India Housing Finance Market Outlook to 2030

Region:India

Author(s):Naman Rohilla

Product Code:KROD6928

Region:India

Author(s):Naman Rohilla

Product Code:KROD6928

December 2024

81

The India Housing Finance market is dominated by several major players, including both public sector banks and private financial institutions. Companies like HDFC and LIC Housing Finance have a stronghold due to their vast networks and tailored products, while newer FinTech players are introducing innovation into the space, offering digital-first mortgage solutions.

|

Company Name |

Establishment Year |

Headquarters |

Loan Portfolio (INR Cr) |

Digital Lending Initiatives |

NPA (%) |

Market Share (%) |

No. of Branches |

ESG Initiatives |

|

Housing Development Finance Corp. |

1977 |

Mumbai |

- |

- |

- |

- |

- |

- |

|

State Bank of India |

1955 |

Mumbai |

- |

- |

- |

- |

- |

- |

|

LIC Housing Finance Ltd. |

1989 |

Mumbai |

- |

- |

- |

- |

- |

- |

|

ICICI Bank |

1994 |

Mumbai |

- |

- |

- |

- |

- |

- |

|

Indiabulls Housing Finance Ltd. |

2000 |

New Delhi |

- |

- |

- |

- |

- |

- |

Over the next five years, the India Housing Finance market is expected to witness robust growth driven by continued government initiatives promoting affordable housing, coupled with increasing urbanization and a growing middle-class population. The rise of FinTech lenders providing digital mortgage solutions and the development of green housing finance products will also contribute to the expansion of the market. Additionally, lower interest rates and innovative loan products are expected to further fuel demand for home loans in both metropolitan and tier-2 cities.

|

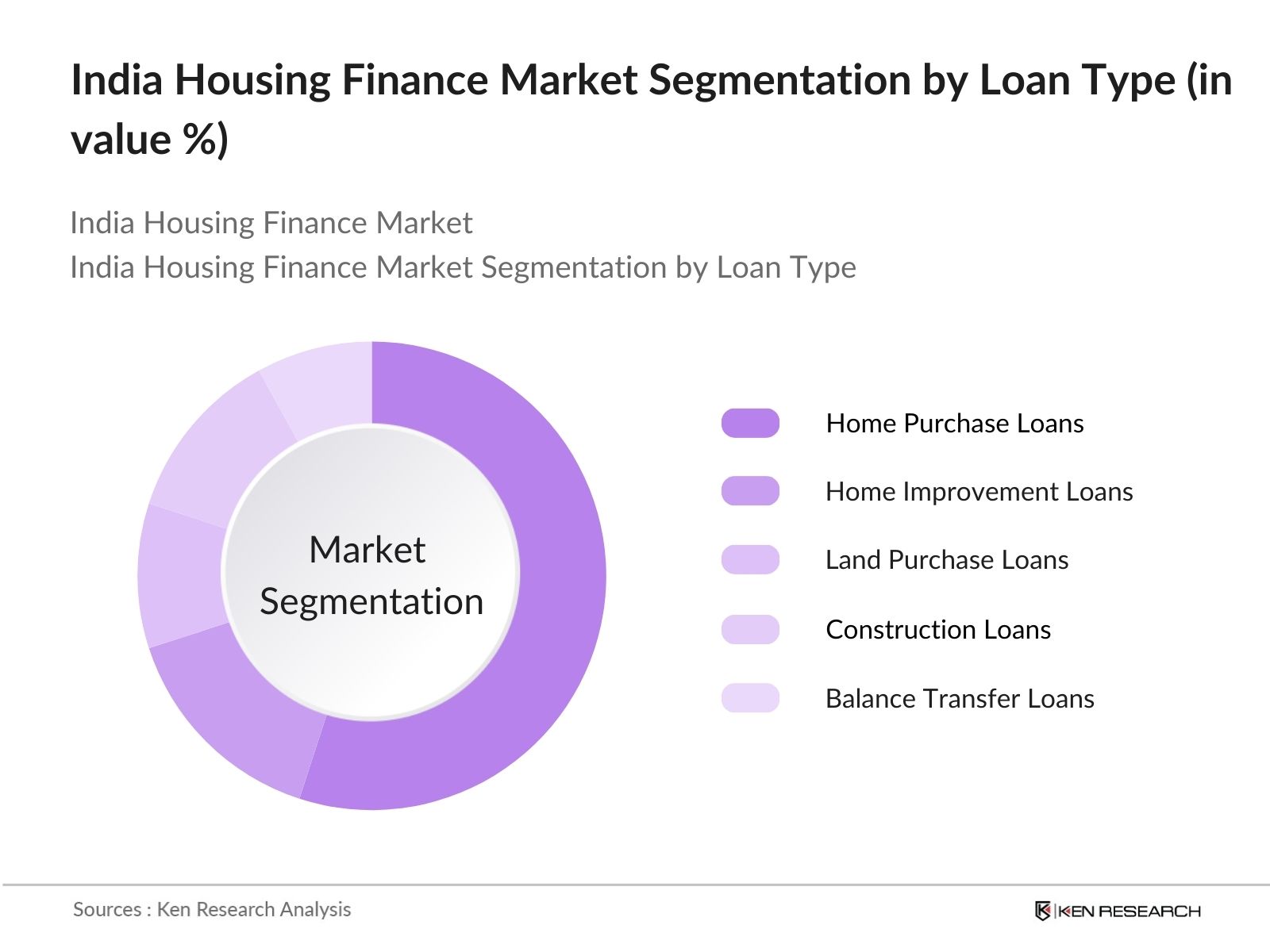

Loan Type |

Home Purchase Loans Home Improvement Loans Land Purchase Loans Construction Loans Balance Transfer Loans |

|

End-User |

Individuals Developers Institutions |

|

Interest Rate Type |

Fixed Rate Floating Rate Hybrid Rate |

|

Provider Type |

Public Sector Banks Private Sector Banks Housing Finance Companies (HFCs) Non-Banking Financial Companies (NBFCs) FinTech Lenders |

|

Region |

Northern India Southern India Eastern India Western India |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Urbanization and Housing Demand

3.1.2 Government Schemes (e.g., PMAY, Housing for All)

3.1.3 Interest Rate Dynamics

3.1.4 Rising Middle-Class Population

3.2 Market Challenges

3.2.1 Regulatory Constraints

3.2.2 Non-Performing Assets (NPA) in Housing Finance

3.2.3 Access to Affordable Credit

3.3 Opportunities

3.3.1 Digitalization of Housing Finance

3.3.2 Growth in Affordable Housing Segment

3.3.3 Entry of FinTech in Mortgage Solutions

3.4 Trends

3.4.1 Increasing Adoption of AI for Credit Scoring

3.4.2 Rise of Green Housing Loans

3.4.3 Integration of Blockchain in Loan Processing

3.5 Government Regulations

3.5.1 RBI Guidelines for Housing Finance

3.5.2 Affordable Housing Fund (AHF) Policies

3.5.3 Regulatory Framework on Loan-to-Value (LTV) Ratios

3.6 SWOT Analysis

3.7 Stake Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competition Ecosystem

4.1 By Loan Type (In Value %)

4.1.1 Home Purchase Loans

4.1.2 Home Improvement Loans

4.1.3 Land Purchase Loans

4.1.4 Construction Loans

4.1.5 Balance Transfer Loans

4.2 By End-User (In Value %)

4.2.1 Individuals

4.2.2 Developers

4.2.3 Institutions

4.3 By Interest Rate Type (In Value %)

4.3.1 Fixed Rate

4.3.2 Floating Rate

4.3.3 Hybrid Rate

4.4 By Provider Type (In Value %)

4.4.1 Public Sector Banks

4.4.2 Private Sector Banks

4.4.3 Housing Finance Companies (HFCs)

4.4.4 Non-Banking Financial Companies (NBFCs)

4.4.5 FinTech Lenders

4.5 By Region (In Value %)

4.5.1 Northern India

4.5.2 Southern India

4.5.3 Eastern India

4.5.4 Western India

5.1 Detailed Profiles of Major Companies

5.1.1 Housing Development Finance Corporation (HDFC)

5.1.2 State Bank of India (SBI)

5.1.3 ICICI Bank

5.1.4 LIC Housing Finance Ltd.

5.1.5 Indiabulls Housing Finance Ltd.

5.1.6 PNB Housing Finance Ltd.

5.1.7 Axis Bank

5.1.8 Bajaj Finserv

5.1.9 Bank of Baroda

5.1.10 Canara Bank

5.1.11 DHFL

5.1.12 Tata Capital Housing Finance

5.1.13 Kotak Mahindra Bank

5.1.14 Reliance Home Finance

5.1.15 Piramal Capital & Housing Finance Ltd.

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Loan Portfolio, Market Share, NPA %, Digital Lending Initiatives, ESG Compliance)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 Housing Finance Guidelines by NHB

6.2 Compliance Requirements for Housing Finance Companies

6.3 Certification Processes for Affordable Housing Loans

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Loan Type (In Value %)

8.2 By End-User (In Value %)

8.3 By Interest Rate Type (In Value %)

8.4 By Provider Type (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsThis initial phase involved identifying key variables such as loan portfolios, market penetration, and government schemes, which influence the dynamics of the India Housing Finance Market. Extensive desk research using secondary databases was conducted to gather relevant data.

We compiled and analyzed historical data on housing loan disbursements, interest rate trends, and policy impacts. The aim was to understand market dynamics and gauge future projections.

Experts from housing finance companies, real estate developers, and policymakers were consulted through interviews. Their insights provided critical validation of the trends identified during the desk research.

This step involved synthesizing findings into a comprehensive report. Data from both primary and secondary sources were combined to ensure a holistic and accurate portrayal of the market.

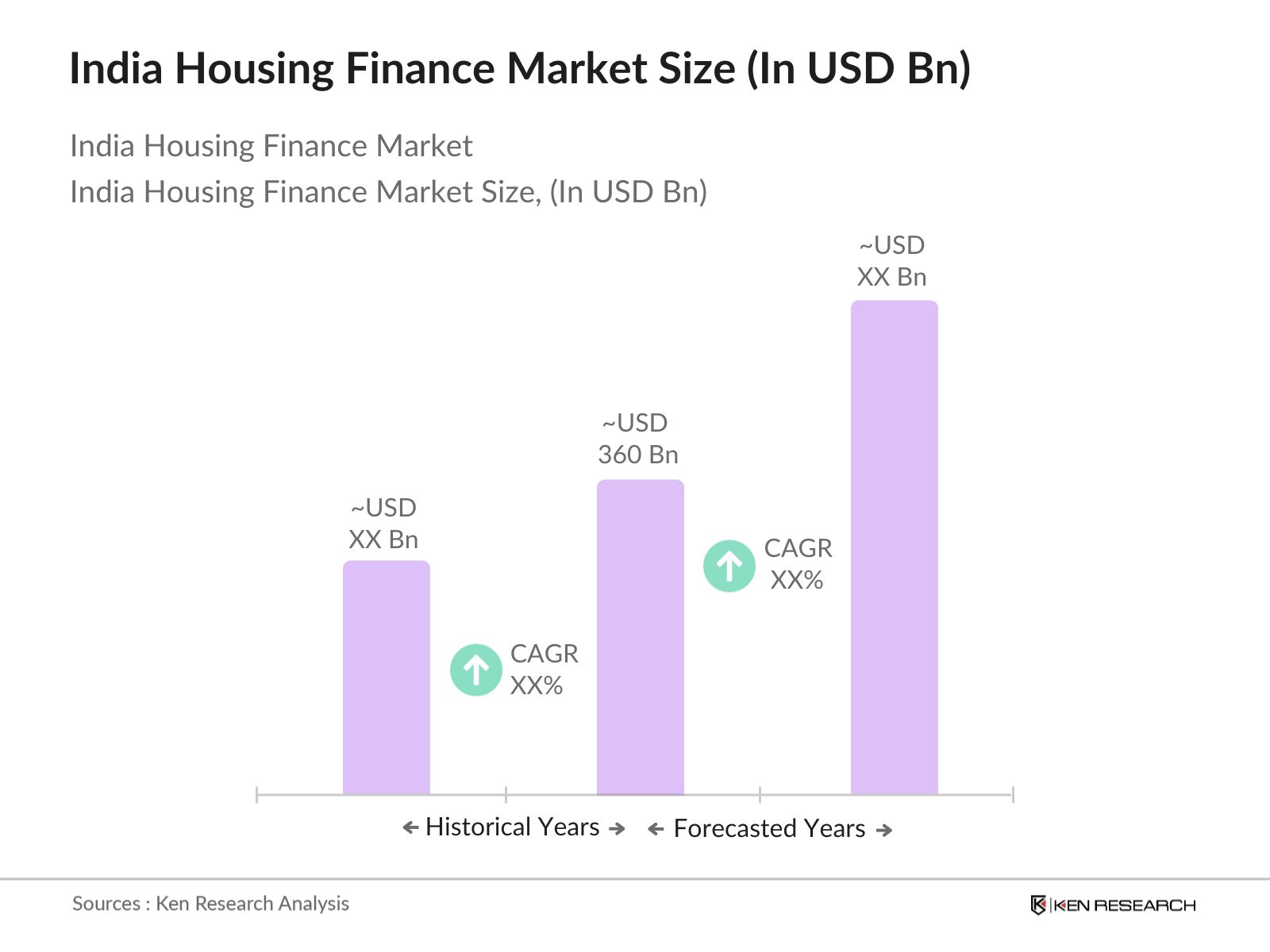

The India Housing Finance Market is valued at USD 360 billion, driven by government schemes promoting affordable housing and increasing urban migration.

Challenges in the India Housing Finance Market include regulatory constraints, non-performing assets (NPA) issues, and the limited availability of affordable credit options for low-income consumers.

Key players in the India Housing Finance Market include Housing Development Finance Corporation (HDFC), State Bank of India, LIC Housing Finance Ltd., Indiabulls Housing Finance Ltd., and ICICI Bank.

Growth drivers of the India Housing Finance Market include urbanization, the increasing middle-class population, government schemes such as PMAY, and the rise of digital mortgage solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.