India Flavor Market Outlook to 2030

Region:Asia

Author(s):Shubham Kashyap

Product Code:KROD2711

November 2024

89

About the Report

India Flavor Market Overview

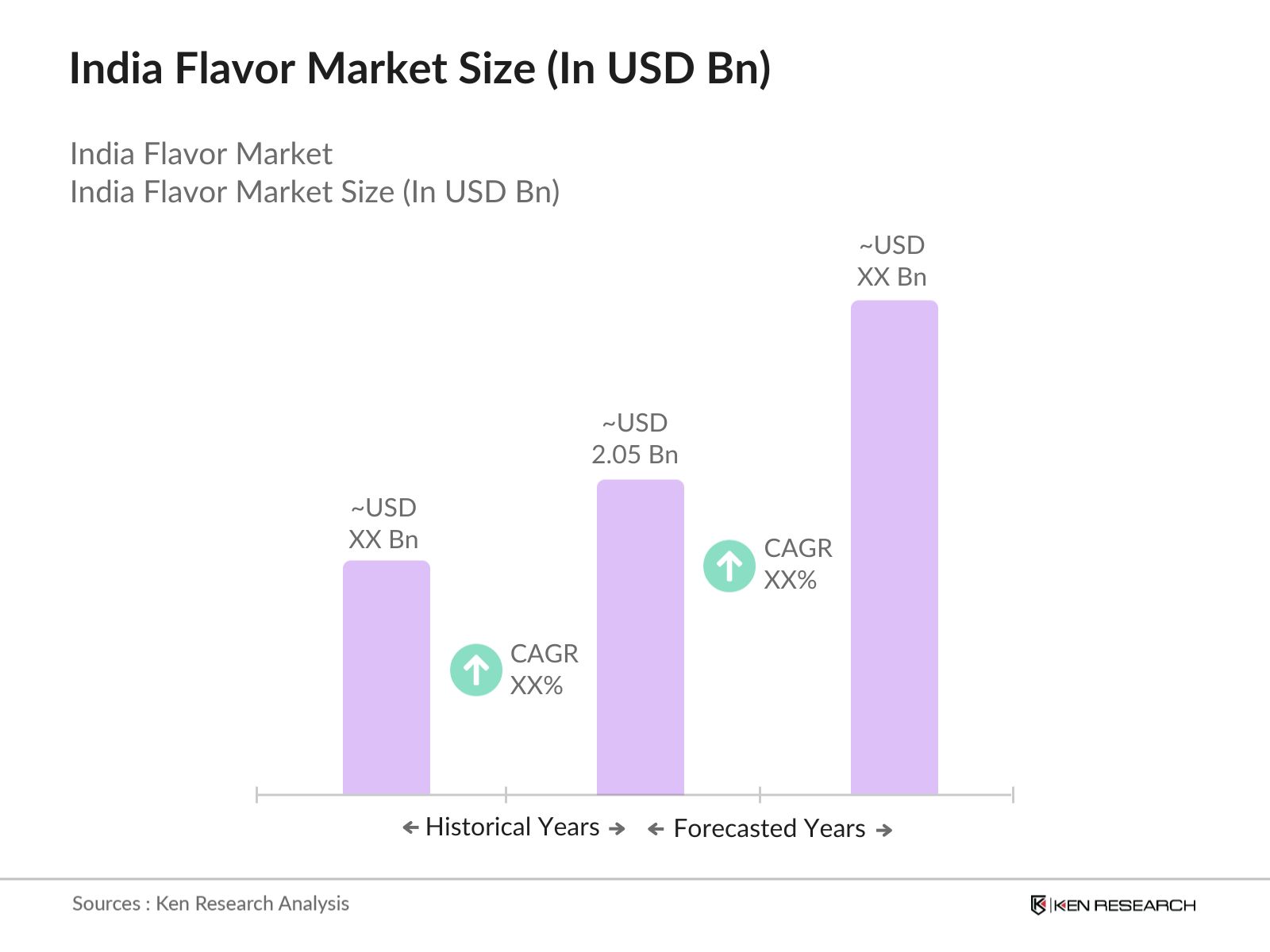

- The India flavor market is valued at USD 2.05 billion, based on a five-year historical analysis. This market's growth is primarily driven by the increasing demand for natural and organic flavors across various industries, such as food & beverages, pharmaceuticals, and personal care. With changing consumer preferences for clean-label products and healthier food options, natural flavors have gained significant traction. Additionally, the expansion of the food processing industry in India and the rise of the ready-to-eat segment are contributing to the growth of the flavor market.

- The Indian flavor market is concentrated in metropolitan cities such as Mumbai, Delhi, and Bangalore, where the food and beverage industry is well-established. These regions have a robust supply chain and infrastructure to support the flavor industry, with easy access to raw materials and a growing consumer base. Additionally, the presence of key international players and growing investments in the food processing sector are driving innovation and product development in the flavor market.

- The Food Safety and Standards Authority of India (FSSAI) has implemented stringent regulations concerning the use of food additives and flavors to ensure safety and compliance with health standards. In 2022, the FSSAI introduced new guidelines limiting the use of synthetic flavors in food products, which has accelerated the shift toward natural and organic flavor options. Compliance with these regulations is critical for manufacturers looking to capitalize on the growing demand for healthier and more sustainable flavoring solutions.

India Flavor Market Segmentation

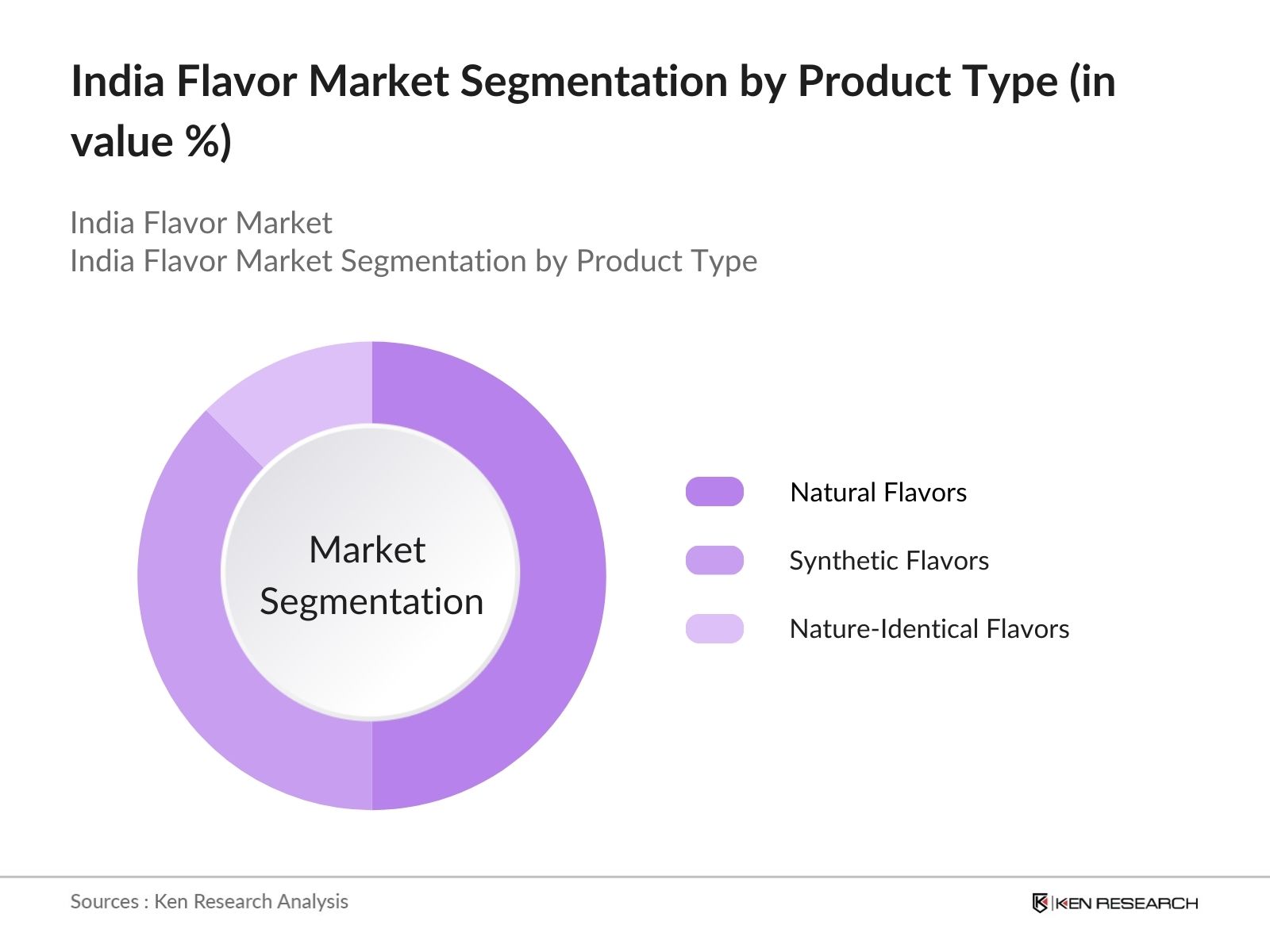

- By Flavor Type: The market is segmented by flavor type into natural flavors, synthetic flavors, and nature-identical flavors. Natural flavors dominate the market, with a growing consumer preference for clean-label products and sustainable ingredients. Companies like Givaudan, Firmenich, and Mane are leading this segment, offering a wide range of natural flavor solutions that cater to the increasing demand for organic and non-GMO products in India.

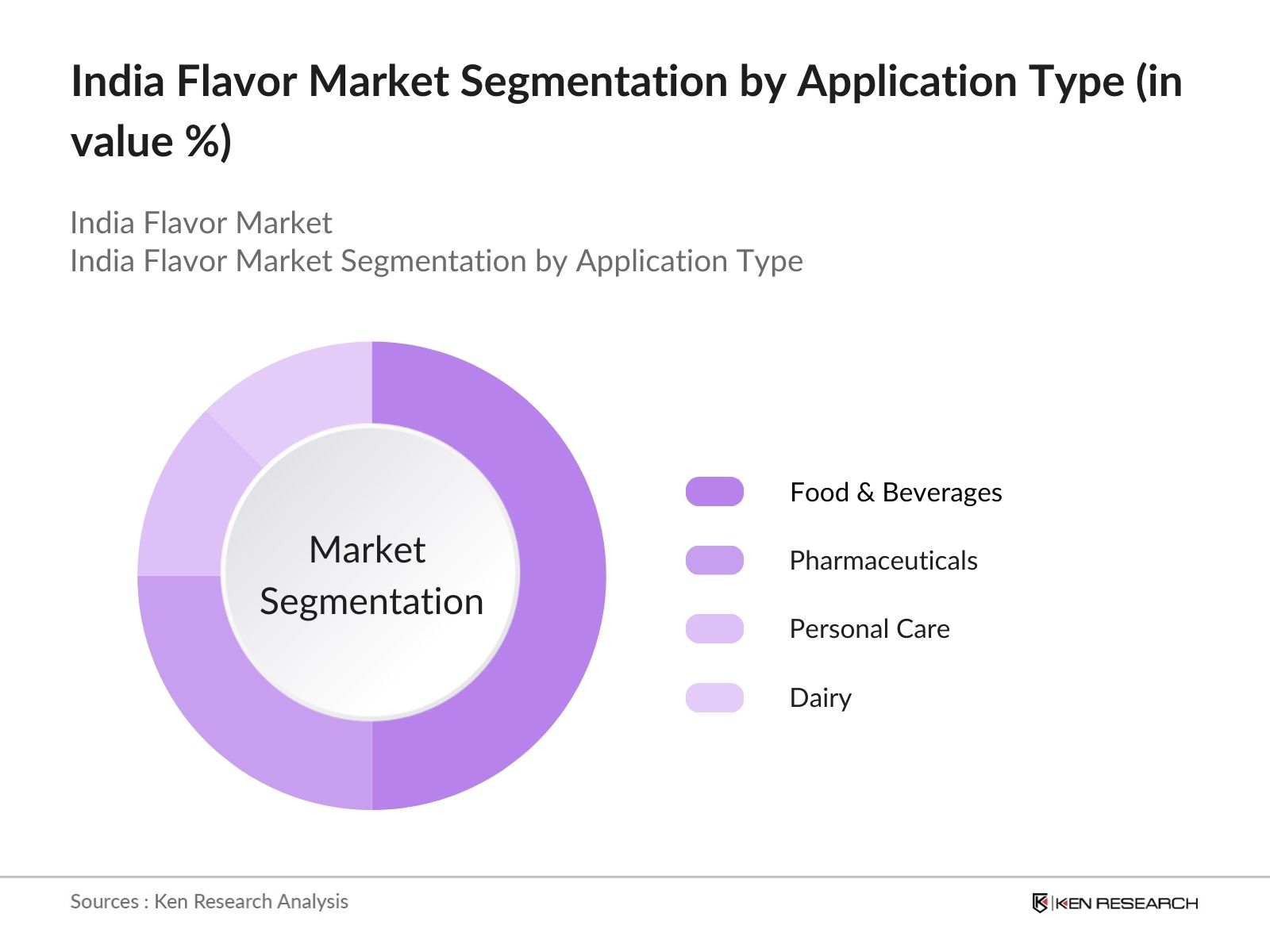

- By Application: The market is segmented by application into food & beverages, pharmaceuticals, personal care, and dairy. The food & beverages segment holds the largest market share, driven by the rise in processed food consumption and the growing demand for convenience foods. The beverage industry, particularly the soft drink and juice segments, has seen a significant uptake in natural and exotic flavor use, further boosting the market.

India Flavor Market Competitive Landscape

The India flavor market is highly competitive, with a mix of domestic and international players striving to expand their market share. Leading companies such as Givaudan, Firmenich, and Mane dominate the market through continuous innovation, mergers, and acquisitions. These companies focus on creating customized flavor solutions tailored to local preferences, contributing to their strong market presence. Indian players like Synthite and Kancor Ingredients are also gaining prominence, particularly in the natural flavor segment.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (2023) |

Employees |

Key Product |

R&D Investment |

Key Clients |

Partnerships |

|

Givaudan |

1895 |

Switzerland |

||||||

|

Firmenich |

1895 |

Switzerland |

||||||

|

Mane |

1871 |

France |

||||||

|

Synthite |

1972 |

India |

||||||

|

Kancor Ingredients |

1969 |

India |

India Flavor Industry Analysis

Growth Drivers

- Demand for Natural Ingredients:: Consumers are increasingly seeking natural ingredients in their foods and beverages. According to data from the Indian Ministry of Agriculture, the demand for natural extracts such as vanilla, ginger, and turmeric has grown significantly, with turmeric and turmeric products exports alone reaching 153,400 metric tons in 2023. This demand is driven by health-conscious consumers who prefer natural over synthetic ingredients, aligning with the growing preference for clean labels. Additionally, Indias natural flavoring ingredient production is supported by its large agricultural base, contributing to around 60% of the global spice trade in 2024.

- Expanding Processed Food Sector: The processed food industry in India is growing substantially in 2023, according to the Ministry of Food Processing Industries, continuing to drive the demand for diverse and innovative flavors. India's rising urbanization, expected to reach 540 million people by 2025, has spurred the demand for ready-to-eat and packaged food products, leading to an increased need for various flavorings to enhance food appeal. As a result, flavor manufacturers are innovating to meet this rising consumer demand, ensuring a steady supply of new flavor profiles to match the evolving food landscape

- Technological Innovation in Flavor Extraction: Indias investment in food technology, including advancements in supercritical CO2 extraction for natural flavors, has contributed to more efficient and cost-effective flavor extraction processes. The Indian Institute of Spices Research estimates that these innovations have increased flavor extraction yields substantially in 2024, allowing companies to meet growing consumer demand for high-quality natural flavors while reducing costs.

Market Challenges

- Raw Material Price Volatility: Indias agriculture sector, which supplies key flavor ingredients like cardamom and saffron, is highly susceptible to climate fluctuations, significantly impacting raw material availability. Changes in weather patterns, such as unpredictable monsoons and droughts, directly affect the yield of these crops, leading to fluctuations in supply. This scarcity drives up raw material prices, placing a financial strain on flavor manufacturers and disrupting the production of essential flavor compounds. Companies dependent on these natural ingredients must adopt strategic sourcing practices to mitigate the impact of such price volatility.

- Regulatory Hurdles: FSSAI regulations have imposed stricter guidelines on the use of synthetic flavors, including a mandate that restricts the permissible levels of artificial additives in food products. These regulatory changes have created significant challenges for flavor companies that rely on synthetic flavors, requiring them to reformulate products to meet new compliance standards. Such reformulations often involve increased research and development efforts, leading to higher production costs and extended timelines. Companies must navigate this evolving regulatory landscape while ensuring that their products maintain the same taste and quality to satisfy consumer demands.

India Flavor Market Future Outlook

The India flavor market is expected to witness substantial growth over the next five years, driven by increasing consumer demand for natural and organic products, as well as the expanding food processing industry. Innovations in flavor technology, including the development of plant-based and sustainable flavors, will play a key role in shaping the future of the market. The growing focus on health and wellness will continue to drive demand for clean-label flavors, creating opportunities for both domestic and international players in the market.

Market Opportunities

- Rising Demand for Vegan and Plant-Based Flavors: The growing popularity of plant-based diets in India has driven demand for plant-derived flavors. In 2023, plant-based product sales reached 800,000 metric tons, and this trend has led to a surge in demand for botanical and herbal flavors, such as lemongrass, mint, and curry leaves, particularly in the beverage and snack industries. This demand reflects consumers growing preference for natural and organic ingredients, which are perceived as healthier alternatives to artificial flavors.

- Expansion into the Ready-to-Eat Segment: The ready-to-eat (RTE) food segment in India has expanded rapidly, growing substantially in 2023 according to data from the National Institute of Food Technology. This has created opportunities for flavour companies to develop new and exciting taste profiles, particularly in convenience foods, as consumers look for products that replicate home-cooked flavours while saving time.

Scope of the Report

|

By Flavor |

Natural Flavors Synthetic Flavors Nature-Identical Flavors |

|

By Application |

Food & Beverages Pharmaceuticals Personal Care Dairy |

|

By Form |

Dairy Liquid Powder Paste |

|

By Source |

Paste Plant-Based Animal-Based Microbial-Based |

|

By Region |

North West East South |

Products

Key Target Audience

Food & Beverage Manufacturers

Pharmaceuticals Companies

Personal Care Product Manufacturers

Dairy Product Manufacturers

Government and Regulatory Bodies (FSSAI)

Banks and Financial Institues

Investment and Venture Capitalist Firms

Exporters and Importers of Food Ingredients

Flavors and Fragrance Manufacturers

Companies

Major Players in the India Flavor Market

Givaudan

Firmenich

Mane

Synthite Industries

Kancor Ingredients

Kerry Group

Symrise

IFF (International Flavors & Fragrances)

Takasago International

Sensient Technologies

Archer Daniels Midland (ADM)

Robertet Group

Doehler Group

McCormick & Company

T. Hasegawa Co. Ltd.

Table of Contents

01 India Flavor Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

02 India Flavor Market Size (In USD Million)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

03 India Flavor Market Analysis

3.1. Growth Drivers

Demand for Natural Ingredients

Expanding Processed Food Sector

Technological Innovation in Flavor Extraction

Consumer Shift towards Clean Label

Increase in Packaged Food Consumption3.2. Market Challenges

Raw Material Price Volatility

Regulatory Hurdles

High Competition from Unorganized Players

Consumer Preference for Local Flavors3.3. Opportunities

Rising Demand for Plant-Based Flavors

Innovation in Beverage Industry

Expanding Ready-to-Eat Segment

Growing Demand for Exotic Flavors in Food Service Industry

3.4. Trends

Preference for Organic and Sustainable Flavors

Rise of Functional and Health-Oriented Flavors

Increasing Use of Flavor Modulation in Beverages3.5. Government Regulation

FSSAI Regulations on Additives

Restrictions on Synthetic Flavoring

Food Safety Standards for Flavor Use in Pharmaceuticals

Import Tariffs on Flavor Ingredients

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

04 India Flavor Market Segmentation

4.1. By Flavor Type (In Value %)

4.1.1. Natural Flavors

4.1.2. Synthetic Flavors

4.1.3. Nature-Identical Flavors

4.2. By Application (In Value %)

4.2.1. Food & Beverages

4.2.2. Pharmaceuticals

4.2.3. Personal Care

4.2.4. Dairy

4.3. By Form (In Value %)

4.3.1. Liquid

4.3.2. Powder

4.3.3. Paste

4.4. By Source (In Value %)

4.4.1. Plant-Based

4.4.2. Animal-Based

4.4.3. Microbial-Based

4.5. By End-User (In Value %)

4.5.1. Manufacturers

4.5.2. Retail

4.5.3. Foodservice

05 India Flavor Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. Givaudan

5.1.2. Firmenich

5.1.3. Mane

5.1.4. Synthite Industries

5.1.5. Kancor Ingredients

5.1.6. Kerry Group

5.1.7. Symrise

5.1.8. IFF (International Flavors & Fragrances)

5.1.9. Takasago International

5.1.10. Sensient Technologies

5.1.11. Archer Daniels Midland (ADM)

5.1.12. Robertet Group

5.1.13. Doehler Group

5.1.14. McCormick & Company

5.1.15. T. Hasegawa Co. Ltd.

5.2. Cross Comparison Parameters (Inception Year, Headquarters, Revenue, No. of Employees, Key Clients, Market Presence, Product Portfolio, Sustainability Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Mergers & Acquisitions, New Product Launches, Strategic Partnerships, R&D Investment)

5.5. Investment Analysis

5.6. Venture Capital Funding

5.7. Private Equity Investments

06 India Flavor Market Regulatory Framework

6.1. FSSAI Guidelines on Flavoring Substances

6.2. Certification Standards for Natural and Organic Flavors

6.3. Compliance Requirements for Export-Grade Flavors

07 India Flavor Market Future Size (In USD Million)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

08 India Flavor Market Future Segmentation

8.1. By Flavor Type (In Value %)

8.2. By Application (In Value %)

8.3. By Form (In Value %)

8.4. By Source (In Value %)

8.5. By End-User (In Value %)

09 India Flavor Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the India Flavor Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the India Flavor Market. This includes assessing market penetration, the ratio of flavor companies to food and beverage manufacturers, and the resultant revenue generation. An evaluation of consumer trends and demand for clean-label products is conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple flavor manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, ensuring a comprehensive, accurate, and validated analysis of the India Flavor Market.

Frequently Asked Questions

01 How big is the India Flavor Market?

The India flavor market was valued at USD 2.05 billion in 2023, driven by increasing consumer demand for clean-label products, natural ingredients, and the expanding processed food industry.

02 What are the challenges in the India Flavor Market?

Challenges include regulatory compliance, fluctuating raw material prices, and high competition from unorganized players. Additionally, the market faces constraints related to the transition from synthetic to natural flavors, which can be cost-prohibitive for smaller companies.

03 Who are the major players in the India Flavor Market?

Key players in the market include Givaudan, Firmenich, Mane, Synthite Industries, and Kancor Ingredients. These companies dominate the market through their extensive distribution networks, product innovation, aand strong focus on natural and sustainable flavors.

04 What are the growth drivers of the India Flavor Market?

The market is propelled by the rising demand for natural and organic flavors, the expansion of the food processing industry, and growing consumer preferences for healthier and clean-label food products. Government initiatives and increased R&D investment also contribute to market growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.