India Plastic Additives Market Outlook to 2030

Region:India

Author(s):Meenakshi Bisht

Product Code:KROD2609

Region:India

Author(s):Meenakshi Bisht

Product Code:KROD2609

December 2024

92

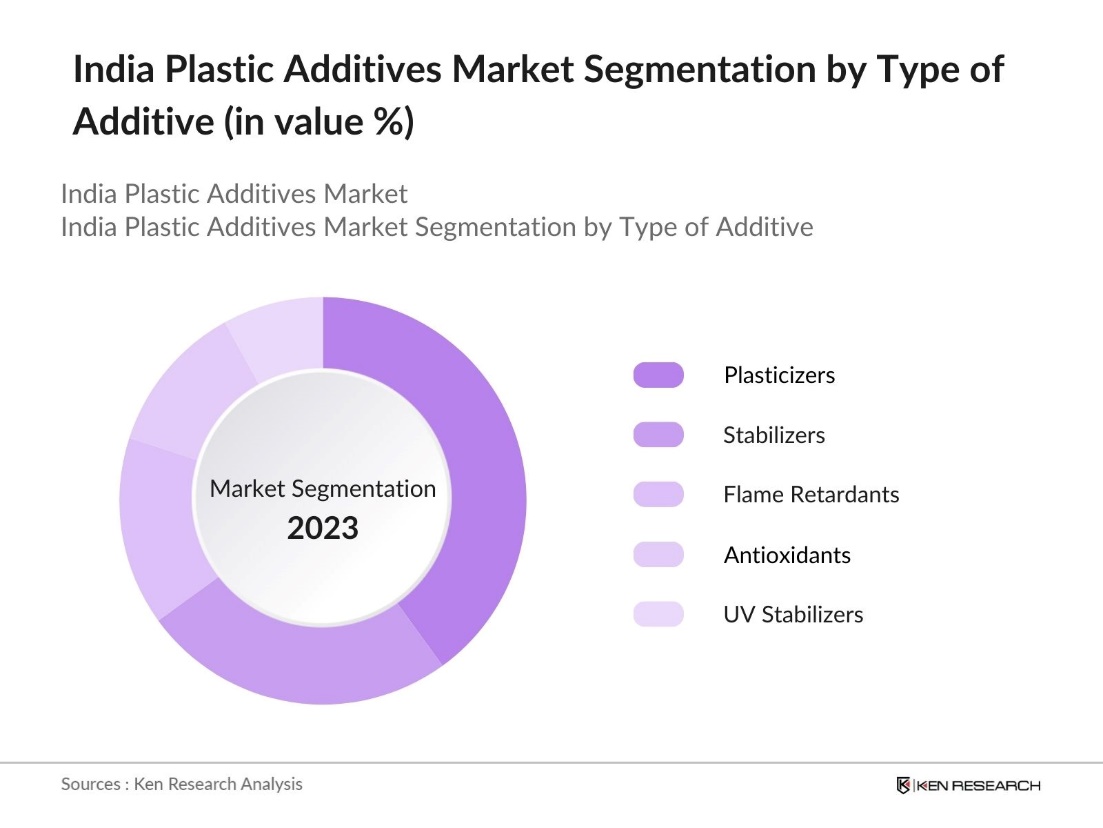

By Type of Additive: The India Plastic Additives market is segmented by type of additive into plasticizers, stabilizers, flame retardants, antioxidants, and UV stabilizers. Among these, plasticizers hold a dominant share due to their extensive use in flexible PVC applications. Plasticizers are essential in increasing the flexibility, durability, and longevity of plastic products, making them integral for products like cables, films, and sheets. The demand from the construction and automotive sectors further strengthens their dominance, especially in producing pipes and wiring materials that require enhanced flexibility.

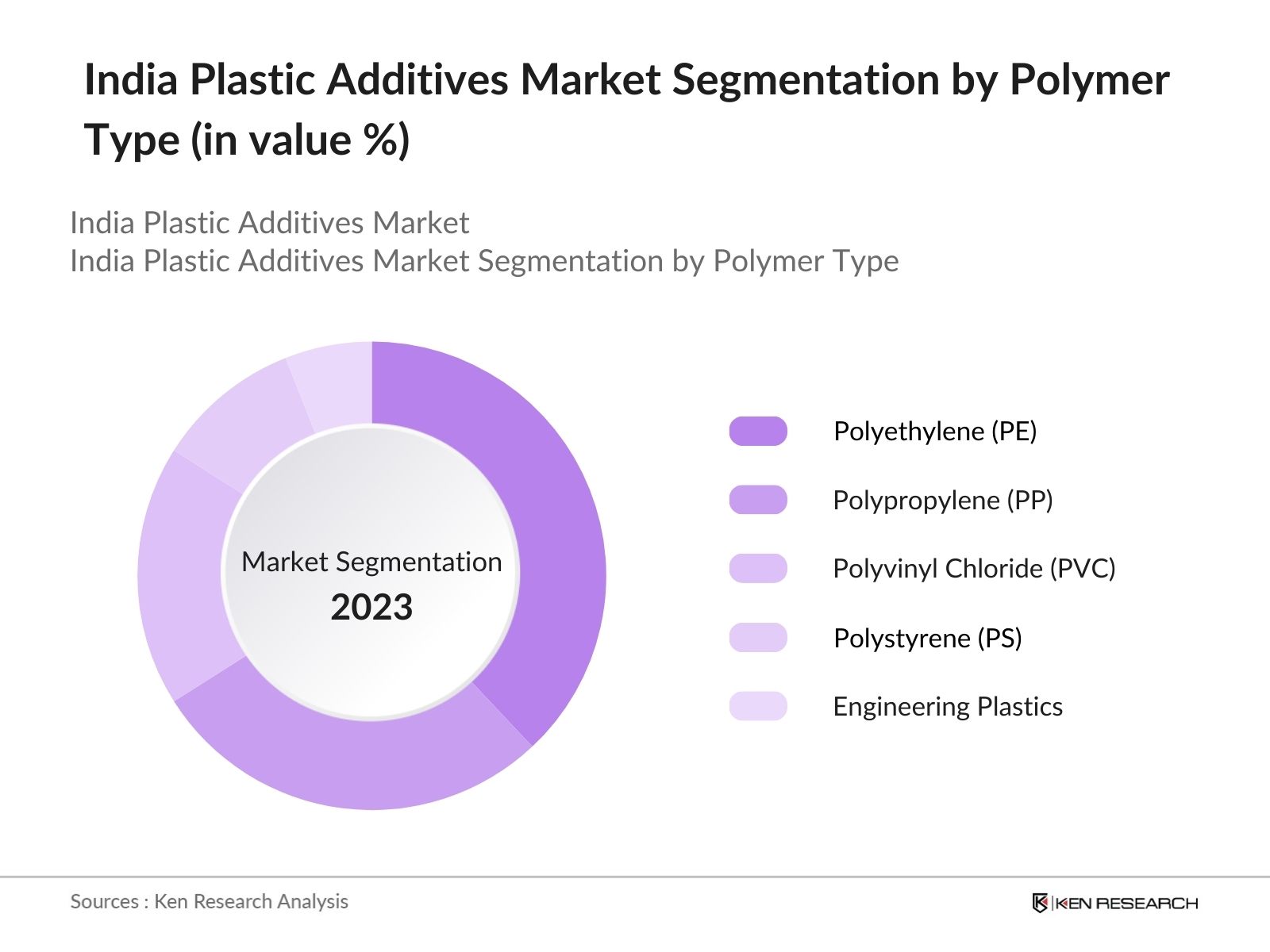

By Polymer Type: The market is segmented by polymer type into polyethylene (PE), polypropylene (PP), polyvinyl chloride (PVC), polystyrene (PS), and engineering plastics. Polyethylene holds the largest market share due to its widespread use in packaging materials, especially in the food and beverage industry. PE's lightweight and versatile properties, coupled with its cost-effectiveness, make it the preferred choice for flexible and rigid packaging solutions, including plastic bags, bottles, and containers, driving its demand in the plastic additives market.

The India Plastic Additives market is characterized by a few key players who dominate the market, leveraging their extensive production capabilities, innovative product offerings, and strong distribution networks. The presence of global giants such as BASF SE and Clariant AG further strengthens the competitive environment. Companies are focusing on sustainability initiatives and investments in R&D to offer eco-friendly additive solutions to comply with rising environmental regulations.

|

Company |

Establishment Year |

Headquarters |

No. of Employees |

R&D Investment |

Product Portfolio |

Revenue (2023) |

Sustainability Initiatives |

Global Presence |

Market Strategy |

|

BASF SE |

1865 |

Ludwigshafen, Germany |

|||||||

|

Clariant AG |

1995 |

Muttenz, Switzerland |

|||||||

|

Evonik Industries AG |

2007 |

Essen, Germany |

|||||||

|

LANXESS |

2004 |

Cologne, Germany |

|||||||

|

Dow Chemical Company |

1897 |

Midland, Michigan |

Over the next five years, the India Plastic Additives market is poised for significant growth driven by rising demand from key industries like packaging, automotive, and construction. The shift towards bio-based and environmentally friendly plastic additives, in response to stricter environmental regulations, will also fuel market expansion. Additionally, the growing investment in R&D to create high-performance additives will enhance product quality and open new market opportunities.

|

Type of Additive |

Plasticizers Stabilizers Flame Retardants Antioxidants UV Stabilizers |

|

Polymer Type |

Polyethylene Polypropylene Polyvinyl Chloride Polystyrene Engineering Plastics |

|

End-use Industry |

Packaging Automotive Building and Construction Electrical and Electronics Consumer Goods |

|

Functionality |

UV Protection Flexibility Improvement Anti-aging Heat Resistance |

|

Region |

North South West East |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Demand from Packaging Industry

3.1.2. Growth in Automotive Manufacturing

3.1.3. Rising Use in Construction Sector

3.1.4. Government Initiatives for Sustainable Plastic Use

3.2. Market Restraints

3.2.1. Fluctuating Raw Material Prices

3.2.2. Stringent Environmental Regulations

3.2.3. High Manufacturing Costs for Bio-based Additives

3.3. Opportunities

3.3.1. Technological Advancements in Additive Manufacturing

3.3.2. Increasing Preference for Bio-based Additives

3.3.3. Export Opportunities to Neighboring Markets

3.4. Trends

3.4.1. Shift Towards Eco-friendly and Sustainable Additives

3.4.2. Increased Investment in R&D for High-performance Additives

3.4.3. Rising Demand for Additives in Recycled Plastics

3.5. Government Regulation

3.5.1. Plastic Waste Management Rules

3.5.2. BIS Standards for Plastic Additives

3.5.3. Environmental Impact Assessments

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Type of Additive (In Value %)

4.1.1. Plasticizers

4.1.2. Stabilizers

4.1.3. Flame Retardants

4.1.4. Antioxidants

4.1.5. UV Stabilizers

4.2. By Polymer Type (In Value %)

4.2.1. Polyethylene (PE)

4.2.2. Polypropylene (PP)

4.2.3. Polyvinyl Chloride (PVC)

4.2.4. Polystyrene (PS)

4.2.5. Engineering Plastics

4.3. By End-use Industry (In Value %)

4.3.1. Packaging

4.3.2. Automotive

4.3.3. Building and Construction

4.3.4. Electrical and Electronics

4.3.5. Consumer Goods

4.4. By Functionality (In Value %)

4.4.1. UV Protection

4.4.2. Flexibility Improvement

4.4.3. Anti-aging

4.4.4. Heat Resistance

4.5. By Region (In Value %)

4.5.1. North

4.5.2. South

4.5.3. West

4.5.4. East

5.1. Detailed Profiles of Major Companies

5.1.1. BASF SE

5.1.2. Clariant AG

5.1.3. LANXESS

5.1.4. Evonik Industries AG

5.1.5. Croda International Plc

5.1.6. Dow Chemical Company

5.1.7. Adeka Corporation

5.1.8. Solvay

5.1.9. Songwon Industrial Co. Ltd.

5.1.10. Kaneka Corporation

5.1.11. Baerlocher GmbH

5.1.12. AkzoNobel N.V.

5.1.13. Milliken & Company

5.1.14. Lubrizol Corporation

5.1.15. Mitsubishi Chemical Holdings Corporation

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Product Portfolio, R&D Investment, Global Presence, Sustainability Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Additive Type (In Value %)

8.2. By Polymer Type (In Value %)

8.3. By End-use Industry (In Value %)

8.4. By Functionality (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase involves identifying major stakeholders within the India Plastic Additives market through desk research, industry reports, and secondary databases. The primary objective is to outline the critical factors influencing market dynamics, including environmental regulations, industry demand drivers, and technological innovations.

During this phase, historical market data is collected and analyzed to assess growth trends, industry penetration rates, and overall market performance. The analysis includes the relationship between additives and polymer production and a thorough evaluation of market drivers across different segments.

The hypotheses developed are validated through interviews with industry experts and manufacturers. Consultations are carried out via CATIS to obtain operational and financial insights that directly correlate with market trends and projections.

The final stage synthesizes all data, leveraging bottom-up and top-down approaches. This includes comprehensive analysis on product segments, consumer preferences, and distribution networks. The final report is compiled after validating the research findings with real-time industry data.

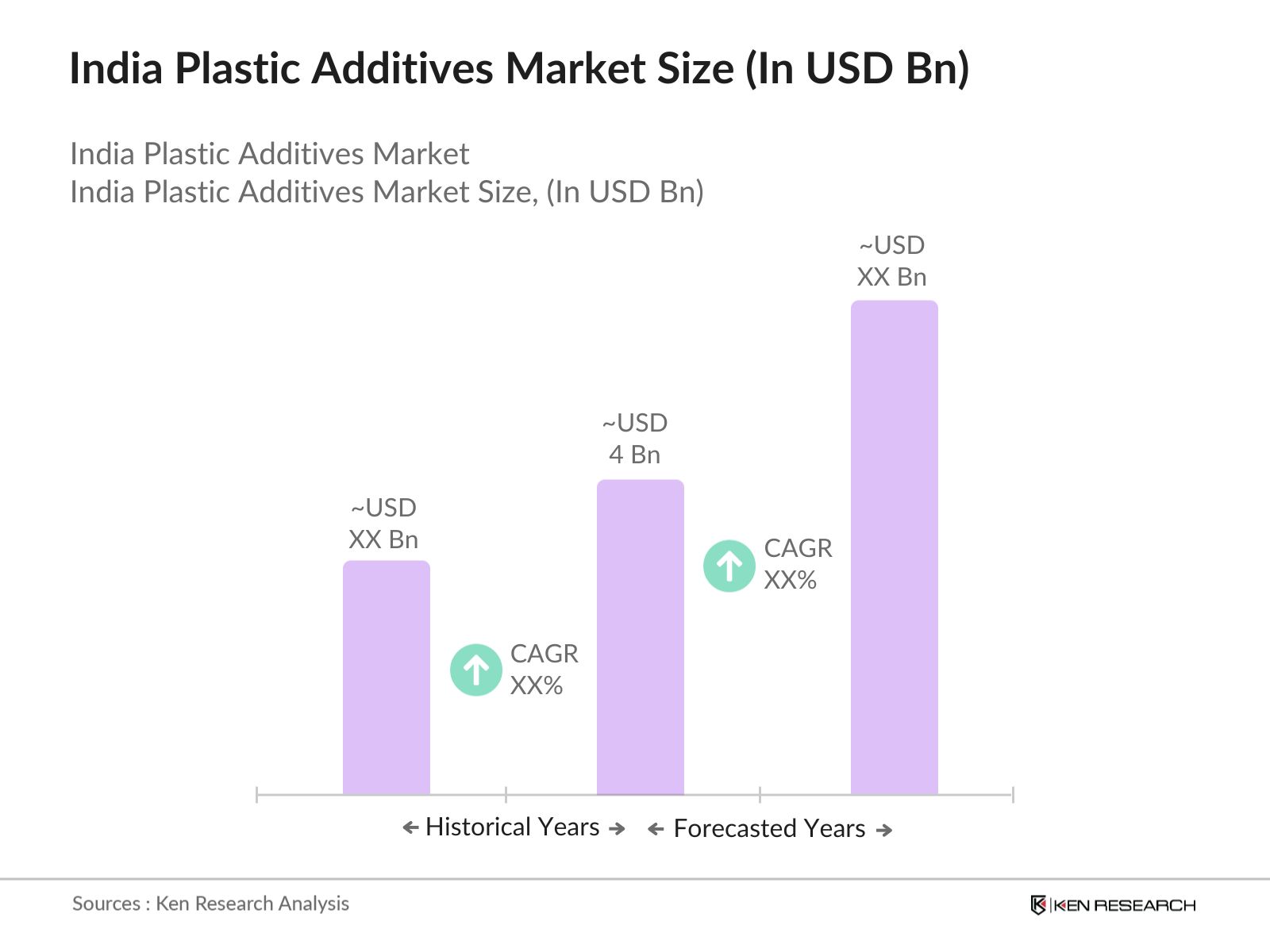

The India Plastic Additives Market is valued at USD 4 billion, driven by the increasing demand from industries such as packaging, automotive, and construction.

Challenges in the India Plastic Additives Market include stringent environmental regulations, fluctuating raw material prices, and the high costs associated with manufacturing bio-based additives.

Key players in the India Plastic Additives Market include BASF SE, Clariant AG, Evonik Industries AG, Dow Chemical Company, and LANXESS, all of which have a strong global presence and a focus on sustainable products.

The India Plastic Additives Market is propelled by increasing demand from the packaging and automotive industries, growing awareness of sustainable products, and government regulations supporting eco-friendly solutions.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.