India Hospital Market Outlook to 2030

Region:India

Author(s):Naman Rohilla

Product Code:KROD3397

Region:India

Author(s):Naman Rohilla

Product Code:KROD3397

November 2024

87

The India Hospitals Market is segmented by ownership, service type, specialty type, bed capacity, and geographical region.

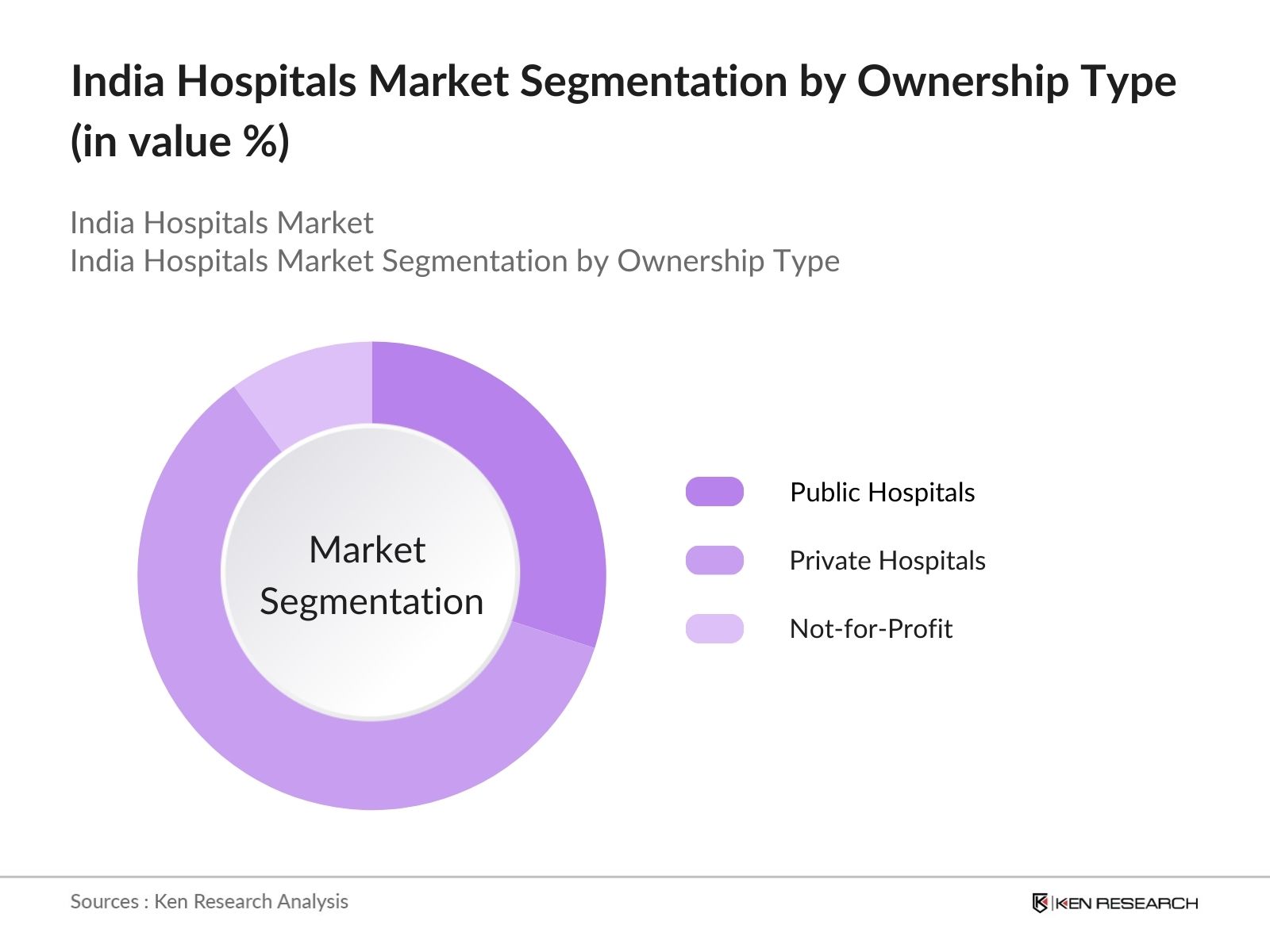

By Ownership: India's hospital market is segmented by ownership into public hospitals, private hospitals, and not-for-profit hospitals. Private hospitals hold a dominant market share due to their state-of-the-art infrastructure, high-quality care, and quicker service delivery. They also attract a number of international patients due to their specialization in complex surgeries and advanced treatments. In contrast, public hospitals are often overburdened, affecting the overall patient experience.

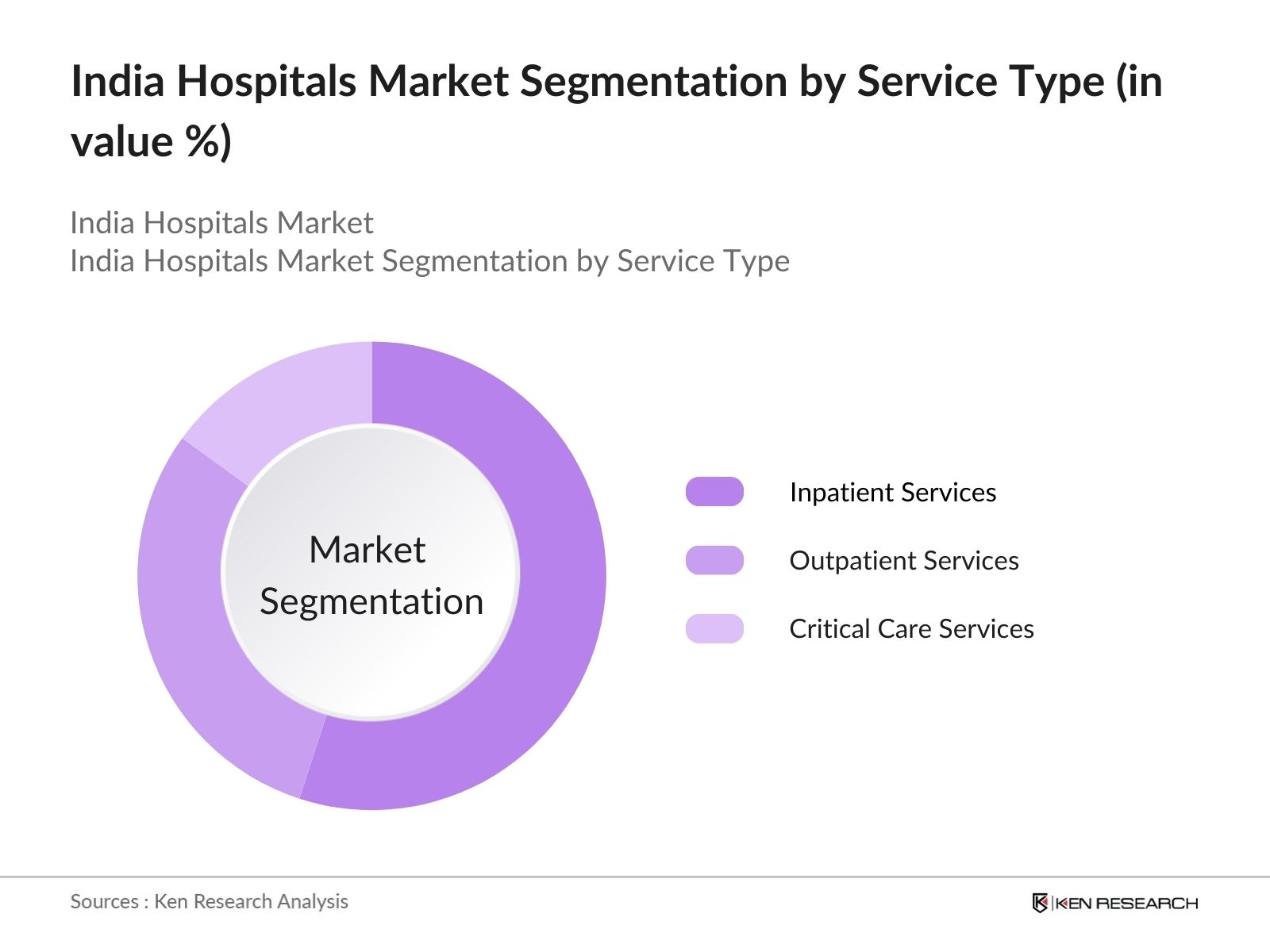

By Service Type: The India Hospitals market is segmented by service type into inpatient services, outpatient services, and critical care services. Inpatient services dominate the market, primarily because hospitals focus on advanced and specialized treatments requiring extended stays, such as cardiac surgeries, organ transplants, and cancer treatments. These services are essential for maintaining continuous care and patient monitoring, which is a key factor driving their dominance.

The India Hospitals market is dominated by major private and corporate players that have well-established healthcare networks and offer a wide range of specialized services. These key players are known for their investments in healthcare technologies, partnerships with global healthcare providers, and expansion into Tier 2 and Tier 3 cities to capture new patient demographics.

|

Company |

Year of Establishment |

Headquarters |

Revenue |

Number of Beds |

Geographic Presence |

Specialty Focus |

Medical Tourism Share |

|

Apollo Hospitals |

1983 |

Chennai |

- |

- |

- |

- |

- |

|

Fortis Healthcare |

2001 |

Gurgaon |

- |

- |

- |

- |

- |

|

Max Healthcare |

2000 |

New Delhi |

- |

- |

- |

- |

- |

|

Narayana Health |

2000 |

Bengaluru |

- |

- |

- |

- |

- |

|

Manipal Hospitals |

1953 |

Bengaluru |

- |

- |

- |

- |

- |

Over the next five years, the India Hospitals market is expected to witness growth driven by government initiatives, advancements in medical technologies, and rising health awareness. Continuous investment in infrastructure, along with the expansion of healthcare services into underserved regions, will contribute to this growth. The rise of digital health platforms and telemedicine services will also play a crucial role in improving healthcare accessibility across the country.

|

Ownership |

Public Hospitals Private Hospitals Not-for-Profit Hospitals |

|

Specialty Type |

Multi-Specialty Hospitals Specialty Hospitals |

|

Service Type |

Inpatient Services Outpatient Services Critical Care Services |

|

Region |

North India South India East India West India |

|

Bed Capacity |

Small (0-100 beds) Medium (100-300 beds) Large (300+ beds) |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (Hospital Infrastructure, Digital Health, Healthcare Spending, Medical Tourism)

3.1.1. Government Investments in Healthcare

3.1.2. Rise of Specialized and Multi-Specialty Hospitals

3.1.3. Growth in Medical Tourism

3.1.4. Increasing Demand for Critical Care Services

3.2. Market Challenges (Healthcare Workforce, Cost Management, Patient Access)

3.2.1. Shortage of Skilled Healthcare Professionals

3.2.2. High Operational Costs

3.2.3. Limited Access to Rural Areas

3.2.4. Complex Regulatory Landscape

3.3. Opportunities (Technological Advancements, Telemedicine, Private Sector Growth)

3.3.1. Adoption of AI and Telemedicine

3.3.2. Expansion of Hospital Chains in Tier 2 & 3 Cities

3.3.3. Health Insurance Expansion

3.4. Trends (Digital Transformation, Preventive Healthcare, Mergers & Acquisitions)

3.4.1. Digitalization and EHR Implementation

3.4.2. Rise of Preventive and Wellness Healthcare Programs

3.4.3. Hospital Chains and Corporate Collaborations

3.5. Government Initiatives (Ayushman Bharat, National Digital Health Mission)

3.5.1. Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (AB-PMJAY)

3.5.2. National Digital Health Mission (NDHM)

3.5.3. Public-Private Partnerships (PPPs) in Healthcare

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Hospitals, Medical Device Suppliers, Insurance Companies)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Ownership (In Value %)

4.1.1. Public Hospitals

4.1.2. Private Hospitals

4.1.3. Not-for-Profit Hospitals

4.2. By Specialty Type (In Value %)

4.2.1. Multi-Specialty Hospitals

4.2.2. Specialty Hospitals (Cardiology, Oncology, Orthopedics)

4.3. By Service Type (In Value %)

4.3.1. Inpatient Services

4.3.2. Outpatient Services

4.3.3. Critical Care Services

4.4. By Region (In Value %)

4.4.1. North India

4.4.2. South India

4.4.3. East India

4.4.4. West India

4.5. By Bed Capacity (In Value %)

4.5.1. Small (0-100 beds)

4.5.2. Medium (100-300 beds)

4.5.3. Large (300+ beds)

5.1. Detailed Profiles of Major Companies (Market Share, Recent Developments, Strategic Initiatives)

5.1.1. Apollo Hospitals

5.1.2. Fortis Healthcare

5.1.3. Max Healthcare

5.1.4. Narayana Health

5.1.5. Manipal Hospitals

5.1.6. Care Hospitals

5.1.7. Medanta The Medicity

5.1.8. Kokilaben Dhirubhai Ambani Hospital

5.1.9. Columbia Asia Hospitals

5.1.10. Aster DM Healthcare

5.1.11. BLK Super Specialty Hospital

5.1.12. Global Hospitals

5.1.13. Dr. Agarwals Eye Hospitals

5.1.14. Vasan Eye Care

5.1.15. Shalby Hospitals

5.2. Cross Comparison Parameters (Revenue, Bed Capacity, Ownership Model, Patient Footfall, Hospital Infrastructure, Geographic Footprint, Digital Health Initiatives, Medical Tourism Statistics)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Healthcare Accreditation (NABH, JCI)

6.2. Compliance Requirements (Clinical Establishments Act, Healthcare Safety Regulations)

6.3. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Ownership

8.2. By Specialty Type

8.3. By Service Type

8.4. By Region

8.5. By Bed Capacity

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsIn the first stage, we identified major stakeholders in the India Hospitals Market by conducting desk research and using proprietary databases to collect industry-specific data. The goal was to define the most critical variables influencing market growth, such as healthcare infrastructure development, patient demographics, and healthcare spending.

Historical data for the India Hospitals Market was analyzed, focusing on market growth rates, key player revenue, and hospital occupancy rates. The analysis also included a study of patient satisfaction and healthcare quality metrics to ensure accurate revenue projections and market penetration analysis.

To validate market hypotheses, we consulted with industry experts through phone interviews and surveys. These consultations provided in-depth insights into hospital operations, investment trends, and service demand, helping us to verify the accuracy of our data and market projections.

In the final phase, we engaged with healthcare providers and manufacturers to validate the gathered data. This direct engagement enabled us to cross-check statistics and ensure the completeness and accuracy of our analysis, leading to the development of a comprehensive market report.

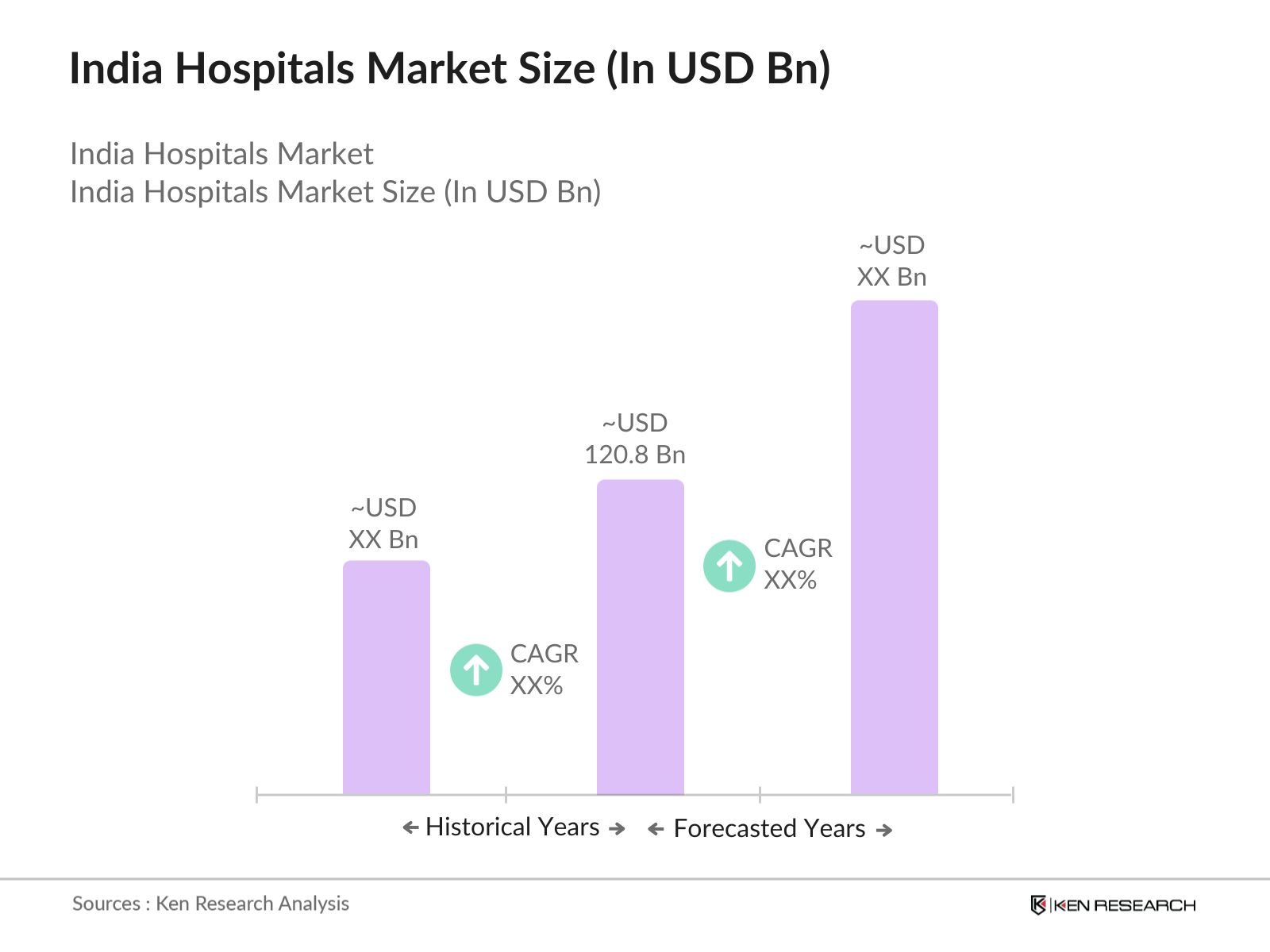

The India Hospitals market is valued at USD 120.8 billion, driven by increasing healthcare spending, technological advancements, and a growing demand for specialised services across Tier 1 and Tier 2 cities.

Challenges include a shortage of skilled healthcare professionals, rising operational costs, and limited access to healthcare services in rural areas. Regulatory complexities and high competition among private hospitals further complicate the market landscape.

Major players include Apollo Hospitals, Fortis Healthcare, Max Healthcare, Narayana Health, and Manipal Hospitals, which dominate due to their extensive networks, advanced healthcare services, and strong brand presence.

Key growth drivers include government healthcare initiatives, rising medical tourism, an aging population, and technological advancements in medical equipment and telemedicine services.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.