India Interactive Whiteboard Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD8296

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD8296

December 2024

80

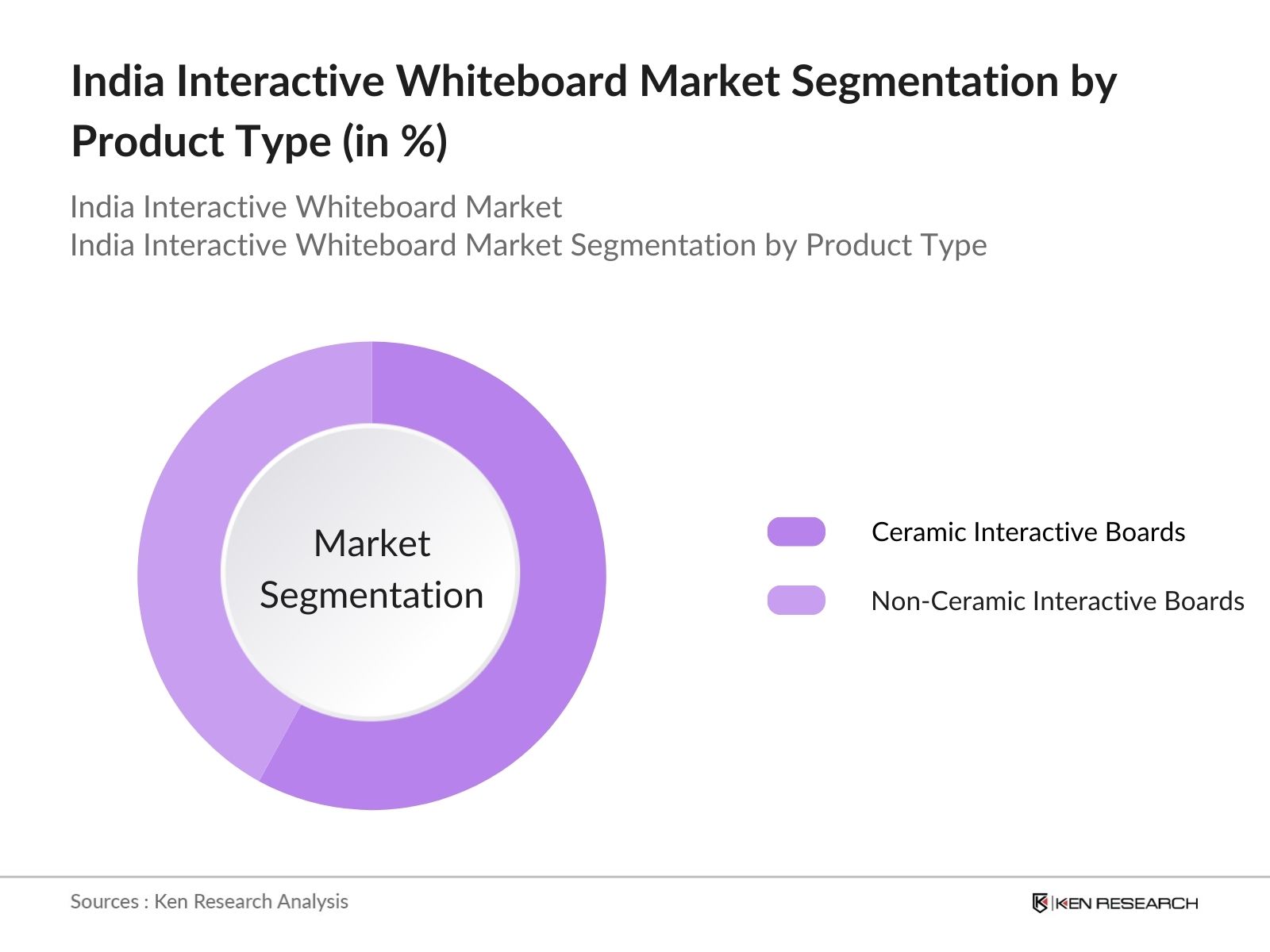

By Product Type: The market is segmented by product type into ceramic interactive whiteboards and non-ceramic interactive whiteboards. Recently, ceramic interactive whiteboards have captured a dominant market share due to their durability and better surface for writing, making them a preferred choice in both educational and corporate settings. Educational institutions, in particular, favor ceramic boards because they can withstand constant use and are more resistant to damage, ensuring long-term use without frequent replacements.

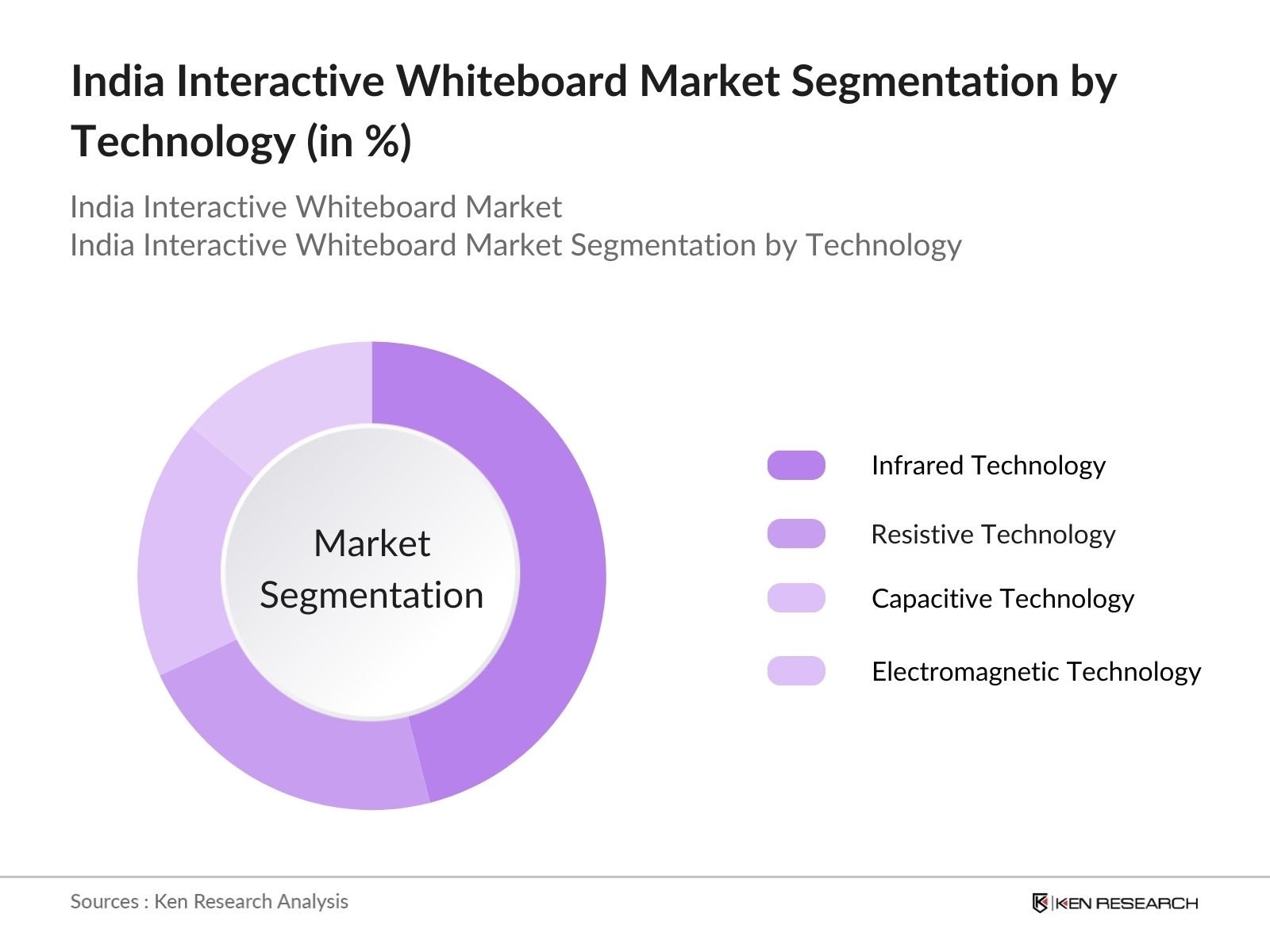

By Technology: Interactive whiteboards in India are also categorized by technology into infrared, resistive, capacitive, and electromagnetic technologies. Among these, infrared technology is currently the most widely adopted due to its accuracy and affordability. Infrared whiteboards allow for multiple touchpoints and can be operated with fingers or any object, making them ideal for educational and collaborative corporate environments. Furthermore, infrared whiteboards offer better resolution, which enhances the overall user experience.

The market is competitive, with several global and local players competing for market share. The market is dominated by both domestic players and well-established global brands that have invested in innovative product offerings and strong distribution networks.

|

Company Name |

Establishment Year |

Headquarters |

Market Position |

Product Portfolio |

Revenue (USD) |

Employee Count |

R&D Investments |

Technological Innovation |

Strategic Initiatives |

|

Hitachi India Pvt. Ltd. |

1930 |

Tokyo, Japan |

|||||||

|

Panasonic India Pvt. Ltd. |

1918 |

Osaka, Japan |

|||||||

|

SMART Technologies |

1987 |

Alberta, Canada |

|||||||

|

Sharp India Limited |

1912 |

Tokyo, Japan |

|||||||

|

Globus Infocom Limited |

2001 |

Noida, India |

Over the next five years, the India Interactive Whiteboard industry is expected to witness growth driven by government support for digital education, increased demand for hybrid learning models, and the corporate sectors focus on enhancing collaboration through technology.

|

Product Type |

Ceramic Non-Ceramic |

|

Screen Size |

Up to 69 inches 70-90 inches Above 90 inches |

|

Technology |

Infrared Resistive Capacitive Electromagnetic |

|

End-User |

Education Corporate Government |

|

Region |

North South East West |

1.1. Definition and Scope

1.2. Market Taxonomy (Technological Classification, Applications)

1.3. Market Growth Rate (Education Sector, Corporate Sector, Government Sector)

1.4. Market Segmentation Overview (By Screen Size, Technology, and End-User)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Adoption in Education (Digital Learning Initiatives)

3.1.2. Corporate Training and Collaboration Needs

3.1.3. Government Push for Digital Infrastructure

3.1.4. Cost Efficiency in Long-Term Operations

3.2. Market Challenges

3.2.1. High Initial Costs for Implementation

3.2.2. Resistance to Technological Adoption (Corporate and Government)

3.2.3. Limited Awareness and Training Gaps

3.3. Opportunities

3.3.1. Expansion into Rural Educational Sectors

3.3.2. Development of Smart Classrooms and Hybrid Learning

3.3.3. Integration with AI for Collaborative Learning

3.4. Trends

3.4.1. Growth of Portable Interactive Whiteboards

3.4.2. Integration of Augmented Reality and AI

3.4.3. Increasing Focus on Gamified Learning

4.1. By Product Type (In Value %)

4.1.1. Ceramic Interactive Whiteboards

4.1.2. Non-Ceramic Interactive Whiteboards

4.2. By Screen Size (In Value %)

4.2.1. Up to 69 inches

4.2.2. 70 to 90 inches

4.2.3. Above 90 inches

4.3. By Technology (In Value %)

4.3.1. Infrared

4.3.2. Resistive

4.3.3. Capacitive

4.3.4. Electromagnetic

4.4. By End-User (In Value %)

4.4.1. Education

4.4.2. Corporate

4.4.3. Government

4.5. By Region (In Value %)

4.5.1. North

4.5.2. South

4.5.3. East

4.5.4. West

5.1. Detailed Profiles of Major Companies

5.1.1. Hitachi India Pvt. Ltd.

5.1.2. Sharp India Limited

5.1.3. Panasonic India Private Limited

5.1.4. SMART Technologies

5.1.5. Visual Display Solutions Pvt. Ltd.

5.1.6. Globus Infocom Limited

5.1.7. Digital Info Media Pvt. Ltd.

5.1.8. Supreme Global Trading Pvt. Ltd.

5.1.9. Title Display System Pvt. Ltd.

5.1.10. BenQ Corporation

5.1.11. PolyVision Corporation

5.1.12. Vestel

5.1.13. Promethean

5.1.14. Newline Interactive

5.1.15. Boxlight Corporation

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Revenue, Market Share, Product Portfolio, Technological Innovations)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Partnerships, Collaborations, Product Launches)

5.5. Mergers and Acquisitions

5.6. Investment Analysis (Venture Capital, Private Equity)

6.1. Education Sector Regulations (Digital Infrastructure Policies)

6.2. Corporate Sector Compliance (Workplace Technology Integration)

6.3. Government Initiatives (NDEAR - National Digital Education Architecture)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (E-learning Expansion, Corporate Training Needs, Government Programs)

8.1. By Product Type

8.2. By Screen Size

8.3. By Technology

8.4. By End-User

8.5. By Region

9.1. TAM/SAM/SOM Analysis

9.2. Go-to-Market Strategy Recommendations (Target Segments, Technology Prioritization)

9.3. White Space Opportunities (AI Integration, Portable Devices, Hybrid Learning Solutions)

Disclaimer Contact UsThe initial step involved mapping all major stakeholders in the India Interactive Whiteboard Market ecosystem. Desk research using secondary databases was conducted to gather information on technological trends, market penetration, and growth dynamics. This phase focused on identifying key variables affecting market dynamics, such as technology adoption and market drivers.

Historical data for the interactive whiteboard market was compiled, including market revenue by product type and technology. This phase involved examining market trends, demand from educational and corporate sectors, and the performance of major players. Additionally, data accuracy was ensured by comparing multiple credible data sources.

To validate the market findings, CATIs (Computer-Assisted Telephone Interviews) were conducted with industry experts from leading companies. This included product managers and sales heads from interactive whiteboard companies, who provided insights into the challenges, market trends, and innovations that influence the market.

The final stage involved synthesizing all research findings to produce an in-depth report. Primary insights from manufacturers were combined with desk research to ensure that the analysis covered all pertinent segments. A top-down and bottom-up approach was used to provide comprehensive market insights.

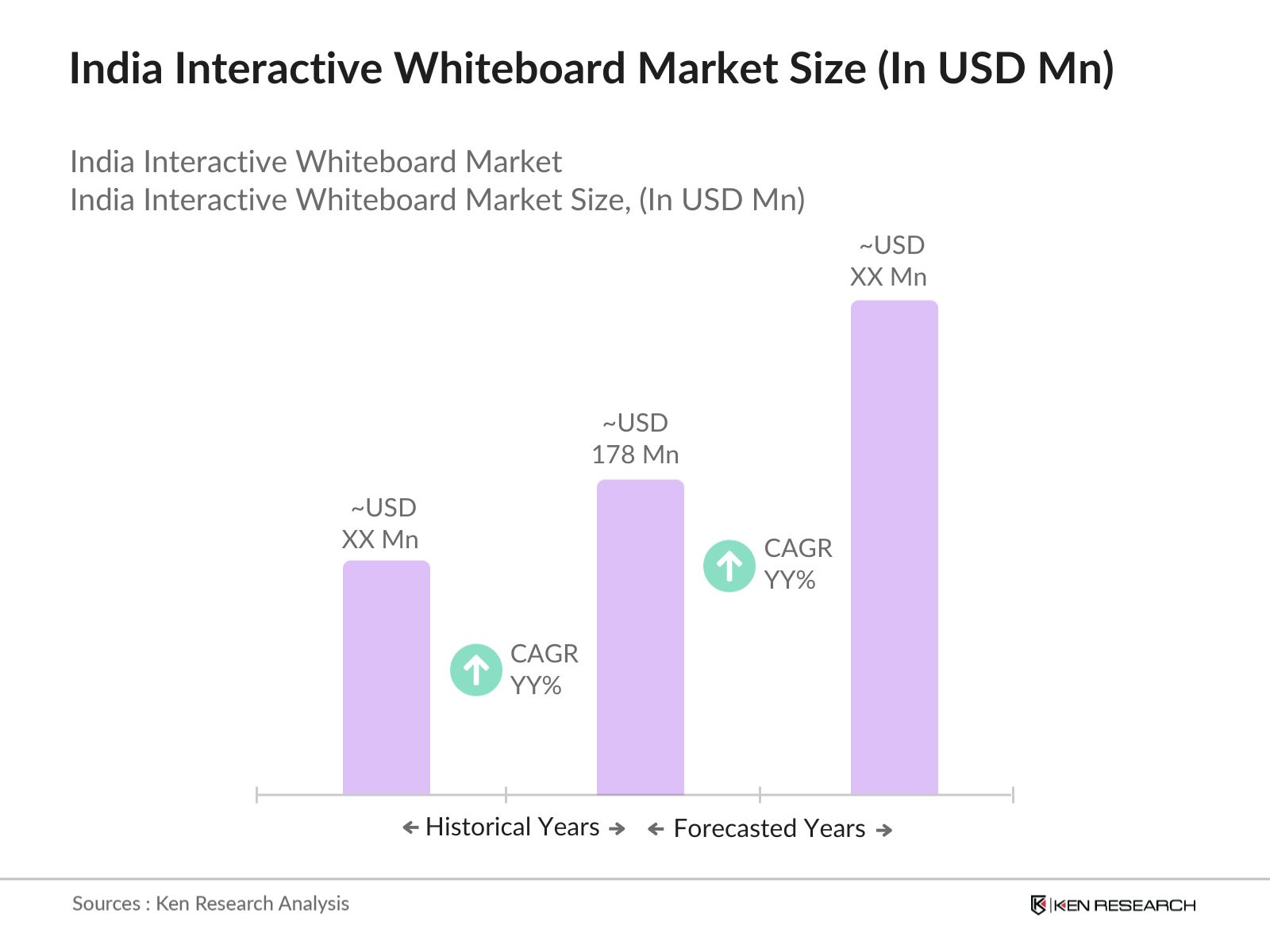

The India interactive whiteboard market was valued at USD 178 million, driven by increased demand in educational and corporate sectors. The governments emphasis on digital classrooms and corporate collaboration has fueled this growth.

Some challenges in the India interactive whiteboard market include the high initial setup costs and limited awareness about the technology, especially in rural areas. Additionally, there is resistance to adopting new technologies in traditional educational environments.

Key players in the India interactive whiteboard market include Hitachi India, Panasonic India, Sharp India, SMART Technologies, and Globus Infocom. These companies dominate due to their extensive product portfolios and established presence in the market.

The India interactive whiteboard market is driven by increased digitalization in education and corporations, government initiatives for smart classrooms, and advancements in IWB technologies like AI integration and multi-touch capabilities.

Technological advancements such as infrared touch and capacitive touch have revolutionized the IWB market by providing better user experience, enhancing collaborative work, and enabling more dynamic content delivery in educational institutions and corporations.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.