India Micro Mobility Charging Infrastructure Market Outlook to 2030

Region:Asia

Author(s):Sanjeev

Product Code:KROD9043

October 2024

91

About the Report

India Micro Mobility Charging Infrastructure Market Overview

-

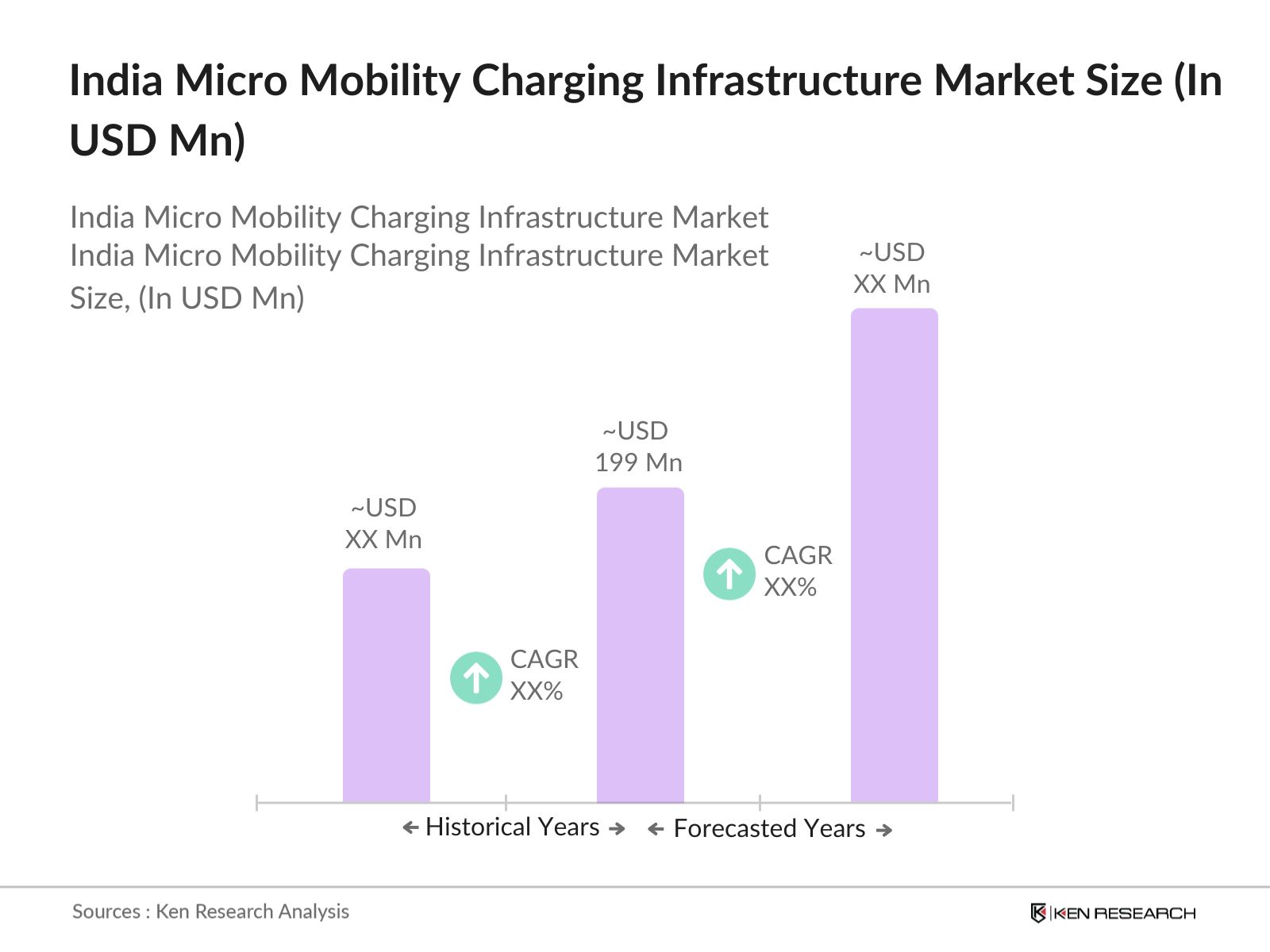

The India micro mobility charging infrastructure market is valued at USD 199 million. This growth has been driven primarily by the rapid adoption of electric two-wheelers and micro-mobility solutions like e-scooters and e-bikes in densely populated urban areas. Government initiatives such as the Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme and various state-level subsidies have propelled this market. Moreover, the increasing cost of fossil fuels has incentivized commuters to shift towards electric micro-mobility solutions, which in turn drives the demand for charging infrastructure.

- Cities like Bengaluru, Delhi, and Pune are dominant players in the micro-mobility market due to their large urban populations and congested traffic conditions, making micro-mobility a practical solution for short commutes. These cities have also been at the forefront of electric vehicle adoption, supported by municipal policies aimed at reducing air pollution. Additionally, these regions have a higher concentration of tech-savvy consumers who are early adopters of green technologies like electric vehicles.

- Public-private partnerships (PPPs) are playing a vital role in developing Indias EV charging infrastructure. In 2023, the Government of India partnered with several private entities, including Tata Power and NTPC, to establish 100,000 charging stations across the country. These collaborations are essential in scaling infrastructure to meet the growing demand for electric micro-mobility charging.

India Micro Mobility Charging Infrastructure Market Segmentation

India's micro mobility charging infrastructure market is segmented by charging type and by vehicle type.

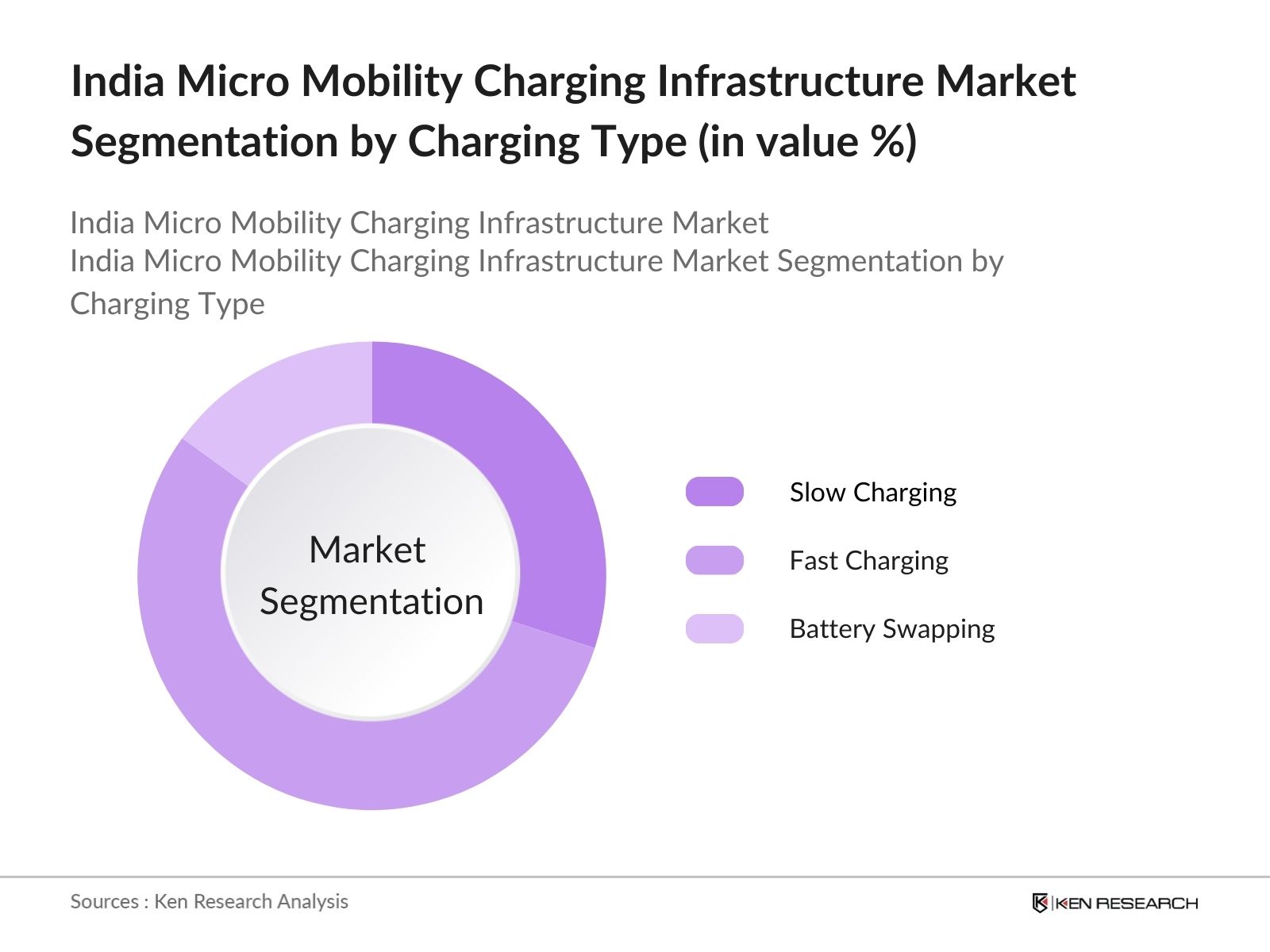

- By Charging Type: The market is segmented by charging type into slow charging, fast charging, and battery swapping. Fast charging currently holds the dominant market share due to its growing demand from fleet operators and consumers who prefer reduced downtime when charging their electric two-wheelers. Major players such as Tata Power and Ather Grid are focusing on expanding fast-charging networks in urban areas, catering to the increasing demand from micro-mobility users.

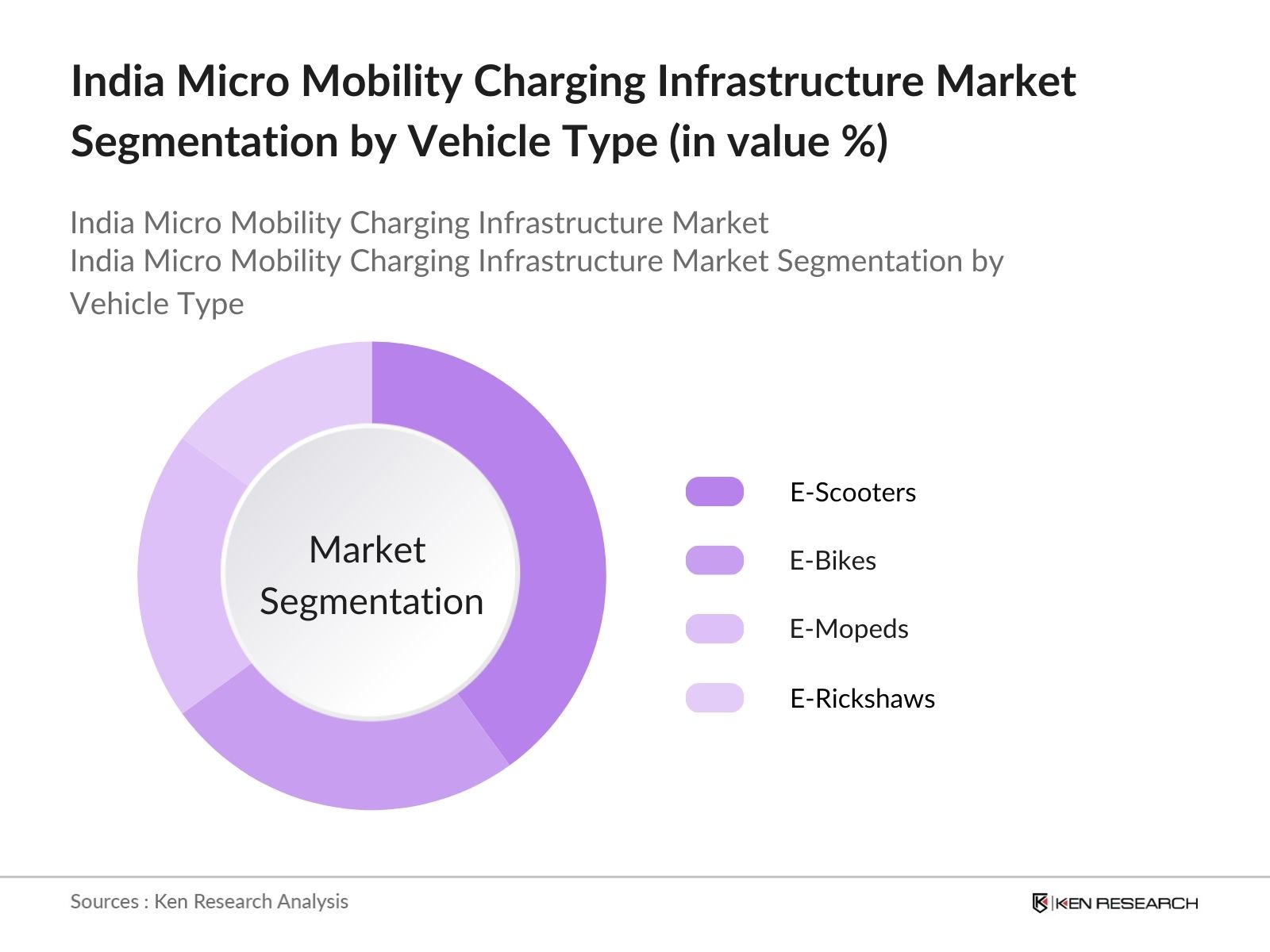

- By Vehicle Type: The micro mobility charging infrastructure market is also segmented by vehicle type into e-scooters, e-bikes, e-mopeds, and e-rickshaws. E-scooters have the largest market share because they are more versatile for urban commutes and have a higher adoption rate due to their affordability and low maintenance. E-scooters are also supported by the availability of compact and easy-to-install charging stations in densely populated cities.

India Micro Mobility Charging Infrastructure Market Competitive Landscape

The India micro mobility charging infrastructure market is highly competitive, with major players such as Tata Power, Ather Grid, and Ola Electric leading the charge. The market is characterized by a mix of established players and new entrants, all vying for market share by expanding their charging networks and collaborating with municipalities and real estate developers for infrastructure deployment. The competitive landscape is driven by the expansion of charging networks, strategic collaborations with municipal authorities, and increasing investments in technology such as fast-charging solutions and battery-swapping technology.

|

Company Name |

Established Year |

Headquarters |

Charging Stations Installed |

Revenue (USD Mn) |

Technology Patents |

Strategic Partnerships |

Regions Covered |

CapEx |

|

Tata Power |

1919 |

Mumbai |

- | - | - | - | - | - |

|

Ather Grid |

2013 |

Bengaluru |

- | - | - | - | - | - |

|

Ola Electric |

2017 |

Bengaluru |

- | - | - | - | - | - |

|

Magenta Power |

2017 |

Navi Mumbai |

- | - | - | - | - | - |

|

Sun Mobility |

2017 |

Bengaluru |

- | - | - | - | - | - |

India Micro Mobility Charging Infrastructure Industry Analysis

Growth Drivers

- Increasing Urbanization: India's urban population is expected to reach over 500 million by 2025, as per World Bank estimates, driving the demand for efficient transportation solutions, including electric micro-mobility options. The growing congestion in cities like Mumbai and Delhi has made micro-mobility solutions more attractive due to their ease of maneuverability. Additionally, the Indian government has invested in urban infrastructure, such as smart cities and electric vehicle (EV) infrastructure, enhancing the ecosystem for micro-mobility services. This growing urban density fuels the need for robust charging infrastructure to support micro-mobility solutions.

- Rise in Electric Micro-Mobility Adoption: India is witnessing a surge in the adoption of electric micro-mobility vehicles such as electric scooters, e-bikes, and e-rickshaws. According to the Ministry of Heavy Industries, over 600,000 electric two-wheelers were sold in 2023, significantly driving the need for enhanced charging infrastructure. As cities move towards greener transport options, this adoption rate is expected to fuel the growth of charging stations in urban and semi-urban areas.

- Government Policies Promoting Electric Vehicles: The Government of India has been proactive in supporting electric vehicle adoption through the Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme. In 2024, the FAME II scheme had a budget outlay of INR 10,000 crore, focusing on establishing a nationwide charging infrastructure. Furthermore, state-level policies are promoting private sector participation in charging infrastructure, reducing the financial burden on the government. This policy-driven approach is expected to significantly impact the micro-mobility charging infrastructure market.

Market Challenges

- High Capital Investment Requirements: Setting up charging infrastructure for micro-mobility requires substantial capital investment, with each station costing between INR 10 lakh to INR 20 lakh. This high cost, which includes land acquisition, installation, and ongoing maintenance, presents a significant challenge for both public and private entities. Despite government incentives, the initial capital outlay remains a significant barrier, particularly for smaller cities and less economically vibrant regions in India.

- Limited Battery Capacity of Micro-Mobility Devices: Most electric micro-mobility vehicles, such as e-scooters and e-bikes, have a limited battery range of around 50-70 kilometers per charge. This limitation creates frequent demand for charging, which increases pressure on the existing infrastructure. Until there is a breakthrough in battery technology, this will remain a challenge for the effective operation of a widespread micro-mobility charging network.

India Micro Mobility Charging Infrastructure Market Future Outlook

Over the next five years, the India micro mobility charging infrastructure market is expected to experience significant growth, driven by continuous government support, the expansion of electric micro-mobility options, and investments in fast-changing technologies. Companies are increasingly focusing on integrating smart-grid solutions and establishing partnerships with real estate developers to install charging points in residential and commercial complexes. The market is also expected to witness the rise of battery-swapping networks, particularly in urban areas, as a quick and convenient alternative for micro-mobility users.

Future Market Opportunities

- Development of Fast Charging Technologies: The demand for fast-charging technology is rising, especially as users seek convenience and quicker charging times. Several companies have developed charging solutions that can power a micro-mobility vehicle in under an hour. For instance, Ola Electric's hypercharger network is designed to charge their e-scooters in less than 30 minutes. The rollout of such technologies will enhance the appeal of electric micro-mobility vehicles, boosting infrastructure development.

- Integration with Smart Grid Solutions: The integration of EV charging infrastructure with smart grid solutions presents a significant opportunity for optimizing energy use. By connecting charging stations to the national grid and allowing for real-time data exchange, utilities can manage load distribution more efficiently. This integration also opens opportunities for renewable energy usage in the charging process, reducing the environmental impact. Smart grid systems have already been piloted in cities like Delhi, where 300 smart meters were installed in 2023 to support EV charging stations.

Scope of the Report

|

|||||||||

|

By Vehicle Type |

|

||||||||

|

|

||||||||

|

By Power Output |

|

||||||||

|

By Region |

North East West South |

|

|

Slow Charging |

|

Fast Charging |

|

Battery Swapping |

|

E-Scooters |

|

E-Bikes |

|

E-Mopeds |

|

E-Rickshaws |

|

By End-User |

|

Residential |

|

Commercial Fleets |

|

Government Initiatives |

|

Less than 2kW |

|

2kW - 7kW |

|

More than 7kW |

Products

Key Target Audience

Electric Vehicle Manufacturers

Charging Infrastructure Providers

Government and Regulatory Bodies (Ministry of Power, Ministry of Road Transport & Highways)

Urban Mobility Solution Providers

Investors and Venture Capitalist Firms

Banks and Financial Institutes

Municipal Corporations and Urban Development Authorities

Real Estate Developers and Property Owners

Technology Providers (Charging Technology, Smart Grid Solutions)

Companies

Players Mention in the Report:

Tata Power

Ather Grid

Ola Electric

Magenta Power

Sun Mobility

Fortum India

EV Motors India

ChargeGrid (Exicom)

Volttic

Hero Electric

Reliance New Energy

Delta Electronics India

ABB India

Statiq

Bosch Indi

Table of Contents

1. India Micro Mobility Charging Infrastructure Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. India Micro Mobility Charging Infrastructure Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. India Micro Mobility Charging Infrastructure Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Urbanization

3.1.2. Rise in Electric Micro-Mobility Adoption

3.1.3. Government Policies Promoting Electric Vehicles

3.1.4. Expansion of Charging Infrastructure by Private Entities

3.2. Market Challenges

3.2.1. High Capital Investment Requirements

3.2.2. Limited Battery Capacity of Micro-Mobility Devices

3.2.3. Land Acquisition Issues for Charging Stations

3.3. Opportunities

3.3.1. Development of Fast Charging Technologies

3.3.2. Integration with Smart Grid Solutions

3.3.3. Increased Demand for Shared Mobility Solutions

3.4. Trends

3.4.1. Adoption of Battery Swapping Technology

3.4.2. Expansion of Charging Networks in Tier 2 and Tier 3 Cities

3.4.3. Collaborations Between OEMs and Charging Solution Providers

3.5. Government Regulation

3.5.1. Electric Vehicle Charging Guidelines

3.5.2. National Electric Mobility Mission Plan

3.5.3. Public-Private Partnerships for Charging Infrastructure

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Ecosystem

4. India Micro Mobility Charging Infrastructure Market Segmentation

4.1. By Charging Type (In Value %)

4.1.1. Slow Charging

4.1.2. Fast Charging

4.1.3. Battery Swapping

4.2. By Vehicle Type (In Value %)

4.2.1. E-Scooters

4.2.2. E-Bikes

4.2.3. E-Mopeds

4.2.4. E-Rickshaws

4.3. By End-User (In Value %)

4.3.1. Residential

4.3.2. Commercial Fleets

4.3.3. Government Initiatives

4.4. By Power Output (In Value %)

4.4.1. Less than 2kW

4.4.2. 2kW - 7kW

4.4.3. More than 7kW

4.5. By Region (In Value %)

4.5.1. Northern India

4.5.2. Southern India

4.5.3. Western India

4.5.4. Eastern India

5. India Micro Mobility Charging Infrastructure Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Tata Power

5.1.2. Fortum India

5.1.3. Ather Grid

5.1.4. Magenta Power

5.1.5. Reliance New Energy

5.1.6. Hero Electric

5.1.7. Ola Electric

5.1.8. EV Motors India

5.1.9. ChargeGrid (Exicom)

5.1.10. Sun Mobility

5.1.11. Volttic

5.1.12. Delta Electronics India

5.1.13. ABB India

5.1.14. Statiq

5.1.15. Bosch India

5.2 Cross Comparison Parameters (Market Share, Installed Charging Stations, Service Areas, Revenue, Strategic Partnerships, Technology Patents, CapEx, Power Output Capability)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. India Micro Mobility Charging Infrastructure Market Regulatory Framework

6.1. EV Charging Guidelines

6.2. Government Incentives for Infrastructure Development

6.3. Charging Station Certification and Standards

7. India Micro Mobility Charging Infrastructure Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. India Micro Mobility Charging Infrastructure Future Market Segmentation

8.1. By Charging Type (In Value %)

8.2. By Vehicle Type (In Value %)

8.3. By End-User (In Value %)

8.4. By Power Output (In Value %)

8.5. By Region (In Value %)

9. India Micro Mobility Charging Infrastructure Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. White Space Opportunity Analysis

9.3. Marketing Strategies for Market Penetration

9.4. Customer Segment Analysis

Research Methodology

Step 1: Identification of Key Variables

The first step involves mapping out the ecosystem of stakeholders in the India micro mobility charging infrastructure market. This includes a combination of desk research and proprietary databases to identify and define the critical variables that impact the market, such as charging station density, government regulations, and adoption rates of micro-mobility solutions.

Step 2: Market Analysis and Construction

In this step, historical market data is compiled and analyzed to understand the market dynamics of micro-mobility charging infrastructure. Metrics like the number of charging stations, charging infrastructure penetration, and vehicle-charger ratios are assessed to construct a reliable market model.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses developed during data analysis are validated through interviews with industry experts from major companies in the sector. These consultations help in gaining insights into operational and financial aspects of the market, further refining the data.

Step 4: Research Synthesis and Final Output

The final stage involves direct engagement with micro-mobility solution providers and charging station operators to validate data obtained from the bottom-up approach. This includes gathering detailed insights into product segments, customer preferences, and the expansion plans of key players in the market.

Frequently Asked Questions

01. How big is India Micro Mobility Charging Infrastructure Market?

The India micro mobility charging infrastructure market is valued at USD 199 million, driven by the rapid growth of electric two-wheelers and micro-mobility solutions in urban areas.

02. What are the challenges in India Micro Mobility Charging Infrastructure Market?

Key challenges in India micro mobility charging infrastructure market include high capital investment for setting up charging stations, land acquisition hurdles, and the lack of fast-charging infrastructure in tier 2 and tier 3 cities.

03. Who are the major players in India Micro Mobility Charging Infrastructure Market?

Key players in India micro mobility charging infrastructure market include Tata Power, Ather Grid, Ola Electric, Magenta Power, and Sun Mobility. These companies dominate due to their extensive charging networks and strategic partnerships with municipalities and urban developers.

04. What are the growth drivers of India Micro Mobility Charging Infrastructure Market?

Growth drivers in India micro mobility charging infrastructure market include increasing government support for electric vehicles, the rising adoption of electric micro-mobility solutions, and advancements in fast-changing technology.

05. What are the market trends in India Micro Mobility Charging Infrastructure Market?

Key trends in India micro mobility charging infrastructure market include the rise of battery-swapping networks, increased deployment of fast chargers in urban areas, and growing collaborations between real estate developers and charging solution providers.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.