India Linux Operating System Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD4585

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD4585

December 2024

97

The India Linux Operating System market is dominated by several key players, both global and domestic. The market is highly competitive, with major players focusing on product innovation, integration with cloud technologies, and offering better support services to capture market share.

|

Company Name |

Establishment Year |

Headquarters |

License Type |

No. of Employees |

Key Partnerships |

Developer Community Size |

Adoption Rate |

Pricing Model |

|

Canonical Ltd. (Ubuntu) |

2004 |

London, UK |

- |

- |

- |

- |

- |

- |

|

Red Hat, Inc. (RHEL) |

1993 |

Raleigh, USA |

- |

- |

- |

- |

- |

- |

|

SUSE |

1992 |

Nuremberg, DE |

- |

- |

- |

- |

- |

- |

|

Oracle Corporation |

1977 |

Austin, USA |

- |

- |

- |

- |

- |

- |

|

IBM (LinuxONE) |

1911 |

New York, USA |

- |

- |

- |

- |

- |

- |

The India Linux Operating System market is poised for substantial growth over the next five years, driven by an increasing reliance on open-source software in enterprise solutions, government backing for open-source projects, and growing digital transformation initiatives. The proliferation of cloud technologies, paired with the increased use of Linux in IoT and AI-based applications, will further boost market demand. The future of the Linux OS market in India looks promising as it continues to gain traction across both large enterprises and small-to-medium enterprises (SMEs).

|

By Distribution Type |

Ubuntu Fedora RHEL Debian CentOS |

|

By End-User Industry |

IT & Telecommunication Government Education BFSI Retail & E-Commerce |

|

By Deployment Mode |

On-Premise Cloud-Based |

|

By Enterprise Size |

SMEs Large Enterprises |

|

By Region |

North India South India East India West India |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Open-Source Adoption (Low-cost solutions, flexibility)

3.1.2. Rise in Digital Transformation (Public and Private Sectors)

3.1.3. Government Push for Open-Source Adoption (Digital India Initiative)

3.1.4. Expanding Cloud Infrastructure (Integration with Open-Source Platforms)

3.2. Market Challenges

3.2.1. Competition with Proprietary Systems (Microsoft Windows dominance)

3.2.2. Perceived Technical Complexity (User adaptation and learning curves)

3.2.3. Vendor Lock-In (Migration and transition challenges)

3.3. Opportunities

3.3.1. Cloud-Native Linux Deployments (Docker, Kubernetes integrations)

3.3.2. Rising Data Center Deployments (Preference for Linux-based systems)

3.3.3. Collaboration with Indian Tech Firms (Custom Linux distributions)

3.4. Trends

3.4.1. Increasing Usage in IoT Devices (Embedded Linux systems)

3.4.2. Linux for AI and Machine Learning (Growing developer communities)

3.4.3. Expansion of Linux in Edge Computing (Real-time Linux)

3.5. Government Regulations

3.5.1. Open-Source Software Policy (Indian government policies)

3.5.2. Data Localization Laws (FOSS preference in India)

3.5.3. Cybersecurity Regulations (Linux security standards)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Developers, Corporates, SMEs)

3.8. Porters Five Forces

3.9. Competition Ecosystem

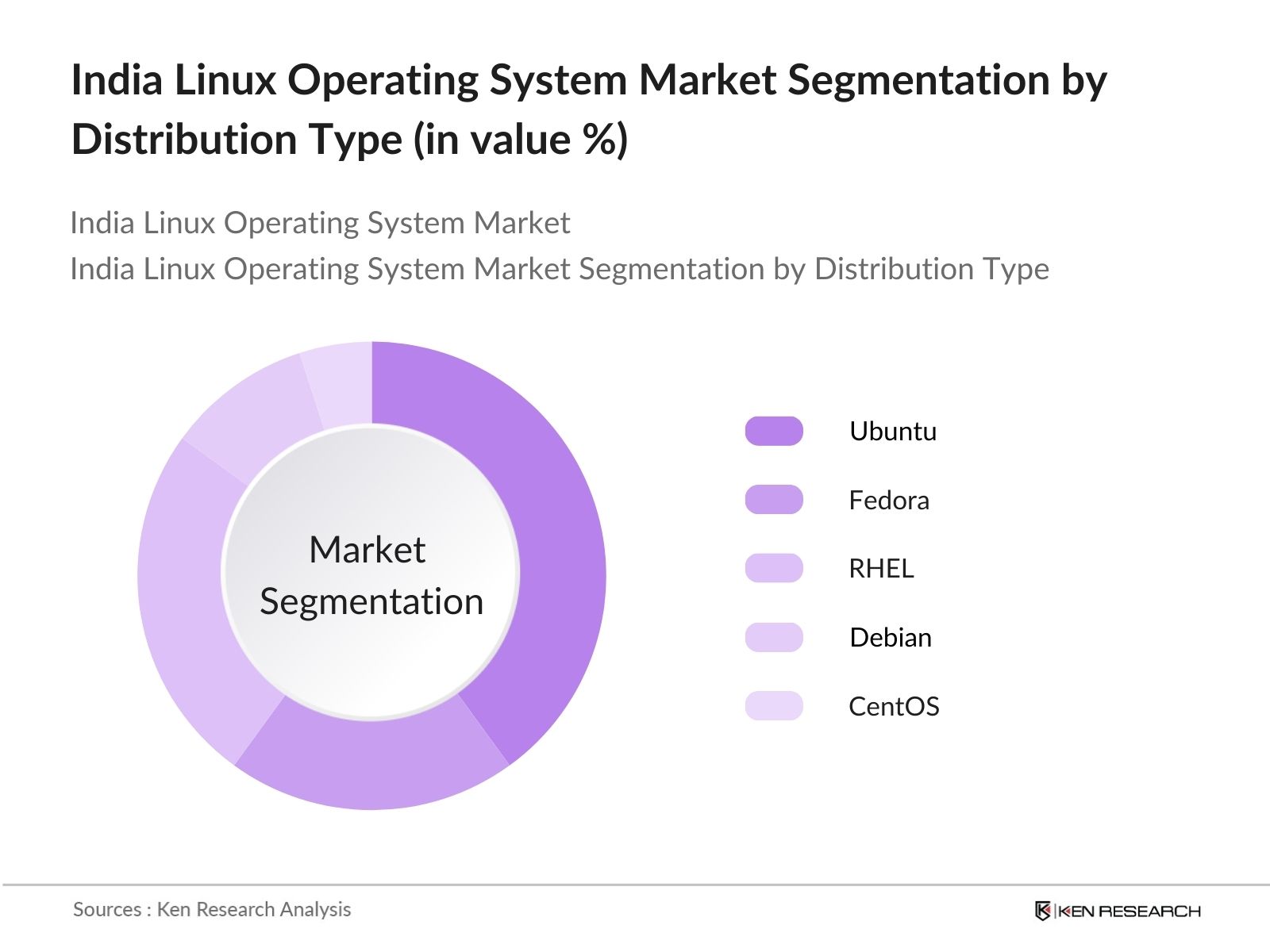

4.1. By Distribution Type (In Value %)

4.1.1. Ubuntu

4.1.2. Fedora

4.1.3. Red Hat Enterprise Linux (RHEL)

4.1.4. Debian

4.1.5. CentOS

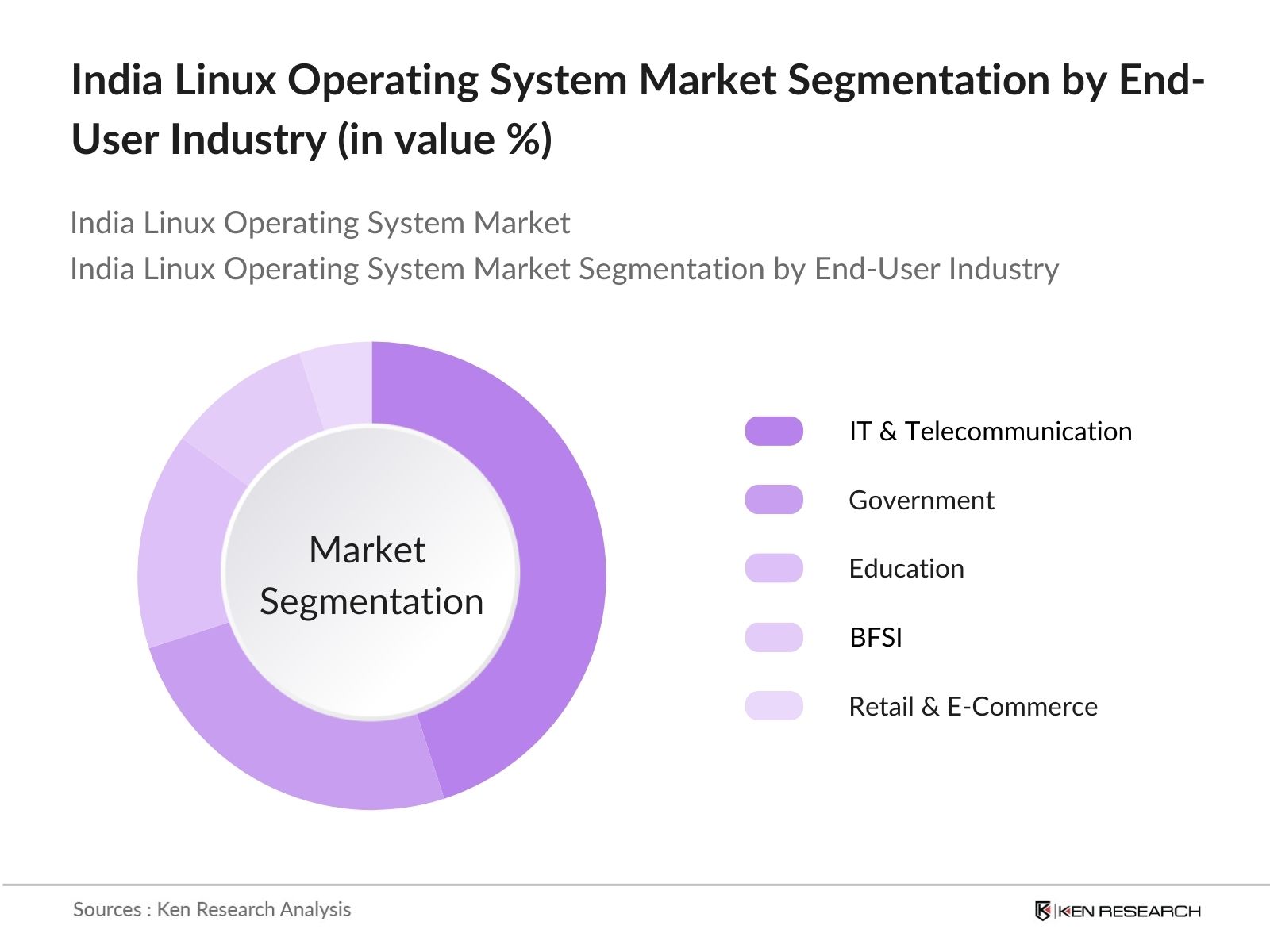

4.2. By End-User Industry (In Value %)

4.2.1. IT & Telecommunication

4.2.2. Government

4.2.3. Education

4.2.4. Banking, Financial Services, and Insurance (BFSI)

4.2.5. Retail & E-Commerce

4.3. By Deployment Mode (In Value %)

4.3.1. On-Premise

4.3.2. Cloud-Based

4.4. By Enterprise Size (In Value %)

4.4.1. Small and Medium Enterprises (SMEs)

4.4.2. Large Enterprises

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. East India

4.5.4. West India

5.1. Detailed Profiles of Major Companies

5.1.1. Canonical Ltd. (Ubuntu)

5.1.2. Red Hat, Inc.

5.1.3. SUSE

5.1.4. Oracle Corporation

5.1.5. IBM Corporation

5.1.6. Zorin OS

5.1.7. Manjaro Linux

5.1.8. PCLinuxOS

5.1.9. Endless OS

5.1.10. Arch Linux

5.1.11. Elementary OS

5.1.12. ClearOS

5.1.13. Deepin Linux

5.1.14. CentOS

5.1.15. Rocky Linux

5.2. Cross Comparison Parameters (Market Capitalization, Customer Base, License Type, Headquarters, Key Partnerships, Developer Community Size, Adoption Rate, Pricing Model)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Open-Source Licensing Regulations (GPL, MIT, Apache)

6.2. Software Compliance Requirements (Security patches, Support)

6.3. Data Protection and Privacy Laws (Implications for Linux OS)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Distribution Type (In Value %)

8.2. By End-User Industry (In Value %)

8.3. By Deployment Mode (In Value %)

8.4. By Enterprise Size (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The research process began with the identification of critical variables affecting the India Linux Operating System Market. This involved constructing a comprehensive ecosystem map, which included open-source developers, enterprise users, and government stakeholders.

In this phase, historical data was analyzed to assess the penetration of Linux in different industries and its rate of adoption. Additionally, industry reports and government publications were referenced to provide accurate financial estimates for the Linux OS market.

Market experts from the IT and telecommunications industries were consulted through interviews to validate our research hypotheses. These interviews provided valuable insights regarding operational trends, growth drivers, and market challenges.

Data gathered from both primary and secondary research was synthesized to produce a comprehensive analysis of the market. This phase involved verification of Linux's growth trajectory using both top-down and bottom-up approaches.

The India Linux Operating System market was valued at USD 540 million, with growth driven by its increased use in IT and telecommunications, government projects, and cloud applications.

Key challenges include competition with proprietary systems such as Microsoft Windows, and the technical complexity associated with Linux deployments, especially for organizations without dedicated IT resources.

Major players include Canonical Ltd., Red Hat, SUSE, Oracle Corporation, and IBM, which dominate due to their enterprise offerings, partnerships, and established developer ecosystems.

Growth drivers include increased adoption of open-source software, government initiatives promoting open-source solutions, and the rising use of Linux in cloud computing and data centers.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.