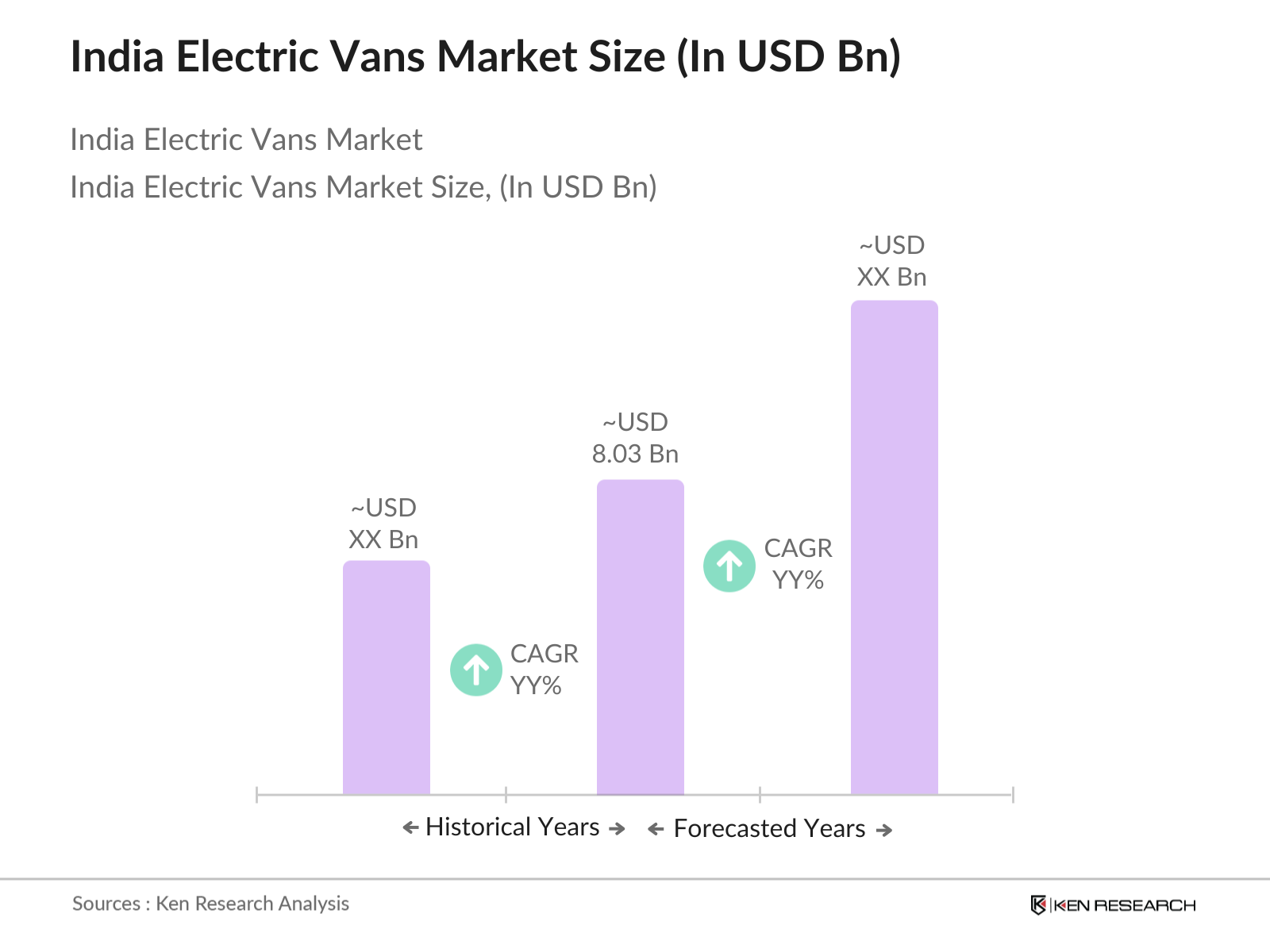

- The India Electric Vans Market is valued at USD 8.03 billion, based on a five-year historical analysis. The market's growth is primarily driven by the rapid adoption of electric vehicles (EVs) in the commercial sector, supported by government incentives under initiatives like the FAME (Faster Adoption and Manufacturing of Hybrid and EVs) scheme.

- The dominant cities in this market include Delhi, Bangalore, and Mumbai due to their established infrastructure, high urbanization rates, and large-scale adoption of EV policies. These cities have favorable government policies supporting EV fleets and enhanced charging infrastructure. Additionally, demand from e-commerce logistics in these cities, which prioritize reducing carbon footprints, further cements their leadership in the market.

- The Government of India introduced the Production-Linked Incentive (PLI) scheme for the automobile and auto components sector with a budget of INR 26,000 crore. This initiative supports electric vehicle manufacturers by incentivizing the production of advanced technologies, including light commercial EVs with integrated telematics and smart systems. The PLI scheme encourages domestic production of critical EV components, such as battery systems, to enhance technological innovation in electric vans.

India Electric Vans Market Segmentation

-

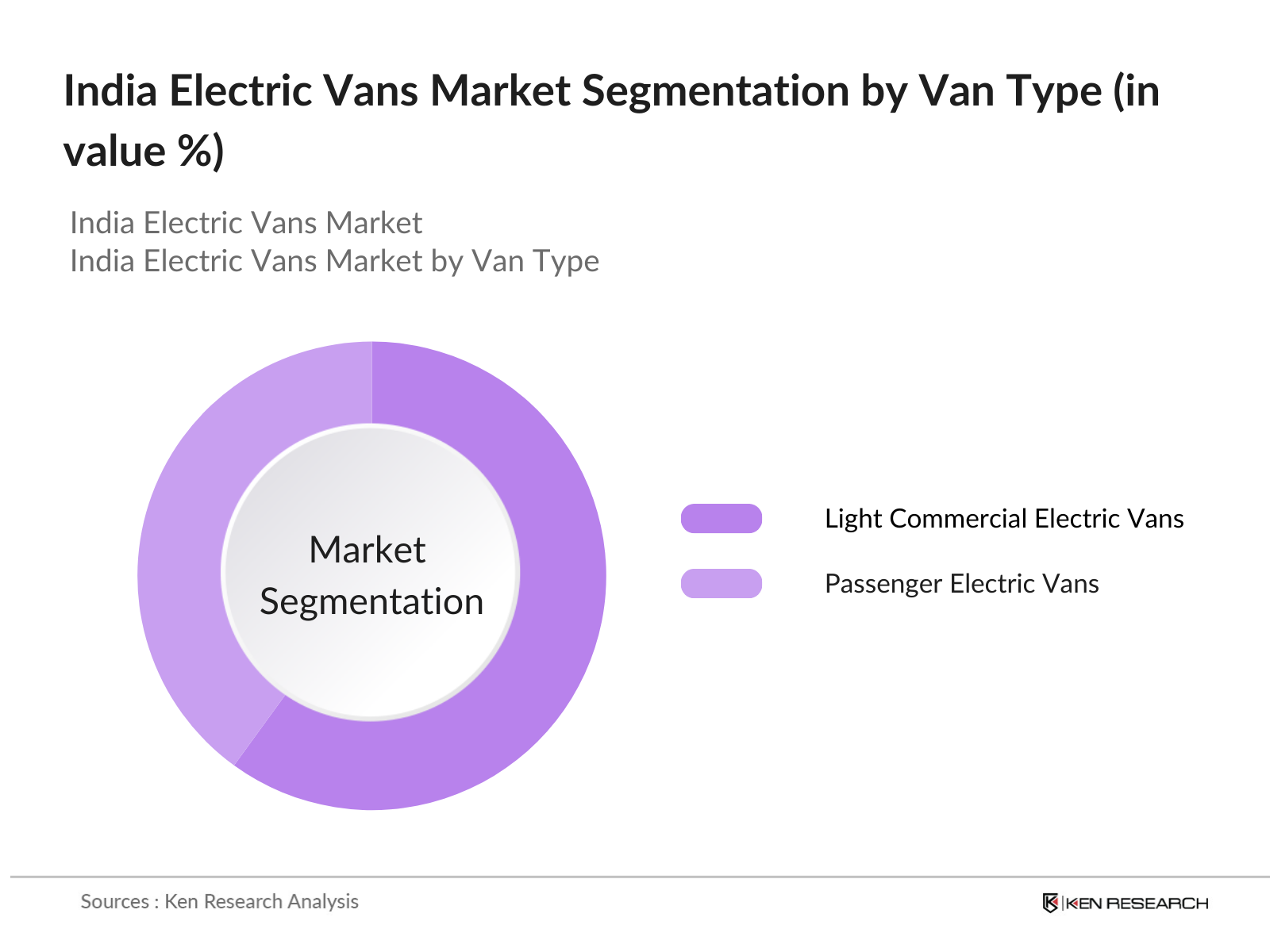

By Van Type: The India Electric Vans Market is segmented by van type into light commercial electric vans and passenger electric vans. Recently, light commercial electric vans have gained a dominant market share under the van type segment, primarily due to their growing demand in last-mile delivery services for e-commerce companies. The logistics and transportation sectors are increasingly adopting electric vans due to cost benefits in fuel savings, lower maintenance expenses, and their positive impact on sustainability goals. E-commerce giants are focusing on electrifying their fleets to achieve carbon neutrality, which is driving the growth of light commercial electric vans.

-

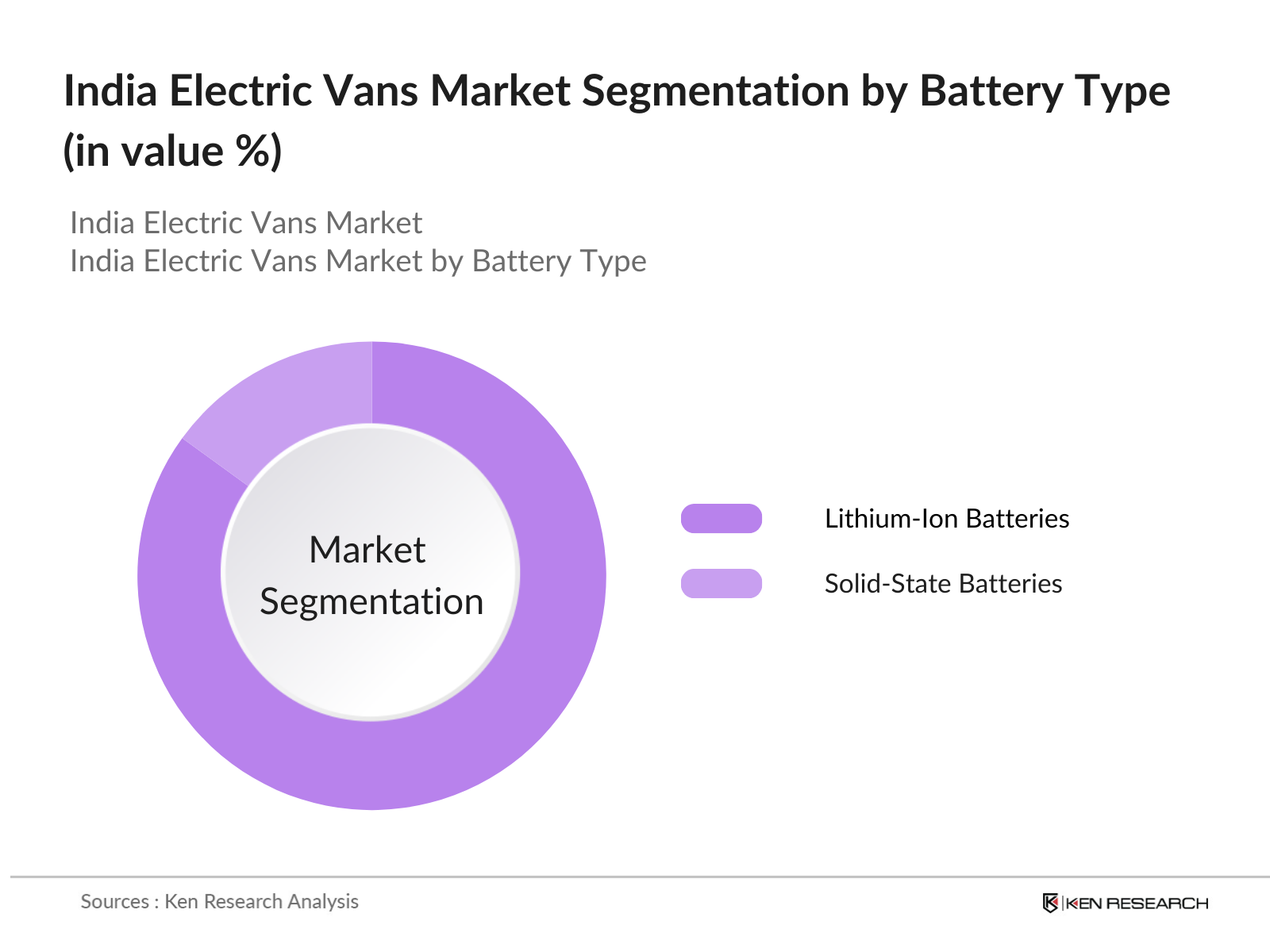

By Battery Type: The India Electric Vans Market is segmented by battery type into lithium-ion batteries and solid-state batteries. Lithium-ion batteries dominate the market due to their widespread use in electric vehicles for their superior energy density and longer life span. These batteries are highly efficient and are favored by manufacturers due to their well-established supply chains and economies of scale. Moreover, the advancements in lithium-ion battery technology, along with decreasing battery costs, continue to drive their dominance in the market.

India Electric Vans Competitive Landscape

The India Electric Vans market is dominated by a combination of local and international companies that have strategically invested in EV technology and infrastructure. Companies like Tata Motors and Mahindra Electric lead the market with their extensive R&D efforts and strong brand equity, while international players like Tesla Inc. are increasingly eyeing market entry due to the growing EV demand. The competitive landscape is further shaped by the focus on collaboration with governments to establish EV infrastructure and manufacturing capabilities.

|

Company |

Establishment Year |

Headquarters |

Production Capacity |

R&D Investment |

EV Fleet Size |

Revenue (INR) |

Geographic Reach |

Charging Network |

|

Tata Motors |

1945 |

Mumbai, India |

||||||

|

Mahindra Electric |

1945 |

Bangalore, India |

||||||

|

Ashok Leyland |

1948 |

Chennai, India |

||||||

|

Tesla Inc. |

2003 |

California, USA |

||||||

|

BYD India |

1995 |

Shenzhen, China |

India Electric Vans Market Analysis

Market Growth Drivers

- Electric Vehicle (EV) Policy Implementation: The Indian government's push for electric vehicles (EVs) is driven by policies such as the FAME II scheme. The scheme, with a budget of INR 10,000 crore, aims to support 7,000 electric buses and 35,000 electric four-wheelers by 2024. This policy is promoting the adoption of electric vans by reducing the upfront costs through subsidies and lowering operational costs due to fuel savings. The policy encourages EV adoption in the commercial vehicle segment, where electric vans play a crucial role in logistics and transportation.

- Reduction in Total Cost of Ownership (TCO): Electric vans in India benefit from lower Total Cost of Ownership (TCO) when compared to internal combustion engine (ICE) vehicles. For instance, while the upfront cost of electric vans may be higher, the reduced maintenance costs and fuel savings, averaging INR 20,000 per year, make them financially viable for fleet operators. The cost of running electric vans is INR 1 per km as opposed to INR 4 per km for diesel vehicles, encouraging large-scale adoption in the logistics sector.

- Public Transportation Electrification: India's electrification of public transportation is extending to light commercial vehicles (LCVs) such as electric vans. In 2023, India saw a rise in the deployment of over 5,000 electric buses under the FAME II scheme, showcasing the government's commitment to electrifying public transport. Electric vans are expected to complement this effort by reducing emissions from delivery services and intra-city goods transportation. With favorable government policies, this transition is accelerating, making electric vans a critical part of India's sustainable transportation model.

Market Challenges

- Charging Infrastructure Development: India currently has around 5,000 public EV charging stations, insufficient to meet the growing demand for electric vehicles, including vans. The lack of widespread infrastructure creates logistical challenges for operators, particularly for long-distance commercial vehicles. To address this, the government has set a target to install 50,000 EV charging stations by 2025. However, the current shortage of charging points remains a major hurdle for the commercial adoption of electric vans.

- Range Anxiety Among Consumers: Range anxiety is a significant concern for electric van operators, especially in commercial fleets that require longer driving ranges. Currently, electric vans in India offer an average range of 120–200 km per charge, which may not be sufficient for long-haul operations. Fleet operators are hesitant to adopt electric vans without reliable solutions for charging infrastructure and extended range, which is crucial for their day-to-day logistics and delivery services.

India Electric Vans Market Future Outlook

Over the next few years, the India Electric Vans Market is expected to witness significant growth driven by strong government support, advancements in battery technology, and increasing demand for eco-friendly transportation solutions. As logistics companies continue to adopt electric vans to reduce operational costs and meet sustainability goals, the market will experience robust growth in both urban and rural regions. The government's focus on expanding the charging infrastructure across the country will further accelerate this growth, ensuring the market's sustainability.

Market Opportunities:

- Growth in E-commerce and Logistics: India's e-commerce sector, valued at INR 4 trillion, is driving demand for electric vans. Major logistics companies are now integrating electric vans into their delivery fleets to meet sustainability goals. In 2023, leading companies such as Amazon and Flipkart added over 2,000 electric delivery vans to their operations in India. The trend towards electrification of logistics fleets is expected to accelerate as companies look for cost-effective and eco-friendly transportation solutions.

- Light Commercial EV Innovations: Light commercial electric vans in India are undergoing technological advancements, including the integration of telematics and smart charging systems. These innovations enhance fleet management capabilities, providing real-time data on vehicle performance and optimizing delivery routes. By 2024, Indian manufacturers are expected to introduce electric vans with autonomous driving features, increasing efficiency and safety in commercial transportation.

Scope of the Report

|

By Van Type |

Light Commercial Electric Vans Passenger Electric Vans |

|

By Battery Type |

Lithium-Ion Batteries Solid-State Batteries |

|

By Application |

Logistics and E-commerce Public Transportation Corporate and Rental Services |

|

By End-User |

Government Fleets Private Companies Individual Consumers |

|

By Region |

North-East Midwest West Coast Southern States |

Products

Key Target Audience

- Electric Vehicle Manufacturers

- Battery Suppliers and Manufacturers

- Government Agencies (Ministry of Heavy Industries, Ministry of Road Transport and Highways)

- Charging Infrastructure Providers

- Logistics and E-commerce Companies

- Corporate Fleet Management Companies

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies (FAME II Steering Committee)

Companies

Major Players in India Electric Vans Market

- Tata Motors

- Mahindra Electric

- Ashok Leyland

- Tesla Inc.

- BYD India

- Hyundai Motor India

- JBM Auto

- Force Motors

- Eicher Motors

- Piaggio Vehicles

- Hero Electric

- Okinawa Autotech

- VE Commercial Vehicles

- TVS Motor Company

- Kinetic Green

Table of Contents

1. India Electric Vans Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. India Electric Vans Market Size (In INR Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. India Electric Vans Market Analysis

3.1. Growth Drivers (Government Incentives, Fuel Cost Savings, Environmental Concerns)

3.1.1. Electric Vehicle (EV) Policy Implementation

3.1.2. Reduction in Total Cost of Ownership (TCO)

3.1.3. Rising Urban Air Pollution

3.1.4. Public Transportation Electrification

3.2. Market Challenges (Infrastructure Limitations, High Initial Cost, Battery Technology)

3.2.1. Charging Infrastructure Development

3.2.2. Range Anxiety Among Consumers

3.2.3. High Acquisition Costs

3.2.4. Battery Recycling and Disposal Challenges

3.3. Opportunities (Emerging Battery Technologies, Public-Private Partnerships, Export Potential)

3.3.1. Solid-State Batteries

3.3.2. Government Subsidies and Schemes

3.3.3. Expansion into Rural Markets

3.3.4. International Export Opportunities

3.4. Trends (Fleet Electrification, Light Commercial Vehicle Adoption, EV Leasing)

3.4.1. Growth in E-commerce and Logistics

3.4.2. Light Commercial EV Innovations

3.4.3. Shift Towards EV Leasing Models

3.4.4. Integration of Autonomous Driving in Electric Vans

3.5. Government Regulation (FAME II Scheme, GST Benefits, Emission Norms)

3.5.1. Faster Adoption and Manufacturing of Electric Vehicles (FAME) Policy

3.5.2. Subsidies for EV Manufacturers

3.5.3. Green Tax Implementation

3.5.4. Policies Supporting Domestic Manufacturing

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (EV Manufacturers, Charging Infrastructure Providers, Component Suppliers)

3.8. Porter’s Five Forces Analysis

3.9. Competition Ecosystem

4. India Electric Vans Market Segmentation

4.1. By Van Type (In Value %)

4.1.1. Light Commercial Electric Vans

4.1.2. Passenger Electric Vans

4.2. By Battery Type (In Value %)

4.2.1. Lithium-Ion Batteries

4.2.2. Solid-State Batteries

4.3. By Application (In Value %)

4.3.1. Logistics and E-commerce

4.3.2. Public Transportation

4.3.3. Corporate and Rental Services

4.4. By End-User (In Value %)

4.4.1. Government Fleets

4.4.2. Private Companies

4.4.3. Individual Consumers

4.5. By Region (In Value %)

4.5.1. Northern India

4.5.2. Southern India

4.5.3. Western India

4.5.4. Eastern India

4.5.5. Central India

5. India Electric Vans Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Mahindra Electric

5.1.2. Tata Motors

5.1.3. Ashok Leyland

5.1.4. Maruti Suzuki

5.1.5. Tesla Inc.

5.1.6. BYD India

5.1.7. Hyundai Motor India

5.1.8. JBM Auto

5.1.9. Force Motors

5.1.10. VE Commercial Vehicles

5.1.11. Piaggio Vehicles

5.1.12. TVS Motor Company

5.1.13. Eicher Motors

5.1.14. Hero Electric

5.1.15. Okinawa Autotech

5.2. Cross Comparison Parameters (Production Capacity, Revenue, EV Market Share, Fleet Size, R&D Expenditure, Battery Supply Chain, Charging Infrastructure, Geographic Reach)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Product Launches, Strategic Collaborations, Expansion Plans)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants and Funding

5.8. Private Equity and Venture Capital Investments

6. India Electric Vans Market Regulatory Framework

6.1. EV Manufacturing Standards

6.2. Compliance with Safety and Emission Regulations

6.3. Certification for Battery and Vehicle Standards

7. India Electric Vans Future Market Size (In INR Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. India Electric Vans Future Market Segmentation

8.1. By Van Type (In Value %)

8.2. By Battery Type (In Value %)

8.3. By Application (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9. India Electric Vans Market Analysts’ Recommendations

9.1. Total Addressable Market (TAM)/Serviceable Available Market (SAM)/Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Segmentation and Preference Analysis

9.3. Go-to-Market Strategies for Electric Van Providers

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the India Electric Vans Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we will compile and analyze historical data pertaining to the India Electric Vans Market. This includes assessing market penetration, the ratio of marketplace to service providers, and resultant revenue generation. Furthermore, an evaluation of market-specific parameters will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple electric vehicle manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the India Electric Vans Market.

Frequently Asked Questions

01. How big is the India Electric Vans Market?

The India Electric Vans Market was valued at USD 8.03 billion, primarily driven by rising demand for eco-friendly transportation solutions in urban areas and government incentives encouraging EV adoption.

02. What are the challenges in the India Electric Vans Market?

The challenges in the India Electric Vans Market include limited charging infrastructure, high initial costs of electric vans, and issues with battery disposal and recycling, which impact both operational efficiency and consumer confidence.

03. Who are the major players in the India Electric Vans Market?

Key players in the India Electric Vans Market include Tata Motors, Mahindra Electric, Ashok Leyland, Tesla Inc., and BYD India. These companies dominate due to their strong manufacturing capabilities, extensive distribution networks, and active participation in government EV schemes.

04. What are the growth drivers of the India Electric Vans Market?

Growth drivers include government incentives such as the FAME II scheme, increasing consumer awareness of environmental sustainability, and cost savings associated with the lower total cost of ownership compared to traditional fuel-powered vans.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.