India Orthopedic Market Outlook to 2030

Region:Asia

Author(s):Meenakshi Bisht

Product Code:KROD2700

Region:Asia

Author(s):Meenakshi Bisht

Product Code:KROD2700

December 2024

90

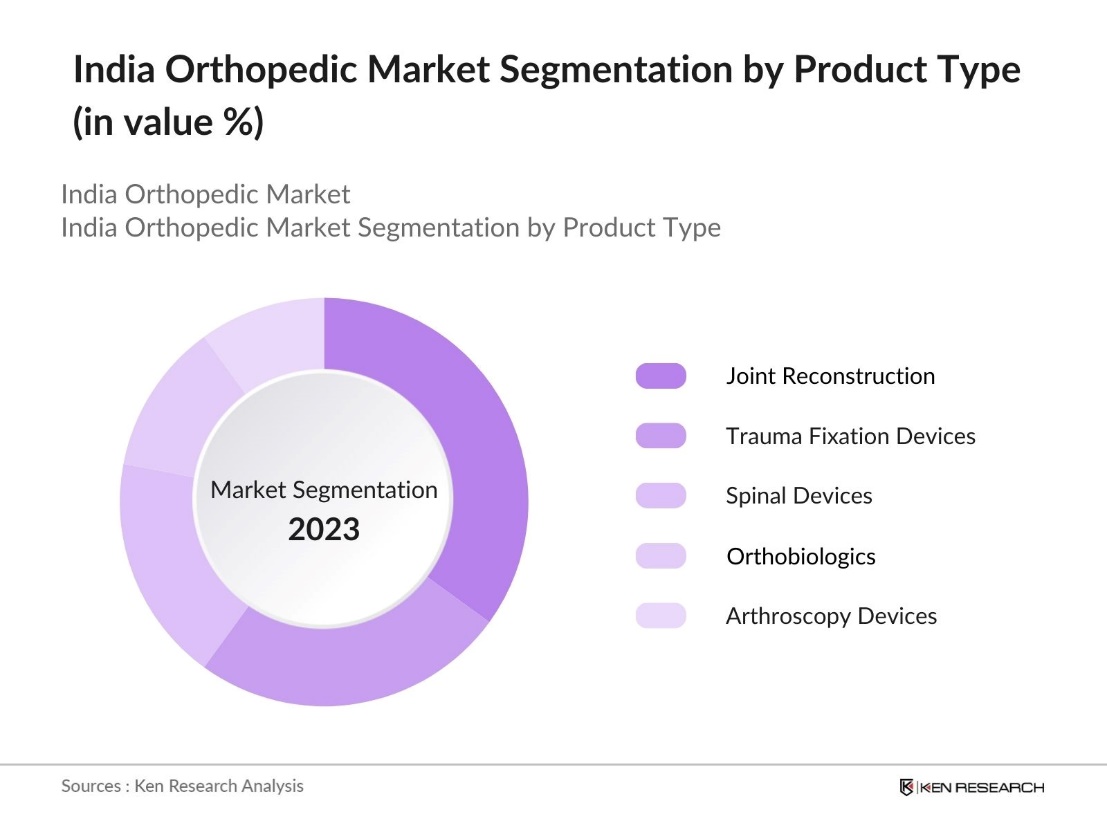

By Product Type: The India Orthopedic Market is segmented by product type into joint reconstruction devices, trauma fixation devices, spinal devices, orthobiologics, and arthroscopy devices. Among these, joint reconstruction devices dominate the market due to the high prevalence of knee and hip replacement surgeries. The aging population, particularly in urban areas, drives the demand for these devices as degenerative joint diseases become more common. Additionally, advancements in implant materials and techniques, such as minimally invasive surgeries, have increased patient satisfaction and recovery outcomes, further strengthening the dominance of this segment.

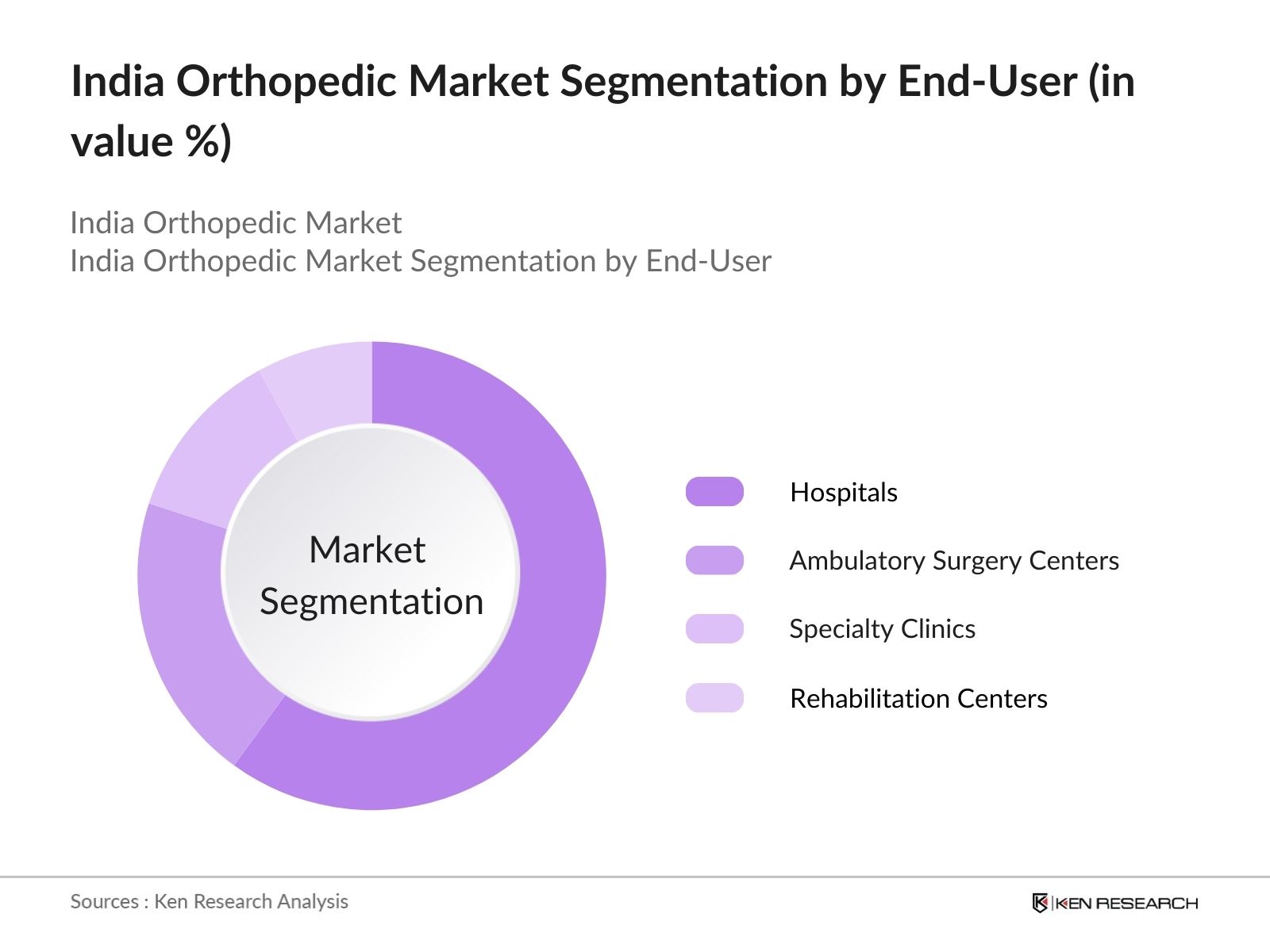

By End-User: The India Orthopedic Market is segmented by end-user into hospitals, ambulatory surgery centers (ASCs), specialty clinics, and rehabilitation centers. Hospitals hold the dominant market share in this segment due to their advanced infrastructure, the availability of expert surgeons, and the capacity to perform complex surgeries. Furthermore, hospitals are well-equipped with cutting-edge technologies, such as robotic surgery and 3D-printed implants, which makes them the preferred choice for orthopedic treatments, especially for procedures requiring multidisciplinary teams.

The market is characterized by the presence of both global and domestic players. Leading companies focus on product innovation, technological advancements, and collaborations to gain a competitive edge. Companies like Johnson & Johnson and Stryker have a significant foothold, attributed to their extensive portfolios and strong distribution networks.

|

Company Name |

Establishment Year |

Headquarters |

Product Portfolio |

Revenue (INR Bn) |

Innovation Index |

Market Presence |

R&D Investment |

No. of Employees |

|

Johnson & Johnson Pvt. Ltd. |

1886 |

New Jersey, USA |

||||||

|

Stryker India Pvt. Ltd. |

1941 |

Michigan, USA |

||||||

|

Zimmer Biomet Holdings, Inc. |

1927 |

Indiana, USA |

||||||

|

Smith & Nephew Plc |

1856 |

London, UK |

||||||

|

Medtronic India Pvt. Ltd. |

1949 |

Minnesota, USA |

Over the next five years, the India Orthopedic Market is expected to witness steady growth driven by factors such as technological advancements in robotic-assisted surgeries, increasing medical tourism, and a growing focus on minimally invasive procedures. The expansion of healthcare infrastructure in tier-2 and tier-3 cities is also likely to boost the demand for orthopedic devices. Moreover, the development of cost-effective solutions for joint replacement surgeries, along with the governments initiatives to improve healthcare access and affordability, will further accelerate market growth.

|

By Product Type |

Joint Reconstruction Devices Trauma Fixation Devices Spinal Devices Orthobiologics Arthroscopy Devices |

|

By End-User |

Hospitals Ambulatory Surgery Centers (ASCs) Specialty Clinics Rehabilitation Centers |

|

By Surgical Approach |

Open Surgery Minimally Invasive Surgery Robotic-Assisted Surgery |

|

By Technology |

3D Printing, Robotics Augmented Reality (AR) AI-Based Diagnostics |

|

By Region |

North South East West |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Aging Population

3.1.2. Increasing Incidence of Osteoporosis and Arthritis

3.1.3. Rise in Trauma Cases (Road Accidents, Sports Injuries)

3.1.4. Healthcare Infrastructure Development

3.2. Market Restraints

3.2.1. High Cost of Orthopedic Devices

3.2.2. Reimbursement Issues

3.2.3. Regulatory Hurdles

3.3. Opportunities

3.3.1. Advancements in 3D Printing and Robotics

3.3.2. Rise in Medical Tourism

3.3.3. Increasing Penetration of Telemedicine

3.4. Trends

3.4.1. Growth in Minimally Invasive Surgeries

3.4.2. Shift Toward Personalized Implants

3.4.3. Digital Orthopedic Solutions

3.5. Government Regulation

3.5.1. Regulatory Approvals (CDSCO, MDR)

3.5.2. National Health Mission Initiatives

3.5.3. Price Control on Medical Devices (NPPA)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Joint Reconstruction Devices (Hip, Knee, Shoulder)

4.1.2. Trauma Fixation Devices

4.1.3. Spinal Devices

4.1.4. Orthobiologics

4.1.5. Arthroscopy Devices

4.2. By End-User (In Value %)

4.2.1. Hospitals

4.2.2. Ambulatory Surgery Centers (ASCs)

4.2.3. Specialty Clinics

4.2.4. Rehabilitation Centers

4.3. By Surgical Approach (In Value %)

4.3.1. Open Surgery

4.3.2. Minimally Invasive Surgery

4.3.3. Robotic-Assisted Surgery

4.4. By Technology (In Value %)

4.4.1. 3D Printing

4.4.2. Robotics

4.4.3. Augmented Reality (AR) for Surgery

4.4.4. AI-Based Diagnostics

4.5. By Region (In Value %)

4.5.1. North

4.5.2. South

4.5.3. East

4.5.4. West

5.1. Detailed Profiles of Major Companies

5.1.1. Johnson & Johnson Pvt. Ltd.

5.1.2. Stryker India Pvt. Ltd.

5.1.3. Zimmer Biomet Holdings, Inc.

5.1.4. Smith & Nephew Plc.

5.1.5. Medtronic India Pvt. Ltd.

5.1.6. B. Braun Medical India Pvt. Ltd.

5.1.7. Depuy Synthes India Pvt. Ltd.

5.1.8. DJO Global, Inc.

5.1.9. Arthrex, Inc.

5.1.10. Conmed Corporation

5.1.11. Integra LifeSciences Holdings Corporation

5.1.12. Wright Medical Group N.V.

5.1.13. Aesculap Implant Systems

5.1.14. NuVasive, Inc.

5.1.15. Globus Medical India Pvt. Ltd.

5.2. Cross Comparison Parameters (No. of Employees, Market Share %, Product Portfolio, Innovation Index, Revenue, Geographical Presence, Manufacturing Capacity, Research & Development Focus)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Regulatory Standards (CDSCO, CE, FDA)

6.2. Compliance Requirements (MDR, Medical Devices Rules)

6.3. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. TAM/SAM/SOM Analysis

8.2. Customer Cohort Analysis

8.3. Marketing Initiatives

8.4. White Space Opportunity Analysis

This step focuses on compiling historical data on market growth and penetration of orthopedic devices across India. The evaluation includes assessing patient demographics, device adoption rates, and procedural trends to ensure accuracy in revenue estimates.

This step focuses on compiling historical data on market growth and penetration of orthopedic devices across India. The evaluation includes assessing patient demographics, device adoption rates, and procedural trends to ensure accuracy in revenue estimates.

Consultations with orthopedic surgeons, medical device manufacturers, and healthcare providers validate market hypotheses. These expert insights contribute to the refinement of data, ensuring it reflects actual market conditions.

Direct engagement with orthopedic device companies enables detailed insights into product segments, sales performance, and consumer preferences. This step confirms the validity of the data and ensures comprehensive market analysis.

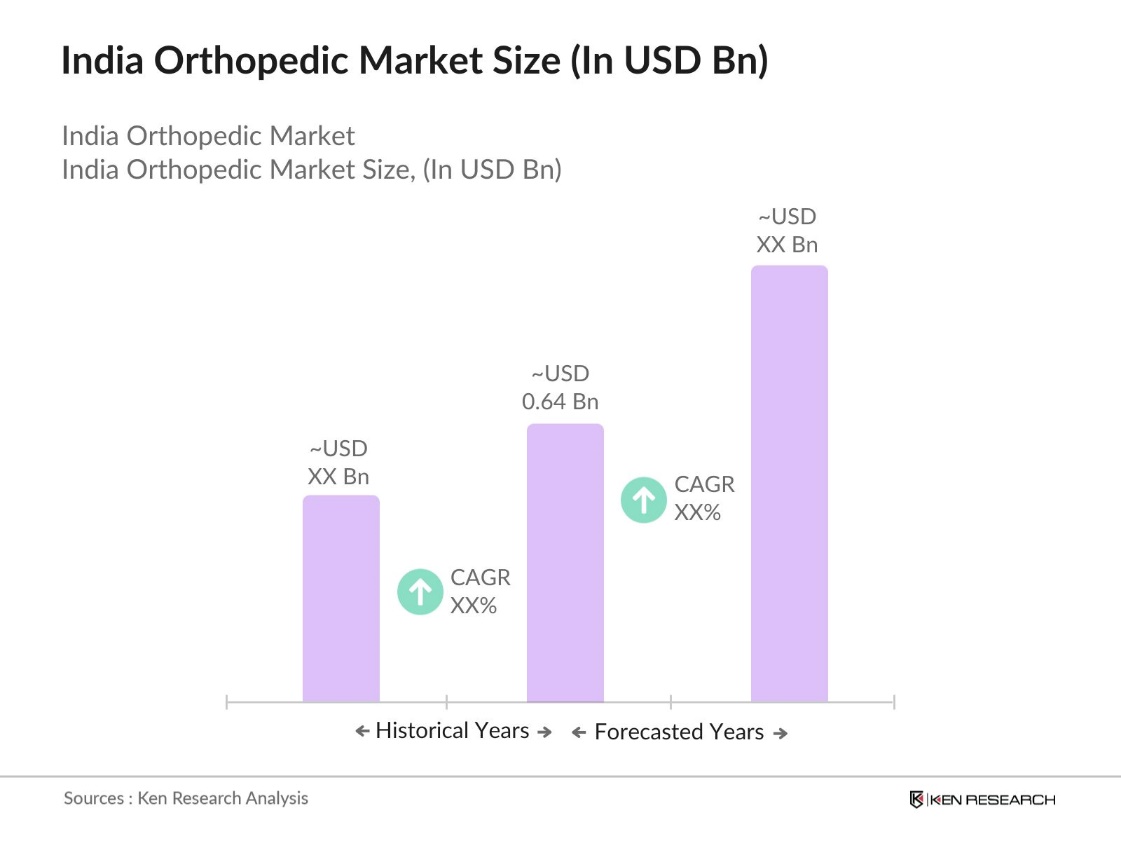

The India Orthopedic Market is valued at USD 0.64 billion, driven by the aging population, increased prevalence of joint diseases, and advances in medical technologies.

Challenges in the India Orthopedic Market include high costs of advanced devices, limited healthcare access in rural areas, and stringent regulatory requirements that delay the introduction of new products.

Key players in the India Orthopedic Market include Johnson & Johnson Pvt. Ltd., Stryker India Pvt. Ltd., Zimmer Biomet Holdings, and Smith & Nephew Plc. These companies dominate due to their strong distribution networks and focus on innovation.

The India Orthopedic Market is driven by factors such as the aging population, the rise in trauma cases, increased demand for minimally invasive surgeries, and advancements in technologies like 3D printing and robotic surgeries.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.