India Packaged Food Market Outlook to 2030

Region:India

Author(s):Yogita Sahu

Product Code:KROD10626

Region:India

Author(s):Yogita Sahu

Product Code:KROD10626

December 2024

91

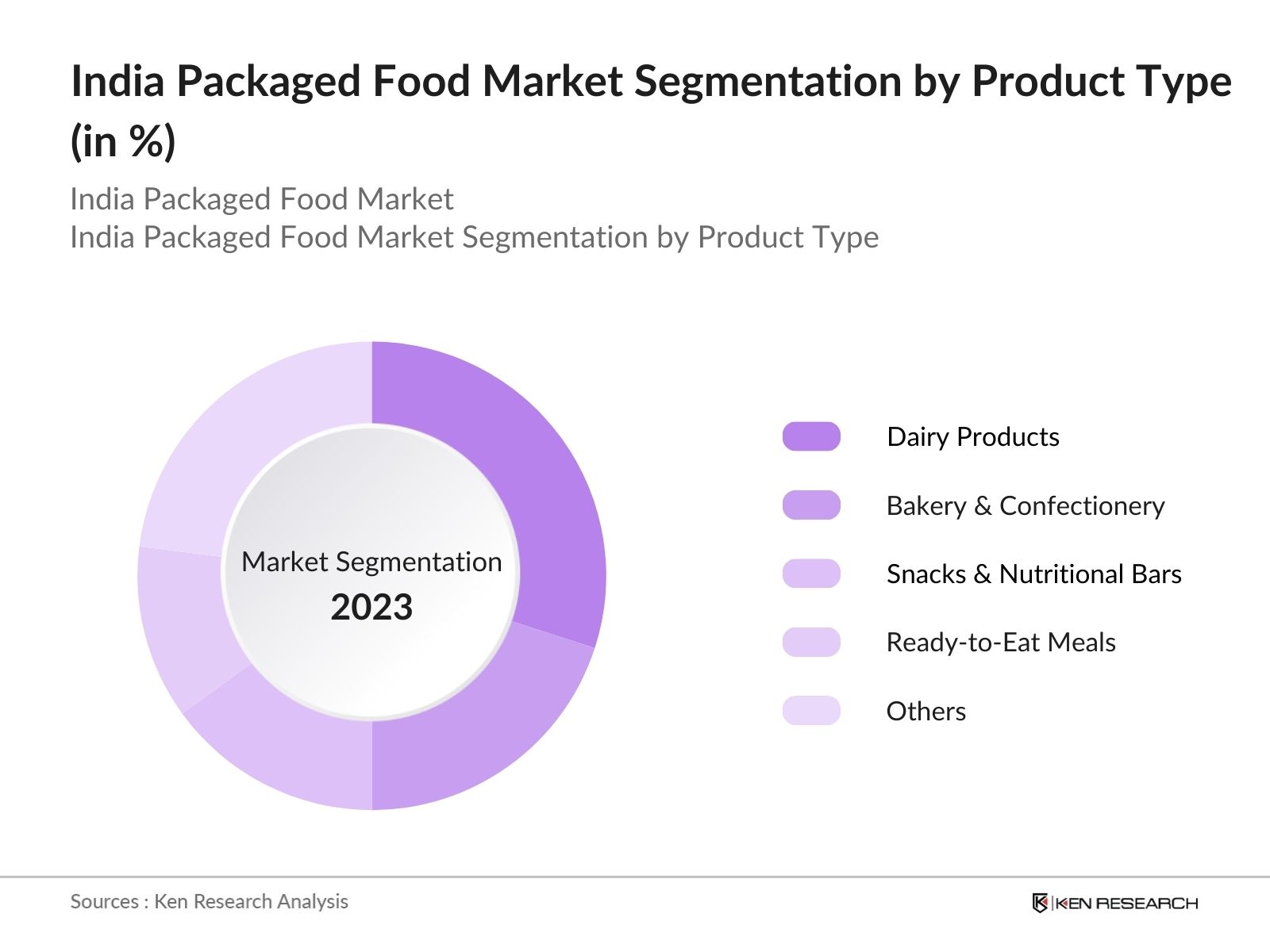

By Product Type: The market is segmented by product type into dairy products, bakery and confectionery, snacks and nutritional bars, ready-to-eat meals, beverages, and processed meats. Among these, dairy products hold a dominant market share, fueled by the strong presence of established brands and high demand for products such as milk, yogurt, and cheese. The Indian diet traditionally emphasizes dairy, making it a staple product.

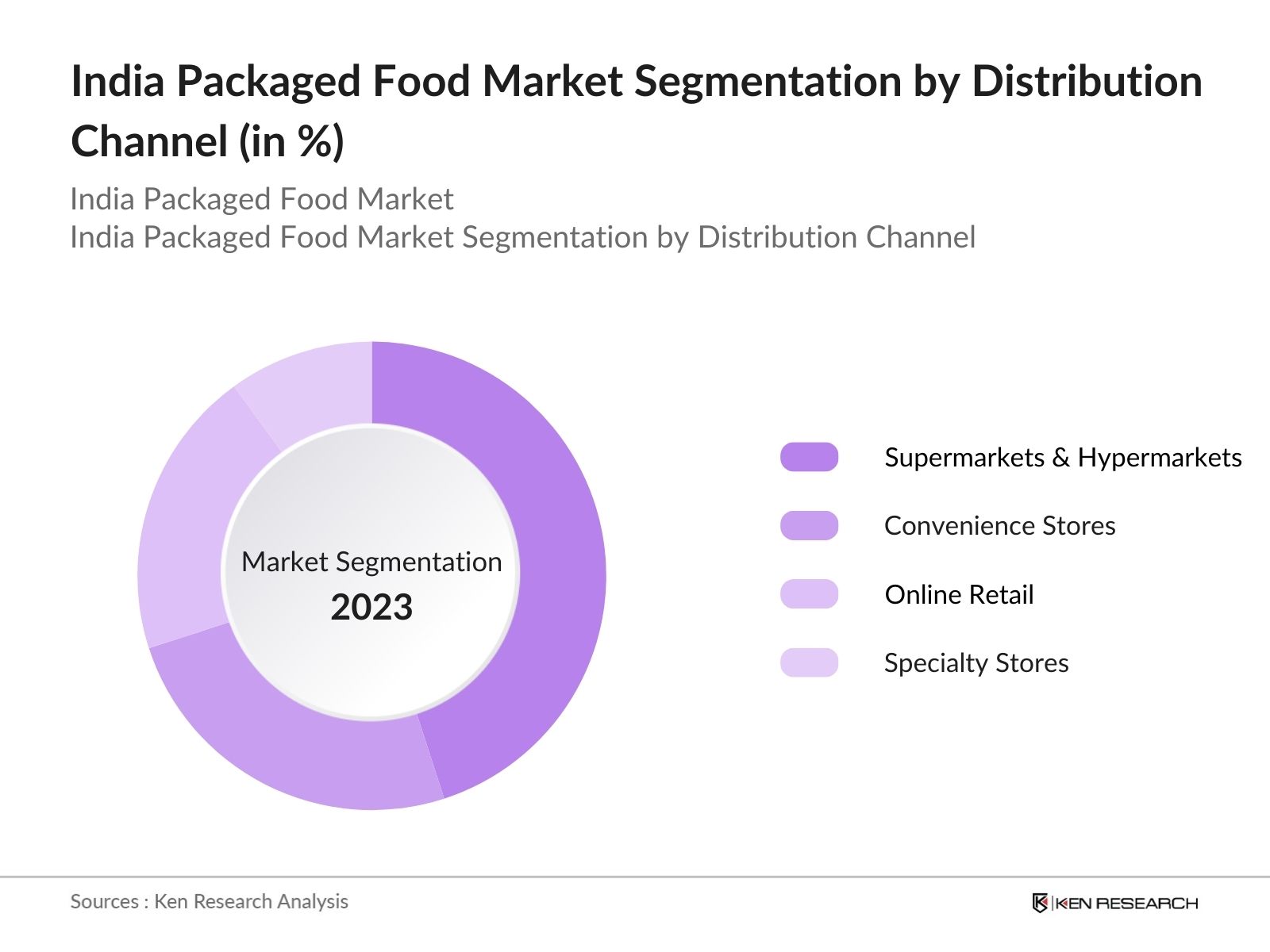

By Distribution Channel: The market is also segmented by distribution channels into supermarkets & hypermarkets, convenience stores, online retail, and specialty stores. Supermarkets and hypermarkets account for the largest market share, owing to their widespread reach, ability to offer discounts, and the availability of a variety of packaged food options under one roof. These outlets have become increasingly popular as they cater to the needs of urban consumers who seek both variety and convenience.

The market is highly competitive, with several key players dominating the landscape. These companies leverage strong brand recognition, extensive distribution networks, and continuous product innovation to maintain their market positions.

|

Company Name |

Established |

Headquarters |

Key Product Portfolio |

Revenue (USD Bn) |

Market Share (%) |

Distribution Reach |

Sustainability Initiatives |

Recent Developments |

|

Nestle India Ltd |

1961 |

Gurgaon, Haryana |

||||||

|

Britannia Industries Ltd |

1892 |

Kolkata, West Bengal |

||||||

|

ITC Limited |

1910 |

Kolkata, West Bengal |

||||||

|

Hindustan Foods Ltd |

1984 |

Mumbai, Maharashtra |

||||||

|

Parle Products Pvt Ltd |

1929 |

Mumbai, Maharashtra |

Over the next five years, the India Packaged Food industry is expected to experience sustained growth, driven by increasing demand for convenience foods, expanding urbanization, and the rise of e-commerce.

|

By Product Type |

Dairy Products Bakery Snacks RTE |

|

By Distribution |

Supermarkets Hypermarkets Online |

|

By Region |

North India South India West India East India |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate (Key Growth Metrics: Revenue Growth, Market Expansion)

1.4 Market Segmentation Overview (Core Market Segments: By Product Type, By Distribution Channel, By Region)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Growing Urbanization and Modernization

3.1.2 Expansion of Retail Sector (Contribution to Increased Consumer Access)

3.1.3 Rise in Consumer Preference for Convenience Foods

3.1.4 Government Initiatives to Boost Food Processing Infrastructure

3.2 Market Challenges

3.2.1 Health Concerns Related to Processed Foods (Public Health Impact)

3.2.2 Fluctuating Raw Material Prices (Impact on Profit Margins)

3.2.3 Regulatory Compliance and Food Safety Standards

3.2.4 Cold Chain Infrastructure Deficiency

3.3 Opportunities

3.3.1 Rising Demand for Healthy and Organic Packaged Foods

3.3.2 E-commerce Expansion in Food Retail

3.3.3 Investment in Technological Advancements (Smart Packaging, Automation)

3.4 Trends

3.4.1 Plant-Based and Vegan Foods (Growing Segment)

3.4.2 Increasing Penetration of Private Labels

3.4.3 Sustainability Trends (Eco-friendly Packaging, Reduced Food Waste)

3.5 Government Regulations

3.5.1 FSSAI Compliance for Packaged Foods

3.5.2 Initiatives Supporting Food Safety and Public Health

3.5.3 Promotion of Make in India for Packaged Foods

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.8.1 Bargaining Power of Suppliers

3.8.2 Bargaining Power of Buyers

3.8.3 Threat of New Entrants

3.8.4 Threat of Substitutes

3.8.5 Intensity of Rivalry

3.9 Competitive Landscape

4.1 By Product Type (In Value %)

4.1.1 Dairy Products

4.1.2 Bakery and Confectionery

4.1.3 Snacks and Nutritional Bars

4.1.4 Ready-to-Eat Meals

4.1.5 Beverages

4.1.6 Processed Meats

4.1.7 Rice, Pasta, & Noodles

4.1.8 Ice Creams & Frozen Novelties

4.1.9 Others (Organic Foods, Plant-based Foods)

4.2 By Distribution Channel (In Value %)

4.2.1 Supermarkets & Hypermarkets

4.2.2 Convenience Stores

4.2.3 Online Retail

4.2.4 Others (Specialty Stores)

4.3 By Region (In Value %)

4.3.1 North India

4.3.2 South India

4.3.3 East India

4.3.4 West India

5.1 Profiles of Key Companies

5.1.1 ADF Foods Ltd

5.1.2 Nestle India Ltd

5.1.3 Hatsun Agro Products

5.1.4 Britannia Industries Ltd

5.1.5 DFM Foods Ltd

5.1.6 Hindustan Foods Ltd

5.1.7 MTR Foods

5.1.8 Unilever

5.1.9 ITC Limited

5.1.10 Parle

5.1.11 Zydus Wellness Ltd

5.1.12 Gold Coin Health Foods Ltd

5.1.13 Herman Milkfoods Ltd

5.1.14 Pepsico Inc

5.1.15 General Mills Inc

5.2 Cross Comparison Parameters

(Key Parameters: Revenue, Market Presence, Product Portfolio, Distribution Network, Innovation Index, Sustainability Initiatives, Employee Count, Mergers & Acquisitions)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers And Acquisitions

5.6 Investment and Expansion Analysis

6.1 Key Regulatory Authorities

6.2 FSSAI Standards for Packaged Food

6.3 Environmental Regulations on Packaging Materials

6.4 Compliance and Certifications

7.1 Future Market Size Projections

7.2 Key Growth Drivers for Future Market Expansion

8.1 By Product Type

8.2 By Distribution Channel

8.3 By Region

9.1 TAM/SAM/SOM Analysis

9.2 Innovation and White Space Opportunity Analysis

9.3 Strategic Market Positioning

9.4 Consumer Demographic Insights and Marketing Initiatives

Disclaimer Contact UsThis stage involves identifying all key stakeholders within the India Packaged Food market, including manufacturers, distributors, and retailers. Extensive desk research was conducted, utilizing both secondary and proprietary databases to understand the market structure and key influencing factors.

Historical market data was compiled to analyze market trends and revenue generation across various segments. This phase also included a review of service quality metrics and an evaluation of supply chain infrastructure.

Hypotheses developed in the previous stages were validated through interviews with key industry experts and stakeholders. These consultations provided insights into operational efficiencies, market challenges, and growth opportunities, contributing to more accurate market estimations.

The final research output was synthesized by triangulating data from interviews and market databases. The data was further verified through consultations with top manufacturers and distributors to ensure the validity of the findings.

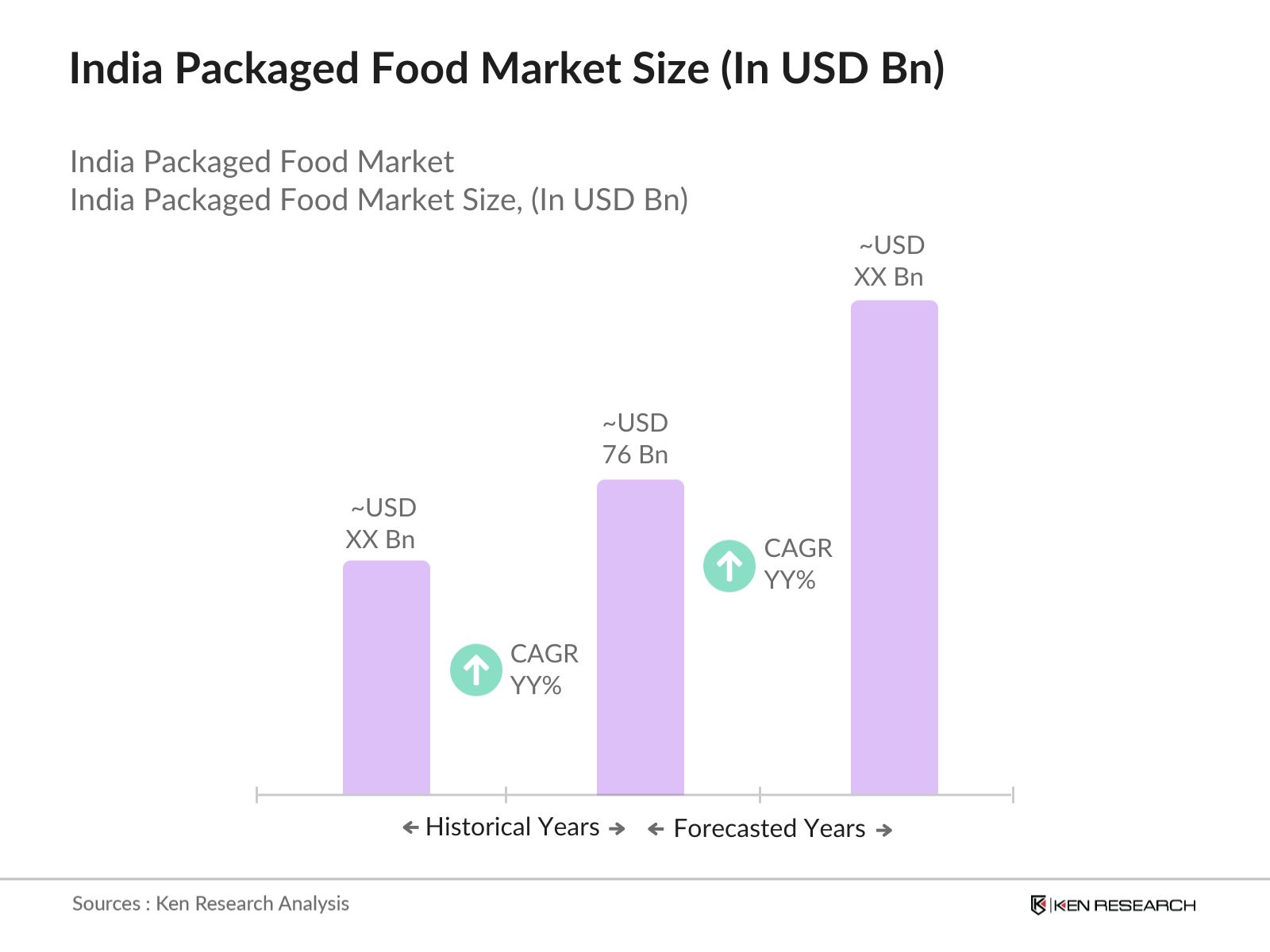

The India Packaged Food market was valued at USD 76 billion, driven by rapid urbanization, evolving consumer preferences, and the rise of modern retail formats.

Challenges in the India Packaged Food market include health concerns related to processed foods, fluctuating raw material prices, and the need for robust cold chain infrastructure to maintain product quality.

Key players in the India Packaged Food market include Nestle India Ltd, Britannia Industries Ltd, ITC Limited, Hindustan Foods Ltd, and Parle Products Pvt Ltd.

Growth drivers in the India Packaged Food market include the expansion of urban areas, increasing demand for convenience foods, and government support for the food processing sector.

The e-commerce segment is growing rapidly, with online retail expected to account for a significant share of sales in the coming years, thanks to increasing internet penetration and consumer preference for convenience.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.