India Endoscopic Devices Market Outlook to 2030

Region:India

Author(s):Yogita Sahu

Product Code:KROD6899

Region:India

Author(s):Yogita Sahu

Product Code:KROD6899

November 2024

89

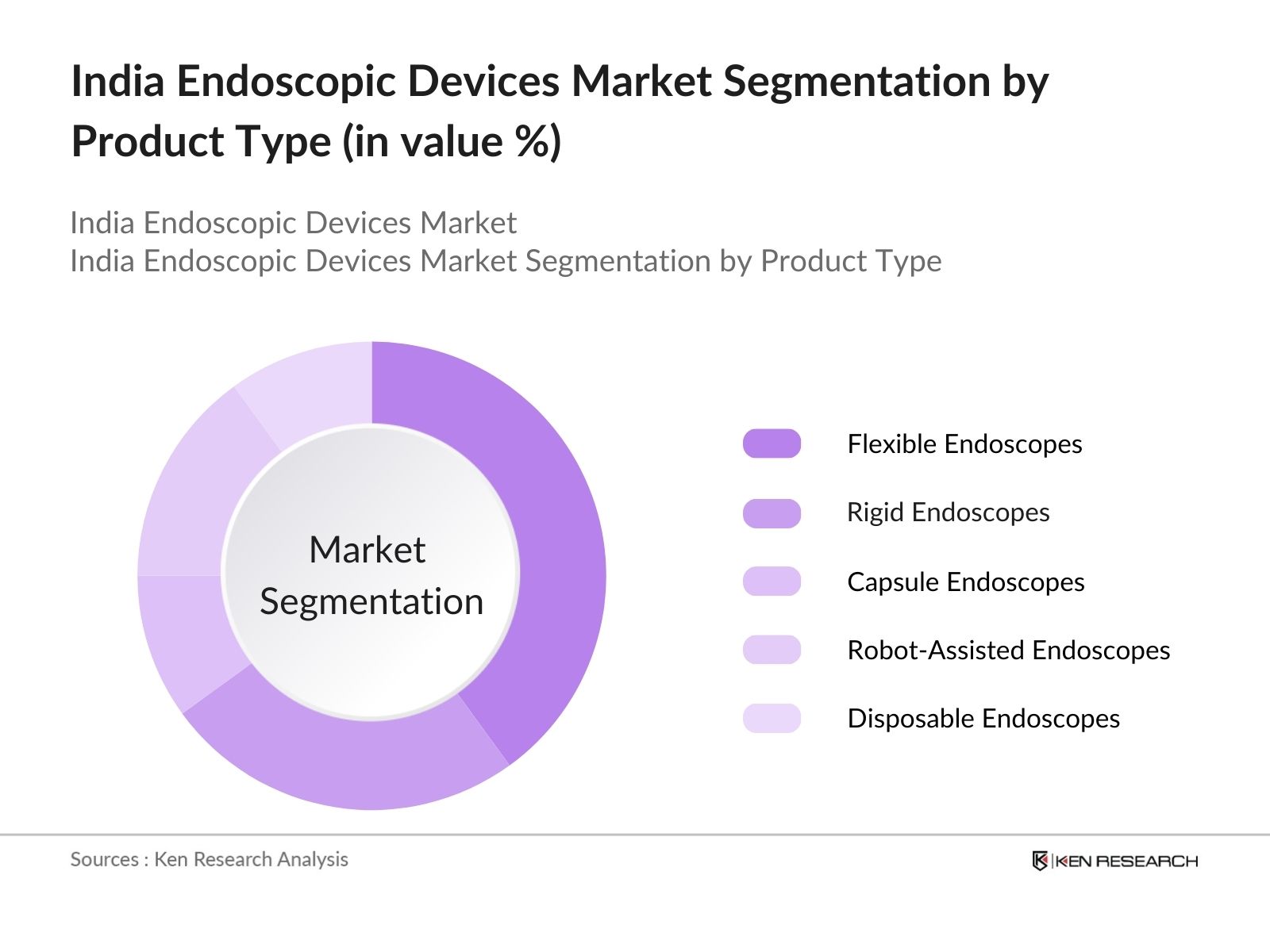

By Product Type: The market is segmented by product type into flexible endoscopes, rigid endoscopes, capsule endoscopes, robot-assisted endoscopes, and disposable endoscopes. Flexible endoscopes hold a dominant market share due to their versatility in performing multiple procedures, particularly in gastroenterology. These devices are favored because they allow physicians to access difficult-to-reach areas within the body while offering superior imaging quality.

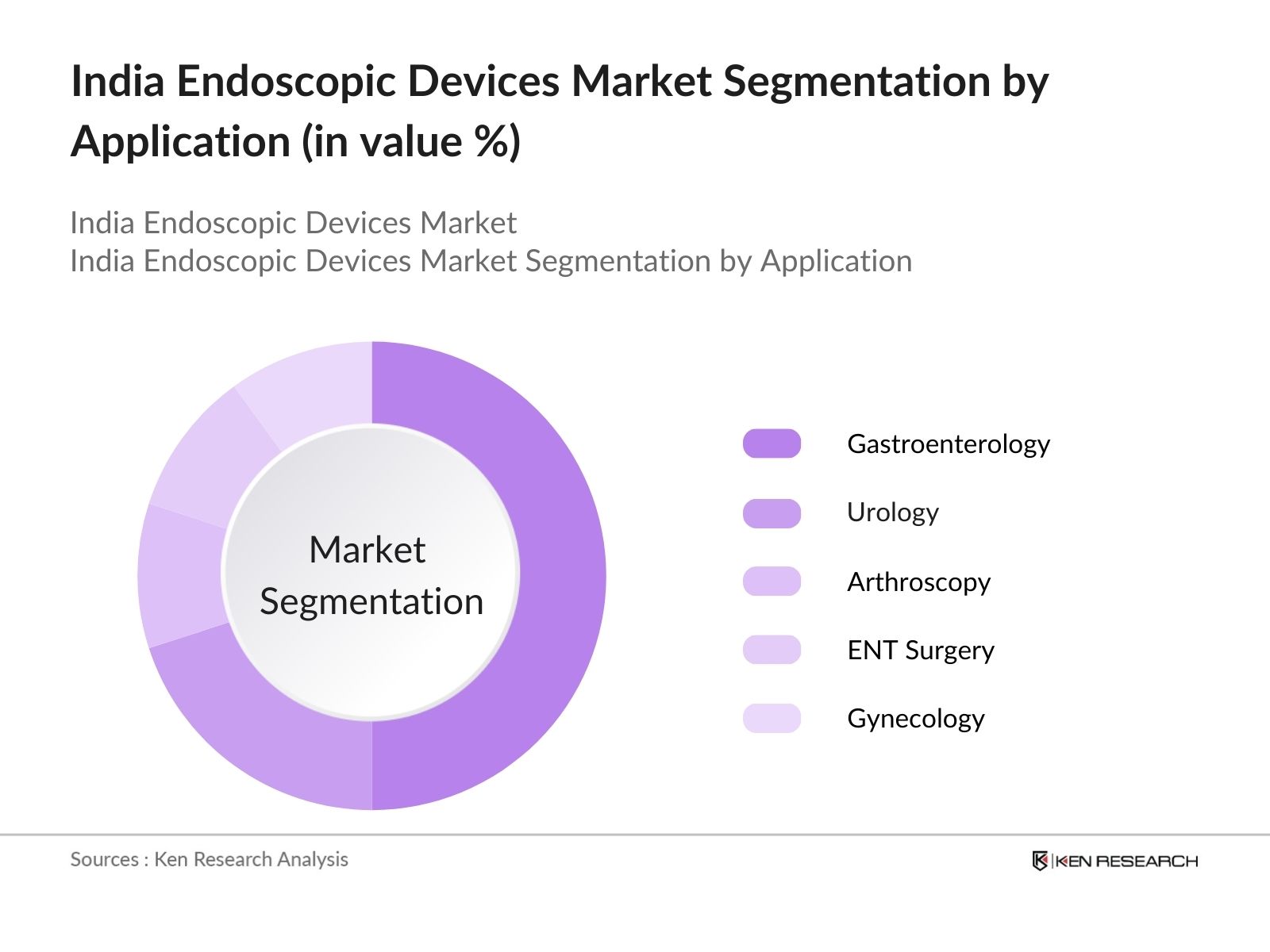

By Application: The market is also segmented by application into gastroenterology, urology, arthroscopy, ENT surgery, and gynecology. Gastroenterology has emerged as the dominant application segment due to the rising incidence of gastrointestinal disorders, such as colorectal cancer and Crohns disease, which require endoscopic interventions. The increasing preference for minimally invasive surgeries in the gastrointestinal space, combined with the rising number of early-stage screenings, contributes significantly to this segment's market dominance.

The market is characterized by the presence of several international and domestic players. Companies like Olympus, Karl Storz, and Fujifilm dominate the market, with significant investments in research and development and advanced manufacturing facilities.

|

Company |

Establishment Year |

Headquarters |

Global Presence |

Product Portfolio |

R&D Spending |

Revenue |

Market Strategy |

Acquisition History |

Key Patents |

|

Olympus Corporation |

1919 |

Tokyo, Japan |

|||||||

|

Karl Storz SE & Co. KG |

1945 |

Tuttlingen, Germany |

|||||||

|

Fujifilm Holdings Corporation |

1934 |

Tokyo, Japan |

|||||||

|

Stryker Corporation |

1941 |

Michigan, USA |

|||||||

|

Boston Scientific |

1979 |

Marlborough, USA |

Over the next five years, the India Endoscopic Devices industry is expected to exhibit robust growth, driven by rising healthcare spending, advancements in medical technology, and an increasing preference for non-invasive surgical procedures.

|

Product Type |

Flexible Endoscopes Rigid Endoscopes Capsule Endoscopes Robot-Assisted Endoscopes Disposable Endoscopes |

|

Application |

Gastroenterology Urology Arthroscopy ENT Surgery Gynecology |

|

End User |

Hospitals Ambulatory Surgical Centers (ASCs) Specialty Clinics Diagnostic Centers |

|

Technology |

Optical Endoscopes Digital Endoscopes Virtual Endoscopy |

|

Region |

North India South India East India West India |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Demand-Supply Equilibrium, Technological Adoption Rate)

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis (Units Sold, Devices Installed)

2.3. Key Market Developments and Milestones (Device Registration, Regulatory Approvals)

3.1. Growth Drivers

3.1.1. Rising Incidence of Gastrointestinal Disorders

3.1.2. Government Initiatives for Healthcare Infrastructure

3.1.3. Increasing Minimally Invasive Surgeries

3.1.4. Healthcare Insurance Penetration

3.2. Market Challenges

3.2.1. High Costs of Advanced Devices

3.2.2. Lack of Skilled Workforce in Rural Areas

3.2.3. Regulatory Approval Delays

3.2.4. Low Awareness in Tier-2 and Tier-3 Cities

3.3. Opportunities

3.3.1. Expansion of Healthcare Infrastructure in Tier-2 Cities

3.3.2. Collaboration with Global Technology Firms

3.3.3. Growing Medical Tourism Industry

3.3.4. Increasing R&D for Advanced Endoscopic Solutions

3.4. Trends

3.4.1. Adoption of AI-Assisted Endoscopic Procedures

3.4.2. Disposable Endoscopes for Infection Control

3.4.3. Integration of Robotic Surgery with Endoscopy

3.4.4. Remote Endoscopic Monitoring for Diagnostics

3.5. Government Regulation

3.5.1. Medical Device Regulations (MD Rules) Compliance

3.5.2. FDI Policies for Medical Device Manufacturing

3.5.3. Certification Standards for Medical Devices (CE Marking, FDA Approval)

3.5.4. Subsidies for Hospital Upgrades (Focus on Endoscopic Procedures)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Endoscopy Device Manufacturers, Healthcare Providers, Distributors, Regulators)

3.8. Porters Five Forces Analysis

3.9. Competitive Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Flexible Endoscopes

4.1.2. Rigid Endoscopes

4.1.3. Capsule Endoscopes

4.1.4. Robot-Assisted Endoscopes

4.1.5. Disposable Endoscopes

4.2. By Application (In Value %)

4.2.1. Gastroenterology

4.2.2. Urology

4.2.3. Arthroscopy

4.2.4. ENT Surgery

4.2.5. Gynecology

4.3. By End User (In Value %)

4.3.1. Hospitals

4.3.2. Ambulatory Surgical Centers (ASCs)

4.3.3. Specialty Clinics

4.3.4. Diagnostic Centers

4.4. By Technology (In Value %)

4.4.1. Optical Endoscopes

4.4.2. Digital Endoscopes

4.4.3. Virtual Endoscopy

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. East India

4.5.4. West India

5.1. Detailed Profiles of Major Companies

5.1.1. Olympus Corporation

5.1.2. Karl Storz SE & Co. KG

5.1.3. Fujifilm Holdings Corporation

5.1.4. Boston Scientific Corporation

5.1.5. Stryker Corporation

5.1.6. Medtronic PLC

5.1.7. Johnson & Johnson (Ethicon)

5.1.8. HOYA Corporation (PENTAX Medical)

5.1.9. Smith & Nephew PLC

5.1.10. Richard Wolf GmbH

5.1.11. Cook Medical

5.1.12. B. Braun Melsungen AG

5.1.13. Conmed Corporation

5.1.14. EndoMed Systems GmbH

5.1.15. Schlly Fiberoptic GmbH

5.2. Cross Comparison Parameters (Revenue, Product Innovation, R&D Spend, Global Presence, Manufacturing Capability, Product Portfolio, Service Contracts, Acquisition History)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Medical Device Standards and Certifications (ISO 13485, MDR)

6.2. Import-Export Policies for Medical Devices

6.3. Licensing and Compliance Requirements

6.4. Quality Control and Safety Standards

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Healthcare Expansion, Technological Innovations)

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By End User (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

In this step, a comprehensive review of the endoscopic devices ecosystem in India was conducted. This included identifying key stakeholders such as manufacturers, distributors, healthcare providers, and regulators. Secondary research, using reliable industry databases and proprietary sources, helped identify critical variables influencing the market.

Historical data on endoscopic device sales, usage rates in different healthcare facilities, and demand dynamics were analyzed to understand the growth patterns. The market's revenue generation and penetration levels across various healthcare institutions were also evaluated.

Market assumptions were verified through in-depth interviews with industry experts, including endoscopy specialists, manufacturers, and hospital procurement heads. These consultations helped refine market forecasts and provided practical insights into operational challenges and opportunities.

A combination of bottom-up and top-down approaches was employed to validate the market size and segmentation. The final analysis was derived from inputs from leading manufacturers, along with real-time data on product usage and healthcare trends across India.

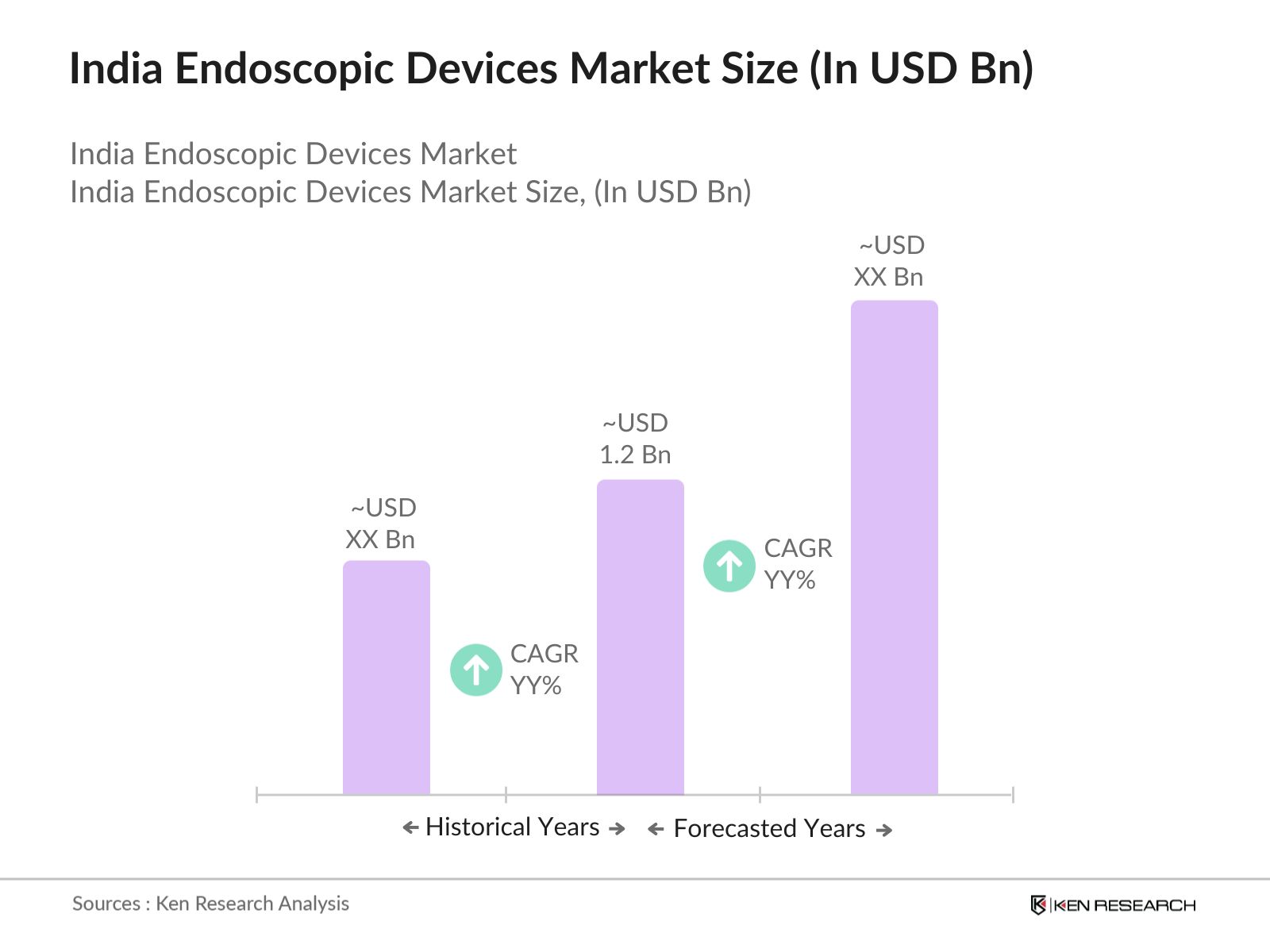

The India Endoscopic Devices Market is valued at USD 1.2 billion, driven by the increasing demand for minimally invasive surgeries and advancements in endoscopic technology.

Challenges in the India Endoscopic Devices Market include the high cost of advanced devices, regulatory approval delays, and a lack of skilled professionals in rural areas, limiting market penetration.

Key players in the India Endoscopic Devices Market include Olympus Corporation, Karl Storz SE & Co. KG, Fujifilm Holdings Corporation, Boston Scientific Corporation, and Stryker Corporation, known for their technological advancements and extensive product portfolios.

Growth drivers in the India Endoscopic Devices Market include the rising prevalence of gastrointestinal disorders, increasing government healthcare expenditure, and the expansion of healthcare infrastructure in both urban and rural areas.

Flexible endoscopes hold the largest share due to their wide applicability in gastroenterology, urology, and gynecology, making them a preferred choice for hospitals and diagnostic centers.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.