India Photonics Integrated Circuits Market Outlook to 2030

Region:Asia

Author(s):Samanyu

Product Code:KROD4920

November 2024

93

About the Report

India Photonics Integrated Circuits Market Overview

- The India Photonics Integrated Circuits market is valued at USD 980 million, based on a five-year historical analysis. This growth is driven primarily by the increased demand for high-speed data transfer in telecommunications and data centers. With India being a hub for emerging technologies like 5G, PICs are being integrated into a variety of applications that require enhanced bandwidth and reduced energy consumption. Government initiatives, such as the National Photonics Mission, have further accelerated market growth by encouraging domestic production of photonic components.

- Cities like Bengaluru, Hyderabad, and Pune have become dominant in the Indian Photonics Integrated Circuits market due to their strong presence in the IT and technology sectors. These cities house numerous research institutions, high-tech companies, and innovation centers, which have led to higher adoption rates of photonic technologies. The presence of well-established semiconductor industries in these regions further strengthens their dominance in the photonics market, positioning them as key players.

- The integration of photonic integrated circuits with silicon technology represents a growing trend in Indias semiconductor sector, leveraging Indias existing electronics manufacturing infrastructure. Silicon photonics enables the integration of PICs into existing semiconductor devices, optimizing performance in telecommunication and data transmission applications. Indias semiconductor market is poised for significant growth, with the government committing $10 billion for developing semiconductor manufacturing facilities under the "Semicon India" program. The convergence of photonics with silicon technologies allows for enhanced data transfer speeds and energy efficiency, particularly as India continues to advance its 5G, data center, and AI sectors.

India Photonics Integrated Circuits Market Segmentation

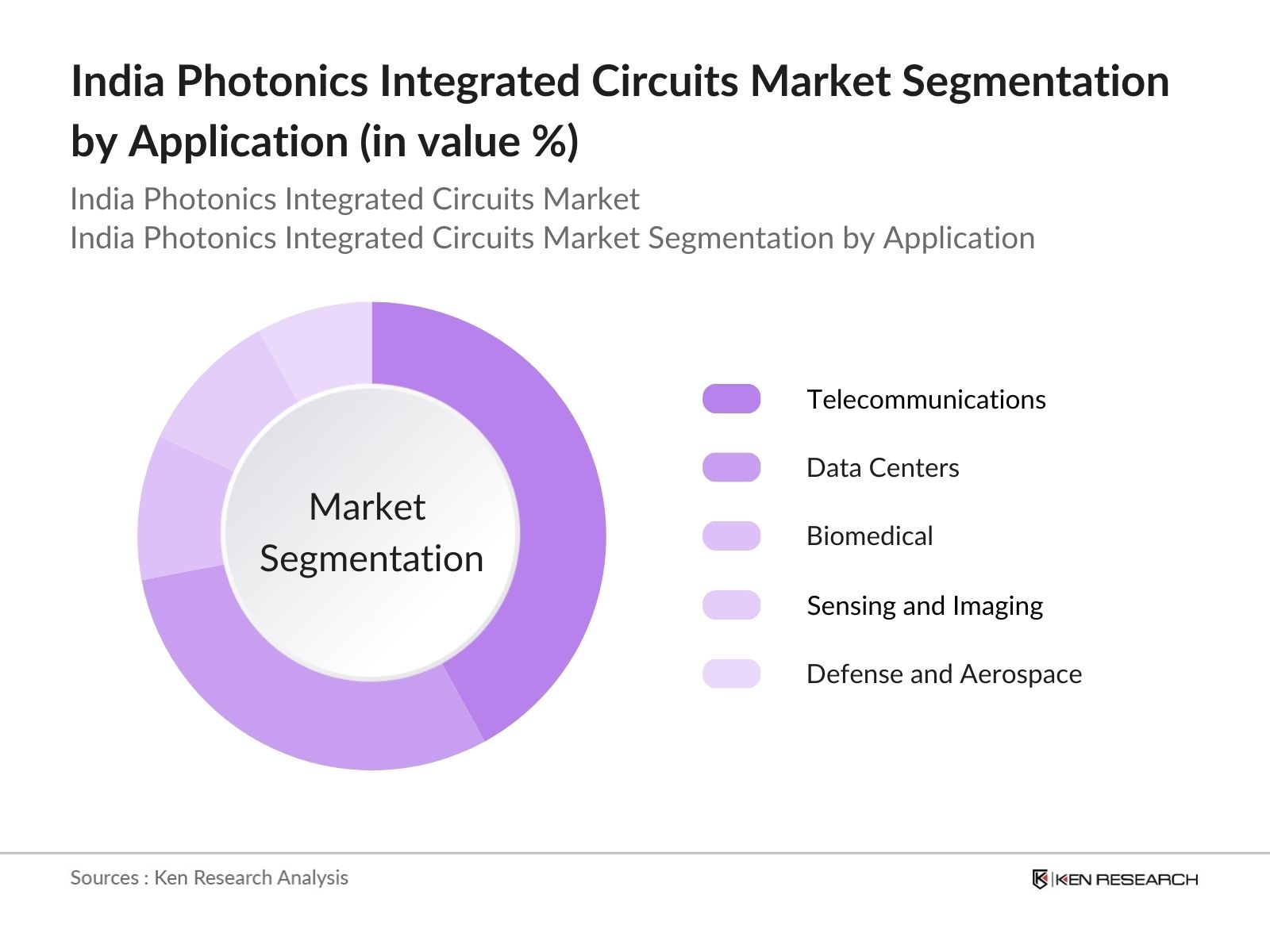

By Application: Market is segmented by application into telecommunications, data centers, biomedical, defense and aerospace, and sensing and imaging. Recently, telecommunications have a dominant market share under the application segment. This is driven by the need for higher bandwidth and energy efficiency as the country transitions towards 5G infrastructure. With growing internet usage, data consumption, and cloud storage requirements, telecommunications companies are increasingly adopting PICs to enhance their network capabilities and reduce energy costs.

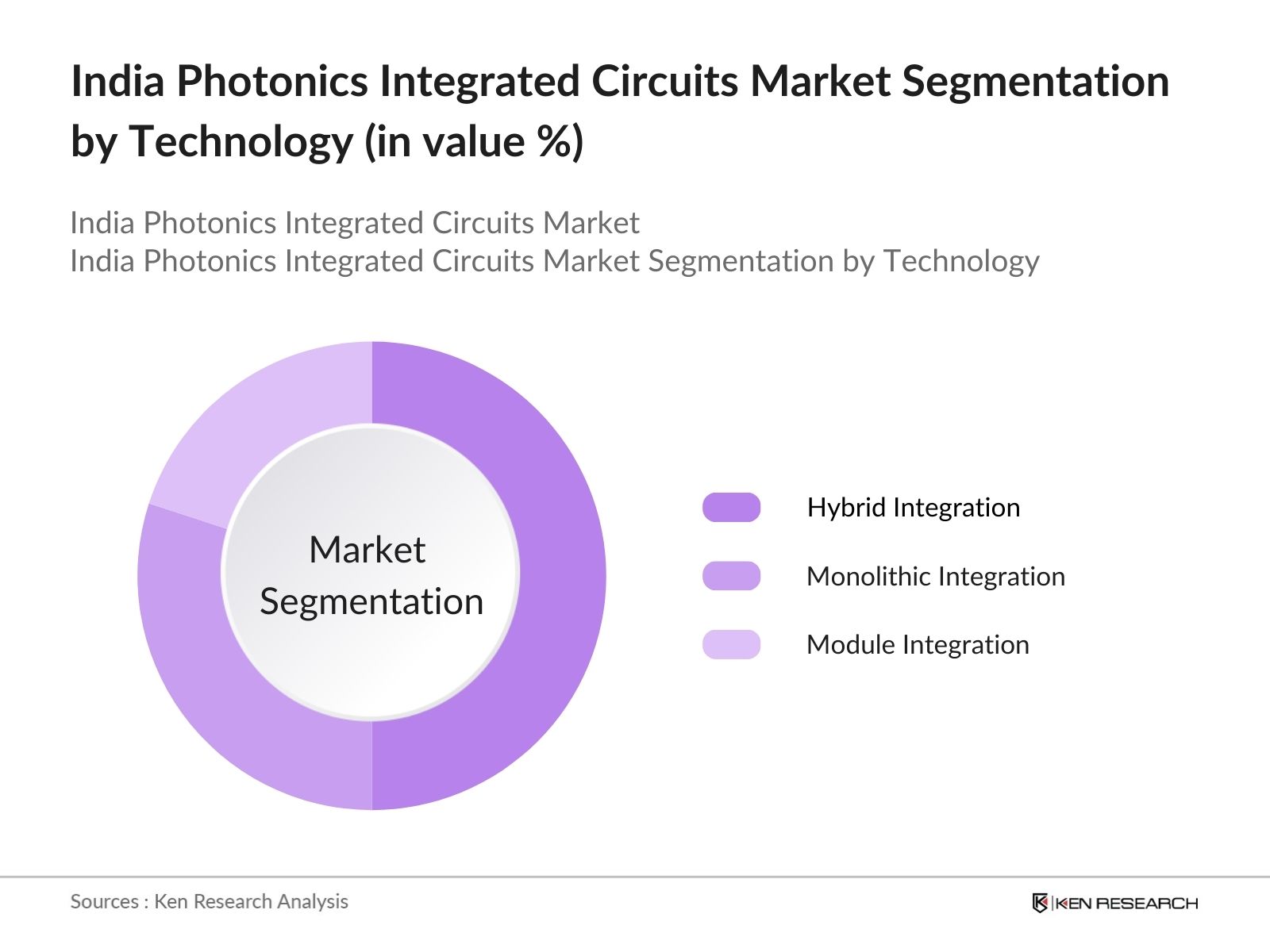

By Technology: Market is also segmented by technology into hybrid integration, monolithic integration, and module integration. Hybrid integration is leading the market share, as it allows for the combination of different materials and components in a single platform, enhancing performance and reducing costs. The flexibility and scalability of hybrid PICs have made them the preferred choice across various sectors, especially in high-speed data applications, making them essential in both telecommunications and data centers.

India Photonics Integrated Circuits Market Competitive Landscape

The India Photonics Integrated Circuits market is dominated by both domestic and global players, fostering a competitive landscape characterized by innovation and strategic partnerships. The presence of key global players like Intel Corporation and Cisco Systems, combined with local companies ability to offer custom solutions, positions this market for steady growth.

|

Company Name |

Establishment Year |

Headquarters |

Revenue (2023) |

Employees |

Key Technology |

R&D Investment |

Key Clients |

Partnerships |

|

Intel Corporation |

1968 |

California, USA |

||||||

|

Cisco Systems Inc. |

1984 |

California, USA |

||||||

|

NeoPhotonics Corporation |

1996 |

California, USA |

||||||

|

Infinera Corporation |

2000 |

California, USA |

||||||

|

Lumentum Holdings Inc. |

2015 |

California, USA |

India Photonics Integrated Circuits Industry Analysis

Growth Drivers

- Demand for High-Bandwidth Communication: India's rapid digitization has led to an unprecedented demand for high-bandwidth communication, driven by rising internet consumption and digital transformation across industries. As of 2023, India had over 925 million internet users, with daily data consumption surpassing 18 GB per user, supported by macroeconomic factors such as the countrys projected GDP growth of 6.3% for 2024 (World Bank). With growing reliance on cloud computing, IoT, and digital platforms, photonic integrated circuits (PICs) are essential for increasing bandwidth capacity in communication networks, providing faster data transfer with reduced energy consumption.

- Data Centers Expansion: Indias data center market has experienced rapid expansion due to the surge in demand for cloud services, e-commerce, and government digital initiatives. The country currently hosts over 138 operational data centers, according to industry estimates, and the number of facilities is expected to rise with Indias projected addition of 40 GW renewable energy by 2030 to support the energy needs of data centers (International Energy Agency). The increased use of photonic circuits in data centers improves data transmission efficiency, addressing the growing data storage demands. With GDP per capita nearing $2,500 in 2023, the rise of IT infrastructure continues to drive PIC adoption.

- 5G Infrastructure: India's ongoing 5G network rollout, initiated in 2022, has driven the demand for faster and more efficient data transmission technologies like PICs. As of 2024, more than 40,000 5G towers have been installed nationwide, with expectations for over 200,000 towers in the next two years, according to the Telecom Regulatory Authority of India (TRAI). PICs help manage the higher bandwidth and faster data rates required by 5G technology, improving overall network performance. Additionally, with Indias urban population expected to exceed 600 million by 2025, the 5G infrastructure relies heavily on advanced photonic technologies to support its robust growth.

Market Challenges

- Cost of Fabrication and Packaging: The cost of fabricating and packaging photonic integrated circuits remains a significant challenge in India due to the need for specialized manufacturing facilities and skilled labor. Indias limited semiconductor fabrication infrastructure hampers the mass production of PICs. With India importing nearly 94% of its semiconductor needs as of 2023 (Ministry of Electronics and IT), the absence of local production increases overall costs, as materials and equipment must be sourced internationally. Macroeconomic pressures, such as currency fluctuations and rising material costs due to global supply chain disruptions, also contribute to elevated fabrication expenses.

- Thermal Management Issues: Thermal management remains a critical challenge in deploying photonic integrated circuits, as PICs generate significant heat during operation. Indias climate adds to the complexity, with average temperatures exceeding 35C in many regions during peak summer months, which could affect the performance and longevity of PICs. The challenge is particularly pronounced in high-density data centers, where maintaining optimal temperature is crucial for preventing equipment failure. According to the India Meteorological Department, the average annual temperature has increased by 0.6C over the last two decades, exacerbating the need for efficient cooling solutions in PIC-powered systems.

India Photonics Integrated Circuits Market Future Outlook

Over the next five years, the India Photonics Integrated Circuits market is expected to witness significant growth driven by advancements in data communication technologies, the proliferation of 5G networks, and increasing government support for domestic manufacturing. As industries continue to demand faster, more efficient data transfer systems, PICs will play an integral role in shaping the future of India's digital infrastructure.

Future Market Opportunities

- Emergence of Quantum Computing: The rise of quantum computing presents a significant opportunity for Indias photonics industry. The National Quantum Mission, launched in 2023 with a budget of $780 million (Government of India), aims to advance quantum technology by leveraging photonic circuits for faster and more secure computations. Photonic integrated circuits play a critical role in quantum communication and computing by facilitating the transmission of quantum information with minimal loss. Indias ambitious target to develop quantum computers with 50100 qubits by 2031 relies heavily on innovations in photonics, which opens new avenues for PIC applications in research and technology sectors.

- LIDAR in Automotive: The Indian automotive industrys growing interest in autonomous driving and advanced driver-assistance systems (ADAS) has led to a rising demand for Light Detection and Ranging (LIDAR) technology, where photonic integrated circuits are instrumental. With over 4 million vehicles sold in India in 2023 (Society of Indian Automobile Manufacturers), the adoption of LIDAR-based solutions for safety and navigation is increasing. India's focus on electric vehicle (EV) development, supported by incentives under the Faster Adoption and Manufacturing of Electric Vehicles (FAME) initiative, further boosts the role of PICs in enhancing the performance of LIDAR systems, facilitating greater accuracy and speed in distance measurement.

Scope of the Report

|

By Component |

Lasers Modulators Detectors Multiplexers/Demultiplexers Attenuators |

|

By Application |

Telecommunications Data Centers Biomedical Defense and Aerospace Sensing and Imaging |

|

By Technology |

Hybrid Integration Monolithic Integration Module Integration |

|

By Material Type |

Indium Phosphide (InP) Silicon Photonics (SiPh) Gallium Arsenide (GaAs) Lithium Niobate (LiNbO3) |

|

By Region |

North India South India East India West India |

Products

Key Target Audience

Telecommunications Companies

Data Center Operators

Semiconductor Manufacturers

Photonics Research Institutes

Government and Regulatory Bodies (Ministry of Electronics and Information Technology, Telecom Regulatory Authority of India)

Defense and Aerospace Contractors

Venture Capital Firms and Investors

Medical Device Manufacturers

Companies

Major Players

Intel Corporation

Cisco Systems Inc.

NeoPhotonics Corporation

Infinera Corporation

Lumentum Holdings Inc.

Broadcom Inc.

Fujitsu Optical Components Limited

II-VI Incorporated

Mellanox Technologies (NVIDIA)

GlobalFoundries

Anello Photonics

Rockley Photonics

MACOM Technology Solutions

Aurrion (Juniper Networks)

Ciena Corporation

Table of Contents

1. India Photonics Integrated Circuits Market Overview

1.1. Definition and Scope (Photonics-based Technologies and Applications)

1.2. Market Taxonomy (Semiconductor and Optoelectronics Classification)

1.3. Market Growth Rate (Key Growth Indicators in Photonics)

1.4. Market Segmentation Overview (Application, End-Use, Technology, Region)

2. India Photonics Integrated Circuits Market Size (In USD Mn)

2.1. Historical Market Size (Photonics Industry Performance)

2.2. Key Market Milestones (Technological Innovations and Government Initiatives)

2.3. Year-On-Year Growth Analysis (Growth Trajectories of Photonics Integrated Circuits)

3. India Photonics Integrated Circuits Market Analysis

3.1. Growth Drivers

3.1.1 Demand for High-Bandwidth Communication

3.1.2 Data Centers

3.1.3 5G Infrastructure

3.2. Restraints

3.2.1 Cost of Fabrication and Packaging

3.2.2 Thermal Management Issues

3.3. Opportunities

3.3.1 Emergence of Quantum Computing

3.3.2 LIDAR in Automotive

3.4. Trends

3.4.1 Miniaturization of Photonic Devices

3.4.2 Integration with Silicon Technology

3.5. Government Regulation

3.5.1 Make in India Initiative

3.5.2 National Photonics Mission

3.5.3 Policy Incentives for Semiconductors

3.6. Competitive Ecosystem (Photonics Ecosystem in India)

3.7. Porters Five Forces (Bargaining Power, Competitive Rivalry, and Substitution Threats)

3.8. Value Chain Analysis (From Photonic Materials to End-Use Applications)

4. India Photonics Integrated Circuits Market Segmentation

4.1. By Component (In Value %)

4.1.1. Lasers

4.1.2. Modulators

4.1.3. Detectors

4.1.4. Multiplexers/Demultiplexers

4.1.5. Attenuators

4.2. By Application (In Value %)

4.2.1. Telecommunications

4.2.2. Data Centers

4.2.3. Biomedical

4.2.4. Defense and Aerospace

4.2.5. Sensing and Imaging

4.3. By Technology (In Value %)

4.3.1. Hybrid Integration

4.3.2. Monolithic Integration

4.3.3. Module Integration

4.4. By Material Type (In Value %)

4.4.1. Indium Phosphide (InP)

4.4.2. Silicon Photonics (SiPh)

4.4.3. Gallium Arsenide (GaAs)

4.4.4. Lithium Niobate (LiNbO3)

4.5. By Region (In Value %)

4.5.1. North India

4.5.2. South India

4.5.3. East India

4.5.4. West India

5. India Photonics Integrated Circuits Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. Intel Corporation

5.1.2. Cisco Systems Inc.

5.1.3. NeoPhotonics Corporation

5.1.4. Broadcom Inc.

5.1.5. Infinera Corporation

5.1.6. Fujitsu Optical Components Limited

5.1.7. II-VI Incorporated

5.1.8. Lumentum Holdings Inc.

5.1.9. MACOM Technology Solutions Holdings

5.1.10. Mellanox Technologies (NVIDIA)

5.1.11. GlobalFoundries

5.1.12. Aurrion (Juniper Networks)

5.1.13. Anello Photonics

5.1.14. Ciena Corporation

5.1.15. Rockley Photonics

5.2. Cross Comparison Parameters (Technology Integration, R&D Expenditure, Patent Portfolio, Market Presence, Global vs Domestic Reach, Revenue)

5.3. Market Share Analysis (Key Competitors and Regional Market Share)

5.4. Strategic Initiatives (Collaborations, Partnerships, and R&D Investments)

5.5. Mergers and Acquisitions (Market Consolidation Trends in Photonics)

5.6. Investment Analysis (Private Equity and Venture Capital Involvement)

5.7. Government Grants (Subsidies and Financial Incentives)

5.8. Industry Roadmap (Key Market Milestones for the Next 5 Years)

6. India Photonics Integrated Circuits Market Regulatory Framework

6.1. Compliance Requirements (Fabrication and Design Standards)

6.2. Certification Processes (ISO, IEC Standards)

6.3. Environmental Standards (Sustainability in Manufacturing Processes)

7. India Photonics Integrated Circuits Future Market Size (In USD Mn)

7.1. Future Market Size Projections (Opportunities in Next-Gen Photonics Technologies)

7.2. Key Factors Driving Future Market Growth (5G, Data Explosion, Autonomous Vehicles)

8. India Photonics Integrated Circuits Future Market Segmentation

8.1. By Component (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By Material Type (In Value %)

8.5. By Region (In Value %)

9. India Photonics Integrated Circuits Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis (Market Potential Assessment)

9.2. Customer Cohort Analysis (Target Segments and Use Cases)

9.3. Marketing Initiatives (Strategies for Market Penetration)

9.4. White Space Opportunity Analysis (Emerging Trends in Photonics Integration)

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The first phase involves identifying all major stakeholders within the India Photonics Integrated Circuits market. Desk research from secondary databases and proprietary resources is employed to gather relevant industry data. This step aims to define critical variables that drive the market, such as demand in telecommunications and data centers.

Step 2: Market Analysis and Construction

In this step, historical data related to the market is compiled, including the adoption rates of photonics technology and revenue generated by key players. Detailed analysis of these trends helps build a comprehensive picture of the markets current state and its future trajectory.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through expert consultations using CATIs. Experts provide insights into the operational challenges and opportunities in the market, ensuring the reliability of the data collected in earlier phases.

Step 4: Research Synthesis and Final Output

The final step involves synthesizing all research findings and creating a comprehensive report. Detailed insights from PIC manufacturers and key players are incorporated to ensure a well-rounded analysis of the market.

Frequently Asked Questions

01. How big is the India Photonics Integrated Circuits Market?

The India Photonics Integrated Circuits market is valued at USD 980 Mn, driven by the rapid adoption of PICs in data communication, telecommunications, and defense sectors.

02. What are the challenges in the India Photonics Integrated Circuits Market?

Challenges in India Photonics Integrated Circuits market include the high cost of photonic components, issues with heat dissipation, and the complexity of integration with existing systems, particularly in data centers and telecommunication networks.

03. Who are the major players in the India Photonics Integrated Circuits Market?

Key players in India Photonics Integrated Circuits market include Intel Corporation, Cisco Systems Inc., NeoPhotonics Corporation, Infinera Corporation, and Lumentum Holdings Inc., who dominate due to their technological innovation and extensive patent portfolios.

04. What are the growth drivers of the India Photonics Integrated Circuits Market?

Growth drivers in India Photonics Integrated Circuits market include increased demand for high-bandwidth communication, the rise of 5G networks, and government initiatives such as the National Photonics Mission, which aims to boost domestic production of photonic components.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.