India Medical Tourism Market Outlook to 2030

Region:India

Author(s):Samanyu

Product Code:KROD4707

Region:India

Author(s):Samanyu

Product Code:KROD4707

November 2024

81

Listen to the audio summary

By Treatment Type: The market is segmented by treatment type into cardiovascular surgery, oncology treatments, cosmetic surgery, orthopedic surgery, and reproductive medicine. Among these, cardiovascular surgery holds a dominant share due to Indias advanced healthcare infrastructure and expertise in complex heart procedures. Medical tourists seek cardiovascular treatments in India primarily because of the high success rates and the significantly lower cost compared to countries like the U.S. and U.K. Additionally, the growing number of specialized cardiac hospitals across key cities has helped India secure its position as a global leader in heart surgeries.

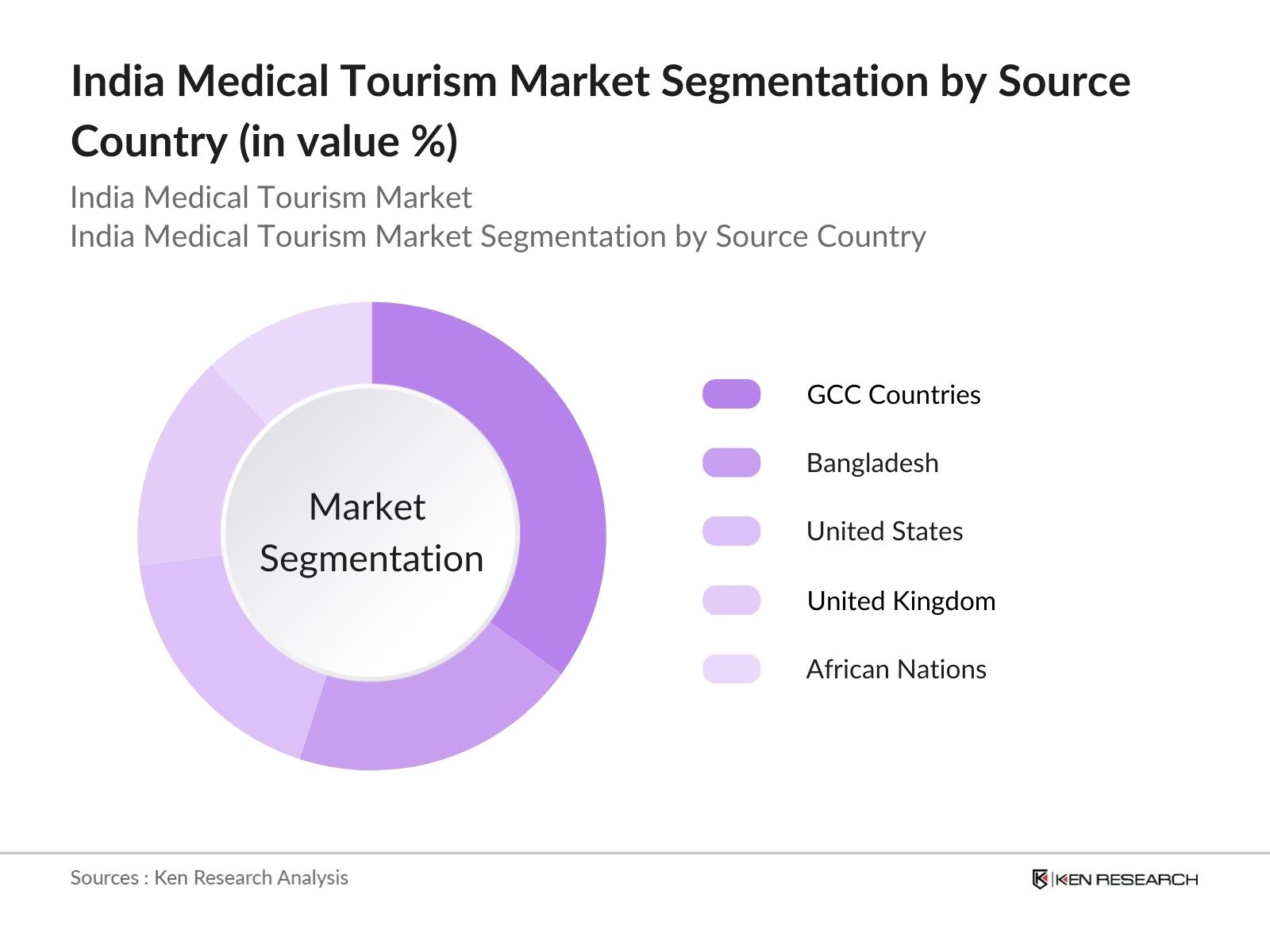

By Source Country: The market is also segmented by source country, including the United States, the United Kingdom, Gulf Cooperation Council (GCC) countries, African nations, and Bangladesh. GCC countries dominate the market share due to cultural and religious similarities, as well as close diplomatic ties with India. Patients from the GCC primarily seek treatments for chronic conditions like cardiovascular disease, diabetes, and organ transplants, areas where Indian healthcare excels. India also provides highly affordable fertility and cosmetic treatments that are otherwise expensive in their home countries.

The India Medical Tourism market is dominated by several key players, including both large hospital chains and specialized clinics. These organizations have established themselves as leaders by offering world-class medical services at affordable costs, attracting patients globally. The competitive landscape is characterized by continuous investments in infrastructure, accreditations, and collaborations with international insurance companies.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (2023) |

Employees |

No. of Beds |

Specializations |

International Patients (per year) |

Partnerships |

|

Apollo Hospitals |

1983 |

Chennai |

||||||

|

Fortis Healthcare |

1996 |

Gurgaon |

||||||

|

Narayana Health |

2000 |

Bengaluru |

||||||

|

Max Healthcare |

2000 |

Delhi NCR |

||||||

|

Manipal Hospitals |

1953 |

Bengaluru |

Over the next five years, the India Medical Tourism market is expected to witness robust growth driven by advancements in healthcare technology, the rise of telemedicine services, and the increasing preference for minimally invasive surgeries. The Indian governments continued focus on improving healthcare infrastructure and promoting wellness tourism, especially Ayurvedic and alternative therapies, is set to further expand the market. With Indias reputation for delivering high-quality medical services at affordable costs, the market is poised to attract a higher influx of patients from new regions such as Southeast Asia and Eastern Europe.

|

By Treatment Type |

Cardiovascular Surgery Orthopedic Surgery Oncology Treatments Cosmetic Surgery Reproductive Medicine |

|

By Source Country |

United States United Kingdom GCC Countries African Nations Bangladesh |

|

By Healthcare Facility |

Multi-Specialty Hospitals Specialized Clinics Wellness and Ayurvedic Centers |

|

By Type of Traveler |

Medical Tourists Wellness Tourists Cosmetic Tourists |

|

By Region |

Delhi NCR Maharashtra Tamil Nadu Kerala Karnataka |

1.1. Definition and Scope (Medical Tourism Services, Patient Categories, Geographical Focus)

1.2. Market Taxonomy (Inpatient vs. Outpatient Procedures, Treatment Specializations)

1.3. Market Dynamics (Growth Rate, Drivers, Challenges)

1.4. Market Segmentation Overview (By Treatment Type, Source Country, Healthcare Facility Type)

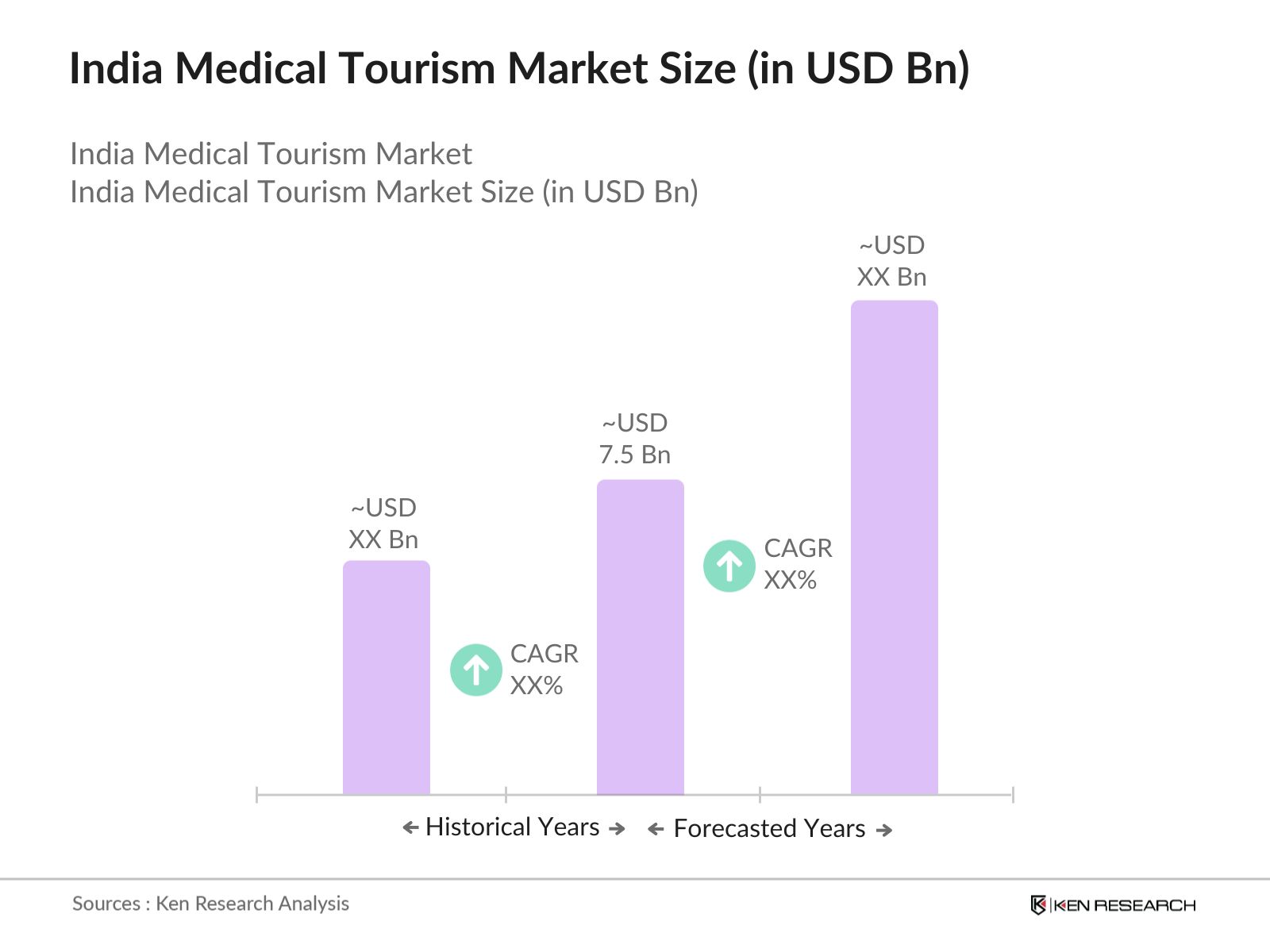

2.1. Historical Market Size (In USD Bn)

2.2. Year-On-Year Growth Analysis (Inpatient vs. Outpatient Growth)

2.3. Key Market Developments and Milestones (Health Infrastructure Investments, Public-Private Collaborations)

3.1. Growth Drivers

3.1.1. Affordability and Cost-Effectiveness of Treatments (Surgical Costs, Comparative Analysis)

3.1.2. Increasing Accreditation of Indian Hospitals (NABH, JCI)

3.1.3. Government Initiatives Promoting Medical Tourism (e-Medical Visa, Healthcare Infrastructure)

3.1.4. Quality of Specialized Treatments (Cardiology, Oncology, Neurology)

3.2. Market Restraints

3.2.1. Language and Cultural Barriers (Communication Challenges)

3.2.2. Regulatory and Legal Complications (Medical Liability, Malpractice)

3.2.3. Infrastructure Bottlenecks (Transport, Accommodation)

3.2.4. COVID-19 Aftermath on Travel and Healthcare Systems

3.3. Market Opportunities

3.3.1. Collaborations with International Healthcare Providers (Joint Ventures, Research Partnerships)

3.3.2. Expansion in Niche Specialties (Reproductive Medicine, Alternative Therapies)

3.3.3. Rise of Telemedicine and Post-treatment Follow-up Services

3.3.4. Promotion of Ayurvedic and Wellness Tourism

3.4. Market Trends

3.4.1. Integration of Technology (AI, Robotics in Surgery)

3.4.2. Growing Demand for Wellness and Preventive Healthcare (Ayurveda, Yoga)

3.4.3. Preference for Minimally Invasive Procedures

3.4.4. Strategic Partnerships with International Insurance Companies

3.5. Regulatory Framework

3.5.1. Medical Visa Policies (e-Visa Facilitation, Visa on Arrival)

3.5.2. International Healthcare Standards Compliance (JCI, NABH)

3.5.3. Guidelines for Medical Practitioners and Hospitals (Accreditation, Ethical Standards)

3.5.4. Tax Incentives and Subsidies for Medical Infrastructure Development

3.6. Competitive Analysis

3.6.1. Porters Five Forces Analysis (Barriers to Entry, Buyer Power)

3.6.2. SWOT Analysis of Indias Medical Tourism Market

3.6.3. Stakeholder Ecosystem (Hospitals, Insurance Companies, Travel Agencies)

4.1. By Treatment Type (In Value USD Bn)

4.1.1. Cardiovascular Surgery

4.1.2. Orthopedic Surgery

4.1.3. Oncology Treatments

4.1.4. Cosmetic Surgery

4.1.5. Reproductive Medicine

4.2. By Source Country (In Value USD Bn)

4.2.1. United States

4.2.2. United Kingdom

4.2.3. Gulf Cooperation Council (GCC) Countries

4.2.4. African Nations

4.2.5. Bangladesh

4.3. By Healthcare Facility Type (In Value USD Bn)

4.3.1. Multi-Specialty Hospitals

4.3.2. Specialized Clinics

4.3.3. Wellness and Ayurvedic Centers

4.4. By Type of Traveler (In Value USD Bn)

4.4.1. Medical Tourists (For Critical Treatments)

4.4.2. Wellness Tourists (For Preventive and Alternative Therapies)

4.4.3. Cosmetic Tourists

4.5. By Region (In Value USD Bn)

4.5.1. Delhi NCR

4.5.2. Maharashtra (Mumbai, Pune)

4.5.3. Tamil Nadu (Chennai)

4.5.4. Kerala (Ayurveda, Wellness Tourism)

4.5.5. Karnataka (Bangalore)

5.1. Detailed Profiles of Major Competitors

5.1.1. Apollo Hospitals

5.1.2. Fortis Healthcare

5.1.3. Max Healthcare

5.1.4. Narayana Health

5.1.5. Medanta-The Medicity

5.1.6. BLK Super Specialty Hospital

5.1.7. AIIMS Delhi

5.1.8. Manipal Hospitals

5.1.9. Artemis Hospitals

5.1.10. Global Hospitals

5.1.11. Columbia Asia

5.1.12. Wockhardt Hospitals

5.1.13. Jaslok Hospital and Research Centre

5.1.14. Aster DM Healthcare

5.1.15. Care Hospitals

5.2. Cross Comparison Parameters (Number of International Patients, Specialization, Accreditation, Success Rates, Geographic Reach)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Joint Ventures, Facility Expansions)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Private Equity and Venture Capital Funding

5.8. Government Grants and Support Programs

6.1. Healthcare and Hospital Regulations (Licensing, Certifications)

6.2. Medical Liability and Insurance Regulations (International Patient Coverage)

6.3. Environmental and Hygiene Standards Compliance

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Growth (Expansion of Specialized Facilities, Government Policies)

8.1. By Treatment Type

8.2. By Source Country

8.3. By Healthcare Facility Type

8.4. By Type of Traveler

8.5. By Region

9.1. TAM/SAM/SOM Analysis

9.2. White Space Opportunities in Niche Specialties

9.3. Patient Journey Mapping

9.4. Marketing Strategies for Attracting International Patients

Disclaimer Contact Us

The first stage involves identifying the key drivers and barriers influencing the India Medical Tourism market. Extensive desk research was conducted to understand the dynamics of international patient inflow, the types of treatments most in demand, and the regions/countries that contribute to medical tourism growth. This phase included analysis of government reports, industry publications, and hospital data.

In this stage, we compiled and analyzed data on patient numbers, revenue generation from medical tourism, and the ratio of international to domestic patients. This data allowed us to gauge market size accurately and predict future growth. We also analyzed market segments based on treatment types and the origin of patients to provide a granular view of the market dynamics.

During this phase, market assumptions and data points were validated by consulting medical professionals, hospital administrators, and experts in medical tourism. These consultations were conducted through telephonic interviews and surveys to corroborate the data and refine our analysis.

In the final stage, the insights gathered from primary and secondary research were synthesized to provide a comprehensive understanding of the India Medical Tourism market. The final report includes a detailed analysis of market trends, competitive dynamics, and future outlook based on validated data.

The India Medical Tourism market is valued at USD 7.5 billion, driven by the countrys affordability in healthcare services and increasing international patient inflows.

Challenges in the India Medical Tourism market include language barriers, cultural differences, and regulatory complexities related to medical liability and patient care.

Key players in India Medical Tourism market include Apollo Hospitals, Fortis Healthcare, Narayana Health, Max Healthcare, and Manipal Hospitals, which dominate due to their international accreditations and high success rates in specialized treatments.

Growth drivers in India Medical Tourism market include the availability of cost-effective treatments, government support through streamlined medical visa processes, and increasing accreditation of hospitals to international standards.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.