India Electronics Market Outlook to 2030

Region:India

Author(s):Paribhasha Tiwari

Product Code:KROD10733

Region:India

Author(s):Paribhasha Tiwari

Product Code:KROD10733

November 2024

85

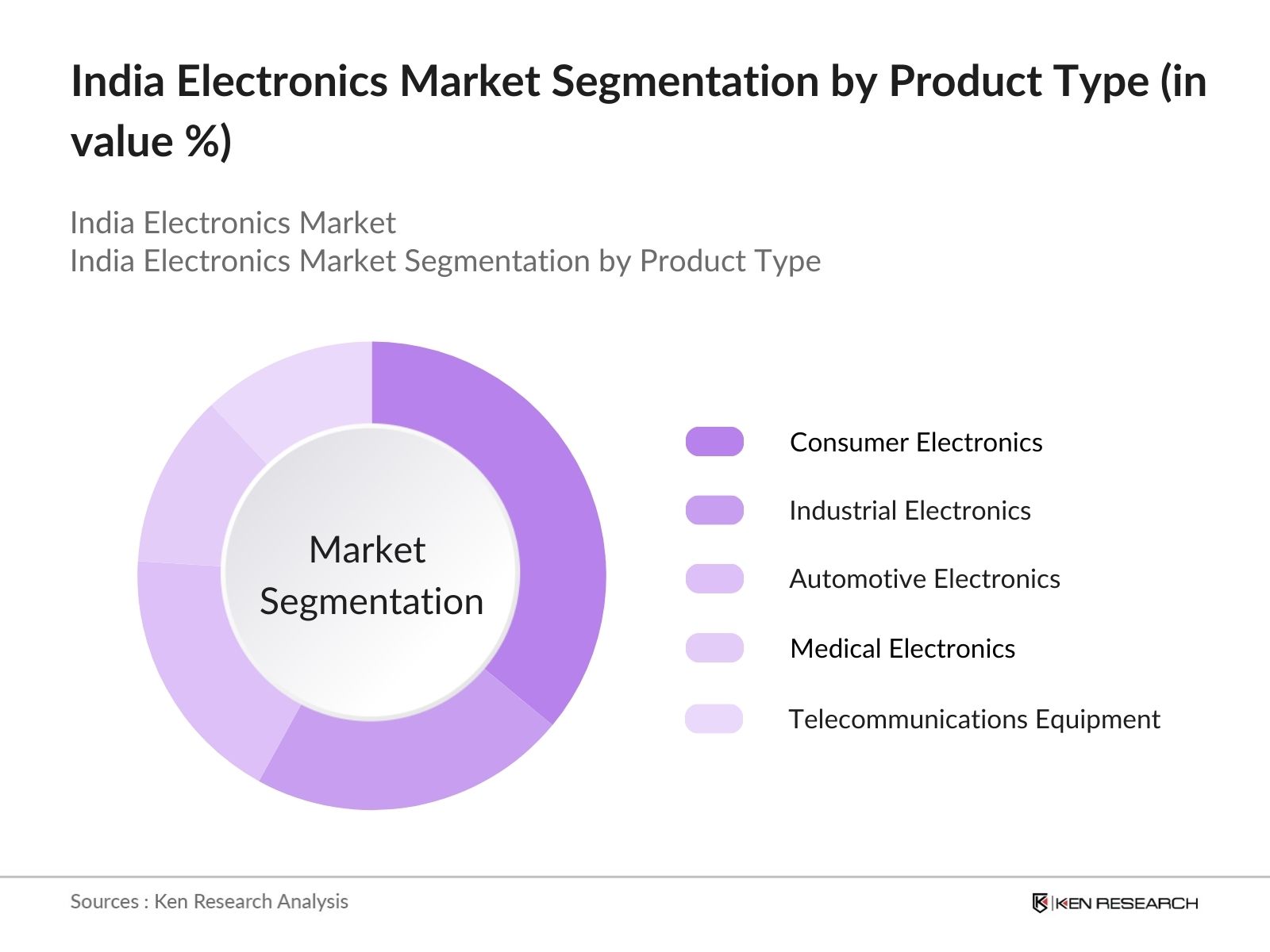

By Product Type: The India Electronics Market is segmented by product type into consumer electronics, industrial electronics, automotive electronics, medical electronics, and telecommunications equipment. Currently, consumer electronics holds the dominant market share within the product type segment due to the widespread use and popularity of smartphones, laptops, and wearables. This growth is largely attributed to the rising demand for digital devices, advancements in technology, and the expansion of e-commerce platforms, enabling easier accessibility and distribution.

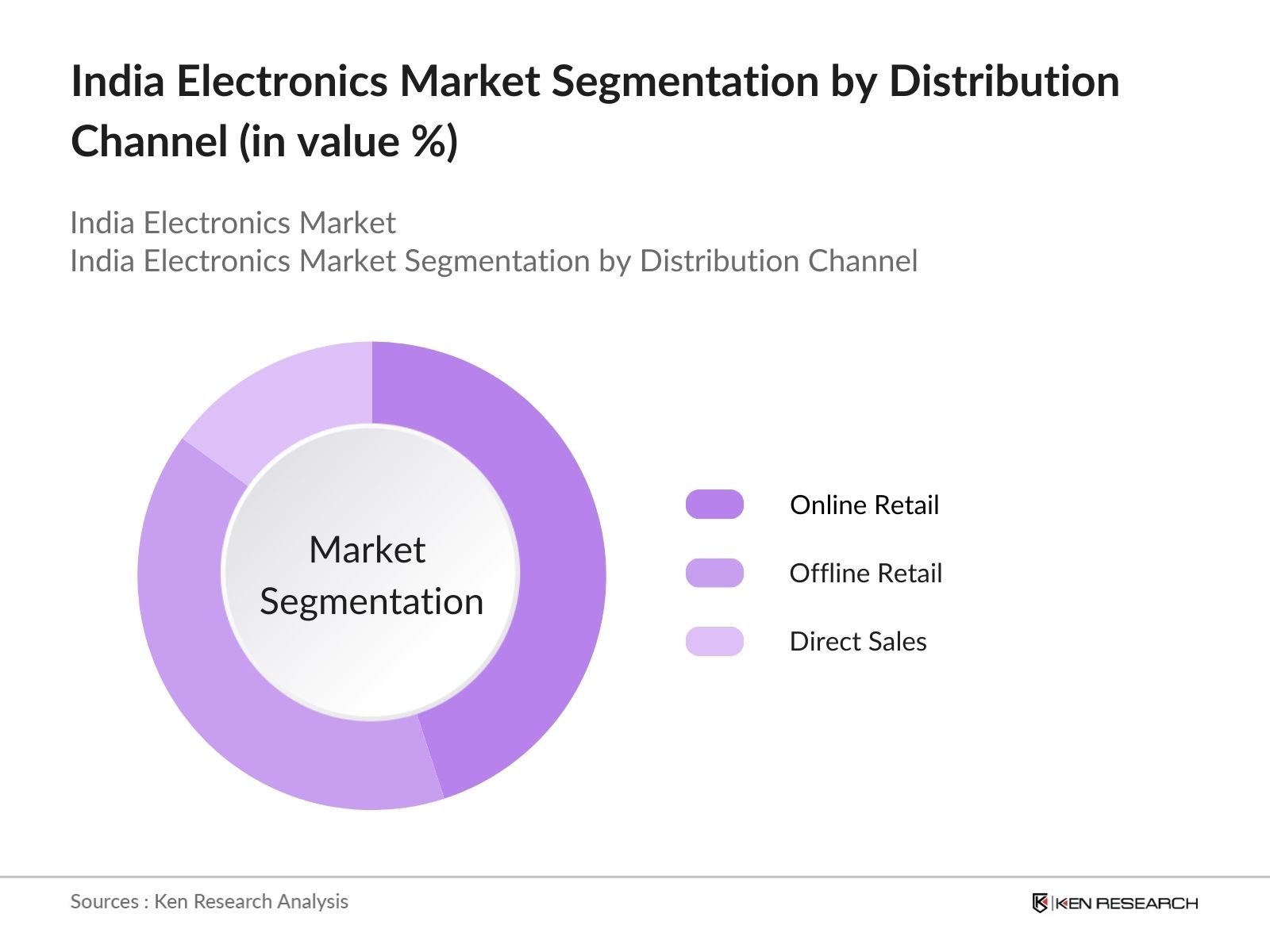

By Distribution Channel: The India Electronics Market is further segmented by distribution channels into online retail, offline retail, and direct sales. Online retail dominates this segment due to the convenience, extensive product variety, and competitive pricing it offers to consumers. The penetration of e-commerce giants like Amazon and Flipkart has also facilitated this trend, catering to the growing digital-savvy population across urban and rural areas alike.

The India Electronics Market is highly competitive, with key players including both domestic and global giants like Samsung, LG, and Tata Electronics. These companies have established robust supply chains, dedicated R&D centers, and strategic partnerships, which significantly shape market dynamics. The dominance of these established players underscores their market influence and customer loyalty.

Over the coming years, the India Electronics Market is expected to witness sustained growth, driven by technological advancements, an increased focus on local manufacturing, and the expanding consumer base. Factors such as the adoption of AI, IoT integration, and green electronics will likely shape the market's trajectory, with government support enhancing manufacturing initiatives. The demand for electronics is anticipated to remain strong across both consumer and industrial applications.

|

By Product Type |

Consumer Electronics Industrial Electronics Automotive Electronics Medical Electronics Telecommunications Equipment |

|

By Application |

Consumer Use Industrial Use Automotive Industry Healthcare Industry Telecommunications Sector |

|

By Distribution Channel |

Online Retail Offline Retail Direct Sales |

|

By End-User |

Individual Consumers Enterprises Government Sector |

|

By Region |

North South East West Central |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Increasing Consumer Demand for Smart Devices

3.1.2 Government Initiatives (PLI Scheme, Digital India, Make in India)

3.1.3 Rising Disposable Income

3.1.4 Expansion of E-commerce

3.2 Market Challenges

3.2.1 High Import Dependency

3.2.2 Complex Regulatory Framework

3.2.3 Supply Chain Disruptions

3.3 Opportunities

3.3.1 Growth of IoT and Smart City Initiatives

3.3.2 Expanding Rural Electrification

3.3.3 Increased Investments in Manufacturing Units

3.4 Trends

3.4.1 Shift Towards Green Electronics

3.4.2 Demand for Wearable Electronics

3.4.3 Integration of AI and Machine Learning in Consumer Electronics

3.5 Government Regulations

3.5.1 Import Tariffs and Duty Structure

3.5.2 Standards by Bureau of Indian Standards (BIS)

3.5.3 Compliance with Environmental Standards (RoHS, E-Waste Management)

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porter’s Five Forces Analysis

3.9 Competitive Ecosystem

4.1 By Product Type (In Value %)

4.1.1 Consumer Electronics (Smartphones, Laptops, Wearables)

4.1.2 Industrial Electronics (PLC, Sensors, Motors)

4.1.3 Automotive Electronics (ADAS, Infotainment, ECU)

4.1.4 Medical Electronics (Diagnostic Equipment, Wearable Health Devices)

4.1.5 Telecommunications Equipment (Network Infrastructure, Routers)

4.2 By Application (In Value %)

4.2.1 Consumer Use

4.2.2 Industrial Use

4.2.3 Automotive Industry

4.2.4 Healthcare Industry

4.2.5 Telecommunications Sector

4.3 By Distribution Channel (In Value %)

4.3.1 Online Retail

4.3.2 Offline Retail (Department Stores, Specialty Stores)

4.3.3 Direct Sales

4.4 By End-User (In Value %)

4.4.1 Individual Consumers

4.4.2 Enterprises

4.4.3 Government Sector

4.5 By Region (In Value %)

4.5.1 North

4.5.2 South

4.5.3 East

4.5.4 West

4.5.5 Central

5.1 Detailed Profiles of Major Companies

5.1.1 Samsung Electronics

5.1.2 LG Electronics

5.1.3 Sony Corporation

5.1.4 Panasonic Corporation

5.1.5 Havells India Ltd.

5.1.6 Bajaj Electricals Ltd.

5.1.7 Voltas Ltd.

5.1.8 Bharat Electronics Ltd.

5.1.9 Tata Electronics Pvt. Ltd.

5.1.10 Videocon Industries Ltd.

5.1.11 Bosch India

5.1.12 Whirlpool of India Ltd.

5.1.13 Foxconn Technology Group

5.1.14 Xiaomi India

5.1.15 Micromax Informatics Ltd.

5.2 Cross Comparison Parameters (Revenue, Production Capacity, Market Presence, Strategic Partnerships, R&D Investment, Product Innovations, CSR Activities, Key Market Regions)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Environmental Standards (RoHS Compliance, E-Waste Management)

6.2 BIS Certification Requirements

6.3 Import Duty and Tariff Regulations

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Product Type (In Value %)

8.2 By Application (In Value %)

8.3 By Distribution Channel (In Value %)

8.4 By End-User (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Consumer Demographic Analysis

9.3 Strategic Marketing Initiatives

9.4 White Space Opportunity Identification

The research begins with an exhaustive assessment of the India Electronics Market landscape. We conducted in-depth desk research and referenced proprietary databases to identify and define critical market variables, such as product types, distribution channels, and consumer preferences.

We collected and analyzed historical data related to market penetration, revenue generation, and distribution patterns. The analysis covered various segments and sub-segments to assess factors impacting market trends and consumer demand.

After constructing initial hypotheses, we consulted industry experts through structured interviews, providing insights into technology integration, supply chain factors, and market dynamics. These consultations aided in validating our data and refining market estimates.

The final stage involved integrating findings from various data sources to ensure a comprehensive and validated analysis. This phase included collaboration with major players and additional secondary research, providing a robust and credible market outlook.

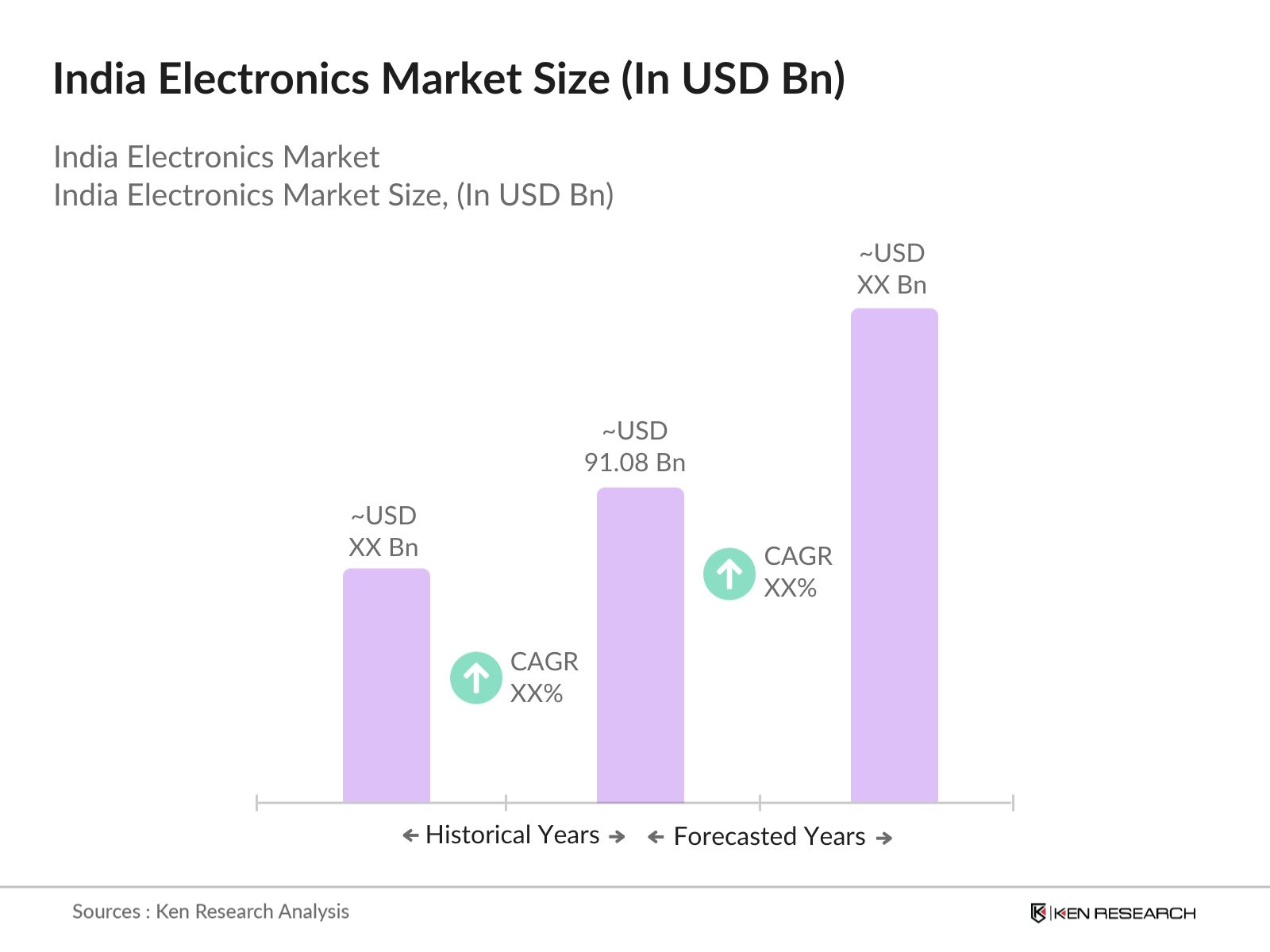

The India Electronics Market, valued at USD 91.08 billion, is driven by increased digital adoption and government support for domestic manufacturing, particularly in consumer and industrial electronics sectors.

Challenges in the India Electronics Market include high import dependency, regulatory complexities, and frequent supply chain disruptions. These factors collectively impact the profitability and stability of the market.

Major players in the India Electronics Market include Samsung, LG, Tata Electronics, Panasonic, and Xiaomi. These companies have a strong market presence owing to their vast distribution networks, advanced R&D, and brand reputation.

Growth drivers for the India Electronics Market include the demand for digital devices, government schemes like PLI, and the increase in e-commerce penetration. Additionally, the rise in consumer spending is supporting robust market growth.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.