India Packaging Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD11411

Region:Global

Author(s):Shivani Mehra

Product Code:KROD11411

December 2024

84

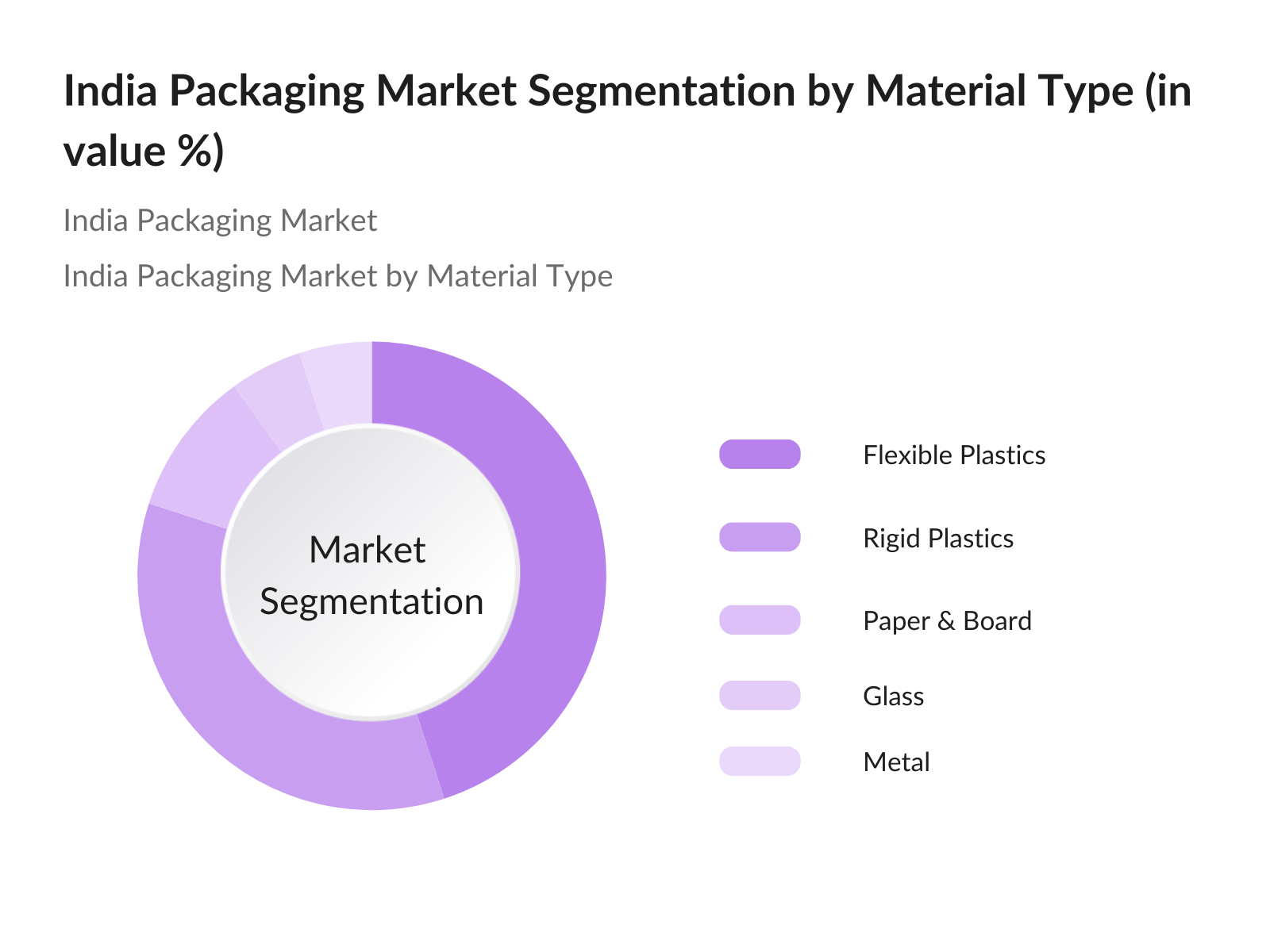

By Material Type: India's packaging market is segmented by material type into plastic, paper, glass, and metal. Among these, plastic packagingboth rigid and flexibleholds the dominant market share. The flexibility, durability, and cost-effectiveness of plastic, coupled with its widespread use in food and beverage, personal care, and pharmaceuticals, make it a preferred choice for manufacturers.

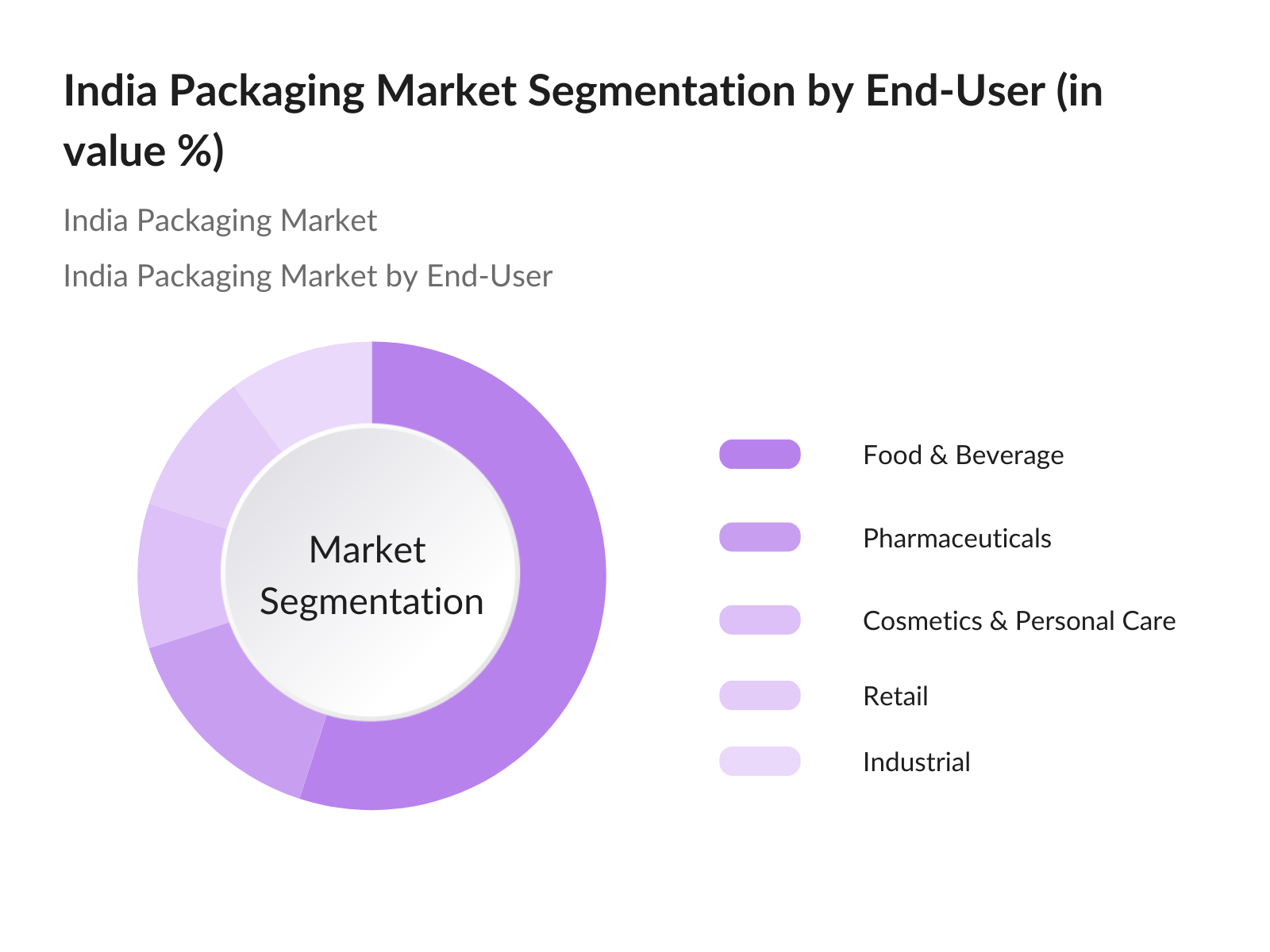

By End-User: The end-user segment is divided into food and beverage, pharmaceuticals, cosmetics, retail, and industrial sectors. The food and beverage industry dominates the market due to the rising demand for packaged food, ready-to-eat meals, and beverages. The shift towards urbanization and increased disposable income have encouraged the adoption of packaged goods. The growth of retail and online food delivery services further amplifies this demand.

The India packaging market is highly competitive, with a mix of domestic and international players. Key players dominate the landscape through strategic acquisitions, innovation, and the adoption of advanced packaging solutions. The introduction of sustainable and eco-friendly packaging alternatives has also become a major trend, as companies compete to meet regulatory demands and consumer preferences.

|

Company |

Established |

Headquarters |

Product Range |

Sustainability Initiatives |

Market Share (%) |

Manufacturing Capacity |

Regional Presence |

|

Manjushree Technopack Ltd. |

1987 |

Bengaluru |

Rigid Plastics |

- |

- |

- |

- |

|

Uflex Limited |

1983 |

Noida |

Flexible Plastics |

- |

- |

- |

- |

|

Jindal Poly Films Ltd. |

1985 |

Delhi |

BOPP Films, PET |

- |

- |

- |

- |

|

Berry Global Inc. |

1967 |

United States |

Rigid & Flexible Plastics |

- |

- |

- |

- |

|

Amcor Plc |

1860 |

Australia |

Rigid & Flexible Plastics |

- |

- |

- |

- |

Market Growth Drivers

Market Challenges:

Over the next five years, the India packaging market is expected to experience substantial growth driven by the expansion of e-commerce, increasing demand for sustainable packaging, and the growth of food and beverage packaging. The government's regulatory push for eco-friendly packaging, combined with advances in technology such as smart packaging, will play pivotal roles in the evolution of the sector. Key players will focus on innovations like biodegradable materials and the use of recycled plastics to align with the global sustainability movement.

Market Opportunities:

|

By Material Type |

Rigid Plastics Flexible Plastics Paper Glass, Metal |

|

By End-User |

Food & Beverage Pharmaceuticals Personal Car E-commerce Industrial |

|

By Technology |

Injection Molding Blow Molding Extrusion Thermoforming |

|

By Packaging Type |

Bottles & Jars, Trays Pouches Caps Cans |

|

By Region |

North-East Midwest West Coast Southern States |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size (Plastic, Paper, Metal, Glass)

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 E-Commerce Boom

3.1.2 Demand for Sustainable Packaging (Green Packaging)

3.1.3 Rising Consumer Awareness on Product Safety

3.1.4 Expanding Food & Beverage Sector

3.2 Market Challenges

3.2.1 High Raw Material Costs (Plastic Resins, Paper)

3.2.2 Government Environmental Regulations

3.2.3 Recycling Infrastructure Limitations

3.3 Opportunities

3.3.1 Technological Advancements (Smart Packaging, IoT Integration)

3.3.2 Sustainable Innovations (Bioplastics, rPET Usage)

3.3.3 Expansion in Rural and Tier-2 Markets

3.4 Trends

3.4.1 Shift to Flexible Packaging

3.4.2 Rise in Refillable and Reusable Packaging

3.4.3 Adoption of Lightweight Materials

3.5 Regulatory Framework

3.5.1 Single-Use Plastic Ban Policies

3.5.2 Extended Producer Responsibility (EPR) Guidelines

3.5.3 BIS Certification for Safety Standards

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces

3.9 Competition Ecosystem

04. India Packaging Market Segmentation

4.1 By Material Type (In Value %)

4.1.1 Rigid Plastics

4.1.2 Flexible Plastics

4.1.3 Paper & Board

4.1.4 Glass

4.1.5 Metal

4.2 By End-User (In Value %)

4.2.1 Food and Beverage

4.2.2 Pharmaceuticals and Healthcare

4.2.3 Personal Care and Cosmetics

4.2.4 Retail and E-commerce

4.2.5 Industrial and Chemical Packaging

4.3 By Technology (In Value %)

4.3.1 Injection Molding

4.3.2 Blow Molding

4.3.3 Extrusion

4.3.4 Thermoforming

4.3.5 Printing Technologies (Digital, Flexographic, Offset)

4.4 By Packaging Type (In Value %)

4.4.1 Bottles and Jars

4.4.2 Trays and Containers

4.4.3 Pouches and Sachets

4.4.4 Caps and Closures

4.4.5 Cans and Tins

4.5 By Region (In Value %)

4.5.1 North India

4.5.2 South India

4.5.3 East India

4.5.4 West India

4.5.5 Central India

5.1 Detailed Profiles of Major Companies

5.1.1 Manjushree Technopack Ltd.

5.1.2 Uflex Limited

5.1.3 Jindal Poly Films Ltd.

5.1.4 Cosmo Films Ltd.

5.1.5 Amcor Plc

5.1.6 Mold-Tek Packaging Ltd.

5.1.7 Berry Global Inc.

5.1.8 Time Technoplast Ltd.

5.1.9 ITC Limited (Packaging Division)

5.1.10 Tetra Pak India Pvt. Ltd.

5.1.11 Pearl Polymers Limited

5.1.12 Huhtamaki Oyj

5.1.13 Constantia Flexibles

5.1.14 Packman Packaging Pvt. Ltd.

5.1.15 Garware Hi-Tech Films Ltd.

5.2 Cross-Comparison Parameters (Revenue, Product Range, Regional Presence, Innovations, Sustainability Initiatives, Strategic Partnerships, Market Share, Manufacturing Capacity)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Government Grants and Policies

5.8 Private Equity and Venture Capital Funding

6.1 Environmental Standards

6.2 Compliance Requirements

6.3 Certification Processes

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Growth

8.1 By Material Type (In Value %)

8.2 By End-User (In Value %)

8.3 By Technology (In Value %)

8.4 By Packaging Type (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Strategies

9.4 White Space Opportunity Analysis

The initial stage involved identifying and mapping all relevant stakeholders in the India packaging industry. This was based on secondary research from reliable industry reports and proprietary databases to establish key influencing factors for the market.

At this phase, historical market data was gathered, focusing on packaging material demand and production across different end-use industries. The analysis included a detailed assessment of revenue generated and the role of evolving customer preferences.

Interviews were conducted with industry experts through telephonic consultations. These discussions provided deeper insights into operational challenges, financial aspects, and trends shaping the packaging industry in India, aiding the hypothesis validation process.

The final step involved verifying and synthesizing data collected from manufacturers, packaging experts, and analysts. This ensured a well-rounded and accurate representation of the market dynamics for the India packaging sector.

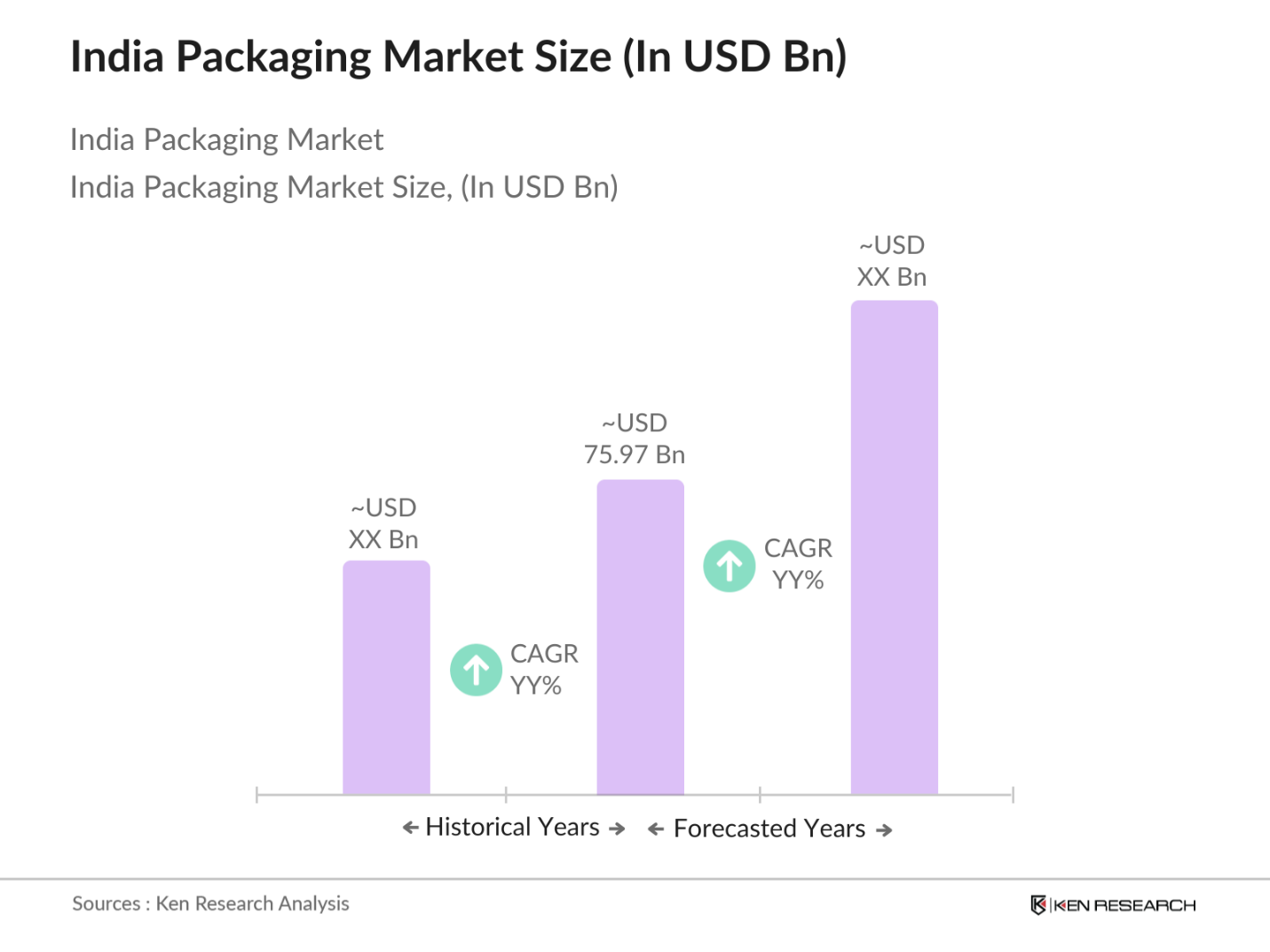

The India packaging market, valued at USD 75.97 billion units, is driven by the surge in e-commerce and packaged food demand, along with innovations in sustainable packaging materials.

Challenges include rising raw material costs, especially for plastic resins, and stricter environmental regulations that are pushing companies to innovate and adopt sustainable solutions.

Major players include Manjushree Technopack Ltd., Uflex Limited, Jindal Poly Films Ltd., and Berry Global Inc., which dominate due to their extensive production capacity and innovative packaging solutions.

The market is driven by increasing demand for packaged food and beverages, expansion of e-commerce, and consumer preferences for eco-friendly packaging.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.