India Hospitals Market Outlook to 2030

Region:Asia

Author(s):Vijay Kumar

Product Code:KROD7055

November 2024

82

About the Report

India Hospitals Market Overview

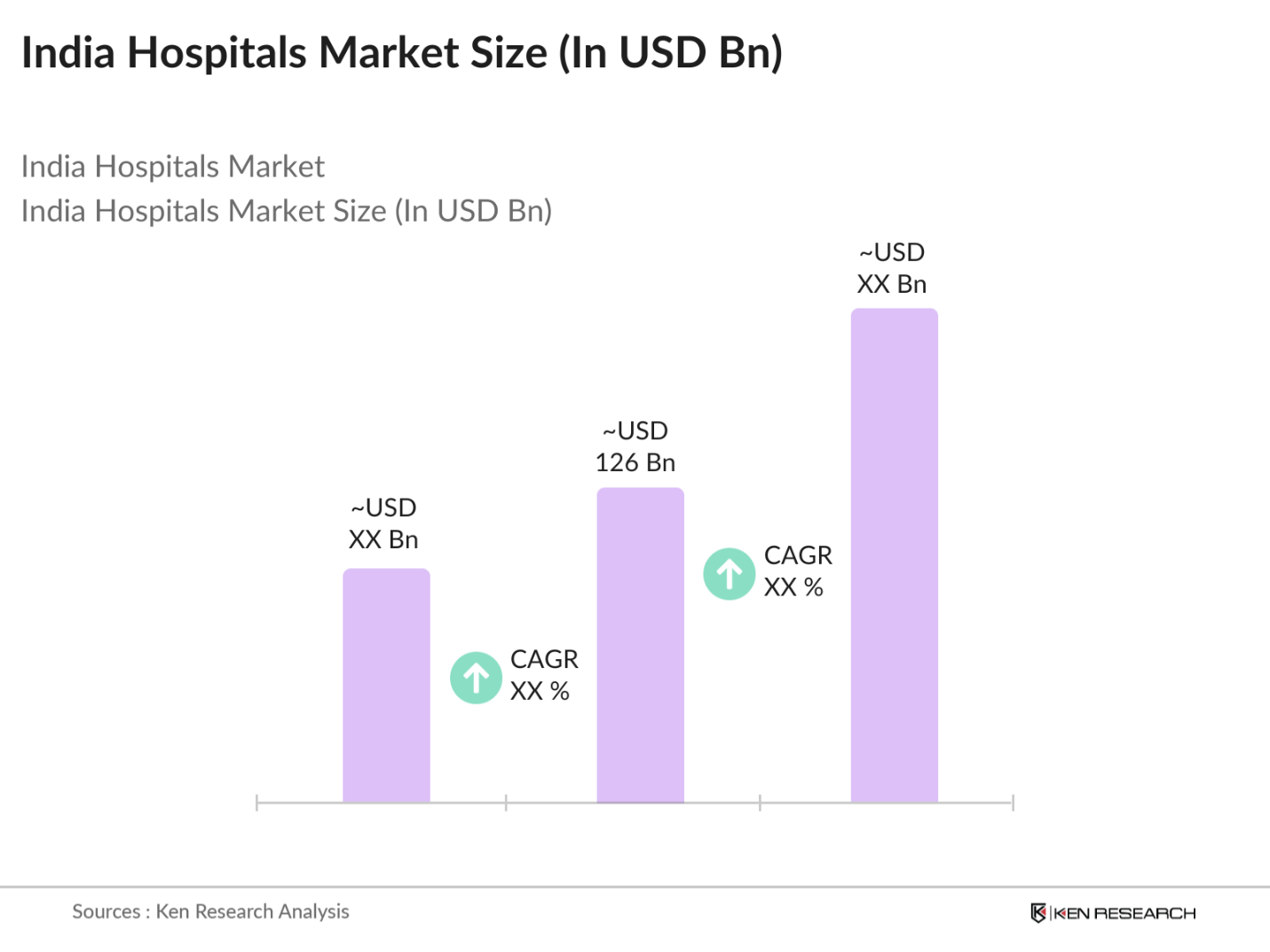

- The India hospitals market is valued at USD 126 billion, based on a five-year historical analysis. This market is primarily driven by the growing population, increasing healthcare spending, and government initiatives like Ayushman Bharat, which aims to provide universal healthcare coverage. Additionally, the rise of medical tourism, improvements in healthcare infrastructure, and the expansion of private hospitals have contributed significantly to the markets growth, especially in urban regions where demand for advanced healthcare services is on the rise.

- Cities such as Delhi, Mumbai, and Bangalore dominate the Indian hospitals market due to their concentration of advanced healthcare facilities, specialized hospitals, and robust medical infrastructure. These metropolitan areas are home to a majority of multi-specialty hospitals, high-end healthcare services, and top medical professionals, attracting not only domestic but international patients as well. The dominance of these cities is further bolstered by strong government support and private sector investments.

- Hospitals in India are increasingly seeking accreditation from bodies such as the National Accreditation Board for Hospitals & Healthcare Providers (NABH) and Joint Commission International (JCI) to ensure quality standards. As of 2023, over 1,000 hospitals have NABH accreditation, which mandates strict quality control measures and patient safety protocols. Accreditation is becoming a critical requirement for hospitals, especially those catering to international patients, as it enhances their credibility and competitiveness in the market.

India Hospitals Market Segmentation

By Type of Hospital: Indias hospital market is segmented by type into public hospitals, private hospitals, specialty hospitals, multispecialty hospitals, and teaching hospitals. Recently, private hospitals have held a dominant market share in India under this segmentation due to their increasing numbers and the superior quality of care provided compared to public hospitals.

By Service Type: In the India hospitals market, inpatient services have a dominant share in the service type segmentation. This dominance is largely due to the comprehensive treatment packages and long-term care these services offer for both critical and chronic health conditions. The high frequency of complex surgeries and long-term hospitalization requirements for severe conditions make inpatient services a key revenue generator for hospitals.

India Hospitals Market Competitive Landscape

The India hospitals market is dominated by a combination of domestic and international healthcare giants. These companies have established a significant presence across India, offering a wide array of services ranging from general healthcare to super-specialized treatments. The competitive landscape is marked by rapid expansion, mergers and acquisitions, and technological advancements, as well as a focus on enhancing the patient experience.

India Hospitals Industry Analysis

Growth Drivers

- Population Growth and Urbanization: India's population, reaching over 1.43 billion by mid-2024, continues to fuel the demand for healthcare services. The United Nations estimates that over 36% of the population now lives in urban areas, where the demand for hospitals and advanced healthcare facilities is increasing. Rapid urbanization, particularly in cities like Delhi, Mumbai, and Bangalore, has heightened the pressure on existing healthcare infrastructure, urging private and public sectors to expand hospital capacities.

- Rising Demand for Advanced Healthcare Services: The demand for advanced healthcare services in India is rising sharply, driven by an increase in chronic diseases like diabetes, cardiovascular conditions, and cancer. The World Health Organization reports that India accounts for over 77 million cases of diabetes, significantly increasing the need for hospitals with specialized services. Additionally, a growing middle-class population with access to health insurance is contributing to the demand for tertiary care hospitals.

- Increased Healthcare Expenditure (Government & Private): India's healthcare spending has seen significant growth, with the government allocating INR 2.23 trillion to the healthcare sector in the 2023 budget, up from INR 1.98 trillion in 2022. This increased spending supports the expansion and modernization of public hospitals across the country. Private healthcare expenditure is also on the rise, driven by a growing affluent population seeking advanced treatment in private hospitals.

Market Challenges

- Infrastructure Constraints in Rural Areas: Despite improvements in urban healthcare, rural areas continue to face significant infrastructure challenges. The National Rural Health Mission reports that there are only 25,000 public health centers across rural India, serving over 800 million people. These centers are often under-equipped and understaffed, creating a disparity between rural and urban healthcare services.

- Skilled Workforce Shortage: India faces a severe shortage of skilled healthcare workers, including doctors, nurses, and allied professionals. According to the World Bank, India has only 9.26 doctors per 10,000 people, which is far below the WHOs recommended minimum of 23 doctors per 10,000 people. This shortage is particularly pronounced in rural areas and smaller towns, making it difficult for hospitals to maintain adequate staffing levels.

India Hospitals Market Future Outlook

Over the next five years, the India hospitals market is poised for substantial growth, driven by rising healthcare demand, increased government spending on healthcare infrastructure, and a growing focus on digital health solutions. The rapid expansion of private hospitals and the continuing influx of foreign investments into India's healthcare sector are also anticipated to fuel market growth.

Market Opportunities

- Growth in Medical Tourism: India has emerged as a leading destination for medical tourism, attracting patients from across the globe due to its affordable yet high-quality healthcare services. In 2023, India welcomed over 500,000 medical tourists, with popular treatments including orthopedic surgeries, cardiac care, and cancer treatments. Medical tourists contribute significantly to the hospital market, particularly in cities like Chennai, Delhi, and Mumbai, where specialized hospitals cater to international patients.

- Adoption of Telemedicine and Digital Health: The adoption of telemedicine has seen a rapid surge in India, particularly following the COVID-19 pandemic. The National Health Digital Mission, launched by the government, aims to digitize healthcare records and facilitate telemedicine services across the country. As of 2023, over 100 million teleconsultations had been conducted through various platforms, significantly expanding access to healthcare in rural areas.

Scope of the Report

|

By Type of Hospital |

Public Hospitals Private Hospitals Specialty Hospitals Multispecialty Hospitals Teaching Hospitals |

|

By Service Type |

Inpatient Services Outpatient Services Emergency Services Diagnostic and Imaging Services Telemedicine Services |

|

By Ownership |

Government-Owned Private Owned Public-Private Partnership (PPP) |

|

By Bed Capacity |

Less than 50 Beds 51-200 Beds 201-500 Beds More than 500 Beds |

|

By Region |

North India South India East India West India |

Products

Key Target Audience

Hospital Operators & Administrators

Government and Regulatory Bodies (Ministry of Health and Family Welfare, NABH)

Healthcare Investors

Private Equity Firms

Venture Capitalists

Medical Device Manufacturers

Insurance Companies

Healthcare IT Providers

Companies

Players Mentioned in the Report

Apollo Hospitals

Fortis Healthcare

Narayana Health

Max Healthcare

Manipal Hospitals

Aster DM Healthcare

CARE Hospitals

Columbia Asia Hospitals

Medanta - The Medicity

Global Hospitals

Table of Contents

1. India Hospitals Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. India Hospitals Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. India Hospitals Market Analysis

3.1. Growth Drivers

3.1.1. Population Growth and Urbanization

3.1.2. Rising Demand for Advanced Healthcare Services

3.1.3. Increased Healthcare Expenditure (Government & Private)

3.1.4. Expansion of Private Hospitals Chains

3.2. Market Challenges

3.2.1. Infrastructure Constraints in Rural Areas

3.2.2. Skilled Workforce Shortage

3.2.3. Regulatory and Compliance Issues

3.2.4. High Operating Costs

3.3. Opportunities

3.3.1. Growth in Medical Tourism

3.3.2. Adoption of Telemedicine and Digital Health

3.3.3. Expansion of Specialty Care Hospitals

3.3.4. Government Support for Infrastructure Development (Pradhan Mantri Jan Arogya Yojana, Ayushman Bharat)

3.4. Trends

3.4.1. Hospital Consolidations & Strategic Collaborations

3.4.2. Growing Focus on Patient Experience and Technology Adoption

3.4.3. Use of AI and Robotics in Healthcare

3.4.4. Rise of Outpatient Care Models (Daycare Surgeries)

3.5. Government Regulation

3.5.1. National Health Policy

3.5.2. Accreditation Standards (NABH, JCI)

3.5.3. Healthcare Financing and PPP Initiatives

3.5.4. Incentives for Healthcare Infrastructure

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. India Hospitals Market Segmentation

4.1. By Type of Hospital (In Value %)

4.1.1. Public Hospitals

4.1.2. Private Hospitals

4.1.3. Specialty Hospitals

4.1.4. Multispecialty Hospitals

4.1.5. Teaching Hospitals

4.2. By Service Type (In Value %)

4.2.1. Inpatient Services

4.2.2. Outpatient Services

4.2.3. Emergency Services

4.2.4. Diagnostic and Imaging Services

4.2.5. Telemedicine Services

4.3. By Ownership (In Value %)

4.3.1. Government-Owned

4.3.2. Private Owned

4.3.3. Public-Private Partnership (PPP)

4.4. By Bed Capacity (In Value %)

4.4.1. Less than 50 Beds

4.4.2. 51-200 Beds

4.4.3. 201-500 Beds

4.4.4. More than 500 Beds

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. East India

4.5.4. West India

5. India Hospitals Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Apollo Hospitals

5.1.2. Fortis Healthcare

5.1.3. Narayana Health

5.1.4. Max Healthcare

5.1.5. Manipal Hospitals

5.1.6. Aster DM Healthcare

5.1.7. CARE Hospitals

5.1.8. Columbia Asia Hospitals

5.1.9. Medanta - The Medicity

5.1.10. Global Hospitals

5.1.11. Hiranandani Hospitals

5.1.12. AIIMS (All India Institute of Medical Sciences)

5.1.13. Wockhardt Hospitals

5.1.14. Sakra World Hospital

5.1.15. KIMS Hospitals

5.2. Cross Comparison Parameters

5.2.1. Number of Employees

5.2.2. Headquarters

5.2.3. Year of Inception

5.2.4. Revenue

5.2.5. Number of Beds

5.2.6. Specialization Areas

5.2.7. Hospital Network

5.2.8. Key Partnerships

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Subsidies

5.9. Private Equity Investments

6. India Hospitals Market Regulatory Framework

6.1. Healthcare Compliance and Licensing

6.2. Accreditation Standards (NABH, JCI)

6.3. Healthcare Data Security Laws

6.4. Government Schemes for Infrastructure Development

7. India Hospitals Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. India Hospitals Future Market Segmentation

8.1. By Type of Hospital (In Value %)

8.2. By Service Type (In Value %)

8.3. By Ownership (In Value %)

8.4. By Bed Capacity (In Value %)

8.5. By Region (In Value %)

9. India Hospitals Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

In this phase, we map the ecosystem of the India Hospitals Market, incorporating key stakeholders such as healthcare providers, regulators, and investors. Comprehensive desk research utilizing secondary data sources helps identify the variables driving market dynamics, such as hospital infrastructure development, patient care services, and healthcare policy impacts.

Step 2: Market Analysis and Construction

Here, historical data is analyzed to assess market penetration, growth rates, and patient flow across different types of hospitals. The analysis includes metrics like bed capacity utilization, the revenue generated by various hospital types, and regional growth trends, ensuring accurate insights into the market's current standing.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through in-depth interviews with healthcare industry experts, including hospital administrators and policy analysts. These consultations provide qualitative insights that help refine data points and predictions about future market trends.

Step 4: Research Synthesis and Final Output

The final output is produced by synthesizing primary and secondary data into a comprehensive report, ensuring that the insights provided reflect both the top-down (macro) and bottom-up (micro) views of the India Hospitals Market.

Frequently Asked Questions

01. How big is the India Hospitals Market?

The India hospitals market is valued at USD 126 billion, based on a five-year historical analysis. This market is primarily driven by the growing population, increasing healthcare spending, and government initiatives like Ayushman Bharat, which aims to provide universal healthcare coverage.

02. What are the challenges in the India Hospitals Market?

The market faces challenges such as infrastructure constraints in rural areas, a shortage of skilled healthcare professionals, and high operational costs, especially for private hospitals that must maintain high-quality standards.

03. Who are the major players in the India Hospitals Market?

Key players include Apollo Hospitals, Fortis Healthcare, Narayana Health, Max Healthcare, and Manipal Hospitals. These companies dominate due to their extensive hospital networks, advanced medical infrastructure, and ability to attract both domestic and international patients.

04. What are the growth drivers of the India Hospitals Market?

The market is propelled by the increasing demand for healthcare services, medical tourism, digital health solutions like telemedicine, and government initiatives such as Ayushman Bharat that aim to provide universal healthcare coverage.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.