India Laundry Appliances Market Outlook to 2030

Region:Asia

Author(s):Abhinav kumar

Product Code:KROD7091

November 2024

81

About the Report

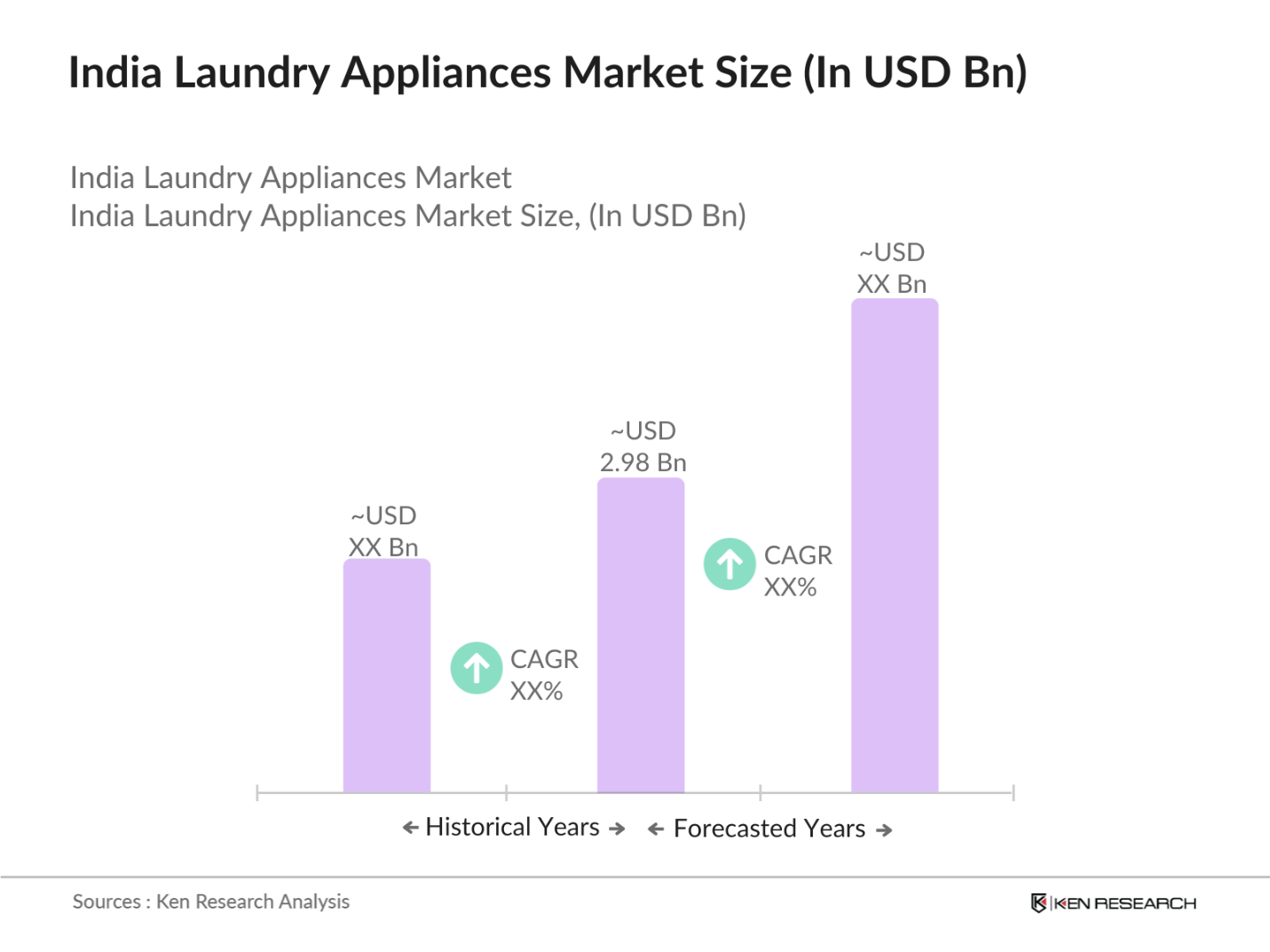

India Laundry Appliances Market Overview

- The India laundry appliances market is valued at USD 2.98 billion, driven by increasing urbanization, the rise in disposable incomes, and a shift towards energy-efficient appliances. Growing demand for convenience, coupled with technological advancements such as the integration of IoT, AI, and smart home technologies, is accelerating the growth of the market. The expansion of organized retail and e-commerce platforms has further contributed to the robust growth, allowing greater market penetration in urban as well as rural areas.

- In India, metropolitan cities like Mumbai, Delhi, and Bengaluru dominate the market due to their high population density, rising income levels, and increased adoption of modern home appliances. The dominance is attributed to the growing preference for time-saving household appliances among working professionals in these cities. Additionally, the presence of organized retail chains and aggressive marketing strategies by key brands helps drive significant sales in these regions.

- The integration of IoT and AI technologies into laundry appliances is transforming how consumers interact with these products. As of 2023, approximately 40% of appliances sold in urban markets have smart capabilities, allowing for remote monitoring and operation. This trend is expected to continue as manufacturers invest in research and development to enhance user experience and product functionality. The use of AI for predictive maintenance and user customization is further driving the demand for smart laundry appliances, positioning the market for significant advancements in technology.

India Laundry Appliances Market Segmentation

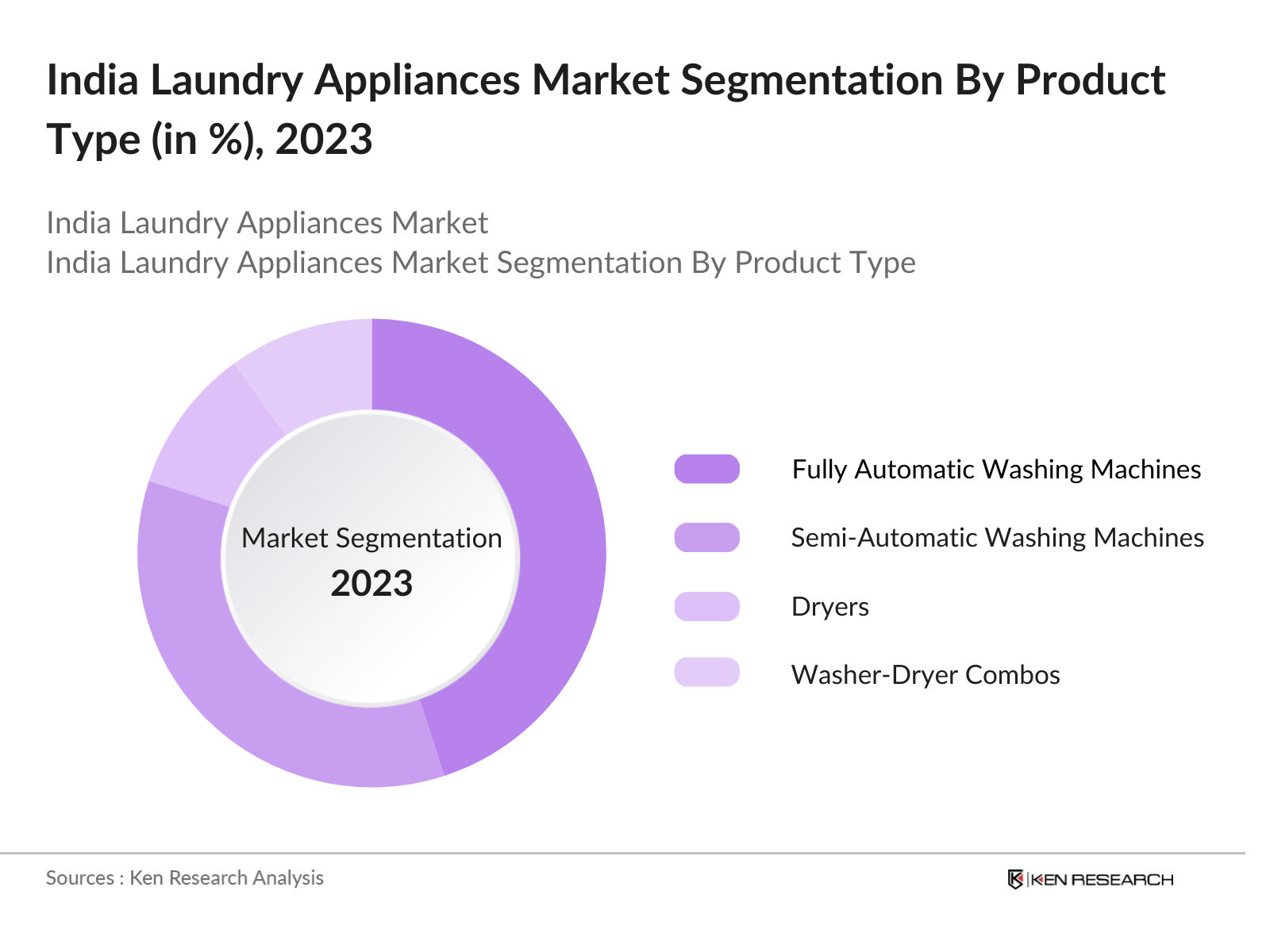

By Product Type: India's laundry appliance market is segmented by product type into fully automatic washing machines, semi-automatic washing machines, dryers, and washer-dryer combos. Fully automatic washing machines hold the largest market share, driven by their convenience and increasing consumer preference for products that save time and effort. Brands such as LG, Samsung, and Whirlpool have introduced a wide variety of models with advanced features like AI-powered wash cycles, adding to their appeal among middle and high-income households.

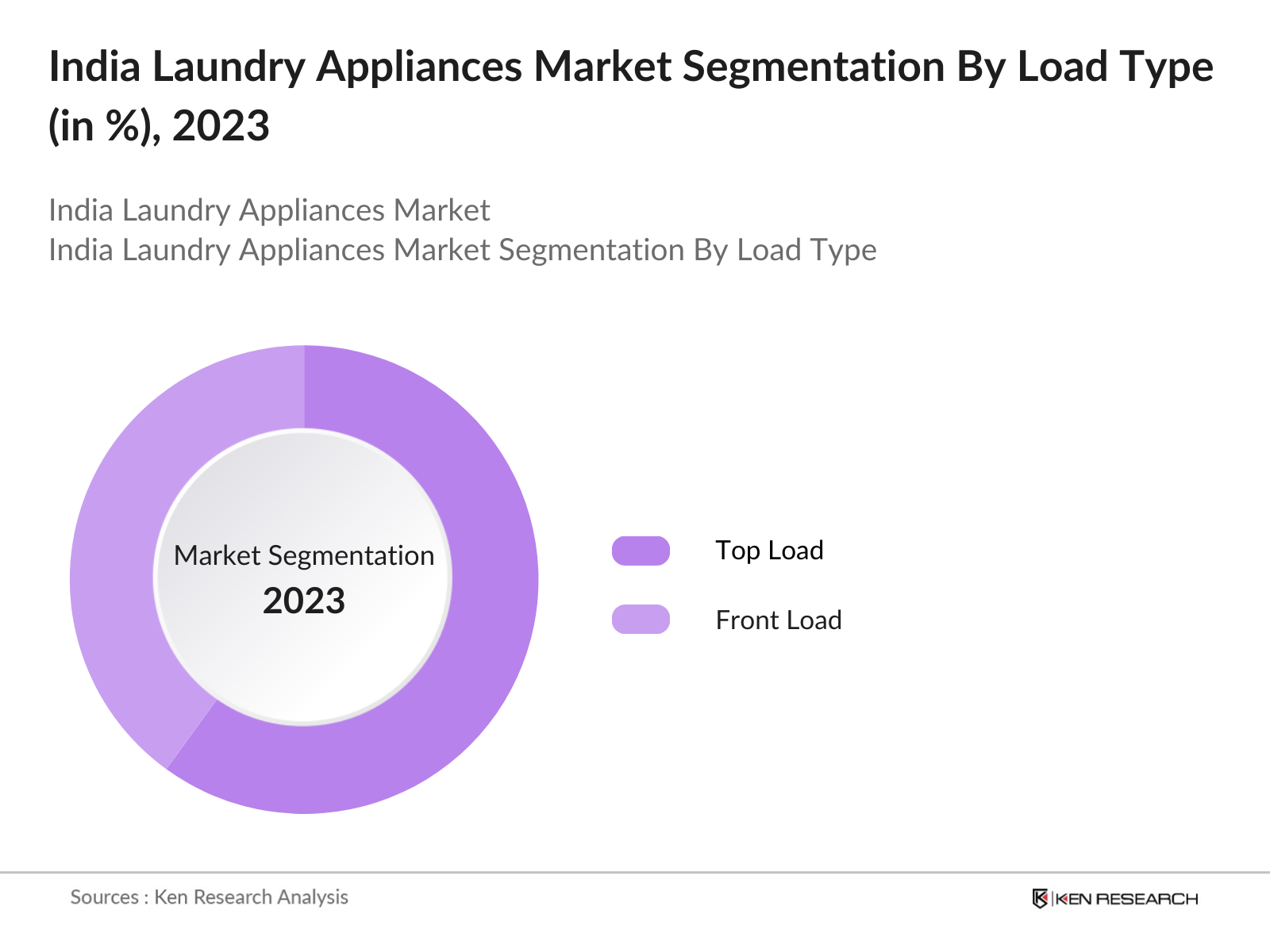

By Load Type: The market is segmented by load type into top load and front load washing machines. Top load washing machines have a higher market share due to their affordability and ease of use. Consumers in India prefer top load machines because they are generally cheaper, require less bending, and are more convenient in areas with water pressure issues. However, front load washing machines are growing in popularity due to their water and energy efficiency, especially in urban areas.

India Laundry Appliances Market Competitive Landscape

The India laundry appliances market is dominated by several major players, both domestic and international. These companies maintain strong distribution networks, offer a wide range of products, and invest heavily in marketing and product development to capture market share. The competition is particularly intense in the fully automatic washing machine segment, where innovation and pricing play a key role in brand differentiation. The market is dominated by companies like LG Electronics, Samsung, and Whirlpool, known for their strong product portfolios and innovation in smart laundry technology. Other notable players include Haier and IFB, which have established themselves in both urban and rural markets.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (2023) |

No. of Employees |

Product Portfolio |

R&D Investment |

Energy Efficiency Rating |

Market Share |

|

LG Electronics |

1958 |

South Korea |

_ |

_ |

_ |

_ |

_ |

_ |

|

Samsung Electronics |

1969 |

South Korea |

_ |

_ |

_ |

_ |

_ |

_ |

|

Whirlpool Corporation |

1911 |

USA |

_ |

_ |

_ |

_ |

_ |

_ |

|

Haier India |

1984 |

China |

_ |

_ |

_ |

_ |

_ |

_ |

|

IFB Industries |

1974 |

India |

_ |

_ |

_ |

_ |

_ |

_ |

India Laundry Appliances Industry Analysis

Growth Drivers

- Increasing Urbanization: Urbanization in India is on the rise, with urban population growth expected to reach 600 million by 2031, as reported by the World Bank. The urbanization rate has been accelerating, with over 34% of India's population living in urban areas as of 2022. This urban shift is leading to a higher demand for laundry appliances as urban residents typically have busy lifestyles that require efficient and convenient washing solutions. With urban households often adopting modern amenities, the transition to appliances like washing machines is significantly increasing, thus driving market growth.

- Rising Disposable Income: India's GDP per capita is projected to grow from $2,256 in 2022 to $2,900 by 2025, indicating an upward trend in disposable income. With an increasing number of households entering the middle-income bracket, there is a growing propensity to spend on household appliances. This rise in disposable income is making laundry appliances more accessible to a broader demographic, particularly in urban areas. The increase in consumer purchasing power is directly linked to higher sales of washing machines and dryers as families seek to enhance their living standards and convenience.

- Growing Demand for Energy-Efficient Appliances: The demand for energy-efficient appliances is increasingly important as consumers become more environmentally conscious. In 2022, the Bureau of Energy Efficiency (BEE) introduced stricter energy labeling norms, promoting energy-efficient washing machines that consume less than 0.9 units per wash. This has led to a rise in the sale of energy-efficient appliances, with sales of BEE-rated appliances increasing by approximately 30% in urban areas. As a result, manufacturers are focusing on producing energy-efficient laundry solutions to meet this growing demand, enhancing market prospects significantly.

Market Challenges

- High Price Sensitivity of Consumers: Price sensitivity remains a significant challenge in the Indian laundry appliances market. Approximately 70% of Indian consumers prioritize cost when purchasing appliances, limiting the willingness to invest in premium products. The average price of washing machines in India ranges between INR 15,000 to INR 25,000, which can be prohibitive for many households, particularly in semi-urban and rural areas. This sensitivity affects manufacturers' pricing strategies and may hinder the introduction of higher-end products, impacting overall market growth.

- Inconsistent Power Supply in Rural Areas: Inconsistent power supply remains a challenge in rural India, with over 300 million people experiencing unreliable electricity access in 2022. This lack of reliable power hampers the adoption of electric appliances, including laundry machines, in these regions. With frequent power outages, many rural households are unable to use electric washing machines, leading to continued reliance on manual washing methods. This inconsistency in electricity supply poses a significant barrier to the growth of laundry appliances in rural markets, limiting overall market expansion potential.

India Laundry Appliances Market Future Outlook

Over the next five years, the India laundry appliances market is expected to experience steady growth, driven by the increasing penetration of smart home technologies, rising consumer awareness around energy efficiency, and the expansion of the organized retail sector. As Indias middle-class population continues to grow, demand for mid-range and premium appliances is expected to rise. Additionally, the government's initiatives to promote energy-efficient appliances and the growing awareness of sustainability will push manufacturers to innovate and introduce more environmentally friendly products.

Opportunities

- Demand for Smart Laundry Appliances: The shift towards smart home technology is creating significant opportunities in the laundry appliances market. With the number of smartphone users in India expected to reach 1 billion by 2025, there is a growing demand for smart appliances that offer connectivity features. Smart washing machines equipped with IoT capabilities can be remotely controlled via mobile applications, enabling users to schedule washes and receive notifications. This trend is driving manufacturers to innovate and invest in smart technologies, aligning with consumer preferences for convenience and connectivity.

- Growth in E-commerce Sales: E-commerce sales in India have surged, expected to reach $111 billion by 2025. This growth presents an enormous opportunity for the laundry appliances market, as online platforms provide an efficient distribution channel. E-commerce allows consumers to compare products easily, read reviews, and take advantage of attractive discounts and financing options. This trend encourages brands to enhance their online presence and leverage digital marketing strategies to tap into this expanding market, making laundry appliances more accessible to consumers across various regions.

Scope of the Report

|

Product Type |

Fully Automatic Washing Machines Semi-Automatic Washing Machines Dryers Washer-Dryer Combos Others (Spin Dryers, Mini Washers) |

|

Load Type |

Top Load Front Load |

|

Capacity (In Kg) |

Below 6 Kg 6-8 Kg Above 8 Kg |

|

Technology |

Conventional Smart Laundry Appliances |

|

Region |

North India South India West India East India |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing to This Report:

Laundry Appliances Companies

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (Bureau of Energy Efficiency)

E-commerce Companies

Organized Retail Chains Industry

Technology Solution Providers for Smart Appliances Companies

Consumer Electronics Companies

Companies

Players Mentioned in the Report:

LG Electronics

Samsung Electronics

Whirlpool Corporation

Haier India

IFB Industries

Godrej & Boyce Mfg. Co. Ltd.

Bosch Siemens Hausgerte (BSH)

Panasonic India Pvt. Ltd.

Voltas Beko

AmazonBasics (Appliances Category)

Videocon Industries

Lloyd (Havells)

Electrolux India

Sharp India Ltd.

Midea India

Table of Contents

1. India Laundry Appliances Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. India Laundry Appliances Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. India Laundry Appliances Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Urbanization

3.1.2. Rising Disposable Income

3.1.3. Growing Demand for Energy-Efficient Appliances

3.1.4. Expansion of Organized Retail

3.2. Market Challenges

3.2.1. High Price Sensitivity of Consumers

3.2.2. Inconsistent Power Supply in Rural Areas

3.2.3. Low Penetration in Tier-III Cities

3.2.4. Competitive Pricing Pressures

3.3. Opportunities

3.3.1. Demand for Smart Laundry Appliances

3.3.2. Growth in E-commerce Sales

3.3.3. Untapped Rural Markets

3.3.4. Energy Conservation Initiatives

3.4. Trends

3.4.1. Integration of IoT and AI in Laundry Appliances

3.4.2. Rise in Demand for Compact and Portable Washing Machines

3.4.3. Environmentally Friendly and Energy-Saving Technologies

3.4.4. Increased Adoption of Inverter Technology

3.5. Government Regulations

3.5.1. Bureau of Energy Efficiency (BEE) Ratings for Energy-Efficient Appliances

3.5.2. Import Duties and Taxation Policies

3.5.3. Make in India and Local Manufacturing Policies

3.5.4. Guidelines for Disposal and Recycling of Electronic Appliances

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. India Laundry Appliances Market Segmentation(Market Segmentation in Value %)

4.1. By Product Type

4.1.1. Fully Automatic Washing Machines

4.1.2. Semi-Automatic Washing Machines

4.1.3. Dryers

4.1.4. Washer-Dryer Combos

4.1.5. Others (Spin Dryers, Mini Washers)

4.2. By Load Type

4.2.1. Top Load

4.2.2. Front Load

4.3. By Capacity (In Kg)

4.3.1. Below 6 Kg

4.3.2. 6-8 Kg

4.3.3. Above 8 Kg

4.4. By Technology

4.4.1. Conventional

4.4.2. Smart Laundry Appliances

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. West India

4.5.4. East India

5. India Laundry Appliances Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. LG Electronics

5.1.2. Samsung Electronics

5.1.3. Whirlpool Corporation

5.1.4. Haier India

5.1.5. Godrej & Boyce Mfg. Co. Ltd.

5.1.6. IFB Industries Ltd.

5.1.7. Panasonic India Pvt. Ltd.

5.1.8. Videocon Industries

5.1.9. Bosch Siemens Hausgerte (BSH)

5.1.10. Voltas Beko

5.1.11. AmazonBasics (Appliances Category)

5.1.12. Midea India

5.1.13. Lloyd (Havells)

5.1.14. Electrolux India

5.1.15. Sharp India Ltd.

5.2. Cross Comparison Parameters (No. of Employees, Manufacturing Facilities, Product Range, Energy Efficiency, Brand Positioning, Service Network, Revenue, Market Share)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Private Equity Investments

6. India Laundry Appliances Market Regulatory Framework

6.1. Compliance with Energy Efficiency Standards

6.2. Certification Processes for Smart Appliances

6.3. Environmental Regulations on E-Waste Disposal

6.4. Industry-Specific Regulations on Import/Export

7. India Laundry Appliances Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. India Laundry Appliances Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Load Type (In Value %)

8.3. By Capacity (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9. India Laundry Appliances Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research begins by identifying critical variables impacting the India laundry appliances market, including product innovation, energy efficiency regulations, and shifts in consumer purchasing behavior. Extensive desk research using proprietary databases and industry publications helps create a detailed ecosystem map of stakeholders.

Step 2: Market Analysis and Construction

In this phase, historical market data is collected and analyzed, evaluating market penetration, growth in urban and rural areas, and performance of key market segments. The focus is on accurate revenue estimation by examining trends in sales, product launches, and promotional activities.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through expert interviews with key stakeholders in the laundry appliances industry, including manufacturers, retailers, and regulatory bodies. These consultations provide practical insights into market dynamics, pricing strategies, and consumer preferences.

Step 4: Research Synthesis and Final Output

The final phase synthesizes data from multiple sources, ensuring an accurate representation of market conditions. Insights from key players are incorporated into the analysis to validate the research findings and project future market trends for the India laundry appliances market.

Frequently Asked Questions

01. How big is the India Laundry Appliances Market?

The India laundry appliances market is valued at USD 2.98 billion, driven by increasing urbanization, rising incomes, and growing demand for energy-efficient and smart appliances.

02. What are the challenges in the India Laundry Appliances Market?

Challenges include high price sensitivity, low penetration in rural areas, and competition from unorganized players. Additionally, inconsistent power supply in rural areas hampers the adoption of advanced appliances.

03. Who are the major players in the India Laundry Appliances Market?

Major players include LG Electronics, Samsung Electronics, Whirlpool Corporation, Haier India, and IFB Industries, all of which dominate due to their strong distribution networks, brand recognition, and technological innovation.

04. What are the growth drivers of the India Laundry Appliances Market?

The market is propelled by urbanization, the rise of dual-income households, and increasing consumer preference for smart and energy-efficient appliances. The growing influence of organized retail and e-commerce platforms further drives market growth.

05. What trends are shaping the India Laundry Appliances Market?

Key trends include the increasing adoption of smart appliances integrated with IoT, AI, and mobile control, along with the growing demand for compact, space-saving appliances in urban households.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.