India Hydropower Market Outlook to 2030

Region:India

Author(s):Shambhavi

Product Code:KROD2085

Region:India

Author(s):Shambhavi

Product Code:KROD2085

December 2024

90

|

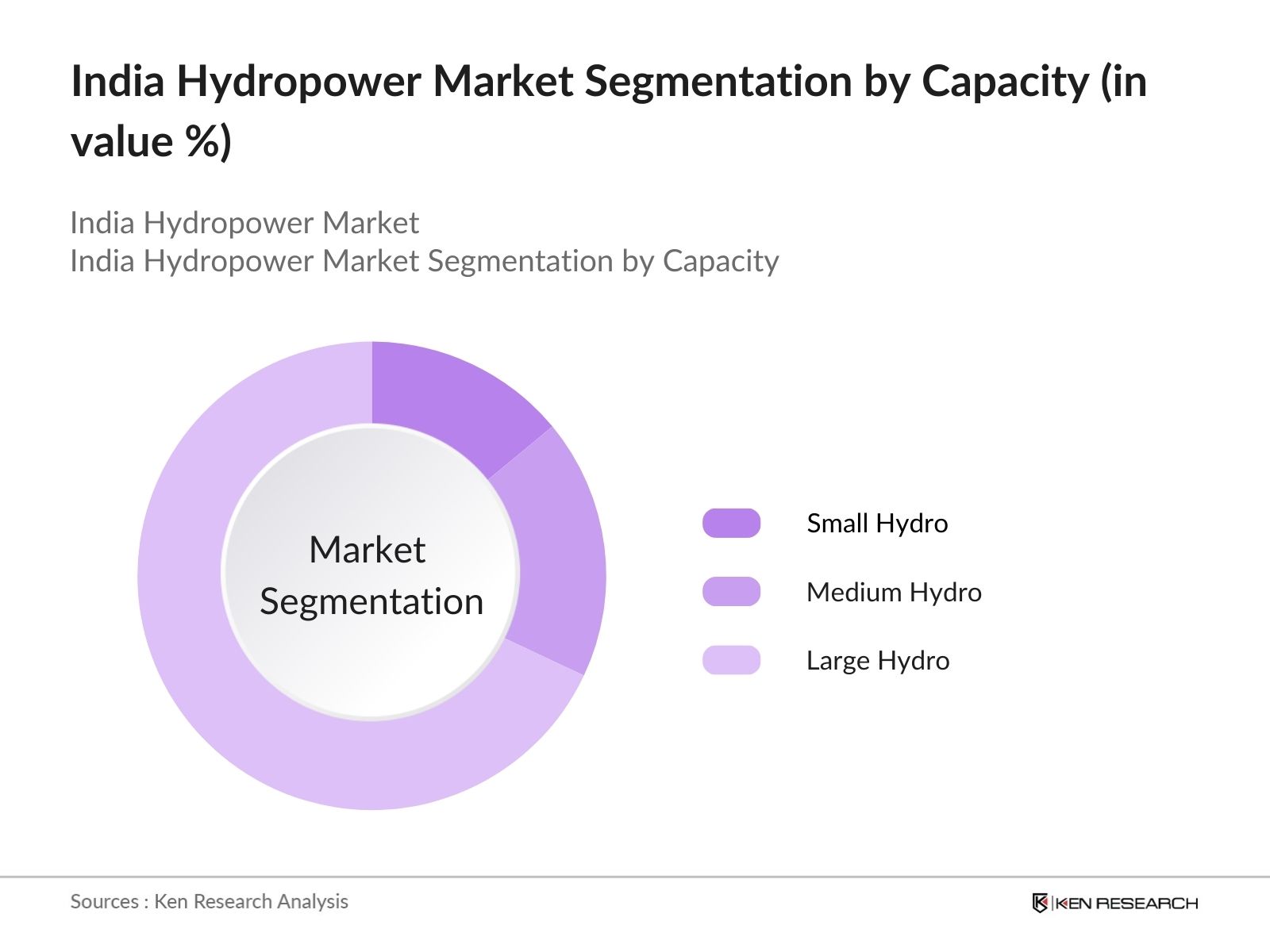

Segment |

Market Share (2023) |

|

Small Hydro |

14% |

|

Medium Hydro |

18% |

|

Large Hydro |

68% |

|

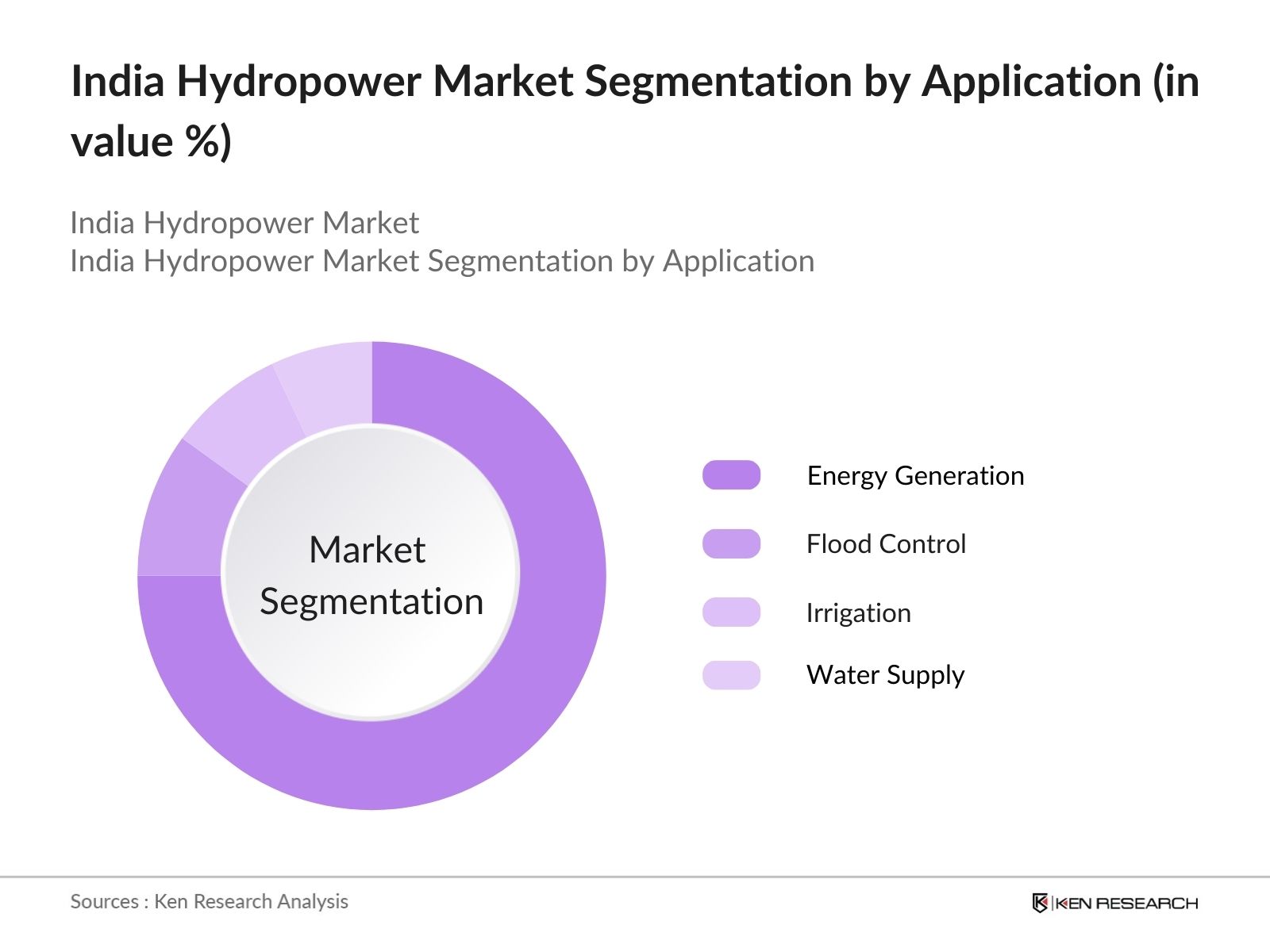

Segment |

Market Share (2023) |

|

Energy Generation |

75% |

|

Flood Control |

10% |

|

Irrigation |

8% |

|

Water Supply |

7% |

|

Company Name |

Establishment Year |

Headquarters |

|---|---|---|

|

NHPC Limited |

1975 |

Faridabad, Haryana |

|

SJVN Limited |

1988 |

Shimla, Himachal Pradesh |

|

Tata Power |

1915 |

Mumbai, Maharashtra |

|

JSW Energy |

1994 |

Mumbai, Maharashtra |

|

Reliance Power |

1995 |

Navi Mumbai, Maharashtra |

NHPC Limited (2023 Developments): In July 2023, NHPC Limited announced the commissioning of its 2,000 MW Subansiri Lower Hydroelectric Project on the Assam-Arunachal Pradesh border. This project is a significant step towards enhancing the hydropower capacity in the northeast. NHPC has also entered into agreements with Bhutan to develop joint ventures in the region, targeting an additional 500 MW capacity.

SJVN Limited (2024 Developments): SJVN Limited, in August 2024, commenced the construction of the 66 MW Dhaulasidh Hydro Electric Project in Himachal Pradesh. The project, costing 687 crore, will help SJVN expand its hydropower footprint in northern India. SJVN is also investing 300 crore in green energy storage solutions to ensure efficient utilization of hydropower.

Growth Drivers

Challenges

Government Initiatives

The India Hydropower Market is projected to grow steadily, driven by government initiatives such as the National Hydropower Policy and increased focus on renewable energy. With significant untapped potential in the Himalayan region, the market will benefit from investments in small and large hydro projects, contributing to Indias clean energy goals and reducing reliance on fossil fuels.

Growth in Small Hydropower Projects: By 2028, small hydropower projects are expected to see significant growth, particularly in rural areas where decentralized energy systems are necessary. The government plans to develop 5,000 MW of small hydropower projects by 2028, with projects like the Loktak Downstream Hydroelectric Project in Manipur leading this trend.

Increased Use of Digital and Smart Grid Technologies: By 2028, Indias hydropower market will increasingly integrate smart grid technologies to enhance efficiency and reduce transmission losses. Digitalization of hydropower plants, such as the Ranganadi Hydroelectric Plant in Arunachal Pradesh, will enable real-time monitoring and optimization of water flow, resulting in a projected 10% increase in operational efficiency across plants nationwide.

|

By Capacity |

Small Hydro Medium Hydro Large Hydro |

|

By Application |

Energy Generation Flood Control Irrigation Water Supply |

|

By Region |

North India South India East India West India |

1.1. Definition and Scope

1.2. Market Growth Rate

1.3. Market Contribution to Indias Energy Matrix

1.4. Hydropower Role in Indias Renewable Energy Targets

1.5. Market Segmentation Overview

2.1. Historical Installed Capacity and Market Size

2.2. Year-on-Year Growth and Installed Capacity in 2023

2.3. Hydropowers Contribution to Energy Security and Grid Stability

2.4. Key Market Milestones and Developments in 2023

3.1. Growth Drivers

3.1.1. Government Investments in Large Hydropower Projects

3.1.2. Grid Modernization and Hydropower Integration

3.1.3. Renewable Energy Status for Large Hydropower Projects

3.2. Market Challenges

3.2.1. Environmental and Social Opposition

3.2.2. High Initial Capital Costs for Hydropower Projects

3.2.3. Delays in Project Approvals

3.3. Market Opportunities

3.3.1. Small Hydropower Development for Rural Electrification

3.3.2. Foreign Investments in Hydropower Projects

3.4. Recent Market Trends

3.4.1. Digitalization and Smart Grid Technology Integration

3.4.2. Growth in Pumped Storage Hydropower Projects

3.4.3. Modernization of Aging Hydropower Plants

4.1. By Capacity (Value %)

4.1.1. Small Hydro (Up to 25 MW)

4.1.2. Medium Hydro (25-100 MW)

4.1.3. Large Hydro (Above 100 MW)

4.2. By Application (Value %)

4.2.1. Energy Generation

4.2.2. Flood Control

4.2.3. Irrigation

4.2.4. Water Supply

4.3. By Region (Value %)

4.3.1. North

4.3.2. South

4.3.3. East

4.3.4. West

4.4. By Technology (Value %)

4.4.1. Pumped Storage Hydropower Plants

4.4.2. Run-of-River Hydropower Plants

4.5. By Operational Mode (Value %)

4.5.1. Base Load Hydropower Plants

4.5.2. Peaking Hydropower Plants

5.1. Market Share Analysis and Key Players

5.2. Company Profiles

5.2.1. NHPC Limited

5.2.2. SJVN Limited

5.2.3. Tata Power

5.2.4. JSW Energy

5.2.5. Reliance Power

5.3. Strategic Initiatives and Developments

5.3.1. Mergers and Acquisitions

5.3.2. Investments in Renewable Energy Storage Solutions

5.3.3. Joint Ventures in Hydropower Projects

5.4. Competitive Strategies and Differentiators

6.1. Environmental Regulations and Compliance

6.2. Hydropower Purchase Obligations (HPO)

6.3. Certification and Project Approval Procedures

6.4. Government Subsidies and Incentives for Hydropower Projects

7.1. Market Growth Projections to 2028

7.2. Government Policies and Future Hydropower Projects

7.3. Increasing Investments in Small and Large Hydro Projects

7.4. Role of Smart Grid and Digital Technologies in Future Projects

7.5. Opportunities for Hydropower Expansion in Rural Areas

8.1. By Capacity (Value %)

8.2. By Application (Value %)

8.3. By Technology (Value %)

8.4. By Region (Value %)

8.5. By Operational Mode (Value %)

9.1. TAM (Total Addressable Market) and SAM (Serviceable Addressable Market) Analysis

9.2. Key Strategic Initiatives for Hydropower Market Penetration

9.3. White Space Opportunities and Investment Potential in Hydropower

9.4. Customer and Market Potential Analysis

Disclaimer Contact UsEcosystem creation for all major entities and referring to multiple secondary and proprietary databases to perform desk research around the market to collate market-level information.

Collating statistics on the India Hydropower Market over the years, analyzing the penetration of India Hydropower technologies, and computing the revenue generated for the market. This step also involves reviewing technology adoption rates and application effectiveness to ensure accuracy behind the data points shared.

Building market hypotheses and conducting CATIs with market experts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Our team will approach multiple India Hydropower companies to understand the nature of technology segments, consumer preferences, and other parameters. This supports validating statistics derived through a bottom-to-top approach from these India Hydropower companies, ensuring accuracy and reliability in the report.

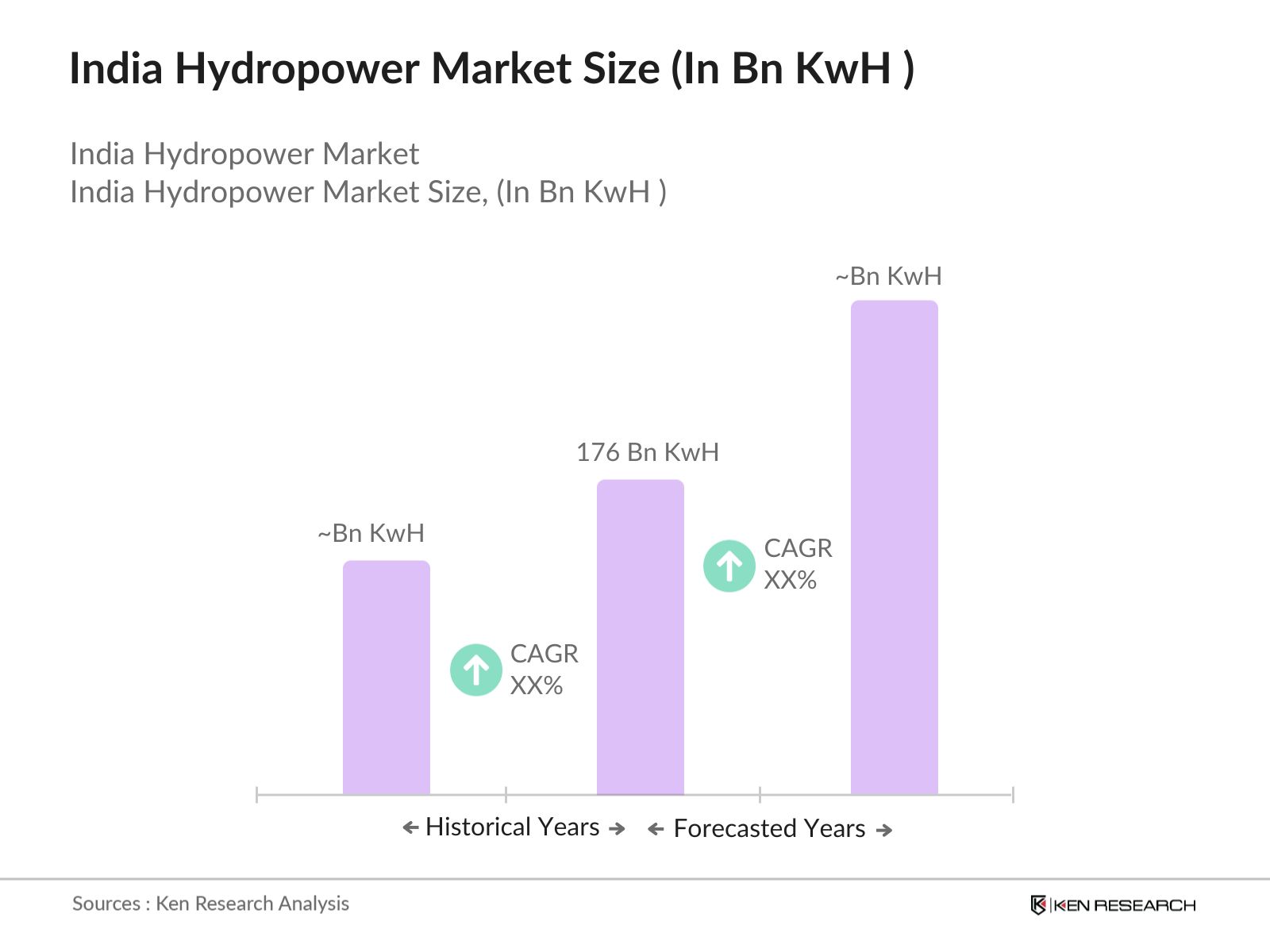

The India hydropower market reached an installed capacity of 176 bn kWh in 2023, driven by increasing investments in renewable energy and infrastructure modernization. The governments commitment to adding 30,000 MW of capacity by 2030 will further enhance this market.

Challenges in the India hydropower market include high capital costs, environmental opposition, and delays in project approvals. For instance, projects like Subansiri Lower Hydroelectric Project faced significant delays due to environmental concerns, slowing overall market growth.

Key players in the India hydropower market include NHPC Limited, SJVN Limited, Tata Power, JSW Energy, and Reliance Power. These companies dominate due to their significant project portfolios and government-backed initiatives.

The India hydropower market is propelled by increased government investments, grid modernization, and the renewable energy status accorded to large hydropower projects. These factors have encouraged both public and private sector investments, particularly in northern and northeastern India.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.