India mHealth Apps Market Outlook to 2030

Region:Asia

Author(s):Paribhasha Tiwari

Product Code:KROD11033

December 2024

81

About the Report

India mHealth Apps Market Overview

- The India mHealth Apps Market is valued at USD 2 billion, based on comprehensive analysis over the past five years. This market is driven primarily by an increase in smartphone penetration, reaching over 600 million users, and rising demand for digital healthcare solutions, particularly in urban areas. The growth is further fueled by government initiatives such as Ayushman Bharat, which emphasizes the digitization of healthcare services, and an increasing awareness of preventive healthcare.

- In India, the dominance in the mHealth market is primarily seen in metropolitan areas such as Delhi, Mumbai, and Bengaluru, driven by a high density of tech-savvy users, access to reliable internet infrastructure, and a high concentration of healthcare facilities. These cities are also hubs for healthcare innovation and partnerships, contributing significantly to the markets expansion. The adoption of health applications in these areas highlights regional trends in digital health engagement and technology utilization.

- These cities are also hubs for healthcare innovation and partnerships, contributing significantly to the market’s expansion. The adoption of health applications in these areas highlights regional trends in digital health engagement and technology utilization.

- The growth is further fueled by government initiatives such as Ayushman Bharat, which emphasizes the digitization of healthcare services, and an increasing awareness of preventive healthcare.

India mHealth Apps Market Segmentation

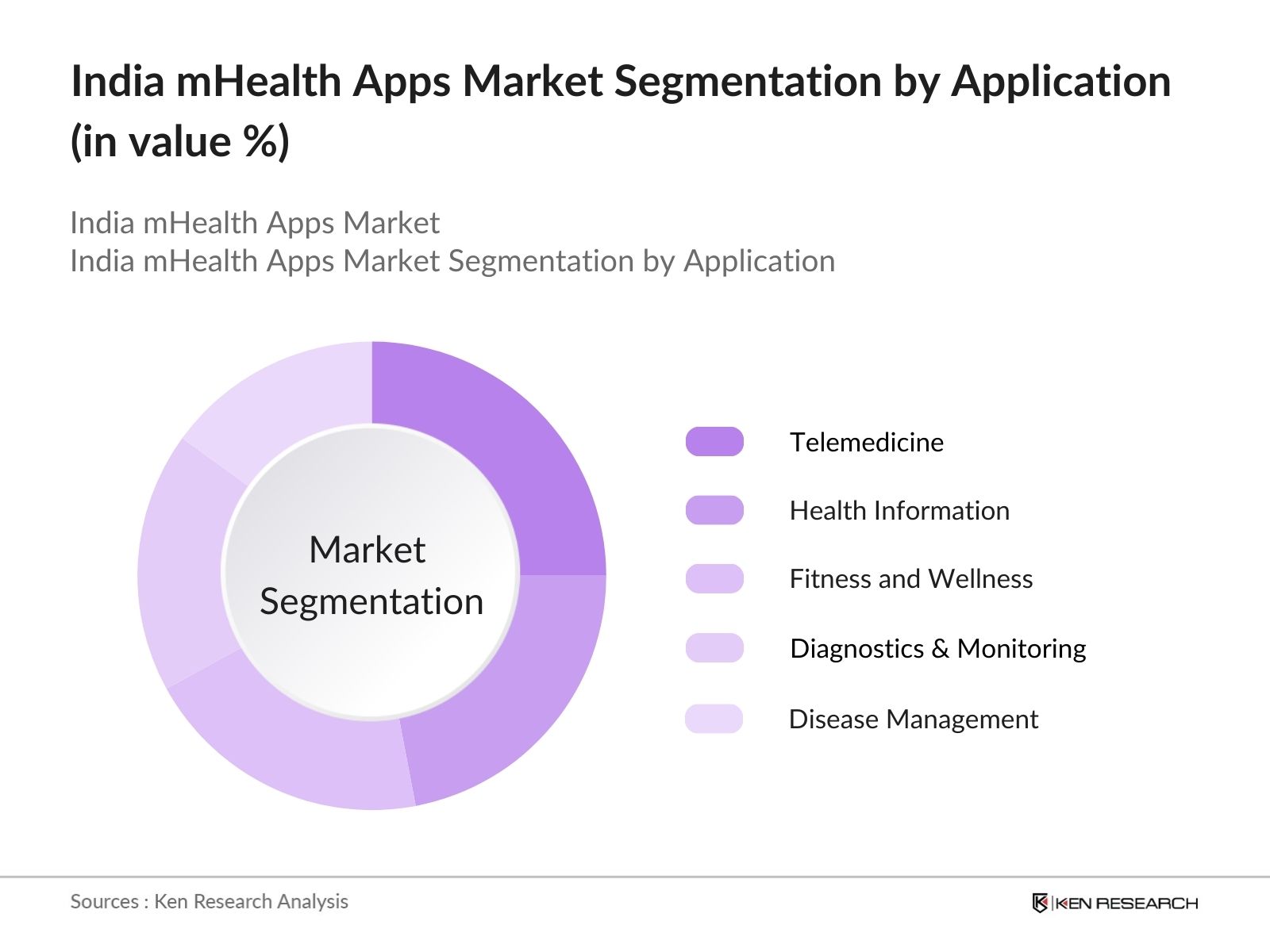

By Application Type: India's mHealth market segments into fitness and wellness, disease management, diagnostics and monitoring, health information and lifestyle, and telemedicine. Among these, telemedicine commands the largest share due to its ability to bridge gaps in healthcare accessibility, especially in underserved rural areas. The rise of telemedicine is attributed to increased partnerships between app developers and healthcare providers, aiming to offer remote consultations and follow-ups for patients who lack immediate access to healthcare facilities.

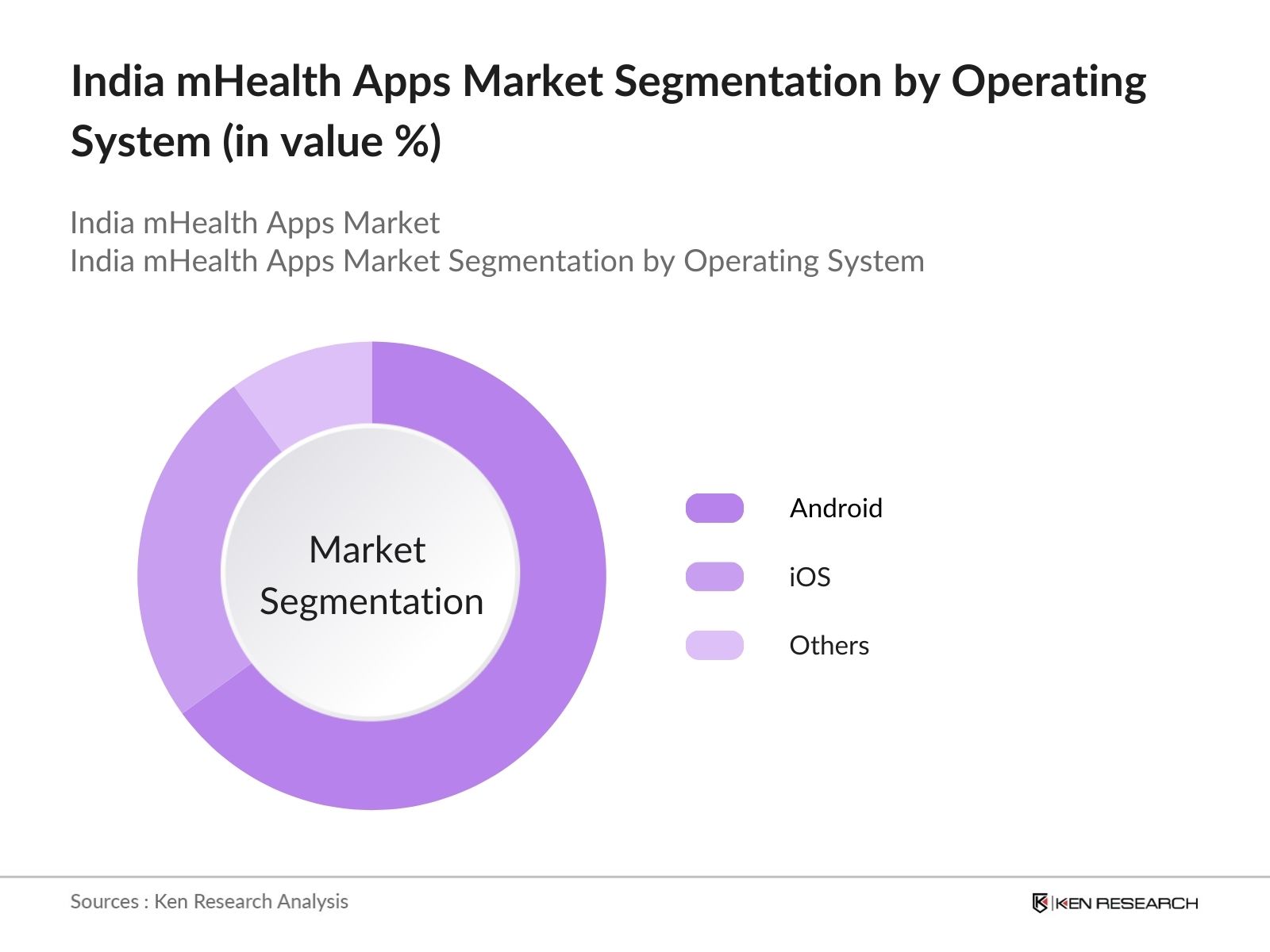

By Operating System: The mHealth apps in India operate across multiple platforms, including Android, iOS, and others. Android apps lead the market owing to the affordability and popularity of Android devices in India. Additionally, Androids compatibility with a wide range of devices ensures accessibility for a diverse user base. The dominance of this segment reflects a preference for cost-effective digital solutions, making health services available even to lower-income groups across the country.

India mHealth Apps Market Competitive Landscape

The India mHealth Apps Market is characterized by the presence of several key players. Local platforms, like Practo and MFine, lead alongside global players expanding into India. This competitive landscape underscores the increasing demand for versatile health apps, with companies continuously improving service offerings, integrating AI, and expanding region-specific features.

India mHealth Apps Market Industry Analysis

Growth Drivers

- Increasing Smartphone Penetration: India's smartphone user base has reached approximately 1.2 billion in 2024, driven by affordable mobile devices and increasing internet accessibility across urban and semi-urban regions. This significant user base has amplified the adoption of mHealth applications, with the health app user count surpassing 450 million in 2024. The governments support for digital connectivity and subsidies for internet usage have played a substantial role in smartphone penetration, providing a strong foundation for mHealth app growth.

- Rise in Digital Health Initiatives: India's government has allocated over $400 million in 2024 for health technology programs, including the Digital Health Mission, aiming to create a comprehensive digital healthcare infrastructure. The National Digital Health Mission (NDHM) supports the development of secure health data storage, directly boosting mHealth app development by making health data accessible to both patients and providers. This initiative enhances patient trust in digital health platforms and accelerates the mHealth market's expansion.

- Growth in Chronic Disease Cases: India reported over 75 million diabetes cases and approximately 30 million heart disease cases in 2024, according to national health data. With the rising prevalence of lifestyle-related diseases, theres an increased need for continuous monitoring and personalized healthcareservices that mHealth apps provide efficiently. The surge in chronic disease cases necessitates widespread health tracking and remote management, boosting demand for mHealth apps among Indias urban and rural populations alike.

Market Challenges

- Data Privacy Concerns: In 2024, India recorded more than 2,000 data breach incidents, a large portion affecting digital health records, as reported by cybersecurity agencies. With mHealth apps handling sensitive health information, concerns over data privacy are a significant challenge. The absence of comprehensive data protection laws exacerbates user hesitation to adopt these platforms, impacting the markets growth momentum.

- Limited Access to Digital Health in Rural Areas: Although smartphone penetration is high in urban regions, over 300 million rural residents still have limited access to high-speed internet, according to telecom data. This digital divide restricts the usage of mHealth applications in rural India, where healthcare facilities are scarce, yet digital health solutions could make a transformative impact. Bridging this gap requires targeted government initiatives and increased infrastructure investment to ensure rural inclusion in mHealth access.

India mHealth Apps Market Future Outlook

Over the next five years, the India mHealth Apps Market is expected to experience substantial growth driven by increased digital health adoption, further government support, and advancements in technology such as AI and machine learning. Additionally, expanding rural internet connectivity will boost accessibility, allowing mHealth services to reach new demographics across India.

Market Opportunities

- AI and Data Analytics Integration: Indias healthcare market saw an investment exceeding $500 million in artificial intelligence technologies in 2024, aimed at enhancing patient care and health insights. By integrating AI into mHealth apps, providers can offer advanced diagnostic features, personalized health recommendations, and predictive analysis tools, positioning Indias mHealth sector at the forefront of health innovation.

- Expansion of Telemedicine: The government allocated around $600 million for telemedicine infrastructure in 2024, expanding telemedicine services across urban and rural areas. With the healthcare system struggling to serve remote populations, telemedicine integration within mHealth apps allows seamless doctor-patient interactions, consultations, and follow-ups, presenting a lucrative opportunity for the mHealth market in India.

Scope of the Report

|

Application Type |

Fitness and Wellness Disease Management Diagnostics & Monitoring Health Information Telemedicine |

|

Operating System |

Android iOS Others |

|

End-User |

Individuals Healthcare Providers Corporate Employers Insurance Providers |

|

Service Type |

Free Apps Subscription-Based Apps In-App Purchases |

|

Region |

North South East West |

Products

Key Target Audience

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (National Health Authority)

Hospitals and Healthcare Providers

Insurance Companies

Pharmaceutical Companies

Health App Developers

Telecommunication Providers

Healthcare Technology Providers

Companies

Players Mentioned in the Report

Practo

HealthifyMe

MyUpchar

MFine

Tata Health

PharmEasy

Netmeds

Cure.fit

DocsApp

Lybrate

Table of Contents

1. India mHealth Apps Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Dynamics (User Engagement, App Accessibility, Health Outcomes)

1.4 Market Segmentation Overview

2. India mHealth Apps Market Size (USD Mn)

2.1 Historical Market Size

2.2 YearonYear Growth Analysis

2.3 Key Market Developments and Milestones

3. India mHealth Apps Market Analysis

3.1 Growth Drivers

3.1.1 Increasing Smartphone Penetration

3.1.2 Rise in Digital Health Initiatives

3.1.3 Growth in Chronic Disease Cases

3.1.4 Increased Focus on Preventative Healthcare

3.2 Market Challenges

3.2.1 Data Privacy Concerns

3.2.2 Limited Access to Digital Health in Rural Areas

3.2.3 Regulatory Barriers

3.3 Opportunities

3.3.1 AI and Data Analytics Integration

3.3.2 Expansion of Telemedicine

3.3.3 Regional Language Support

3.4 Market Trends

3.4.1 Rise of Wearable Health Devices

3.4.2 Increasing Adoption of Virtual Health Services

3.4.3 Gamification of Health Apps

3.5 Regulatory Landscape

3.5.1 Digital Health Regulations

3.5.2 Data Protection Laws

3.5.3 Health Insurance Integration Policies

3.6 Competitive Landscape Analysis (User Reviews, App Downloads, Active User Base)

3.7 SWOT Analysis

3.8 Stakeholder Ecosystem

4. India mHealth Apps Market Segmentation

4.1 By Application (Market Share %)

4.1.1 Fitness and Wellness

4.1.2 Disease Management

4.1.3 Diagnostics and Monitoring

4.1.4 Health Information and Lifestyle

4.1.5 Telemedicine

4.2 By Operating System (Market Share %)

4.2.1 Android

4.2.2 iOS

4.2.3 Others

4.3 By EndUser (Market Share %)

4.3.1 Individuals

4.3.2 Healthcare Providers

4.3.3 Corporate Employers

4.3.4 Insurance Providers

4.4 By Service Type (Market Share %)

4.4.1 Free Apps

4.4.2 SubscriptionBased Apps

4.4.3 InApp Purchases

4.5 By Region (Market Share %)

4.5.1 North India

4.5.2 South India

4.5.3 East India

4.5.4 West India

5. India mHealth Apps Market Competitive Analysis

5.1 Profiles of Major Companies

5.1.1 Practo

5.1.2 HealthifyMe

5.1.3 MyUpchar

5.1.4 MFine

5.1.5 Netmeds

5.1.6 1mg

5.1.7 Cure.fit

5.1.8 PharmEasy

5.1.9 Medlife

5.1.10 Lybrate

5.1.11 DocsApp

5.1.12 Tata Health

5.1.13 Dozee

5.1.14 Remedico

5.1.15 Apollo 24/7

5.2 Cross Comparison Parameters (User Ratings, Platform Compatibility, Data Security, Monthly Active Users, Average Revenue Per User (ARPU), Customer Retention Rate, Product Innovation, Geographical Penetration)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Government and Private Equity Investments

6. India mHealth Apps Market Regulatory Framework

6.1 Compliance Requirements

6.2 Certification Processes

6.3 Industry Standards

7. India mHealth Apps Future Market Size (USD Mn)

7.1 Market Size Projections

7.2 Key Drivers of Future Growth

8. India mHealth Apps Future Market Segmentation

8.1 By Application

8.2 By Operating System

8.3 By EndUser

8.4 By Service Type

8.5 By Region

9. India mHealth Apps Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 User Retention and Engagement Strategies

9.4 White Space Opportunities

Research Methodology

Step 1: Identification of Key Variables

This initial phase involved mapping the ecosystem and identifying key stakeholders in the India mHealth Apps Market. Comprehensive desk research was conducted to gather data on industry trends, supported by secondary and proprietary databases.

Step 2: Market Analysis and Construction

The analysis phase included compiling historical data and evaluating metrics such as app penetration rates, user demographics, and service quality. This allowed for accurate estimations of the current market landscape.

Step 3: Hypothesis Validation and Expert Consultation

Key industry hypotheses were validated through interviews with mHealth experts. These insights, gathered from multiple sectors, provided depth to the data analysis.

Step 4: Research Synthesis and Final Output

This final phase involved engaging with health app developers to verify data insights. Findings were synthesized to ensure a holistic, accurate analysis, forming the basis for the reports comprehensive output.

Frequently Asked Questions

01 How big is the India mHealth Apps Market?

The India mHealth Apps Market, valued at approximately USD 1.5 billion, is propelled by smartphone adoption and a growing need for accessible healthcare services.

02 What are the primary challenges in the India mHealth Apps Market?

Key challenges include data privacy issues, regulatory hurdles, and limited access to digital health solutions in rural areas, which could hinder market growth.

03 Who are the major players in the India mHealth Apps Market?

Leading players include Practo, HealthifyMe, MyUpchar, MFine, and Tata Health, each known for their comprehensive health service offerings.

04 What factors drive the growth of the India mHealth Apps Market?

The markets growth is primarily driven by rising smartphone penetration, government health initiatives, and increased demand for preventive healthcare solutions.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.