India Pipe Market Outlook to 2030

Region:Asia

Author(s):Shubham Kashyap

Product Code:KROD724

April 2025

80

About the Report

India Pipe Market Overview

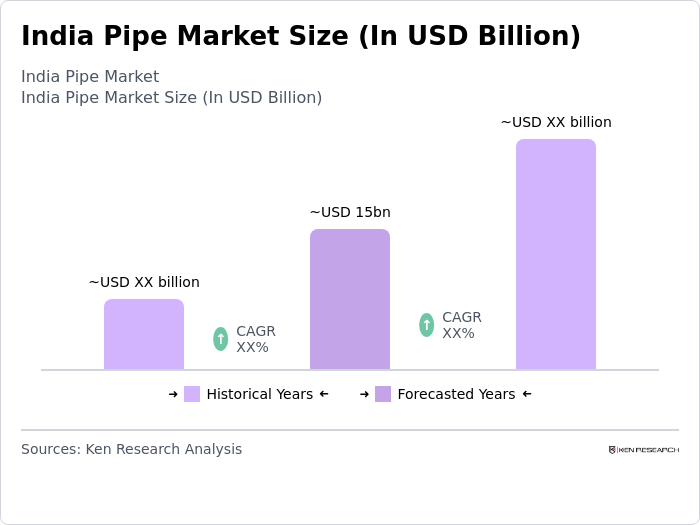

The India Pipe Market is valued at USD 15 billion, based on a five-year historical analysis. This market size is driven by rapid urbanization and infrastructure development across the country. The increasing demand for residential and commercial construction projects has significantly contributed to the growth of the pipe market. Additionally, government initiatives to improve water supply and sanitation infrastructure have further fueled the demand for pipes in various sectors.

In the India Pipe Market, major cities such as Mumbai, Delhi, and Bangalore dominate due to their extensive urban development and industrial activities. These cities have a high demand for pipes in construction, water supply, and sewage systems, making them key players in the market. The presence of numerous construction projects and industrial zones in these cities further strengthens their dominance in the pipe market.

The Indian government has implemented the National Infrastructure Pipeline (NIP) initiative, which aims to invest in infrastructure projects across the country. This regulation has significantly impacted the pipe market by increasing the demand for pipes in various infrastructure projects, including water supply, sanitation, and transportation. The NIP initiative emphasizes the development of sustainable and efficient infrastructure, thereby driving the growth of the pipe market in India.

India Pipe Market Segmentation

By Material Type: The market is segmented by material type into PVC, HDPE, and steel pipes. PVC pipes hold a dominant position due to their cost-effectiveness and versatility in various applications, including water supply, sewage, and irrigation systems. The lightweight nature and easy installation of PVC pipes make them a preferred choice for construction projects. Additionally, the increasing focus on sustainable and eco-friendly materials has further boosted the demand for PVC pipes in the market.

By Application: The market is segmented by application into water supply, sewage, and oil & gas. Water supply applications dominate the market due to the increasing demand for efficient and reliable water distribution systems. The government's focus on improving water supply infrastructure and ensuring access to clean water for all citizens has significantly contributed to the growth of this segment. Additionally, the rising population and urbanization have further increased the demand for water supply pipes in residential and commercial sectors.

India Pipe Market Competitive Landscape

The India Pipe Market is dominated by a few major players, including local manufacturers and global brands. This consolidation highlights the significant influence of these key companies in shaping the market dynamics. The competitive landscape is characterized by strategic partnerships, mergers, and acquisitions, which have enabled companies to expand their market presence and enhance their product offerings.

India Pipe Market Analysis

Growth Drivers

- Infrastructure Development: India's infrastructure sector is a key driver for the pipe market, with the government investing heavily in projects like the Bharatmala and Sagarmala initiatives. According to the World Bank, India's infrastructure investment is projected to reach $1.5 trillion by 2024, significantly boosting demand for pipes in construction and transportation sectors. The expansion of highways, ports, and urban infrastructure necessitates extensive use of pipes for water supply, sewage, and drainage systems, thereby propelling market growth. This infrastructure boom is expected to create substantial opportunities for pipe manufacturers and suppliers.

- Government Initiatives and Policies: The Indian government's focus on improving water supply and sanitation through programs like the Jal Jeevan Mission is a major growth driver for the pipe market. The mission aims to provide piped water to every rural household by 2024, requiring extensive use of pipes. The World Bank reports that India has allocated over $50 billion for water supply and sanitation projects, which will drive demand for pipes across various materials and applications. These initiatives not only enhance public health but also stimulate the pipe manufacturing industry, creating a robust market environment.

- Urbanization and Industrialization: Rapid urbanization and industrialization in India are fueling the demand for pipes in residential, commercial, and industrial sectors. The United Nations projects that India's urban population will reach 600 million by 2031, necessitating significant infrastructure development. This urban expansion requires efficient water supply, sewage, and industrial piping systems, driving the pipe market. Additionally, the growth of industries such as oil and gas, agriculture, and manufacturing further boosts demand for specialized pipes, creating a dynamic market landscape with diverse opportunities for growth and innovation.

Market Restraints

- Fluctuating Raw Material Prices: The pipe market in India faces challenges due to the volatility of raw material prices, particularly for materials like steel and PVC. According to the International Monetary Fund, global steel prices have experienced fluctuations due to supply chain disruptions and geopolitical tensions. These price variations impact the cost of production for pipe manufacturers, affecting their profit margins and pricing strategies. The uncertainty in raw material costs poses a significant challenge for the industry, requiring manufacturers to adopt efficient procurement and cost management strategies to remain competitive.

- Environmental Concerns: Environmental regulations and concerns regarding the sustainability of materials used in pipe manufacturing present challenges for the industry. The increasing focus on reducing plastic waste and promoting eco-friendly alternatives affects the demand for traditional PVC pipes. The World Bank emphasizes the need for sustainable development practices, urging industries to adopt greener technologies. This shift towards sustainable materials requires significant investment in research and development, posing a challenge for manufacturers to balance environmental compliance with cost-effectiveness and market demand.

India Pipe Market Future Outlook

Over the next five years, the India pipe market is poised for substantial growth, driven by government initiatives, urbanization, and technological advancements. The focus on infrastructure development and water supply projects will continue to boost demand for pipes across various sectors. Additionally, the adoption of sustainable materials and innovative technologies will shape the market's future, aligning with global environmental goals. The market is expected to witness increased investments in research and development, fostering innovation and competitiveness among manufacturers.

Market Opportunities

- Expansion in Rural Water Supply: The Indian government's commitment to improving rural water supply through initiatives like the Jal Jeevan Mission presents significant opportunities for the pipe market. With a target to provide piped water to every rural household by 2024, the demand for pipes in rural areas is set to increase substantially. This expansion not only enhances public health and quality of life but also creates a lucrative market for pipe manufacturers, particularly those specializing in cost-effective and durable materials suitable for rural infrastructure.

- Smart City Projects: The development of smart cities in India offers a promising opportunity for the pipe market. The government's Smart Cities Mission aims to create sustainable and efficient urban environments, requiring advanced piping systems for water management, sewage, and industrial applications. According to the World Bank, India's urban population is expected to grow significantly, driving the need for smart infrastructure solutions. Pipe manufacturers can capitalize on this trend by providing innovative products that meet the demands of modern urban planning and development.

Scope of the Report

| By Material Type |

PVC HDPE Steel |

| By Application |

Water Supply Sewage & Drainage Oil & Gas |

| By End-User |

Residential Commercial Industrial |

| By Diameter |

Small Diameter Medium Diameter Large Diameter |

| By Region |

North India South India East India West India |

Products

Key Target Audience

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., Bureau of Indian Standards, Ministry of Commerce and Industry)

Pipe Manufacturers and Producers

Construction and Infrastructure Companies

Water Supply and Sewage Management Authorities

Oil and Gas Companies

Industrial Equipment Suppliers

Financial Institutions and Banks

Companies

Players Mentioned in the Report:

Jindal SAW Ltd.

Astral Poly Technik Ltd

Finolex Industries Ltd.

Supreme Industries Ltd.

Prince Pipes and Fittings Ltd.

Tata Steel Ltd.

Welspun Corp Ltd.

APL Apollo Tubes Ltd.

Hindustan Zinc Ltd.

Man Industries Ltd.

Table of Contents

1. India Pipe Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. India Pipe Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. India Pipe Market Analysis

3.1. Growth Drivers

3.1.1. Infrastructure Development

3.1.2. Government Initiatives and Policies

3.1.3. Urbanization and Industrialization

3.1.4. Technological Advancements in Pipe Manufacturing

3.2. Restraints

3.2.1. Fluctuating Raw Material Prices

3.2.2. Environmental Concerns

3.3. Opportunities

3.3.1. Expansion in Rural Water Supply

3.3.2. Smart City Projects

3.3.3. Export Opportunities

3.4. Trends

3.4.1. Adoption of Sustainable Materials

3.4.2. Increasing Use of Composite Pipes

3.5. SWOT Analysis

3.6. Porters Five Forces

3.7. Competition Ecosystem

4. India Pipe Market Segmentation

4.1. By Material Type

4.1.1. PVC

4.1.2. HDPE

4.1.3. Steel

4.2. By Application

4.2.1. Water Supply

4.2.2. Sewage & Drainage

4.2.3. Oil & Gas

4.3. By End-User

4.3.1. Residential

4.3.2. Commercial

4.3.3. Industrial

4.4. By Region

4.4.1. North

4.4.2. South

4.4.3. East

4.4.4. West

4.5. By Diameter

4.5.1. Small Diameter

4.5.2. Medium Diameter

4.5.3. Large Diameter

5. India Pipe Market Competitive Landscape

5.1. Detailed Profiles of Major Companies

5.1.1. Finolex Industries Ltd.

5.1.2. Astral Poly Technik Ltd.

5.1.3. Finolex Industries Ltd.

5.1.4. Supreme Industries Ltd.

5.1.5. Prince Pipes and Fittings Ltd.

5.1.6. Tata Steel Ltd.

5.1.7. Welspun Corp Ltd.

5.1.8. APL Apollo Tubes Ltd.

5.1.9. Hindustan Zinc Ltd.

5.1.10. Man Industries Ltd.

5.2. Cross Comparison Parameters

5.2.1. Revenue

5.2.2. Market Share

5.2.3. Product Portfolio

5.2.4. Distribution Network

5.2.5. Brand Recognition

5.2.6. Sustainability Initiatives

5.2.7. Technological Innovation

5.2.8. Customer Satisfaction

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investors Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. India Pipe Market Regulatory Framework

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

7. India Pipe Market Future Segmentation

7.1. By Material Type (In Value %)

7.1.1. PVC

7.1.2. HDPE

7.1.3. Steel

7.2. By Application (In Value %)

7.2.1. Water Supply

7.2.2. Sewage & Drainage

7.2.3. Oil & Gas

7.3. By End-User (In Value %)

7.3.1. Residential

7.3.2. Commercial

7.3.3. Industrial

7.4. By Region (In Value %)

7.4.1. North

7.4.2. South

7.4.3. East

7.4.4. West

7.5. By Diameter (In Value %)

7.5.1. Small Diameter

7.5.2. Medium Diameter

7.5.3. Large Diameter

8. Analysts Recommendations

8.1. TAM/SAM/SOM Analysis

8.2. Customer Cohort Analysis

8.3. Marketing Initiatives

8.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the India Pipe Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we will compile and analyze historical data pertaining to the India Pipe Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the India Pipe Market.

Frequently Asked Questions

01. How big is the India Pipe market?

The India Pipe market is valued at USD 15 billion, driven by factors such as increasing demand, technological advancements, and supportive government initiatives.

02. What are the key challenges in the India Pipe market?

Key challenges in the India Pipe market include intense competition, regulatory complexities, and infrastructure limitations affecting market dynamics.

03. Who are the major players in the India Pipe market?

Major players in the India Pipe market include Jindal SAW Ltd., Tata Steel Ltd., Welspun Corp Ltd., Astral Pipes, Finolex Industries Ltd., among others.

04. What are the growth drivers for the India Pipe market?

The primary growth drivers for the India Pipe market are increasing consumer demand, favorable policies, innovation, and substantial investment inflows.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.