India Handicrafts Market Outlook to 2030

Region:India

Author(s):Shreya Garg

Product Code:KROD6247

Region:India

Author(s):Shreya Garg

Product Code:KROD6247

December 2024

88

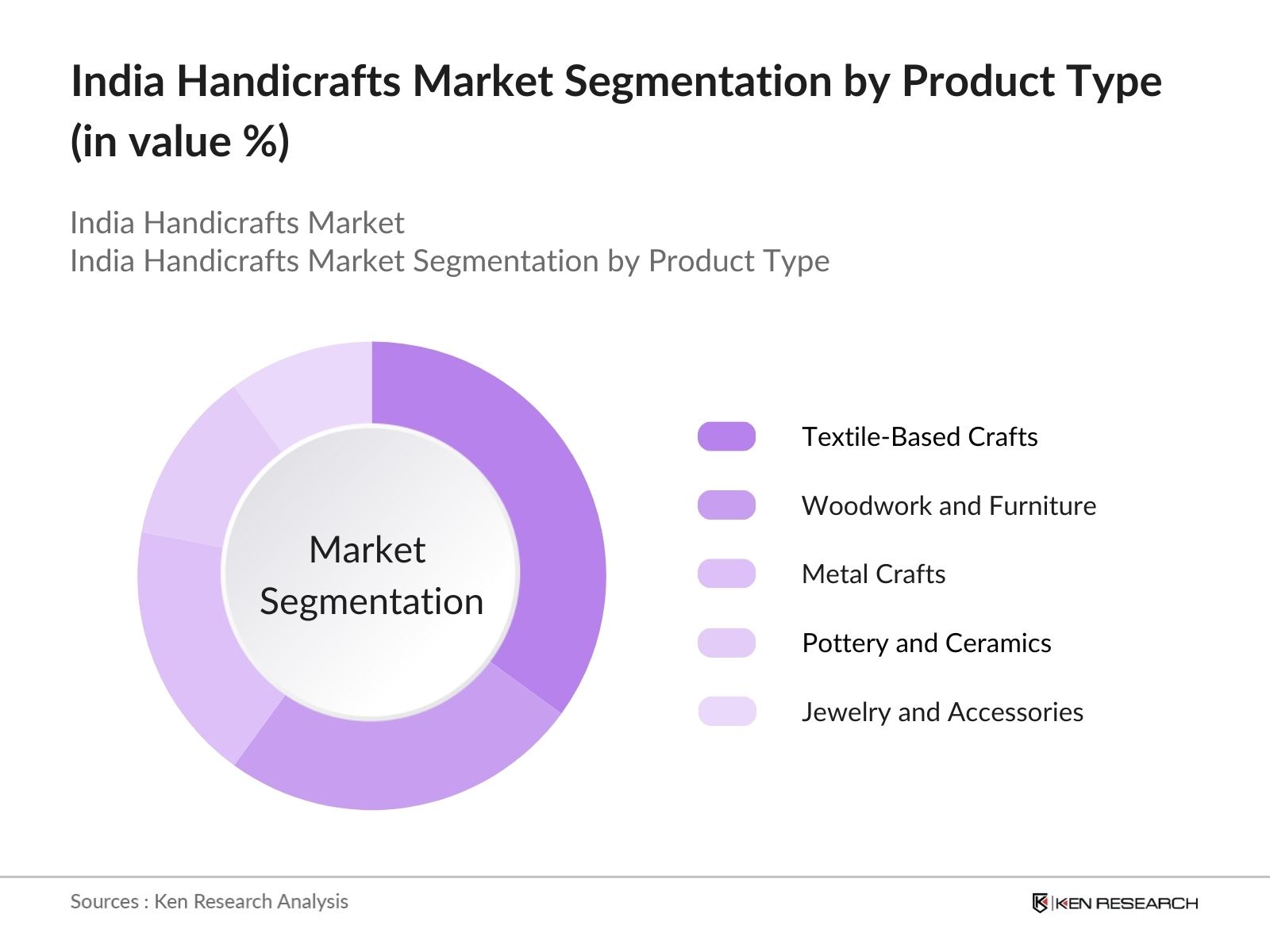

By Product Type: The market is segmented by product type into Textile-Based Crafts, Woodwork and Furniture, Metal Crafts, Pottery and Ceramics, and Jewelry and Accessories. Textile-based crafts, such as handloom and embroidery, have maintained a dominant market share due to the country's renowned expertise in these areas, driven by high domestic demand and strong international interest. Indias handloom industry is world-famous, and brands like Fabindia and Jaypore have capitalized on the popularity of authentic handwoven fabrics. This segments high demand in both fashion and home dcor further consolidates its leading position.

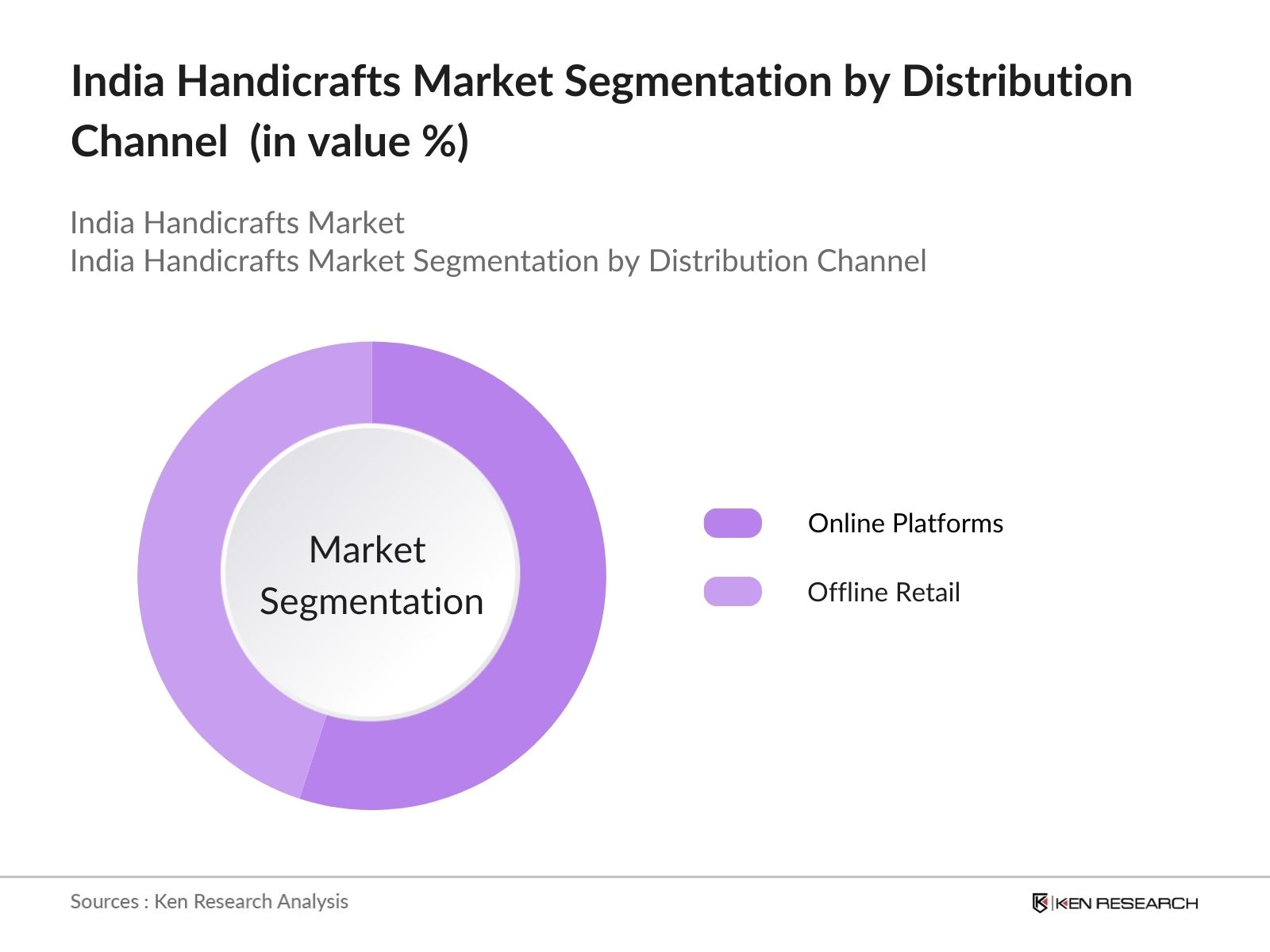

By Distribution Channel: The market is segmented by distribution channels into Offline Retail and Online Platforms. Online platforms have seen a significant surge, now capturing a dominant share of the market. This shift is driven by growing internet penetration and the rise of e-commerce giants such as Amazon and Flipkart, which have created specialized spaces for handcrafted goods. Additionally, niche platforms like Craftsvilla and Jaypore provide curated selections of handmade items, further propelling this segment. The convenience of online shopping and wider visibility for artisans are major factors contributing to this dominance.

The India Handicrafts Market is dominated by a few key players, including both domestic and international brands. Companies such as Fabindia and Craftsvilla have established strong brands by collaborating with artisans across India, while startups like Jaypore are rapidly expanding their footprint in the online space. This competitive landscape is characterized by a mix of traditional retail and digital marketplaces, with many brands focused on sustainable and eco-friendly products. The increasing influence of e-commerce platforms has also facilitated the entry of new players into the market.

|

Company Name |

Establishment Year |

Headquarters |

No. of Artisans |

Annual Revenue |

Export Percentage |

Product Range |

Online Presence |

Sustainability Initiatives |

|

Fabindia |

1960 |

|||||||

|

Tribes India |

1987 |

|||||||

|

Craftsvilla |

2011 |

|||||||

|

Rangsutra |

2006 |

|||||||

|

Jaypore |

2012 |

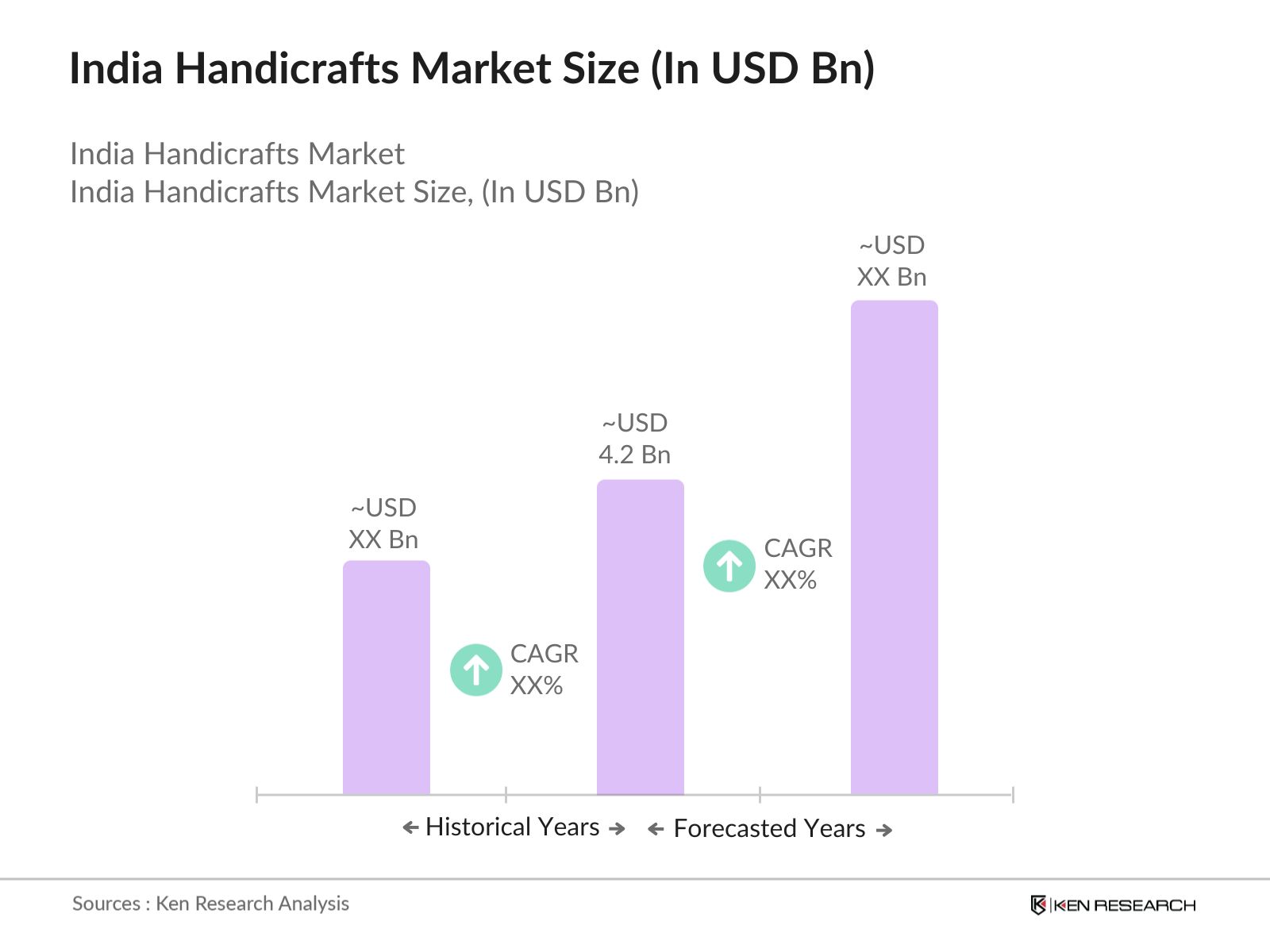

Over the next few years, the India Handicrafts Market is expected to experience robust growth, driven by rising consumer awareness of sustainable and handmade products, along with increasing government support for the handicrafts industry. The expansion of online platforms and global marketplaces like Amazon, coupled with collaborations between modern designers and traditional artisans, will further boost market demand. Additionally, the emphasis on eco-friendly production processes will help artisans tap into niche global markets. The introduction of new policies aimed at improving the livelihood of artisans, such as access to financial services and training programs, will also contribute to the markets positive outlook.

|

Product Type |

Textile-Based Crafts Woodwork and Furniture Metal Crafts Pottery and Ceramics Jewelry and Accessories |

|

Craft Techniques |

Handloom Weaving Embroidery Block Printing Metal Engraving Pottery |

|

End-User Industry |

Home Dcor Apparel and Fashion Jewelry and Accessories Office and Institutional Gifts and Souvenirs |

|

Distribution Channel |

Offline Retail Online Platforms Export |

|

Region |

North India South India West India East India |

1.1. Definition and Scope

1.2. Market Taxonomy (Handicrafts Product Types, Craft Techniques, Raw Materials)

1.3. Market Growth Rate (Handicraft Sector Growth, Export Value Trends, Domestic Demand)

1.4. Market Segmentation Overview (Regional Distribution, Product Types, End-User Industries)

2.1. Historical Market Size (Export and Domestic Market Trends)

2.2. Year-On-Year Growth Analysis (Segment-wise and Region-wise Growth)

2.3. Key Market Developments and Milestones (Government Schemes, Trade Agreements, Skill Development Programs)

3.1. Growth Drivers

3.1.1. Increasing Global Demand for Ethnic and Handmade Products

3.1.2. Rising E-commerce Adoption for Handicrafts

3.1.3. Government Support and Schemes (Artisans Welfare Programs, Export Incentives)

3.1.4. Focus on Sustainability and Eco-Friendly Products

3.2. Market Challenges

3.2.1. Lack of Organized Supply Chain and Standardization

3.2.2. Price Competition from Machine-Made Products

3.2.3. Limited Access to Modern Design and Marketing Expertise

3.2.4. Dependence on Traditional Export Channels

3.3. Opportunities

3.3.1. Digital Transformation and Global Marketplaces

3.3.2. Collaborations with Modern Designers and Luxury Brands

3.3.3. Penetration into Untapped Domestic Markets (Rural and Semi-Urban Areas)

3.3.4. Niche Markets for Personalized and Custom Handmade Products

3.4. Trends

3.4.1. Integration of Technology in Handicrafts Production (3D Printing, AI-Enhanced Designs)

3.4.2. Revival of Traditional Craft Techniques (Handloom, Pottery, Embroidery)

3.4.3. Rise in Sustainable and Ethical Crafting Practices

3.4.4. Growth of Craft-Based Tourism (Craft Villages, Fairs, and Festivals)

3.5. Government Regulation

3.5.1. Geographical Indication (GI) Certification for Handicraft Products

3.5.2. Artisans Livelihood and Welfare Initiatives

3.5.3. Import-Export Regulation Framework

3.5.4. Financial Assistance Schemes (Mudra Loans, Credit Linkages)

3.6. SWOT Analysis (Strengths: Cultural Heritage, Weaknesses: Fragmented Market, Opportunities: Global Markets, Threats: Competition from Imitations)

3.7. Stakeholder Ecosystem (Artisans, Traders, E-commerce Platforms, Export Agencies)

3.8. Porters Five Forces (Bargaining Power of Buyers, Supplier Power, Competitive Rivalry, Threat of New Entrants, Substitutes)

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Textile-Based Crafts (Handloom, Embroidery, Block Printing)

4.1.2. Woodwork and Furniture

4.1.3. Metal Crafts (Brass, Silver, Copper)

4.1.4. Pottery and Ceramics

4.1.5. Jewelry and Accessories (Beads, Stonework)

4.2. By Craft Techniques (In Value %)

4.2.1. Handloom Weaving

4.2.2. Embroidery

4.2.3. Block Printing

4.2.4. Metal Engraving

4.2.5. Pottery

4.3. By End-User Industry (In Value %)

4.3.1. Home Dcor

4.3.2. Apparel and Fashion

4.3.3. Jewelry and Accessories

4.3.4. Office and Institutional

4.3.5. Gifts and Souvenirs

4.4. By Distribution Channel (In Value %)

4.4.1. Offline Retail (Craft Fairs, Specialty Stores, Artisans Showrooms)

4.4.2. Online Platforms (E-commerce, Handicraft Marketplaces)

4.4.3. Export (Wholesale, Trade Fairs, Direct Export)

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. West India

4.5.4. East India

5.1 Detailed Profiles of Major Companies

5.1.1. Tribes India

5.1.2. Fabindia

5.1.3. Dastkar

5.1.4. The India Craft House

5.1.5. Gaatha

5.1.6. Rangsutra

5.1.7. Craftsvilla

5.1.8. Jaypore

5.1.9. Chumbak

5.1.10. Nappa Dori

5.1.11. Bombay Store

5.1.12. The Sandalwood Room

5.1.13. Earth Loaf

5.1.14. Kamala

5.1.15. Indian Artisans Online

5.2 Cross Comparison Parameters (Number of Artisans, Annual Revenue, Export Percentage, Product Range, Online Presence, Partnerships, Craft Type, Sustainability Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Marketing Campaigns, Artisans Training Programs)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants for Handicrafts Industry

5.8. Private Equity Investments in Handicrafts

6.1. Geographical Indications (GI) Act for Handicrafts

6.2. Export Licensing Requirements

6.3. Compliance with Environmental Regulations

6.4. Artisan Welfare and Skill Development Policies

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type

8.2. By Craft Techniques

8.3. By End-User Industry

8.4. By Distribution Channel

8.5. By Region

9.1. TAM/SAM/SOM Analysis

9.2. Consumer Behavior Analysis

9.3. Market Entry Strategies for New Players

9.4. White Space Opportunity Analysis

The initial phase involves mapping out the key stakeholders, including artisans, export bodies, and e-commerce platforms within the India Handicrafts Market. Desk research using both proprietary databases and secondary research will be employed to compile data regarding market drivers, constraints, and opportunities.

In this step, historical data will be analyzed to assess the revenue generated by different segments of the handicrafts industry. Factors such as regional export trends, domestic demand, and the impact of government initiatives on market dynamics will be considered for a comprehensive analysis.

Market assumptions will be validated through detailed interviews with industry experts, including artisans, market players, and government representatives. These consultations will provide deeper insights into the operational dynamics, helping validate market hypotheses and further refine data accuracy.

The final phase involves direct interaction with key industry players and governmental bodies to confirm the findings. These insights will be integrated into a final report, ensuring all data is validated and provides a holistic overview of the India Handicrafts Market.

The India Handicrafts Market is valued at INR 4.2 billion, driven by the rising global demand for sustainable and culturally rich handcrafted products, supported by initiatives such as government-led export programs.

Challenges include the lack of organized supply chains, price competition from mass-produced goods, and limited access to modern design and marketing expertise for artisans.

Key players include Fabindia, Craftsvilla, Jaypore, Tribes India, and The India Craft House. These companies dominate the market due to their strong artisan collaborations, extensive product range, and robust online and offline presence.

The growth drivers include the increasing global demand for eco-friendly handmade products, rising e-commerce adoption, government support for artisans, and the revival of traditional craft techniques.

Opportunities lie in expanding global exports, penetrating rural and untapped domestic markets, and increasing collaborations between traditional artisans and modern designers to cater to niche markets.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.