India Nutraceuticals Market Outlook 2030

Region:India

Author(s):Harsh Saxena

Product Code:KR1550

Region:India

Author(s):Harsh Saxena

Product Code:KR1550

December 2024

99

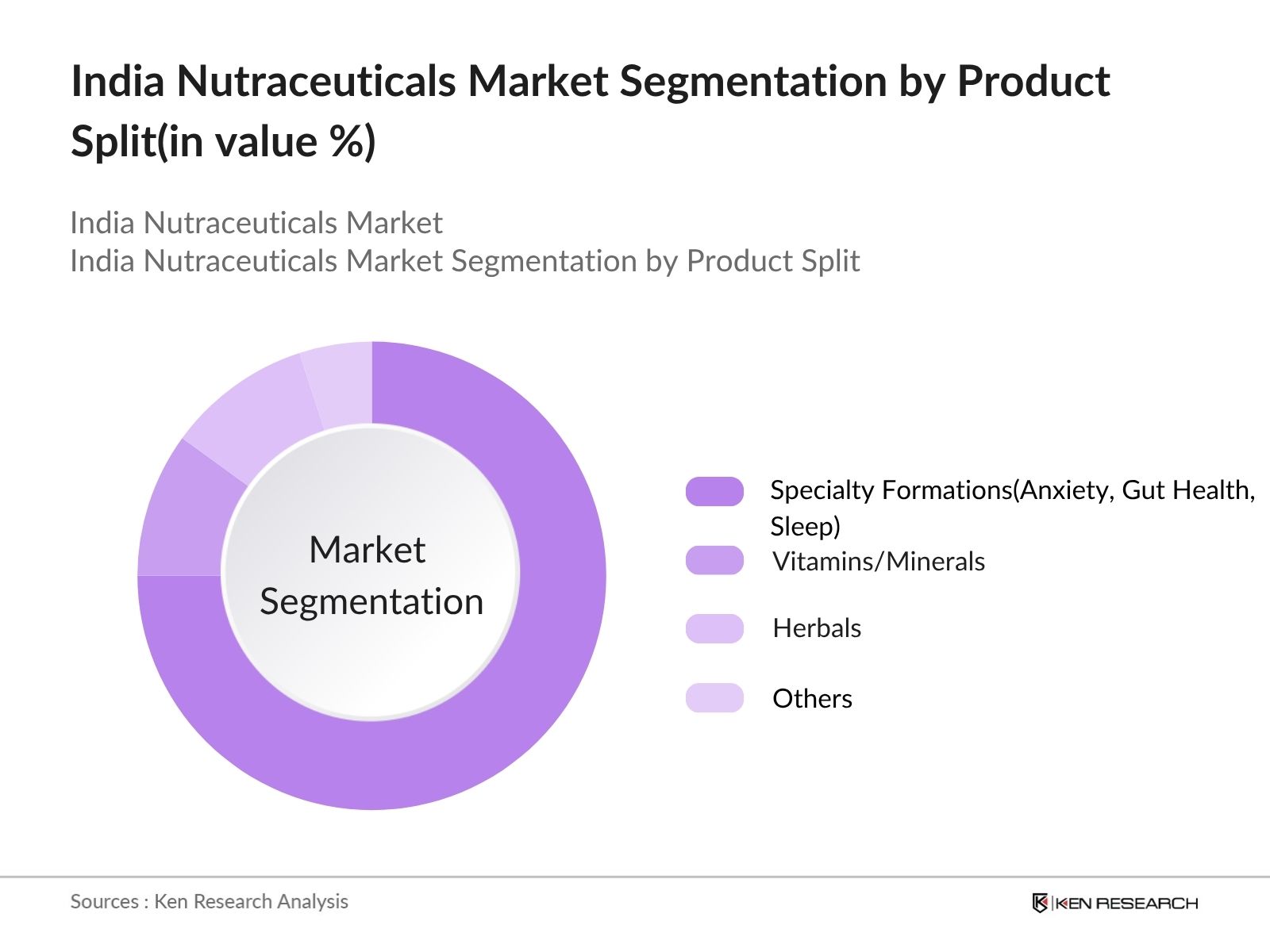

By Product Split: The India nutraceuticals market is segmented into Specialty Formulations, Herbals, Vitamins/Minerals, and Others. Specialty formulations—covering gut health, sleep, and anxiety—lead the market, driven by rising lifestyle stress and preventive health trends. Herbals are gaining strong traction due to increased consumer preference for Ayurveda and plant-based products. Vitamins and minerals also contribute significantly, as awareness around immunity and nutritional balance continues to grow. The market’s expansion is underpinned by a holistic wellness shift, with all segments reflecting strong growth across urban and semi-urban areas.

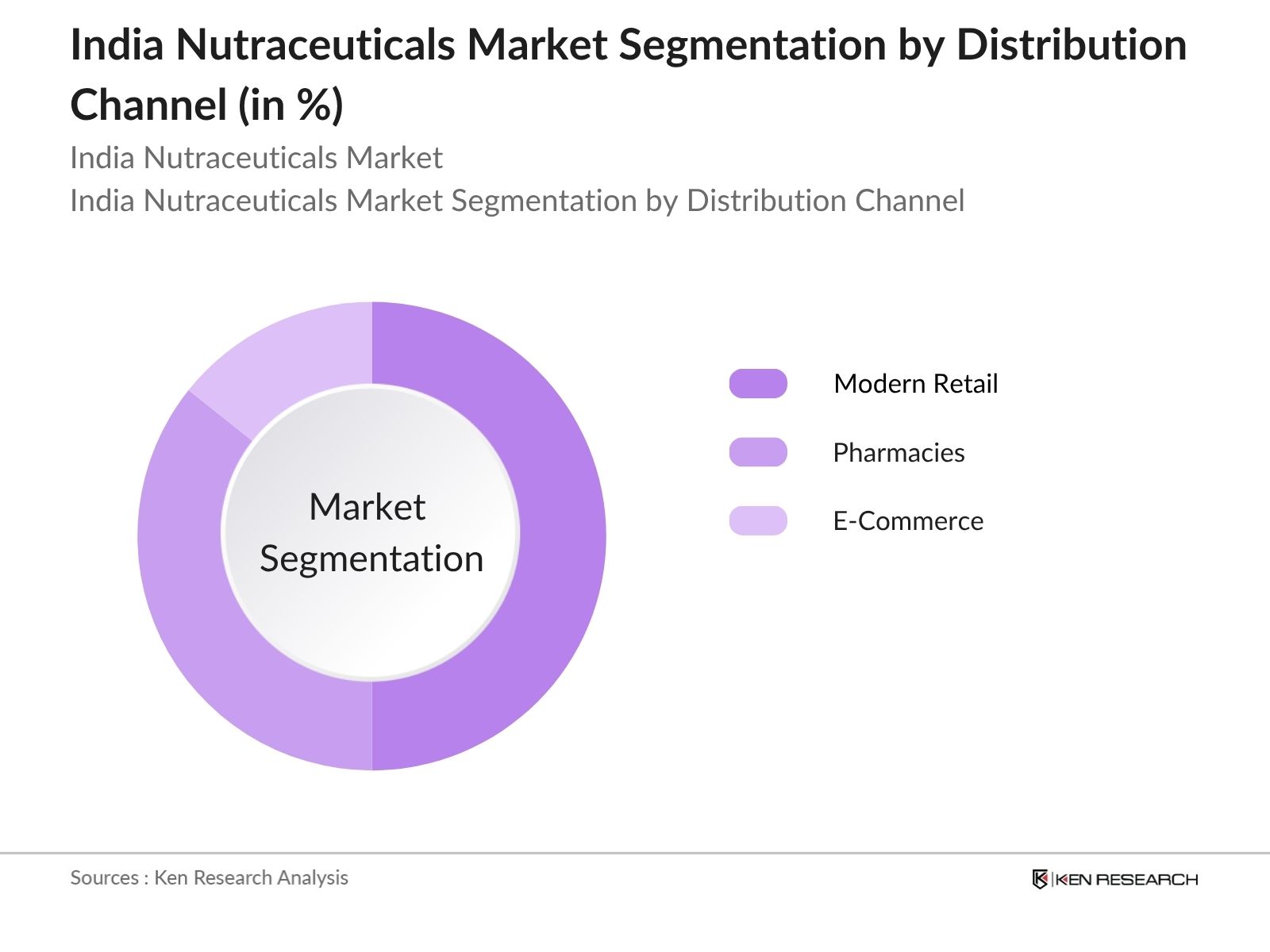

By Distribution Channel: The India nutraceuticals market is segmented into Modern Retail, Pharmacies, and E-Commerce. Modern retail dominates the landscape due to its wide reach, standardized quality, and growing presence in Tier I and Tier II cities. Pharmacies continue to serve as a trusted source for health supplements, especially among older consumers. However, E-commerce is the fastest-growing channel, driven by rising digital adoption and strategic partnerships with pharmacy chains. Online platforms like Tata 1mg, Netmeds, and Apollo 24/7 are making doorstep delivery, personalization, and competitive pricing more accessible to health-conscious consumers across India.

The India nutraceuticals market is dominated by both multinational and local players. Companies like Dabur and Patanjali Ayurved dominate the herbal and Ayurvedic segments, while global brands like GNC and Amway are strong in vitamins and dietary supplements. The competition is high, with players investing heavily in R&D, marketing, and distribution networks to stay ahead. The introduction of innovative products and strategic partnerships with e-commerce platforms have further intensified competition in the market.

|

Company |

Established |

Headquarters |

R&D Investment |

Distribution Network |

Product Range |

Revenue (USD Bn) |

Geographical Reach |

Partnerships |

|

Patanjali Ayurved Ltd. |

2006 |

Haridwar, India |

||||||

| Zydus (Cadila Healthcare) | 1952 | Gujarat, India | ||||||

| Abbott | 1888 | Chicago, Illinois, USA | ||||||

| Dr. Reddy's Laboratories Ltd. | 1984 | Hyderabad, India | ||||||

| Cipla Ltd. | 1935 | Mumbai, India |

Over the next five years, the India nutraceuticals market is expected to show robust growth due to increasing consumer awareness, government initiatives, and advancements in product innovation. The shift towards preventive healthcare, combined with the increasing penetration of e-commerce, is likely to drive significant demand for nutraceuticals. Additionally, growing disposable income levels will make premium nutraceutical products more accessible to a broader audience, further boosting market growth.

|

By Product Split |

Specialty Formations(Anxiety, Gut Health, Sleep) Vitamins/Minerals Herbals Others |

|

By Distribution Channel |

Modern Retail Pharmacies E-Commerce |

3.1.1. By Type of Product Split, FY’25 – FY’30F

3.1.2. By Type of Distribution Channel, FY’25 – FY’30F

Emerging Consumer Health & Wellness Trends

Impact of Urbanization on Nutraceutical Demand

Consolidated Research Approach

The research process begins with constructing a comprehensive ecosystem map of stakeholders within the India Nutraceuticals Market. Extensive desk research is conducted using both proprietary and public databases to gather accurate industry-level information. Critical variables influencing the market, such as consumer behavior, regulatory impacts, and market dynamics, are identified.

Historical data for the India nutraceuticals market is compiled, covering factors such as product penetration, consumer preferences, and regional market variations. The gathered data is analyzed to estimate market revenues and growth rates. Particular attention is paid to ensuring data reliability and accuracy, using multiple data points.

The formulated market hypotheses are validated through direct interviews with industry experts. This is done using CATI (Computer Assisted Telephone Interviews), engaging key stakeholders such as nutraceutical manufacturers, distributors, and industry analysts. These consultations provide deep insights into operational and financial aspects of the market.

The final phase includes synthesizing all research findings into a cohesive report. In addition to numerical insights, qualitative inputs from nutraceutical manufacturers and industry experts are used to refine the market analysis. This ensures a well-rounded and accurate depiction of the India nutraceuticals market.

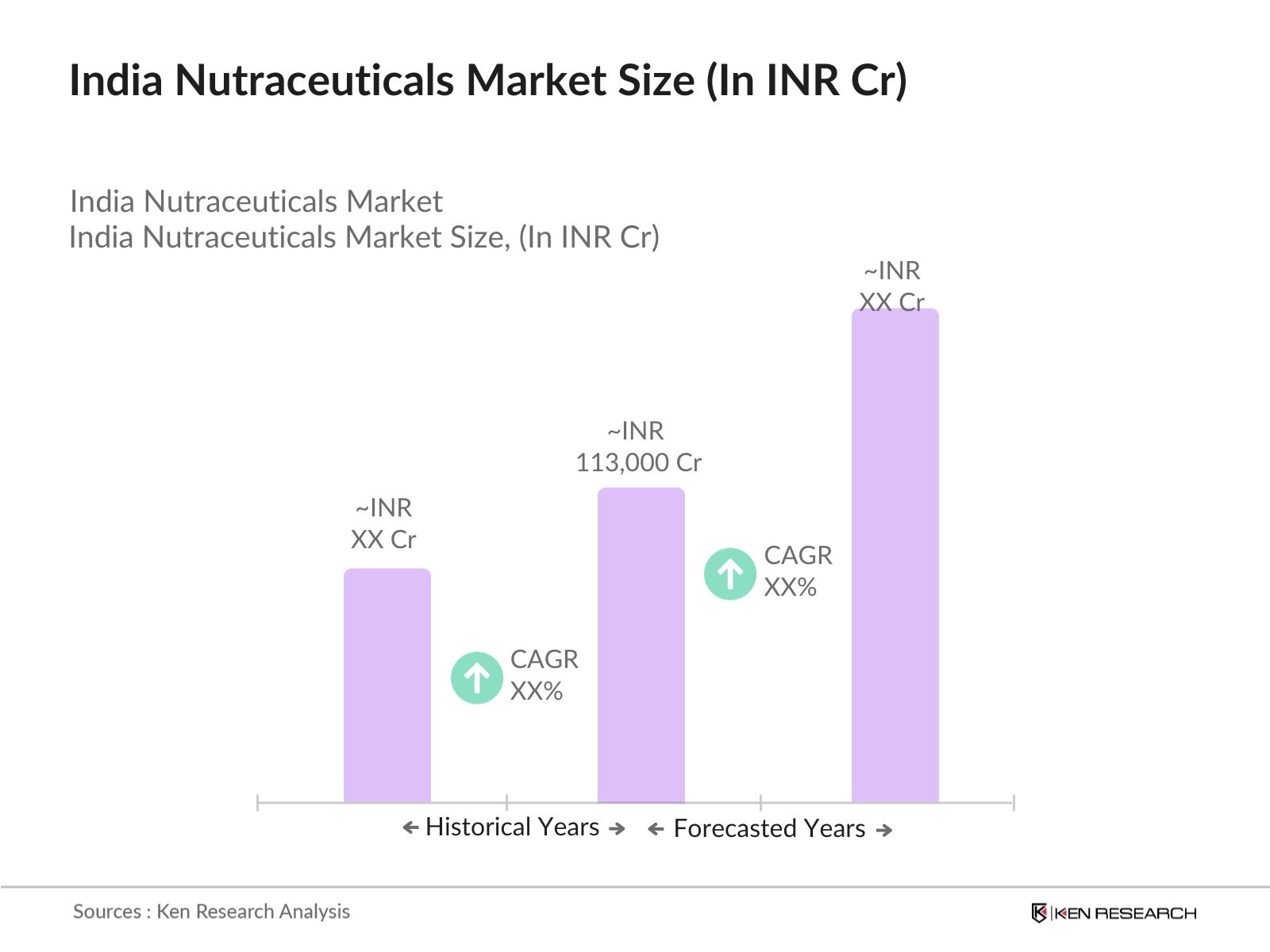

The India nutraceuticals market is valued at INR 113,000 Crores. The market is driven by increasing consumer demand for preventive healthcare solutions, such as dietary supplements and functional foods, amid growing health awareness.

Key challenges include stringent regulatory compliance under FSSAI, limited consumer trust in the efficacy of nutraceutical ingredients, and a fragmented supply chain, which affects the timely distribution of products.

The major players include Dabur India Ltd., Patanjali Ayurved Ltd., Himalaya Drug Company, GNC Holdings Inc., and Amway India Enterprises. These companies are leaders due to their extensive product range and strong distribution networks.

Growth is driven by increasing health awareness, favorable government initiatives, and rising disposable incomes. The expanding e-commerce platforms are also boosting nutraceutical sales, allowing for wider market penetration.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.