India Epoxy Resins Market Outlook to 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD3932

Region:Global

Author(s):Shivani Mehra

Product Code:KROD3932

December 2024

94

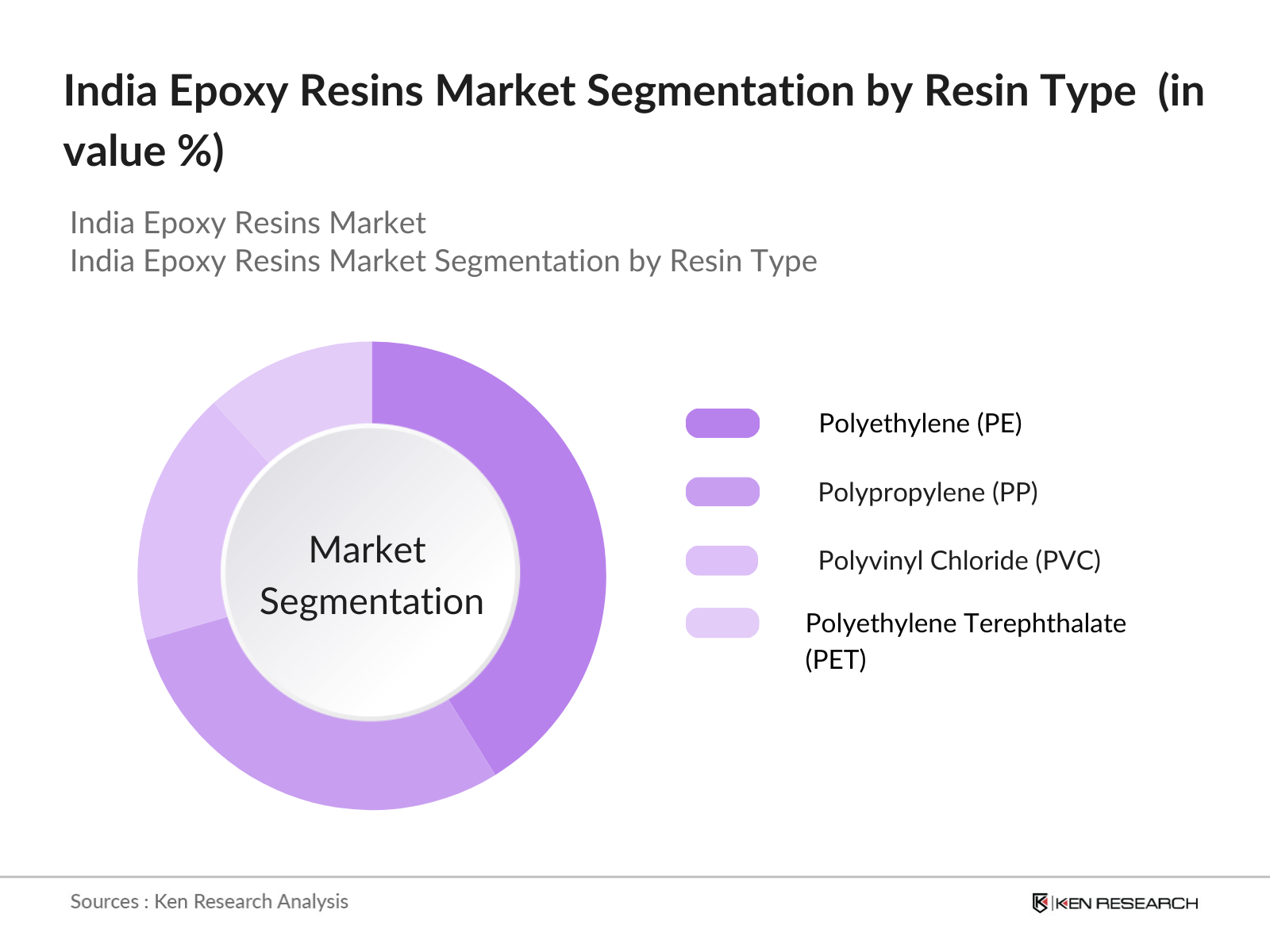

By Resin Type: The market is segmented by resin type into Polyethylene (PE) holds the largest market share due to its extensive use in packaging applications, such as plastic bags, containers, and films. Its versatility, durability, and cost-effectiveness make it a preferred choice in various industries.

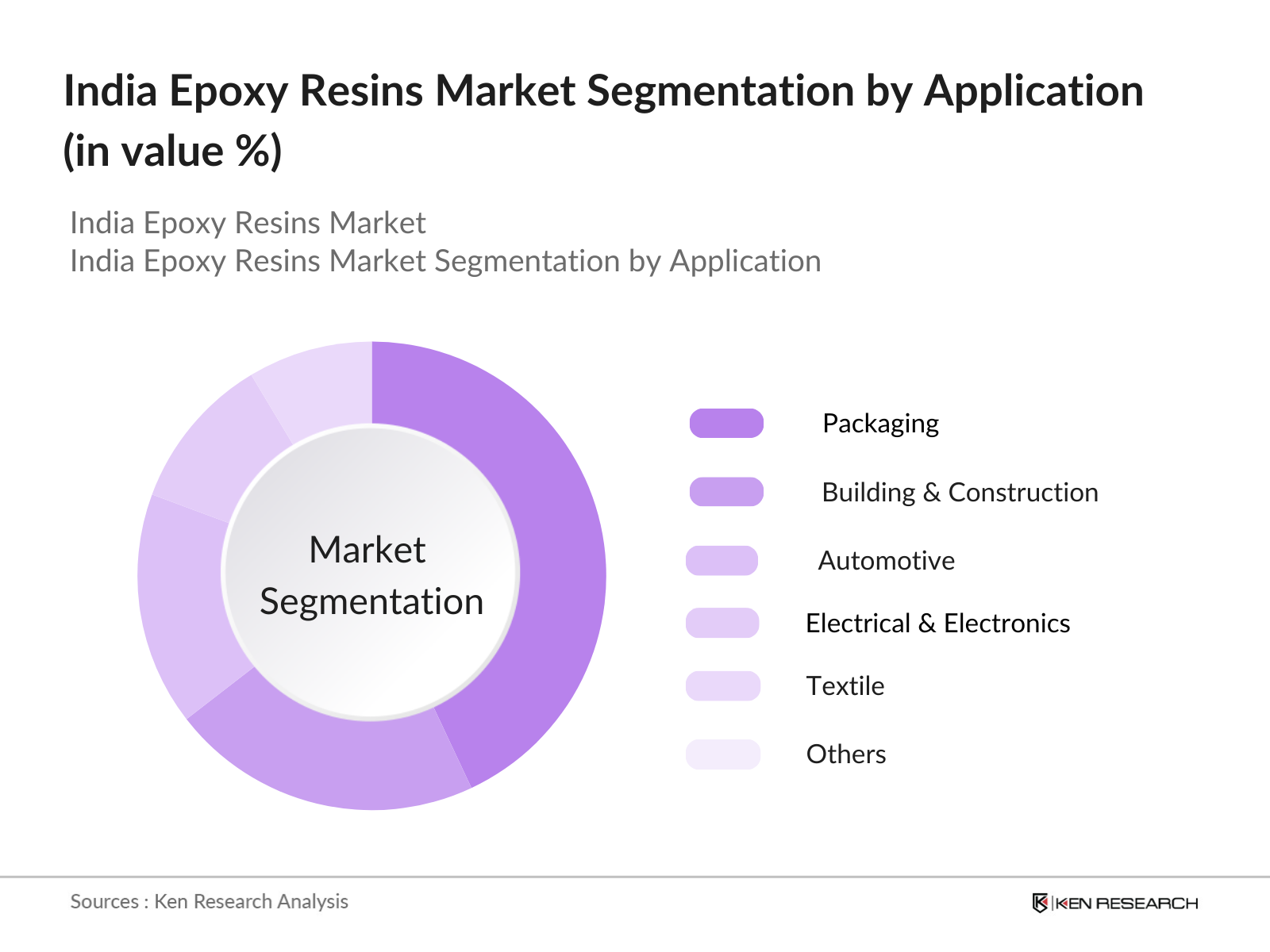

By Application: The market is further segmented by application Packaging is the dominant application segment due to the growing demand for flexible and rigid packaging solutions in the food, beverage, and consumer goods industries. The rise of e-commerce has also spurred the need for efficient packaging materials.

The India Resin Industry is highly competitive, featuring both domestic and multinational companies. Major players like Reliance Industries Limited, Indian Oil Corporation Limited, and Haldia Petrochemicals Limited dominate due to their extensive production capacities, integrated operations, and strong distribution networks. The industry is characterized by strategic collaborations, technological innovations, and expansions to increase market share. Companies are investing in R&D to develop high-performance and sustainable resins to meet evolving consumer demands and comply with environmental regulations.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (2023) |

Key Products |

R&D Investments |

Partnerships/Clients |

|

Reliance Industries Limited |

1966 |

Mumbai, India |

- |

- |

- |

- |

|

Indian Oil Corporation Limited |

1959 |

New Delhi, India |

- |

- |

- |

- |

|

Haldia Petrochemicals Limited |

1985 |

Kolkata, India |

- |

- |

- |

- |

|

Supreme Petrochem Ltd. |

1995 |

Mumbai, India |

- |

- |

- |

- |

|

ONGC Petro additions Limited (OPaL) |

2006 |

Dahej, Gujarat |

- |

- |

- |

- |

India Epoxy Resins Market Growth Drivers

India Epoxy Resins Market Challenges

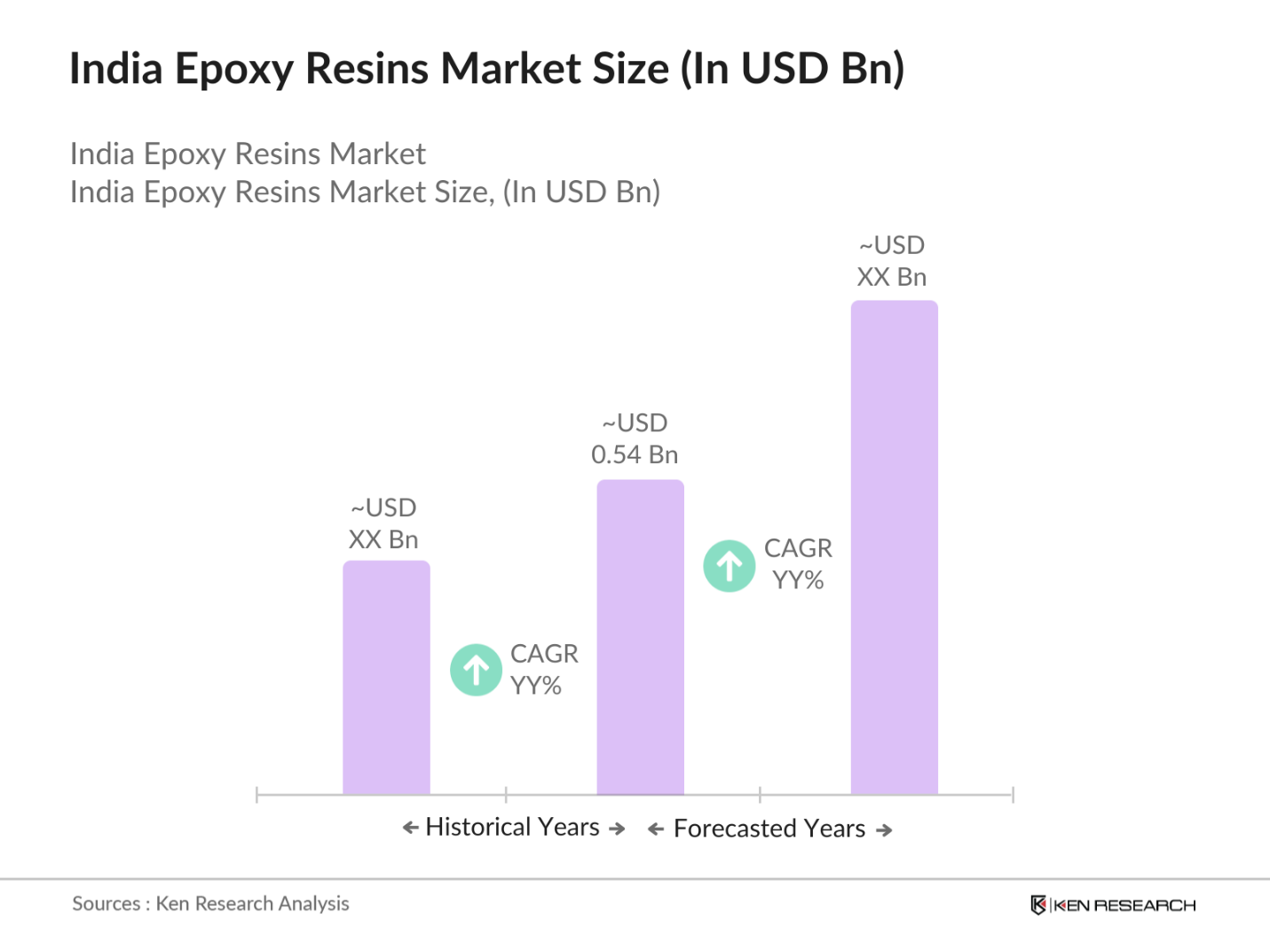

The India Epoxy Resins Market is expected to experience robust growth by 2028, with projections estimating the market size to reach around. Key factors contributing to this growth include increased demand from end-user industries, technological advancements, and government support for domestic manufacturing. The shift towards sustainable and bio-based resins presents new opportunities.

Marketing Opportunities

|

By Resin Type |

Polyethylene (PE) Polypropylene (PP) Polyvinyl Chloride (PVC) Polystyrene (PS) |

|

By Application |

Packaging Building & Construction Automotive Electrical & Electronics |

|

By End-User Industry |

Consumer Goods Healthcare Agriculture Aerospace & Defense Industrial Manufacturing |

|

By Production Process |

Injection Molding Extrusion Blow Molding Compression Molding Film Casting |

|

By Region |

North-East Midwest West Coast Southern States |

1.1. Definition and Scope

1.2. Market Valuation and Historical Analysis

1.3. Key Market Developments and Trends

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Trends Impacting Market Growth

3.1. Growth Drivers

3.1.1. Rapid Industrialization and Urbanization

3.1.2. Growth in End-User Industries

3.1.3. Government Initiatives Promoting Manufacturing

3.1.4. Technological Advancements in Resin Production

3.2. Market Challenges

3.2.1. Environmental Regulations and Compliance

3.2.2. Fluctuating Raw Material Prices

3.2.3. Competition from Low-Cost Imports

3.3. Market Opportunities

3.3.1. Development of Bio-based and Sustainable Resins

3.3.2. Expansion into Emerging Rural Markets

3.4. Future Trends

3.4.1. Growth of E-Commerce in Resin Sales

3.4.2. Shift Towards Eco-Friendly Products

4.1. By Resin Type (In Value %)

4.1.1. Polyethylene (PE)

4.1.2. Polypropylene (PP)

4.1.3. Polyvinyl Chloride (PVC)

4.1.4. Polystyrene (PS)

4.2. By Application (In Value %)

4.2.1. Packaging

4.2.2. Building & Construction

4.2.3. Automotive

4.2.4. Electrical & Electronics

4.3. By End-User Industry (In Value %)

4.3.1. Consumer Goods

4.3.2. Healthcare

4.3.3. Agriculture

4.3.4. Aerospace & Defense

4.3.5. Industrial Manufacturing

4.4. By Production Process (In Value %)

4.4.1. Injection Molding

4.4.2. Extrusion

4.4.3. Blow Molding

4.4.4. Compression Molding

4.4.5. Film Casting

4.5. By Region (In Value %)

4.5.1. North-East

4.5.2. Midwest

4.5.3. West Coast

4.5.4. Southern States

5.1. Profiles of Major Companies

5.1.1. Reliance Industries Limited

5.1.2. Indian Oil Corporation Limited

5.1.3. Haldia Petrochemicals Limited

5.1.4. Supreme Petrochem Ltd.

5.1.5. ONGC Petro additions Limited (OPaL)

5.1.6. BASF India Limited

5.1.7. Dow Chemical International Pvt. Ltd.

5.1.8. DuPont India Pvt. Ltd.

5.1.9. LG Chem India Pvt. Ltd.

5.1.10. SABIC India Pvt. Ltd.

5.2. Competitive Strategies and Market Share Analysis

5.3. Strategic Initiatives and Collaborations

5.4. Innovations and R&D Investments

06. Regulatory Framework for Epoxy Resins in India

6.1. Environmental Regulations

6.2. Compliance Standards and Certification Processes

7.1. Future Market Size Projections (In USD Billion)

7.2. Key Factors Driving Future Market Growth

08. Marketing Opportunities in the India Epoxy Resins Market

8.1. Emerging Trends and Consumer Preferences

8.2. Market Entry Strategies for New Entrants

8.3. Investment Opportunities in R&D

Extensive desk research was conducted to identify key market variables, including market size, growth trends, and key stakeholders. Sources included industry reports, government publications, and reputable news outlets.

Historical data on market size, segmentation, and growth rates were compiled. Market penetration and revenue estimates were analyzed across different segments to build a comprehensive market model.

Hypotheses were validated through interviews with industry experts, including executives from resin manufacturing companies and representatives from end-user industries. This provided insights into market dynamics, challenges, and future prospects.

All data and insights were synthesized into a detailed market report. The final output includes analysis, forecasts, and strategic recommendations for stakeholders in the India Resin Industry Market.

As of 2023, the market is estimated to be valued at around USD 0.54 billion, driven by demand from packaging, construction, and automotive industries.

Key drivers include rapid industrialization, growth in end-user industries, government initiatives promoting manufacturing, and technological advancements in resin production.

Polyethylene (PE) holds the largest market share at 35%, widely used in packaging applications due to its versatility and cost-effectiveness.

Major players include Reliance Industries Limited, Indian Oil Corporation Limited, Haldia Petrochemicals Limited, Supreme Petrochem Ltd., and ONGC Petro additions Limited (OPaL).

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.